I made an MTF version out of latest Vonasi’s version, by:

- replacing empty line 5 with timeframe(Daily,UpdateOnClose)

- replacing empty line 48 with timeframe(default)

- appending Nicolas’ Trailing Stoip code

- launching it form a 2-minute TF

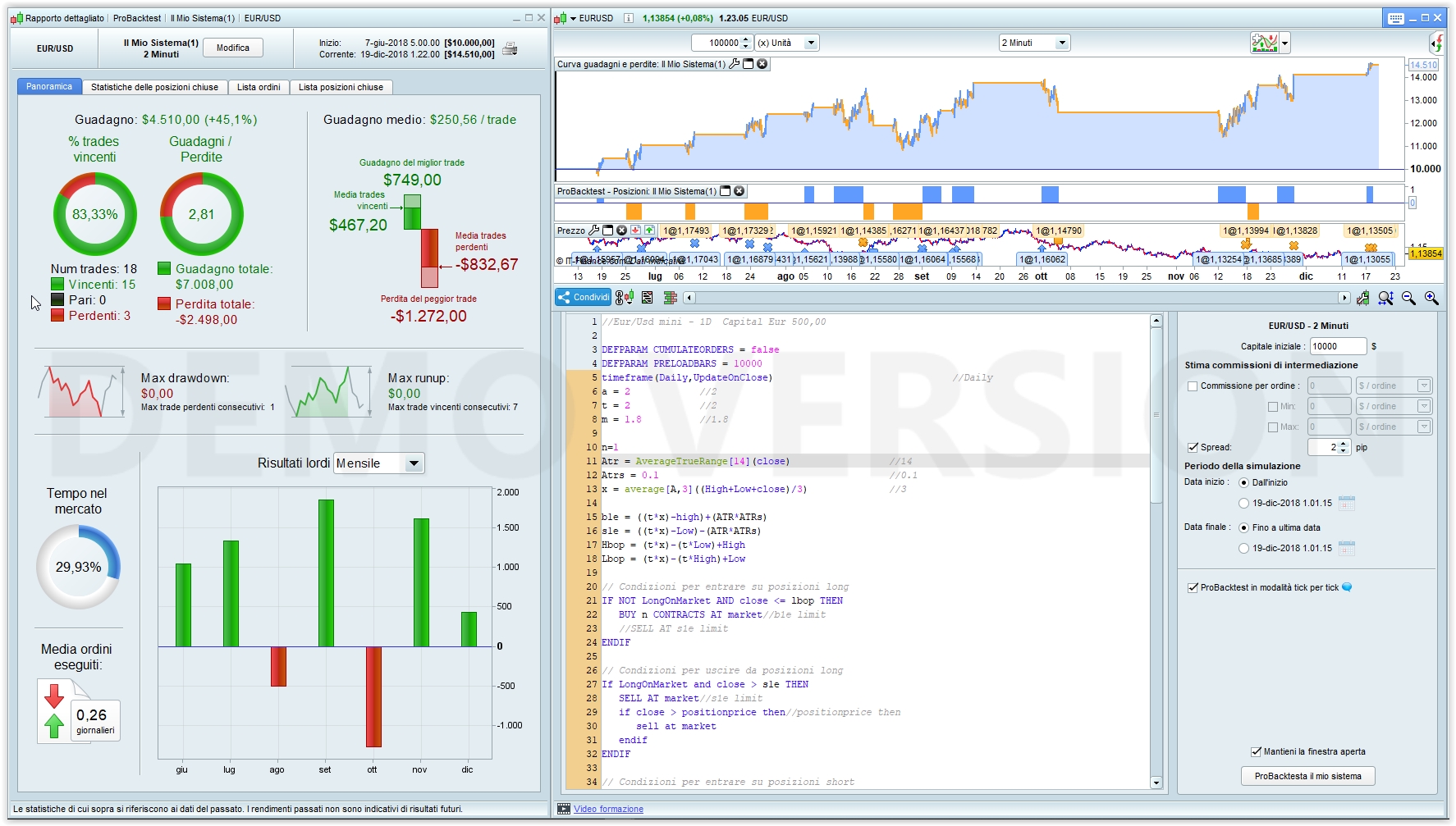

//Eur/Usd mini - 1D Capital Eur 500,00

DEFPARAM CUMULATEORDERS = false

DEFPARAM PRELOADBARS = 10000

timeframe(Daily,UpdateOnClose) //Daily

a = 2 //2

t = 2 //2

m = 1.8 //1.8

n=1

Atr = AverageTrueRange[14](close) //14

Atrs = 0.1 //0.1

x = average[A,3]((High+Low+close)/3) //3

b1e = ((t*x)-high)+(ATR*ATRs)

s1e = ((t*x)-Low)-(ATR*ATRs)

Hbop = (t*x)-(t*Low)+High

Lbop = (t*x)-(t*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close <= lbop THEN

BUY n CONTRACTS AT market//b1e limit

//SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket and close > s1e THEN

SELL AT market//s1e limit

if close > positionprice then//positionprice then

sell at market

endif

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close >= hbop THEN

SELLSHORT n CONTRACTS AT market//s1e limit

//EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket and close < b1e THEN

EXITSHORT AT market//b1e limit

if close < positionprice then

exitshort at market

endif

ENDIF

set stop loss (m*ATR)

//

timeframe(default) //2 min

//************************************************************************

//trailing stop function

trailingstart = 45 //45 trailing will start @trailinstart points profit

trailingstep = 15 //15 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

as from attached screenshot.

**** Google translator*******

Thank you all for your contribution.

In theory, the strategy should appeal to all markets with appropriate optimization, in fact I would like to create a diversified portfolio on this strategy.

Roberto hrazie for your MTF code but are looking for a strategy that can betray in real and I think the MTF is not yet supported in real mode, or something has changed? Currently I use PRT of IG which has some limitation.

You are correct that MTF is still only in beta testing but we should all be using this opportunity to live forward test MTF strategies so that we are ready and confident in them when it finally gets put live. Also it helps PRT/IG find any bugs which can only benefit us too.

Regarding your topic title and trying to reduce draw down. I personally think the draw down is already pretty low on your strategy and it will be difficult to improve on it without adding new conditions which will then just lead to less trades and less profit and increased chance of curve fitting. I usually have in my mind that every time that I add a condition that has a variable then I am multiplying the curve fitting probability by two. My theory is that if we keep it simple and it works then it is more likely to work going forward than a complicated strategy is.

Thanks Vonasi

in fact, my goal is to find a simple strategy that is stable.

Drawdown can be further reduced by applying the same strategy above to Heikin-Ashi candlesticks (still Nicolas’ trailing stop code uses regular japanese candlesticks).

I tested it on regular EurUsd, rather than the mini one because I found out it is not just a simple math issue (it’s, or it should be, just a division by ten), because on the mini contract I’ve been reported more than 300 trades, almost all losing money. While there’s no difference when applied to DAX €25 and DAX €5, it’s the same behaviour, only multiplied/divided by 5!

//Eur/Usd mini - 1D Capital Eur 500,00

DEFPARAM CUMULATEORDERS = false

DEFPARAM PRELOADBARS = 0

timeframe(Daily,UpdateOnClose) //Daily

// HA definition

if BarIndex > 1 then

xClose = (open+close+low+high)/4

xOpen = (xOpen[1]+xClose[1])/2

haHigh = Max(xOpen, xClose)

haLow = Min(xOpen, xClose)

xHigh = Max(High,haHigh)

xLow = Min(Low,haLow)

else

xClose = (open+close+low+high)/4

xOpen = (Open[1]+Close[1])/2

haHigh = Max(xOpen, xClose)

haLow = Min(xOpen, xClose)

xHigh = Max(High,haHigh)

xLow = Min(Low,haLow)

endif

a = 2 //2

t = 2 //2

m = 1.8 //1.8

n=1

Atr = AverageTrueRange[14](xClose) //14

Atrs = 0.1 //0.1

x = average[A,0]((xHigh+xLow+xclose)/3) //4

b1e = ((t*x)-xhigh)+(ATR*ATRs)

s1e = ((t*x)-xLow)-(ATR*ATRs)

Hbop = (t*x)-(t*xLow)+xHigh

Lbop = (t*x)-(t*xHigh)+xLow

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND xclose <= lbop THEN

BUY n CONTRACTS AT market//b1e limit

//SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket and xclose > s1e THEN

SELL AT market//s1e limit

if xclose > positionprice then//positionprice then

sell at market

endif

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND xclose >= hbop THEN

SELLSHORT n CONTRACTS AT market//s1e limit

//EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket and xclose < b1e THEN

EXITSHORT AT market//b1e limit

if xclose < positionprice then

exitshort at market

endif

ENDIF

set stop loss (m*ATR)

//

timeframe(default) //2 min

//************************************************************************

//trailing stop function

trailingstart = 35 //35 trailing will start @trailinstart points profit

trailingstep = 15 //15 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

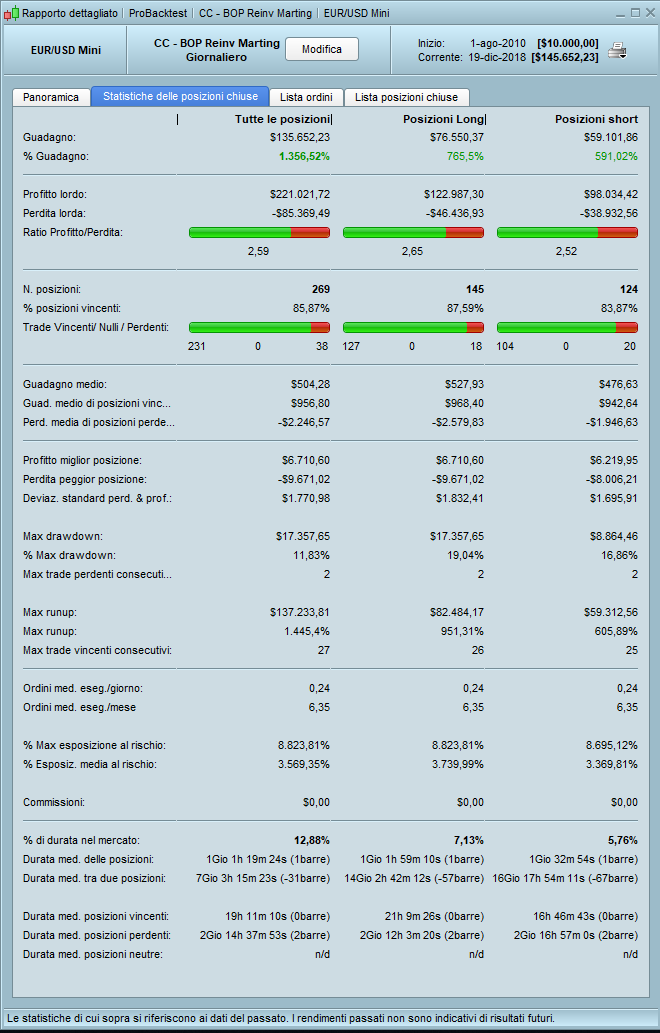

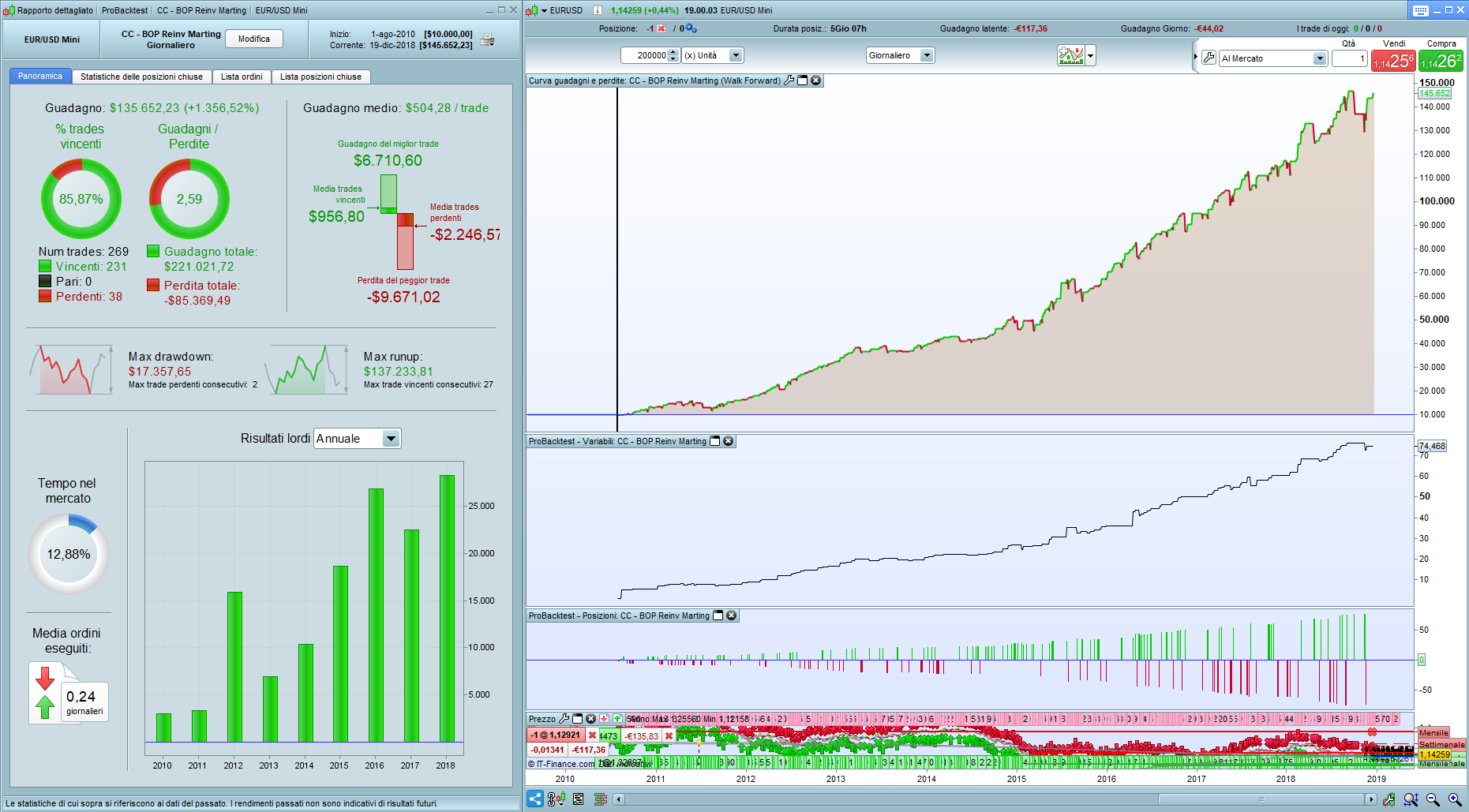

Ok grazie Roberto, lo proverò ma ho notato dal tuo screenshots che per alcuni mesi non scambia.

coscar – English only please in the English speaking forum – even if you are both Italian!

Sorry Vonasi, it’s the fault of the automatic translator.

“Ok, thanks Roberto, I’ll try it but I noticed from your screenshots that for a few months it does not exchange.”

Hello Vonasi and Roberto I still ask you a kindness, you could test the attached code since 1995. Thank you

//@Coscar Break Out Point on Eur/Usd mini - 1D Capital Ini Eur 500,00

DEFPARAM CUMULATEORDERS= false

DEFPARAM PRELOADBARS = 10000

//***********************************************************************************************************

CapitalIni = 10000 // Capitale iniziale cifra intera

NrContratti = 1 // numero di contratti iniziali

MargineBroker = 378 // Margine richiesto dal broker per 1 contratto Eur/Usd Mini

Martingala = 1 // "1" per ON , "0" per OFF del sistema Martinagala

Multi = 1 //Martingala Moltiplicatore in caso di vincita - "1" per OFF

Reinvestimento = 1 // "1" per ON , "0" per OFF reinvestimento Capiatale e profitto

Perc = 20 // Percentuale del capiatale destinato al reinvestimento (consiglio max 30%)

Protec = 100 // "0" per OFF, Contratti massimi consentiti al sistema -Ricordarsi di inserire questo valore in fase di Trading Automatico in PRT

Avg = 2 // Moving Average Period Two Day

Atrs = 0.16 // Multiplier coefficient Atr

m = 1.8 // Multiplier coefficient Stop Loss

//***********************************************************************************************

ONCE OrderSize = NrContratti

ONCE ExitIndex = -2

Capital= CapitalIni + strategyprofit

IF Reinvestimento = 1 THEN

NR = ((Capital * Perc/100)/MargineBroker)*1000

n = (ROUND(NR)/1000)

Else

n = 1

endif

IF Protec>0 and n>Protec THEN

n=Protec

endif

Atr = AverageTrueRange[14](close)

x = average[Avg,3]((High+Low+close)/3)

b1e = ((2*x)-high)+(ATR*ATRs)

s1e = ((2*x)-Low)-(ATR*ATRs)

Hbop = (2*x)-(2*Low)+High

Lbop = (2*x)-(2*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close<lbop THEN

BUY OrderSize CONTRACTS AT b1e limit

SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket THEN

SELL AT s1e limit

if close > positionprice then

sell at market

endif

ExitIndex = BarIndex

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close>hbop THEN

SELLSHORT OrderSize CONTRACTS AT s1e limit

EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket THEN

EXITSHORT AT b1e limit

if close < positionprice then

exitshort at market

endif

ExitIndex = BarIndex

ENDIF

set stop loss (m*ATR)

//Martingala************************

IF Barindex = ExitIndex + 1 THEN

ExitIndex = 0

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize + (Martingala*0)

ELSIF PositionPerf(1) > 0 THEN

OrderSize = 1 * n * Multi

ENDIF

ENDIF

IF Capital<-500 then

Quit

ENDIF

GRAPH OrderSize

It is not possible to test it from 1995 as you need tick by tick data which is only available from mid 2010.

OK thanks, you could check the robustness of this code, I would like to start it in real time. Thanks for your availability

I have not had a chance to test your code yet but the only way to truly test robustness is to live forward test a strategy in demo. Personally I would not put any real money on any strategy until I have seen months of forward testing in a variety of market conditions and preferably lots and lots of trades. It is boring and you need a lot of patience but losing money is easy enough so why be in such a hurry to do it?

I see that you have added some form of martingale and money management. Don’t do this until you have forward tested the strategy with level stakes – it just makes you imagine all the money you could be making when in reality you don’t even know if level stakes would make you any. Martingale is very dangerous unless you have a very high win rate strategy or one where the wins are much bigger than the losses and even then it can all suddenly get very expensive in just a few losing trades. If you have Warren Buffets bank balance behind you then use martingale – if not then don’t.

All just my humble opinion but then people have all sorts of opinions on how to best lose money at this game!

I did a multitimeframe version of this fine system that seems to perform quite well in backtest, I haven´t tried it yet in real or demo

Next autumn v11 is likely to be made available to IG customers, thus making 1M bars available for backtesting.

Here is the code from the version posted by TempusFugit. My main concern if I had coded it myself would be the exit conditions based on days of week and time and bars since trades opened which seem to smell horribly of data mining.

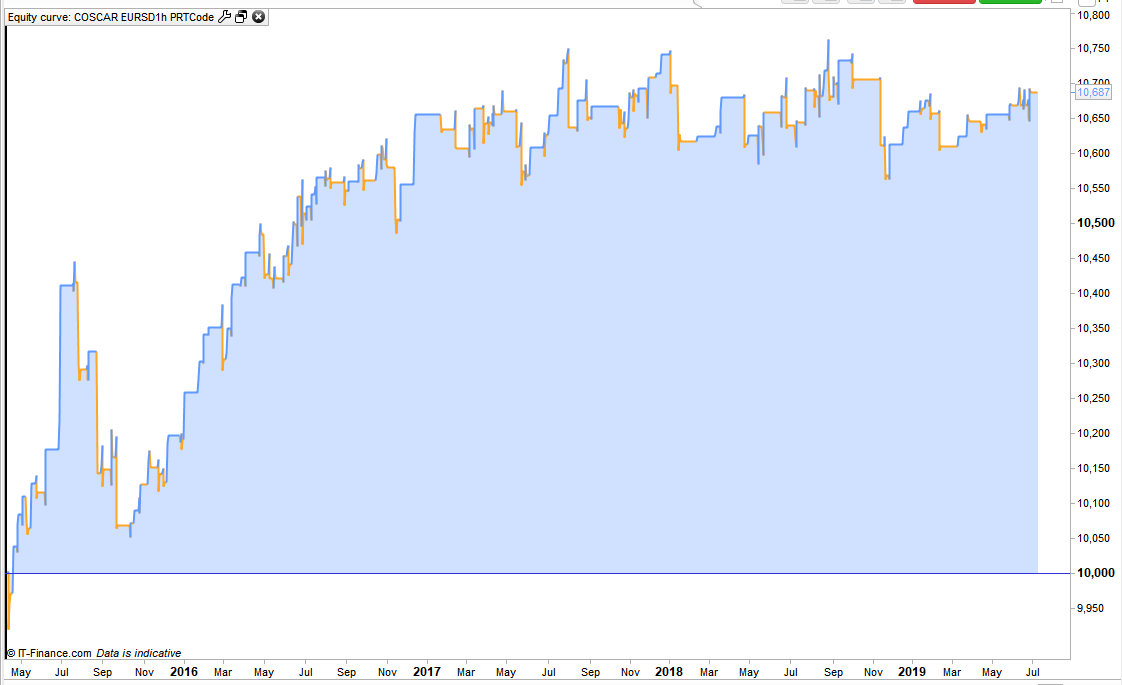

The true test is to remove most of them and see how it fairs. With just the exit if it is 2100 hours and the rest of them are removed then the equity curve is a little less inspiring. Image attached.

If we let them back in one by one then the equity curve starts to look nice again which is really telling us that they are just data mining conditions. IMHO.

// COSCAR Eur/Usd mini - 1H En PRTCode

//Version Tempus Fugit

DEFPARAM CUMULATEORDERS= false

DEFPARAM PRELOADBARS = 10000

//VARIABLES

PositionSize = 1

ENTRYHOURS = HOUR=1

nwma = 2 //Periodos de la Media de Willians sobre "la mediana"

t = 2//Multiplicador de la media y otros valores

NATR = 14//Periodos del ATR

m = 1.8//2.7 //Multiplicador del ATR para el stop

Atrs = 0.16//Multiplicador del ATR para el precio límite de salida

Timeframe(Daily,Updateonclose)

Atr = AverageTrueRange[NATR](close)

x = average[nwma,3]((High+Low+close)/3)

b1e = ((t*x)-high)+(ATR*ATRs)

s1e = ((t*x)-Low)-(ATR*ATRs)

Hbop = (t*x)-(t*Low)+High

Lbop = (t*x)-(t*High)+Low

LONGSIGNAL = CLOSE<LBOP

SHORTSIGNAL = CLOSE>HBOP

Timeframe(Default)

LONGENTRY = LONGSIGNAL

LONGENTRY = LONGENTRY AND ENTRYHOURS

LONGENTRY = LONGENTRY AND DAYOFWEEK<4//SIN JUEVES Y VIERNES

SHORTENTRY = SHORTSIGNAL

SHORTENTRY = SHORTENTRY AND ENTRYHOURS

SHORTENTRY = SHORTENTRY AND DAYOFWEEK<4//SIN JUEVES Y VIERNES

IF LONGENTRY THEN

BUY PositionSize CONTRACTS AT B1E LIMIT

SELL AT s1e limit

ELSIF SHORTENTRY THEN

SELLSHORT PositionSize CONTRACTS AT S1E LIMIT

EXITSHORT AT b1e limit

ENDIF

If LongOnMarket THEN

SELL AT s1e limit

ELSIF ShortOnMarket THEN

EXITSHORT AT b1e limit

endif

WINEXIT = ONMARKET

WINEXIT = WINEXIT AND POSITIONPERF>0

WINEXIT = WINEXIT AND (HOUR=21 OR (BARINDEX-TRADEINDEX>70))

LOSSEXIT = ONMARKET

LOSSEXIT = LOSSEXIT AND POSITIONPERF<0

LOSSEXIT = LOSSEXIT AND BARINDEX-TRADEINDEX>80

LOSSEXIT = LOSSEXIT AND HOUR>=21

LOSSEXIT = LOSSEXIT AND (DAYOFWEEK=3 OR DAYOFWEEK=5)

IF WINEXIT OR LOSSEXIT THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

set stop loss (m*ATR)