Hi Vonasi,

Thanks for the feedback. I am not sure to follow you, do you mean to just exit everyday at 21:00? If that is what you mean I think is normal that the result is not good, IMHO that goes against the logic of the system.

I added two exits:

- the first one anyday at 21:00 if the positionperf>0 and barindex-tradeindex>70. I wanted to reduce the time in market and take quick profits after several days without reaching the limit exit order. This one make the result of the system better but without it, still is a good result.

- Another one is with positionperf<0 and other conditions, but doesn´t matter because it almost don´t act, you can take it out and won´t change much.

But IMHO if you just put to exit EVERYDAY at 21:00 you won´t let the logic of the system to work properly, because often it needs several days to get to the exit´s limit price of the original system. If you put the same condition in the original system I think it won´t work also.

I would like to hear also the opinion of the creator of the system (Coscar) about all this

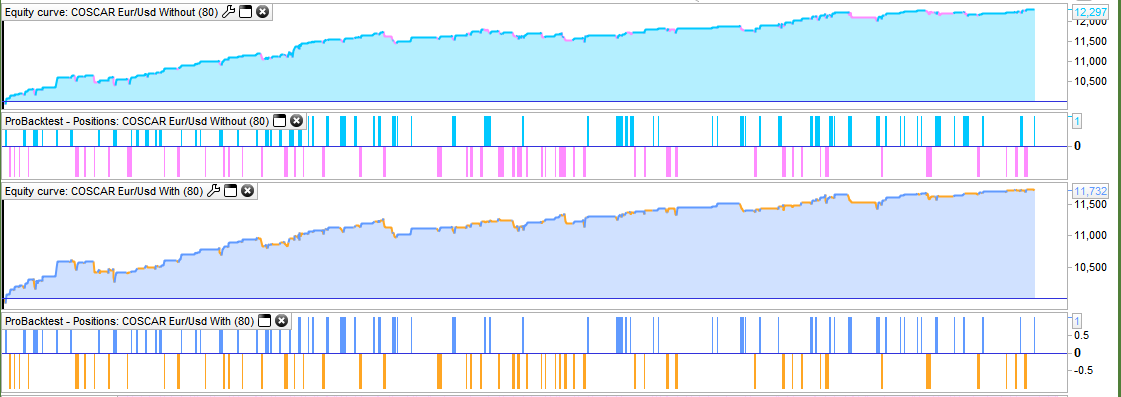

Sorry TempusFugit but I just realised that I read through your code rather quickly and misread it. I was working under the illusion that the conditions were all separate exit conditions whereas they are actually all combined as one

I’m still not sure that they add anything to the strategy of much worth. In my 100k bar test the LOSSEXIT condition was only ever met once. The WINEXIT condition was met 49 times but this just resulted in less overall gain. Time in market was less but with a long and short forex strategy overnight fees are not a major concern as you get paid to be short and you pay to be long.

The win rate was higher by just over 5% but the gain/loss ratio was lower.

With the exit conditions the longest trade was held for 116 bars/hours. Without the conditions only seven trades went longer than this 116 hours and the longest was still only 159 hours.

I’m just not sure that the extra conditions add very much and they definitely reduced profit per trade in the tested data sample.

I agree with you Vonasi, the exit conditions I added are not essential to the system, I like them because they reduce the time in the market quite a lot but the system don´t need them if you don´t want them.

The important point of my version is that I translated this fine system from the 1D TF to 1H TF keeping the good results. I just wanted to share that.

Thank you all for your interest and collaboration in implementing the code. An alternative may be to modify the exit of trades with instruments that do not require optimization. I am currently testing with john ehlers filters. When I get results I’ll post the code. good job

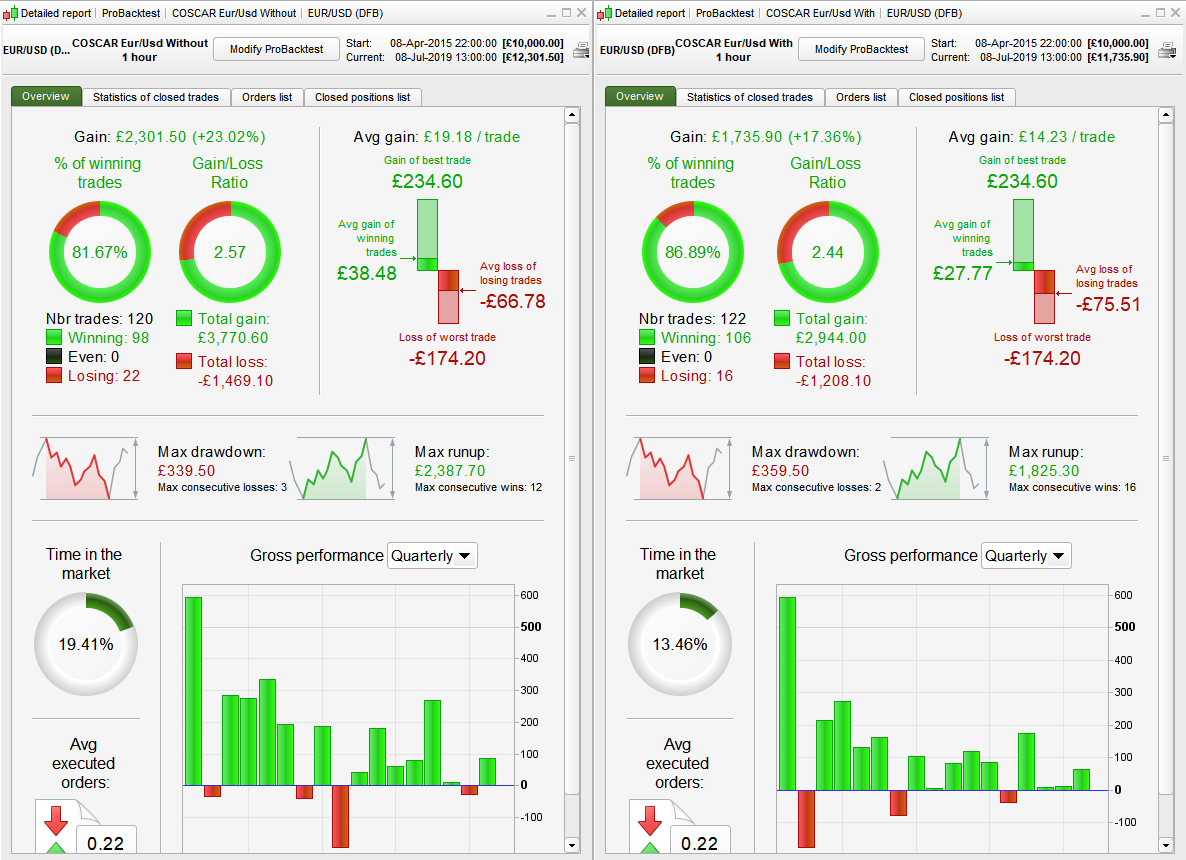

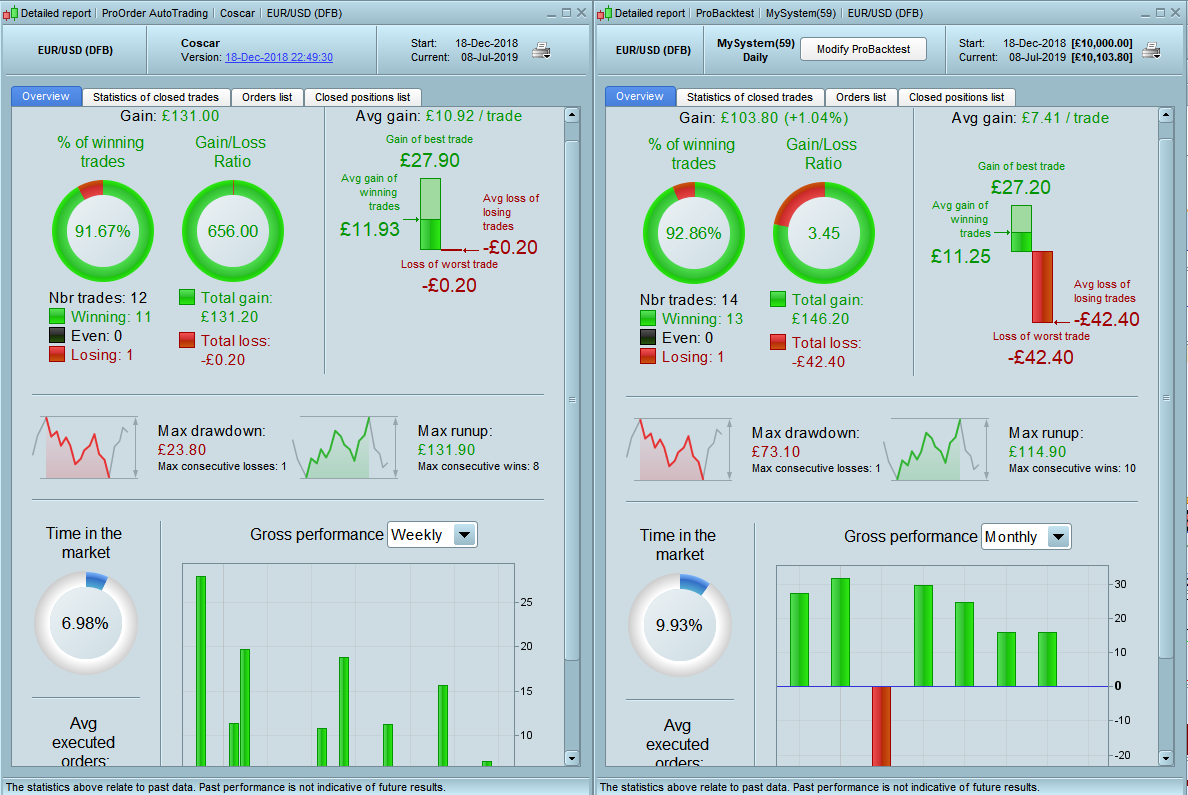

I have had the end of day version running live on demo since 18 December 2018 and I thought that the comparison between backtesting and live forward testing might be of interest to others so I post the results here.

My demo account had several issues that meant that the strategy was stopped several times and many of my strategies went through a long phase of not opening positions – although I can’t confirm that this was one of them but because of all this the trade quantities are different and my live version missed the biggest loser. Despite all this the strategy seems to have traded pretty well so far.

Live test is on the left in the images and backtest is on the right.

Hi guys presents a variant of the code created with the addition of an output based on the filter by John Ehlers, plus I added some optional features like Martingala, Capital reinvestment. I tested the system starting from a minimum capital of € 500.00 and I always got the same result, it seems that the system is quite stable in the long run. I hope someone can take an interest and improve it. Share the variations. Thank you

//@Coscar Break Out Point| Eur/Usd mini - 1D Capital Ini Eur 500,00

DEFPARAM CUMULATEORDERS= false

DEFPARAM PRELOADBARS = 10000

//***********************************************************************************************************

CapitalIni = 10000 // Capitale iniziale cifra intera min € 500,00

CapitalRisk = 10 // Percentuale di rischio del capitale

NrContratti = 0.5 // numero di contratti iniziali

MargineBroker = 378 // Margine richiesto dal broker IG MARKET per 1 contratto Eur/Usd Mini

Martingala = 1 // "1" per ON , "0" per OFF del sistema Martinagala

Multi = 1.8 //Martingala Moltiplicatore in caso di vincita - "1" per OFF

Reinvestimento = 1 // "1" per ON , "0" per OFF reinvestimento Capitale e profitto

Perc = 20 // Percentuale del capitale destinato al reinvestimento (consiglio max 30%)

Protec = 100 // "0" per OFF, Contratti massimi consentiti al sistema -Ricordarsi di inserire questo valore in fase di Trading Automatico in PRT

//------------------ EVENTUALI VARIABILI DEL SISTEMA---------------------------------------

Avg = 2 // Moving Average Period DEFAULT 2 Day

Atrs = 0.16 // Multiplier coefficient Atr

m = 2.1//1.8 // Multiplier coefficient Stop Loss

//***********************************************************************************************

ONCE OrderSize = NrContratti

ONCE ExitIndex = -2

Capital= CapitalIni + strategyprofit

IF Reinvestimento = 1 THEN

NR = ((Capital * Perc/100)/MargineBroker)*1000

n = (ROUND(NR)/1000)

ELSE

n = 0.5

ENDIF

IF Protec>0 AND n>Protec THEN

n=Protec

ENDIF

//**************************************Indicator**************************************

a1 = exp (-1.414 * 3.14159 / 10)

b1 = 2 * a1 * cos (1.414 * 3.14159 / 10)

c2 = b1

c3 = -a1 * a1

c1 = 1 - c2 - c3

if barindex=0 then

Filt = c1 * (Close) / 2

elsif barindex=1 then

Filt = c1 * (Close + Close[1]) / 2 + c2 * Filt[1]

elsif barindex > 1 then

Filt = c1 * (Close + Close[1]) / 2 + c2 * Filt[1] + c3 * Filt[2]

endif

closep=TotalPrice

a1 = exp (-1.414 * 3.14159 / 10)

b1 = 2 * a1 * cos (1.414 * 3.14159 / 10)

c2 = b1

c3 = -a1 * a1

c1 = 1 - c2 - c3

if barindex=0 then

Filtp = c1 * (closep) / 2

elsif barindex=1 then

Filtp = c1 * (Closep + Closep[1]) / 2 + c2 * Filtp[1]

elsif barindex > 1 then

Filtp = c1 * (Closep + Closep[1]) / 2 + c2 * Filtp[1] + c3 * Filtp[2]

endif

Roofing =(Filt-Filtp)

Atr = AverageTrueRange[14](close)

x = average[Avg,3](Typicalprice)

b1e = ((2*x)-high)+(ATR*ATRs)

s1e = ((2*x)-Low)-(ATR*ATRs)

Hbop = (2*x)-(2*Low)+High

Lbop = (2*x)-(2*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close<lbop THEN

BUY OrderSize CONTRACTS AT b1e LIMIT

SELL AT s1e LIMIT

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket THEN

SELL AT s1e LIMIT

IF close > positionprice THEN

SELL AT MARKET

ELSIF Roofing crosses under Roofing [1] THEN

SELL AT MARKET

ENDIF

ExitIndex = BarIndex

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close>hbop THEN

SELLSHORT OrderSize CONTRACTS AT s1e LIMIT

EXITSHORT AT b1e LIMIT

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket THEN

EXITSHORT AT b1e LIMIT

IF close < positionprice THEN

EXITSHORT AT MARKET

elsif Roofing crosses over Roofing [1] then

EXITSHORT AT MARKET

endif

ExitIndex = BarIndex

ENDIF

SET STOP LOSS (m*ATR)

//Martingala************************

IF Barindex = ExitIndex + 1 THEN

ExitIndex = 0

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize + (Martingala*0)

ELSIF PositionPerf(1) > 0 THEN

OrderSize = 1 * n * Multi

ENDIF

ENDIF

IF Capital<-CapitalIni*(CapitalRisk/100) THEN

QUIT

ENDIF

//GRAPH OrderSize

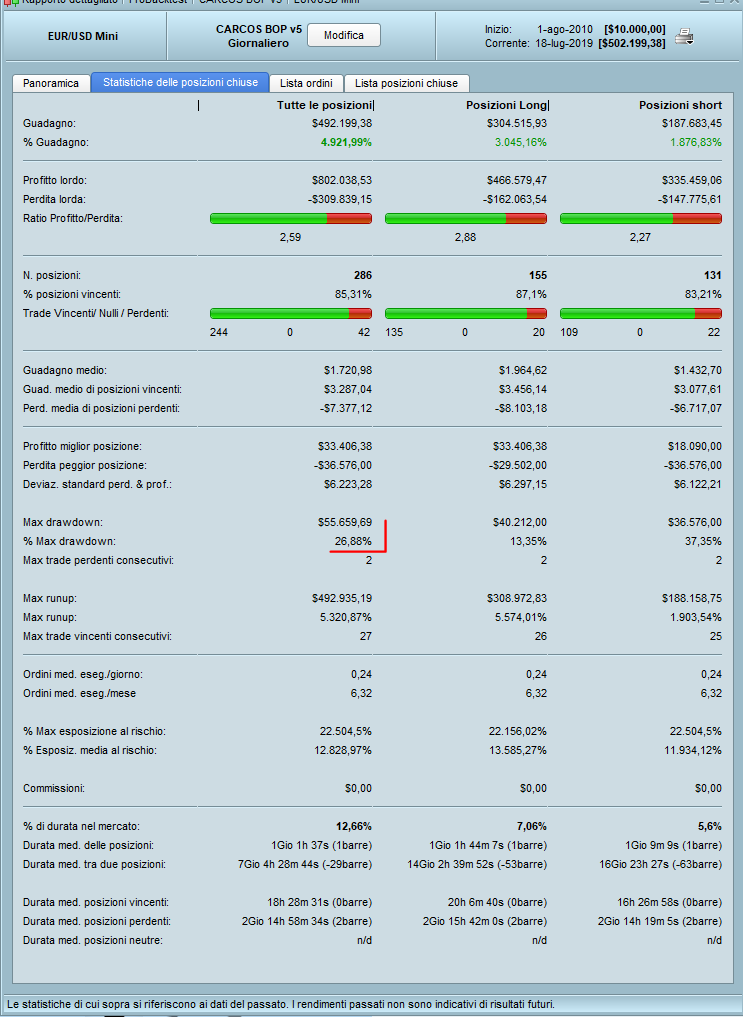

What’s the DRAWDOWN, on my test it was over 41K US$?

I think starting with a minimun capital of 200K US$ would make IG/Esma much happier!

thanks roberto, currently I have suspended the prorealtime platform with IG in Reale, so the test is with 100000 bars. You could send me a screenshots to see the DD, it doesn’t come out to me. thank you

It happens many times to me, too. It’s a real nuisance!

Just repeat the backtest over and over until it appears!!!!

Hi Roberto, I reactivated PRT in Reale, this is the test on 200,000 bars, spread 1 pip. The overall DD is 27% and it is normal that in the end there is a value of 55,000 as proportionate to the contracts. Try disabling Reinvestment and Martingale. If there are errors, could you kindly highlight them? Thank you Greetings

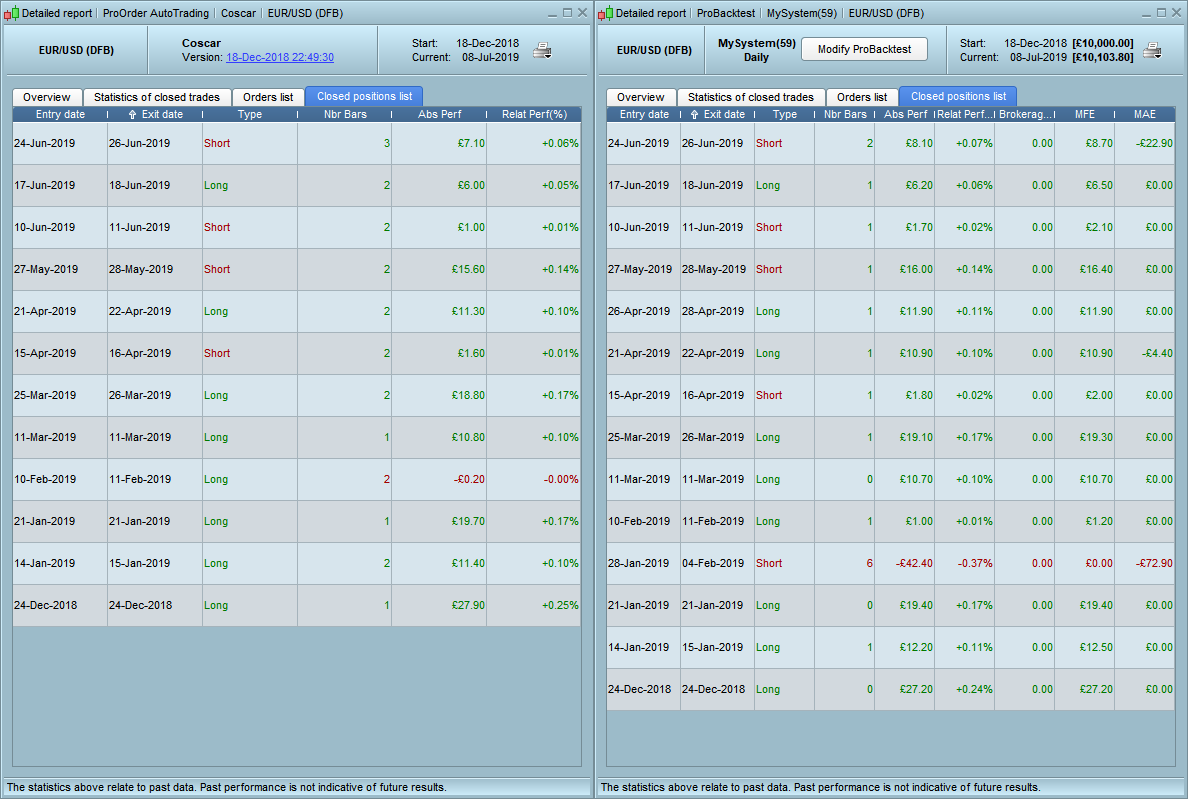

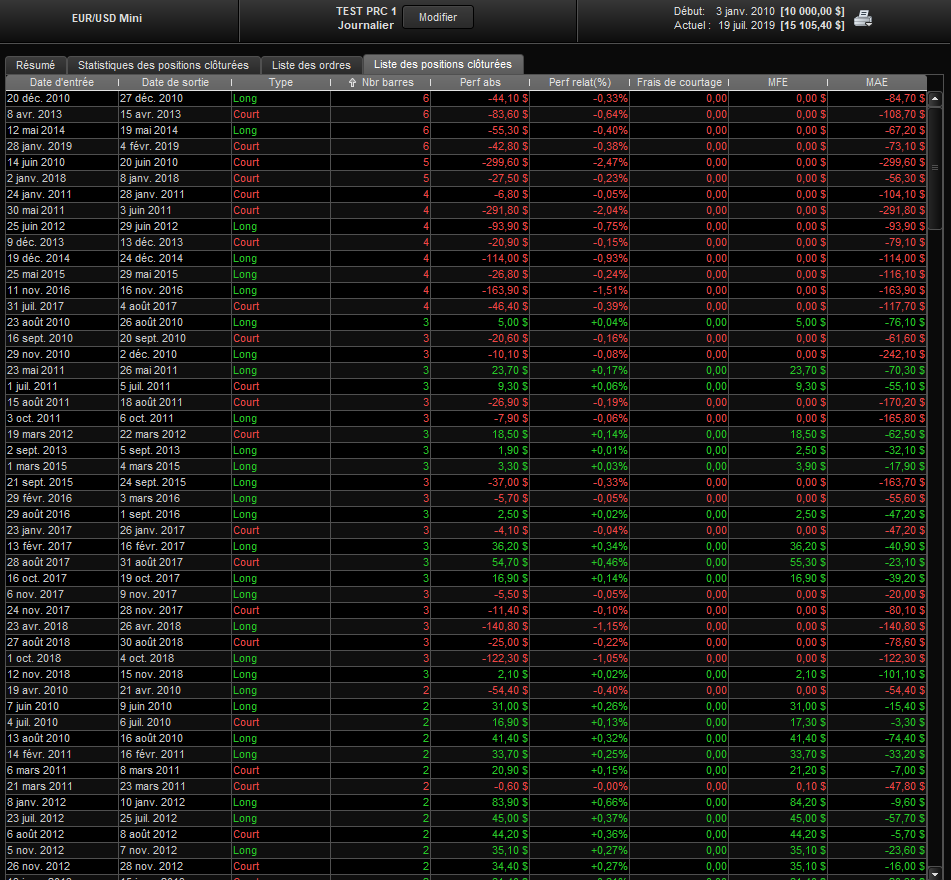

Hi Coscar and Roberto,

it seems that most profits are made in the day or in max 2 or 3 days. And the biggest losses in 3 to 6 days. So should not we close after 48h max?

it seems that most profits are made in the day or in max 2 or 3 days. And the biggest losses in 3 to 6 days. So should not we close after 48h max?

There is not much logic in this as maybe at the 48 hour point all those trades were actually in bigger losses and recovered a bit in the following few days and were closed for a smaller loss than would have been achieved at the 48 hour point.

You can add something to the code to test this but really it is just data mining as there is no good reason why future trades should be at smaller losses just because 48 hours has passed by since they were opened.

Avoiding over night fees is not of major benefit as it is a long and short forex strategy so we pay to be long and get paid to be short.

Thanks Vonasi for your explanation, I agree with you.

However I am surprised when I look at the MFE column. It seems that all losing trades have been directly negative and have never gone positive even for a short time. Unless I do not understand this column well 🙂

Just repeat the backtest over and over until it appears!!!!

Until what appears?

Depending what is your answer then I may have a quicker solution for you than repeating backtests.

I think he is talking about the Drawdown percent! Sometimes it doesn’t calculate and stay to 0 so we have to launch a backtest again.