Hi I’m new and not very experienced and for some time I try to learn information from the community. I ask you advice to improve this simple code that I developed but I would like to reduce the% Ma DrawDown and I think there is some error. Thanks to anyone who wants to help me.

//Eur/Usd mini - 1D Capital Eur 500,00

DEFPARAM CUMULATEORDERS= false

DEFPARAM PRELOADBARS = 10000

n=1

Atr = AverageTrueRange[14](close)

Atrs = 0.1

x = average[A,3]((High+Low+close)/3)

b1e = ((2*x)-high)+(ATR*ATRs)

s1e = ((2*x)-Low)-(ATR*ATRs)

Hbop = (2*x)-(2*Low)+High

Lbop = (2*x)-(2*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close<lbop THEN

BUY n CONTRACTS AT b1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket THEN

SELL AT s1e limit

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close>hbop THEN

SELLSHORT n CONTRACTS AT s1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket THEN

EXITSHORT AT b1e limit

ENDIF

set stop loss (1.8*ATR)

Variable A is missing, what’s its value?

Are you aware that if your long or short limit orders open positions then you will not have a sell or exitshort order on the market until the close of the bar? You should add them in like this:

/ Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close<lbop THEN

BUY n CONTRACTS AT b1e limit

SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket THEN

SELL AT s1e limit

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close>hbop THEN

SELLSHORT n CONTRACTS AT s1e limit

EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket THEN

EXITSHORT AT b1e limit

ENDIF

Variable A is missing, what’s its value?

a = 2

Tanks

DEFPARAM CUMULATEORDERS= false

DEFPARAM PRELOADBARS = 10000

capital = 500 + strategyprofit

n=1

Atr = AverageTrueRange[14](close)

Atrs = 0.1

x = average[2,3]((High+Low+close)/3)

ema=average[3,6](close)

b1e = ((2*x)-high)+(ATR*ATRs)

s1e = ((2*x)-Low)-(ATR*ATRs)

Hbop = (2*x)-(2*Low)+High

Lbop = (2*x)-(2*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close<lbop and close>ema THEN

BUY n CONTRACTS AT b1e limit

SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket THEN

SELL AT s1e limit

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close>hbop and close<ema THEN

SELLSHORT n CONTRACTS AT s1e limit

EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket THEN

EXITSHORT AT b1e limit

ENDIF

set stop loss (1.8*ATR)

If Capital<-300 then

quit

endif

I’ve applied some variations like an EMA filter

You have to try changing values until you find the ones that you think are what suit you (not the market!) best.

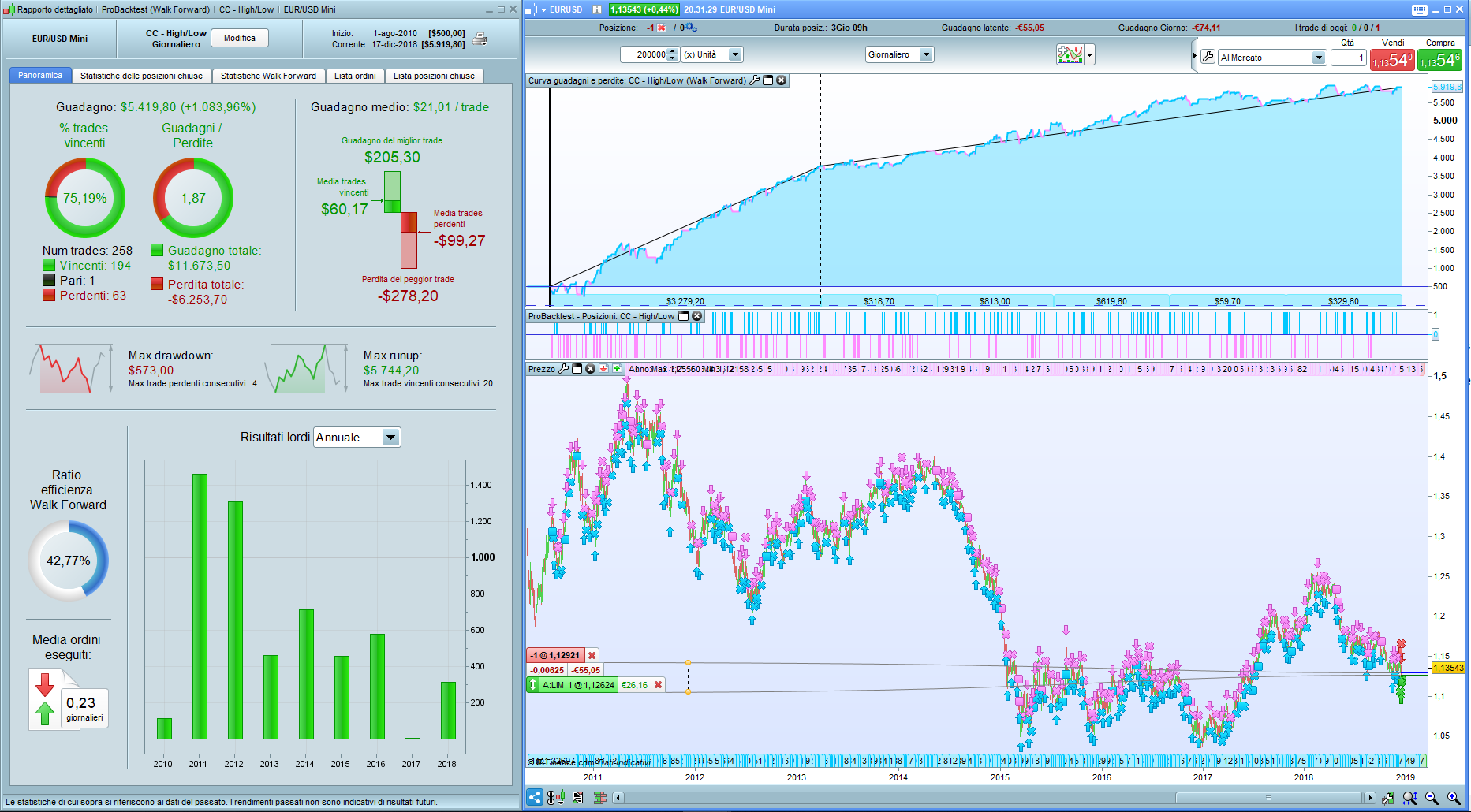

Setting an average type of 2 (wma), instead of 3, then 1.3 at line 34, provided variable A has been assigned 2, my drawdown drops to 267.30 as from screenshot.

Try to walk forward your strategy.

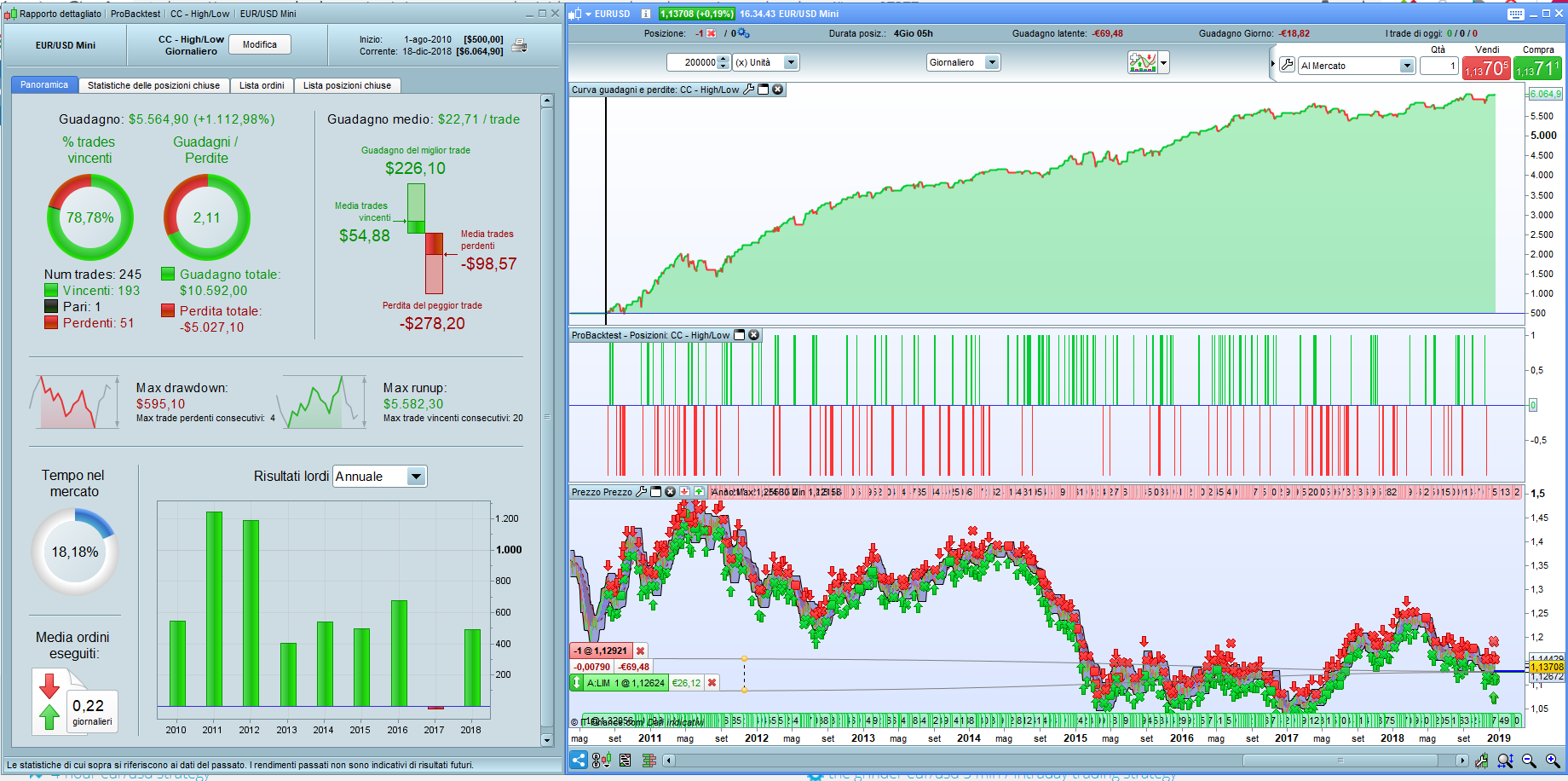

I prefer to take stuff away rather than add it. I have removed the fixed level stop loss (it doesn’t add much anyway) and you have levels set to reverse the trades anyway. Most trades don’t seem to be more than one day so I have added exits at the close of any day that you are in profit. The ATRS variable has been optimised to 0.16. It seems pretty stable for a EUR/USD strategy. I wouldn’t add EMA’s as you are just adding an extra level of curve fit and EMA’s are oh so easy to curve fit!

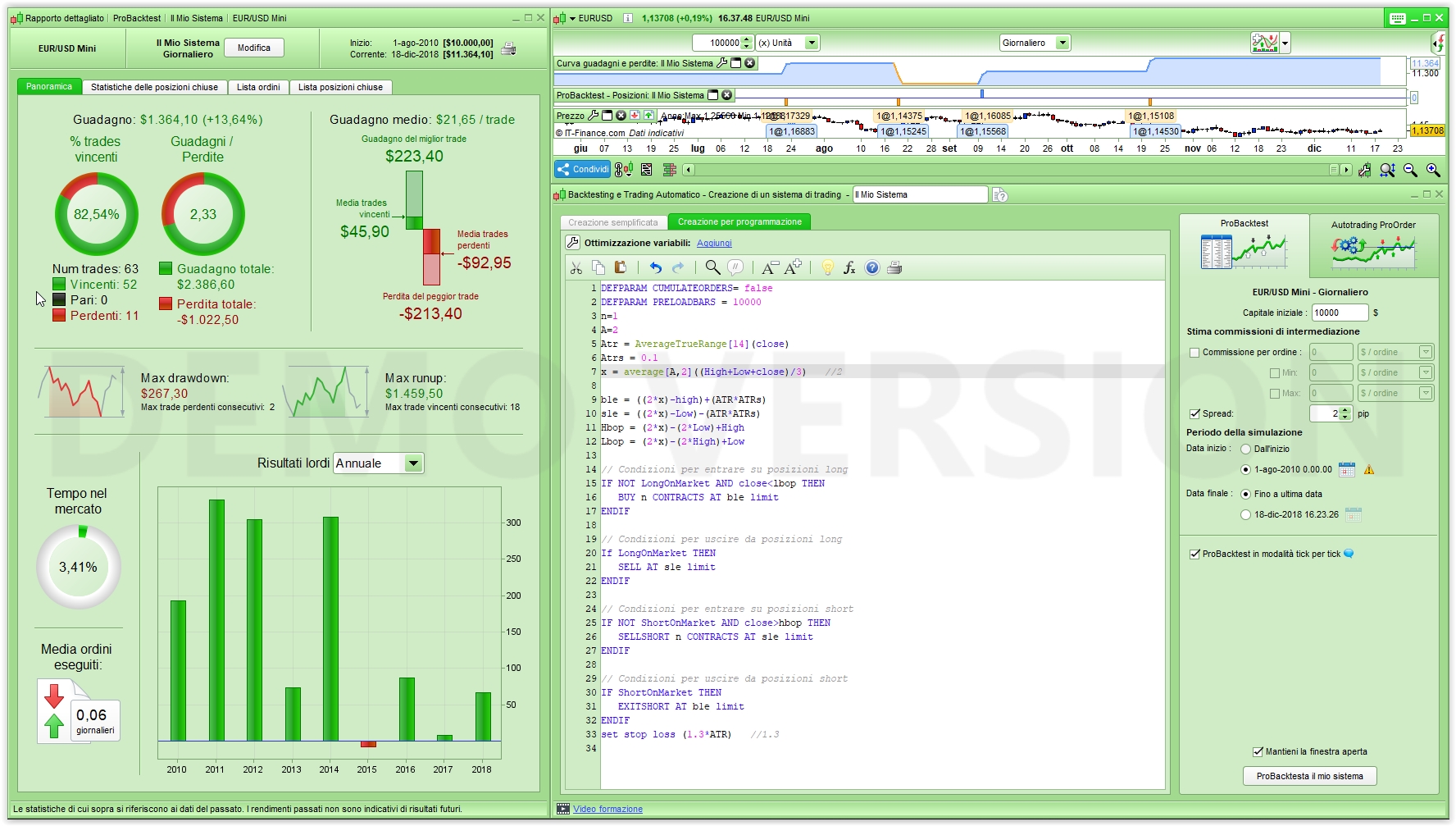

//Eur/Usd mini - 1D Capital Eur 500,00

DEFPARAM CUMULATEORDERS= false

DEFPARAM PRELOADBARS = 10000

a = 2

t = 2

//m = 2.7

n=1

Atr = AverageTrueRange[14](close)

Atrs = 0.16

x = average[A,3]((High+Low+close)/3)

b1e = ((t*x)-high)+(ATR*ATRs)

s1e = ((t*x)-Low)-(ATR*ATRs)

Hbop = (t*x)-(t*Low)+High

Lbop = (t*x)-(t*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close<lbop THEN

BUY n CONTRACTS AT b1e limit

SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket THEN

SELL AT s1e limit

if close > positionprice then

sell at market

endif

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close>hbop THEN

SELLSHORT n CONTRACTS AT s1e limit

EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket THEN

EXITSHORT AT b1e limit

if close < positionprice then

exitshort at market

endif

ENDIF

//set stop loss (m*ATR)

[attachment file=87383]

[attachment file=87384]

The name is Vonasi not Vanosi!

m is the multiple of the ATR for the stoploss. If you unremark the stoploss and unremark the m = 2.7 then you can run it with a stoploss. 2.7 was the value that gave highest results.

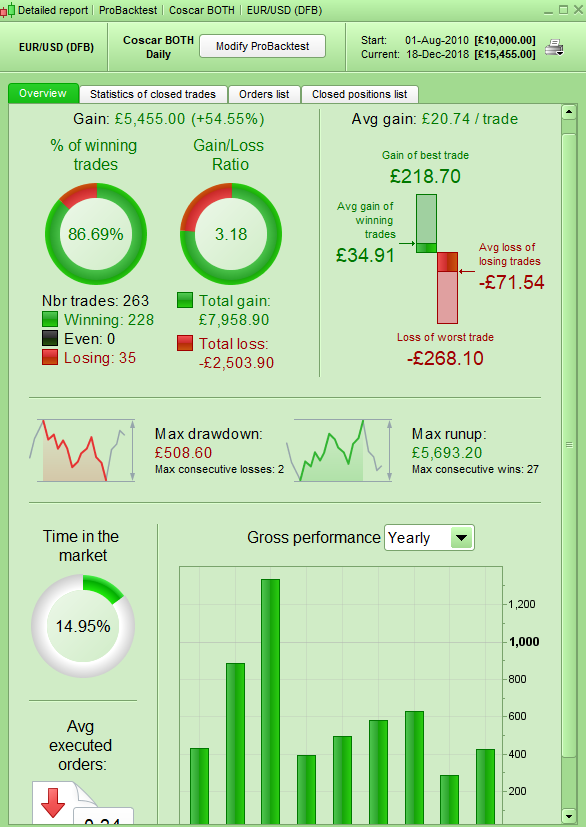

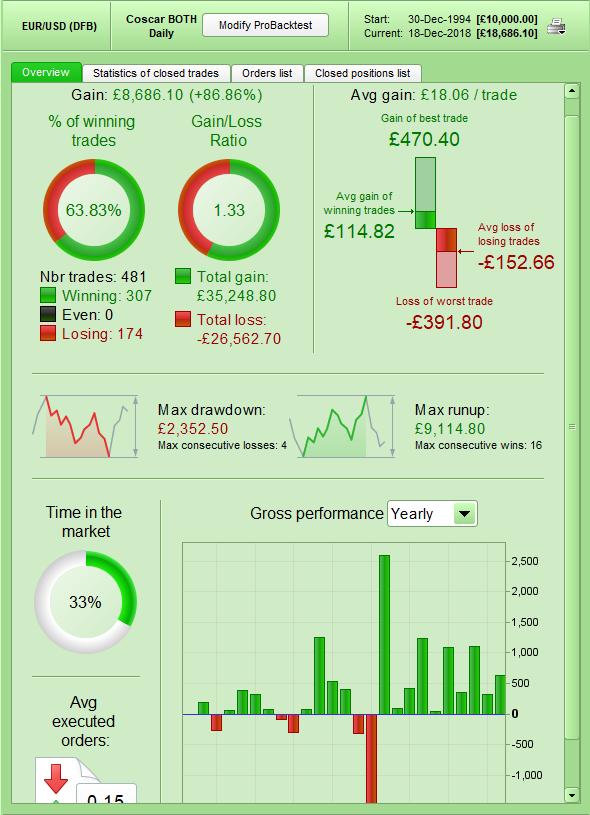

Just out of interest I decided to take my version of your strategy and convert it to an end of day strategy. So I removed the limit orders and just bought or sold if it was above or below lbop and hbop. I reinstated the stop loss and optimised it and ATRS. I tested back to the beginning of 1995. Even if the ride was a little rough especially through the 2008 recession it was still ultimately a good equity curve. You may be on to something with your ATR band calculations. Are you sure that you’re new to this game?

[attachment file=87402]

[attachment file=87403]

//Eur/Usd mini - 1D Capital Eur 500,00

DEFPARAM CUMULATEORDERS = false

DEFPARAM PRELOADBARS = 10000

a = 2

t = 2

m = 1.8

n=1

Atr = AverageTrueRange[14](close)

Atrs = 0.01

x = average[A,3]((High+Low+close)/3)

b1e = ((t*x)-high)+(ATR*ATRs)

s1e = ((t*x)-Low)-(ATR*ATRs)

Hbop = (t*x)-(t*Low)+High

Lbop = (t*x)-(t*High)+Low

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket AND close <= lbop THEN

BUY n CONTRACTS AT market//b1e limit

//SELL AT s1e limit

ENDIF

// Condizioni per uscire da posizioni long

If LongOnMarket and close > s1e THEN

SELL AT market//s1e limit

if close > positionprice then//positionprice then

sell at market

endif

ENDIF

// Condizioni per entrare su posizioni short

IF NOT ShortOnMarket AND close >= hbop THEN

SELLSHORT n CONTRACTS AT market//s1e limit

//EXITSHORT AT b1e limit

ENDIF

// Condizioni per uscire da posizioni short

IF ShortOnMarket and close < b1e THEN

EXITSHORT AT market//b1e limit

if close < positionprice then

exitshort at market

endif

ENDIF

set stop loss (m*ATR)

//graph b1e

//graph s1e

//graph Hbop

//graph Lbop

//

Ok ok sorry Vonasi 🙂 Have a nice weekend…..

What an early weekend! You’re lucky Vonasi.

Roberto, I forgot that someone need still to work … 😁😁