Projet d’intelligence artificielle sur le Dow Jones en bougie de 10 minutes, il faudra bien vous régler sur 10 minutes ! J’ai tenté d’inculquer la réflexion et l’expérience du trader associé à des statistiques

defparam cumulateorders=false

defparam preloadbars = 500

n=1

perte=500

xx=69

rem yy=30

yy=30

J=350

pz=3

py=12

x=169

if (dayofweek=6 or dayofweek=7) or (time<091500 or time>203000) or (time>153000 AND time<160500)or (time>194500 AND time<195500) then

journee=0

else

journee=1

endif

if (highest[288](close)-close)>(close/80) or (highest[144](close)-close)>(close/85) then

sensvente=1

else

sensvente=1

endif

if (close-highest[288](close))>(close/80) or (close-highest[144](close))>(close/85) then

sensachat=0

else

sensachat=1

endif

if close>(highest[30](close)*0.99911) then

achatextrem=0

else

achatextrem=1

endif

if close<(lowest[36](close)*1.00041) then

venteextrem=0

else

venteextrem=1

endif

cloture=((highest[117](close)+lowest[117](close))/2)

if close<(cloture-50) then

cloturevente=0

else

cloturevente=1

endif

if time<140000 and close>(cloture) then

clotureachat=1

else

clotureachat=1

endif

stopventetemps=0

else

stopventetemps=1

endif

if (open[4]<close[4] and open[3]<close[3] and open[2]<close[2] and open[1]>close[1]) then

stopachattemps=1

else

stopachattemps=1

endif

ratio=4.6

gain2=(highest[14](close)-low)

if gain2<0 then

gain=(gain2*-1)/ratio

else

gain=gain2/ratio

endif

if gain>=22 then

gain=78

endif

if gain<=2.7 then

gain=2.8

endif

if gain>=2.8 and gain<=9.4 then

gain=94

endif

SET TARGET PROFIT gain

SET STOP LOSS perte

nombre=12

couleur=7

descente=0

for z=1 to nombre do

if open[z]>close[z] then

descente=descente+1

endif

next

if descente>=couleur then

achatbougie=0

else

achatbougie=1

endif

montee=0

for y=1 to nombre do

if open[y]<close[y] then

montee=montee+1

endif

next

if montee>=couleur then

ventebougie=0

else

ventebougie=1

endif

nombre2=7

couleur2=6

descente2=0

for z2=1 to nombre2 do

if open[z2]>close[z2] then

descente2=descente2+1

endif

next

if descente2>=couleur2 then

achatbougie2=0

else

achatbougie2=1

endif

montee2=0

for y2=1 to nombre2 do

if open[y2]<close[y2] then

montee2=montee2+1

endif

next

if montee2>=couleur2 then

ventebougie2=0

else

ventebougie2=1

endif

if open>highest[14](close) or open>(close[24]*1.014) then

achathaut=0

else

achathaut=1

endif

if open<lowest[17](close) or open<(close[24]/1.0028) then

ventebas=0

else

ventebas=1

endif

p=10

q=8

plusHaut = HIGHEST[p](HIGH)

plusBas = LOWEST[p](LOW)

oscillateur = (CLOSE - plusBas) / (plusHaut - plusBas) * 100

K = AVERAGE[q,6](oscillateur)

periode=34

innere = 2*weightedaverage[ round( Periode/2 ) ](close)-weightedaverage[Periode](close)

MM=weightedaverage[round(sqrt(periode))](innere)

if (close>close[50]*1.02) or (close>close[6]*1.002) or (onmarket and (tradeprice-close)>z) or ventebougie=0 or ventebougie2=0 or close<BollingerDown[20](close)+2 or ventebas=0 or cloturevente=0 or venteextrem=0 or sensvente=0 then

stopventecalcul=0

else

stopventecalcul=1

endif

if (close[50]>close*1.04) or (close[6]>close*1.005) or (onmarket and (tradeprice-close)<z) or achatbougie=0 or achatbougie2=0 or close>BollingerUp[20](close)+18 or achathaut=0 or clotureachat=0 or achatextrem=0 or sensachat=0 then

stopachatcalcul=0

else

stopachatcalcul=1

endif

i1=average[3](close)

c1=i1>i1[6]

if stopachattemps=1 and c1 and journee=1 and k<xx and mm[1]<mm and stopachatcalcul=1 then

buy n shares at market

endif

i2=average[3](close)

i3=average[5](close)

c2=i2 crosses under (I3-50)

if c2 and ((tradeprice-close)<pz) and (time>091000 and time<212000) then

sell at market

endif

periode2=18

innere2 = 2*weightedaverage[ round( Periode2/2 ) ](close)-weightedaverage[Periode2](close)

MM2=weightedaverage[round(sqrt(periode2))](innere2)

c3=i1<i1[6]

if c3 and journee=1 and k>yy and mm2[2]>mm2 and stopventecalcul=1 and stopventetemps=1 then

sellshort n shares at market

endif

c4=i2 crosses OVER (i3-10)

if c4 and (tradeprice-close)>pY and (time>091000 and time<212000) then

//if (i1[6]-i1)<15 then

exitshort at market

endif

if longonmarket and (BarIndex-TRADEINDEX)>j then

sell at market

endif

if shortonmarket and (BarIndex-TRADEINDEX)>j then

exitshort at market

endif

if longonmarket and (BarIndex-TRADEINDEX)>x and (close-tradeprice)>5 then

sell at market

endif

if shortonmarket and (BarIndex-TRADEINDEX)>x and (tradeprice-close)>5 then

exitshort at market

endif

Merci beaucoup pour le partage. J’ai volontairement basculé ton post vers le forum, j’aimerai en savoir plus sur le cheminement de l’élaboration de la stratégie, qui a vraiment piqué mon intérêt, merci.

J’ai tenté d’inculquer la réflexion et l’expérience du trader associé à des statistiques

Merci beaucoup cela semble très prometteur

Il manque une ligne entre 47 et 48, n'est-ce pas?

Bonjour à tous et merci pour votre intérêt partagé

En effet, il manque bien quelques lignes, une erreur de copier/coller, voici la version complète

Le cheminement est ultra complexe, je suis trader depuis 20 ans et j’ai souhaité transcrire ma façon de trader en algorithme

C’est en testant pendant longtemps que l’on voit qu’il fait des erreurs que l’on n’aurait pas faites et donc ensuite il faut trouver le moyen d’apprendre à l’algorithme à ne plus reproduire ces erreurs.

Cet algorithme, j’ai mis 10 mois pour le construire et il évoluera encore et encore.

L’intelligence artificielle m’intéresse et j’y travaille régulièrement.

Biensûr, il y a une faille, dans ce code par exemple, si on perd 550 points, celà fait une grosse perte mais il aura gagné bien + avant.

En général, les variations sont inférieures mais rien ne nous empêche de prévoir une perte supérieure mais dans ce cas on peut se retrouver coincé un moment et perdre + d’argent que de prendre une perte de 550 points et de repartir.

A votre disposition pour échanger et bon week-end à vous tous.

Yann.

defparam cumulateorders=false

defparam preloadbars = 500

n=1

perte=550

xx=69

yy=30

J=350

pz=3

py=12

x=169

if (dayofweek=6 or dayofweek=7) or (time<091500 or time>203000) or (time>153000 AND time<160500)or (time>194500 AND time<195500) then

journee=0

else

journee=1

endif

if (highest[288](close)-close)>(close/80) or (highest[144](close)-close)>(close/85) then

sensvente=1

else

sensvente=1

endif

if (close-highest[288](close))>(close/80) or (close-highest[144](close))>(close/85) then

sensachat=0

else

sensachat=1

endif

if close>(highest[30](close)*0.99911) then

achatextrem=0

else

achatextrem=1

endif

if close<(lowest[36](close)*1.00041) then

venteextrem=0

else

venteextrem=1

endif

cloture=((highest[117](close)+lowest[117](close))/2)

if close<(cloture-50) then

cloturevente=0

else

cloturevente=1

endif

if time<140000 and close>(cloture) then

clotureachat=1

else

clotureachat=1

endif

if (time>120000 and time<142500) or (time>100000 AND time<112000)or (time>175000 AND time<183000) or time>204000 or (open[4]>close[4] and open[3]>close[3] and open[2]>close[2] and open[1]<close[1]) then

stopventetemps=0

else

stopventetemps=1

endif

if (open[4]<close[4] and open[3]<close[3] and open[2]<close[2] and open[1]>close[1]) then

stopachattemps=1

else

stopachattemps=1

endif

ratio=4.6

gain2=(highest[14](close)-low)

if gain2<0 then

gain=(gain2*-1)/ratio

else

gain=gain2/ratio

endif

if gain>=22 then

gain=78

endif

if gain<=2.7 then

gain=2.8

endif

if gain>=2.8 and gain<=9.4 then

gain=94

endif

SET TARGET PROFIT gain

SET STOP LOSS perte

nombre=12

couleur=7

descente=0

for z=1 to nombre do

if open[z]>close[z] then

descente=descente+1

endif

next

if descente>=couleur then

achatbougie=0

else

achatbougie=1

endif

montee=0

for y=1 to nombre do

if open[y]<close[y] then

montee=montee+1

endif

next

if montee>=couleur then

ventebougie=0

else

ventebougie=1

endif

nombre2=7

couleur2=6

descente2=0

for z2=1 to nombre2 do

if open[z2]>close[z2] then

descente2=descente2+1

endif

next

if descente2>=couleur2 then

achatbougie2=0

else

achatbougie2=1

endif

montee2=0

for y2=1 to nombre2 do

if open[y2]<close[y2] then

montee2=montee2+1

endif

next

if montee2>=couleur2 then

ventebougie2=0

else

ventebougie2=1

endif

if open>highest[14](close) or open>(close[24]*1.014) then

achathaut=0

else

achathaut=1

endif

if open<lowest[17](close) or open<(close[24]/1.0028) then

ventebas=0

else

ventebas=1

endif

p=10

q=8

plusHaut = HIGHEST[p](HIGH)

plusBas = LOWEST[p](LOW)

oscillateur = (CLOSE - plusBas) / (plusHaut - plusBas) * 100

K = AVERAGE[q,6](oscillateur)

periode=34

innere = 2*weightedaverage[ round( Periode/2 ) ](close)-weightedaverage[Periode](close)

MM=weightedaverage[round(sqrt(periode))](innere)

if (close>close[50]*1.02) or (close>close[6]*1.002) or (onmarket and (tradeprice-close)>z) or ventebougie=0 or ventebougie2=0 or close<BollingerDown[20](close)+2 or ventebas=0 or cloturevente=0 or venteextrem=0 or sensvente=0 then

stopventecalcul=0

else

stopventecalcul=1

endif

if (close[50]>close*1.04) or (close[6]>close*1.005) or (onmarket and (tradeprice-close)<z) or achatbougie=0 or achatbougie2=0 or close>BollingerUp[20](close)+18 or achathaut=0 or clotureachat=0 or achatextrem=0 or sensachat=0 then

stopachatcalcul=0

else

stopachatcalcul=1

endif

i1=average[3](close)

c1=i1>i1[6]

if stopachattemps=1 and c1 and journee=1 and k<xx and mm[1]<mm and stopachatcalcul=1 then

buy n shares at market

endif

i2=average[3](close)

i3=average[5](close)

c2=i2 crosses under (I3-50)

if c2 and ((tradeprice-close)<pz) and (time>091000 and time<212000) then

sell at market

endif

periode2=18

innere2 = 2*weightedaverage[ round( Periode2/2 ) ](close)-weightedaverage[Periode2](close)

MM2=weightedaverage[round(sqrt(periode2))](innere2)

c3=i1<i1[6]

if c3 and journee=1 and k>yy and mm2[2]>mm2 and stopventecalcul=1 and stopventetemps=1 then

sellshort n shares at market

endif

c4=i2 crosses OVER (i3-10)

if c4 and (tradeprice-close)>pY and (time>091000 and time<212000) then

exitshort at market

endif

if longonmarket and (BarIndex-TRADEINDEX)>j then

sell at market

endif

if shortonmarket and (BarIndex-TRADEINDEX)>j then

exitshort at market

endif

if longonmarket and (BarIndex-TRADEINDEX)>x and (close-tradeprice)>5 then

sell at market

endif

if shortonmarket and (BarIndex-TRADEINDEX)>x and (tradeprice-close)>5 then

exitshort at market

endif

je pense que la ligne manquante est celle ci if time<195500 and close>(cloture) then

a voir

Il faut regarder le post avant le votre ou se trouve la version complète

Hello,

en parcourant en diagonale votre code, je trouve pas mal de conditions qui sont mal codée (ligne 17,43,53), et mon backtest, contrairement au votre, termine en une perte totale du capital. Il faut dire que j’ai pris une plus longue période de backtest que vous.Du coup, votre code ressemble bcp à de la sur-optimisation,…

Bonjour Stefou102, ami belge ! j’habite à côté de Lille et j’ai de la famille Belge

Ta remarque est pertinente et en effet, les 3 conditions que tu évoques sont neutralisées car je les utilise ou pas,comme des interrupteurs

Quand je vois qu’elles sont bénéfiques je mets l’interrupteur sur 1 et quand elles ne le sont pas je mets l’interrupteur sur 0

Celà me permet de ne pas avoir à les retaper à chaque fois

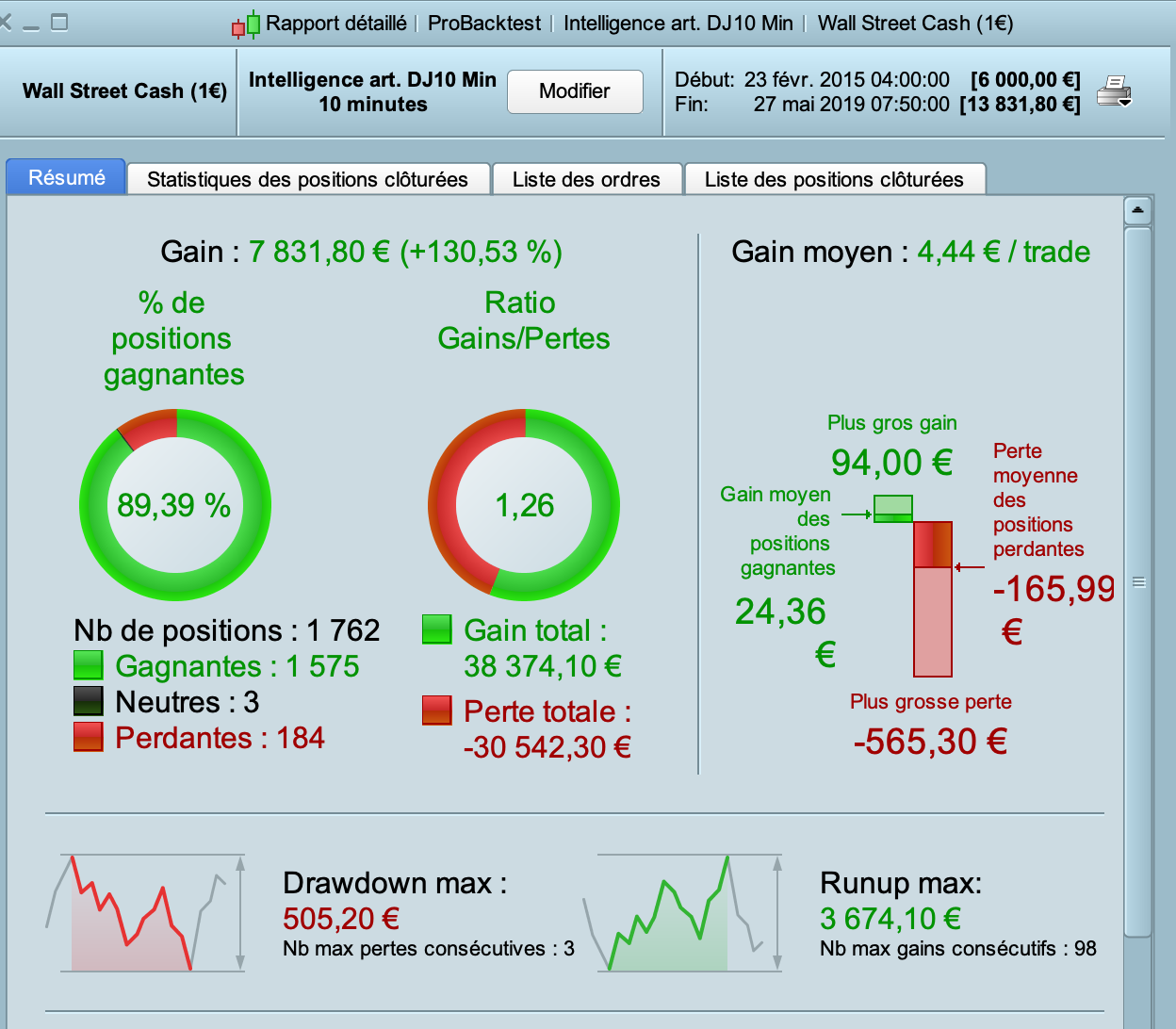

Avec l’expérience, je me suis aperçu qu’il était préférable d’optimiser les algorithmes sur une période de 1 à 3 mois maximum car l’algorithme qui fonctionne bien toute l’année n’est pas efficient, je préfère les backtester sur 3 mois environ soit 10 000 bougies de 10 minutes

Il faut donc bien mettre sur la plateforme prorealtime 10 000 puis 10 minutes sur wall street mini 1€ Cfd Cash

Idéalement il faudrait aussi remplacer en lignes 142 et 147 , “z” par “pz” car “z” varie de 1 à 12 mais j’aime bien apporter un peu d’aléas dans le gain, mais pas dans la perte

Je reste à ta disposition pour tout complément d’information

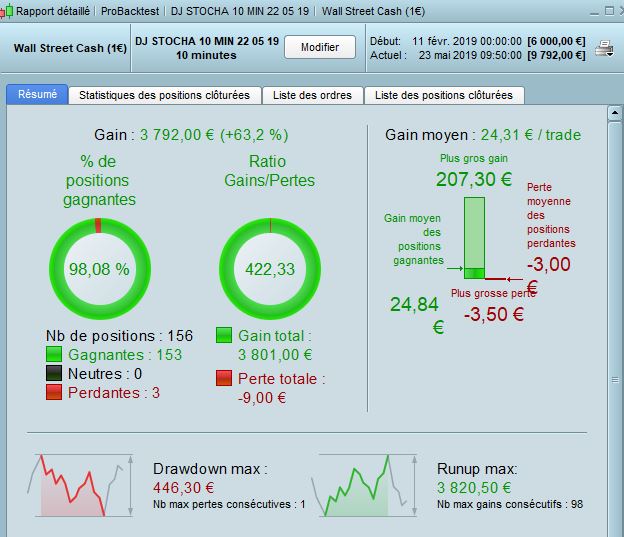

Bonjour Yannchev,

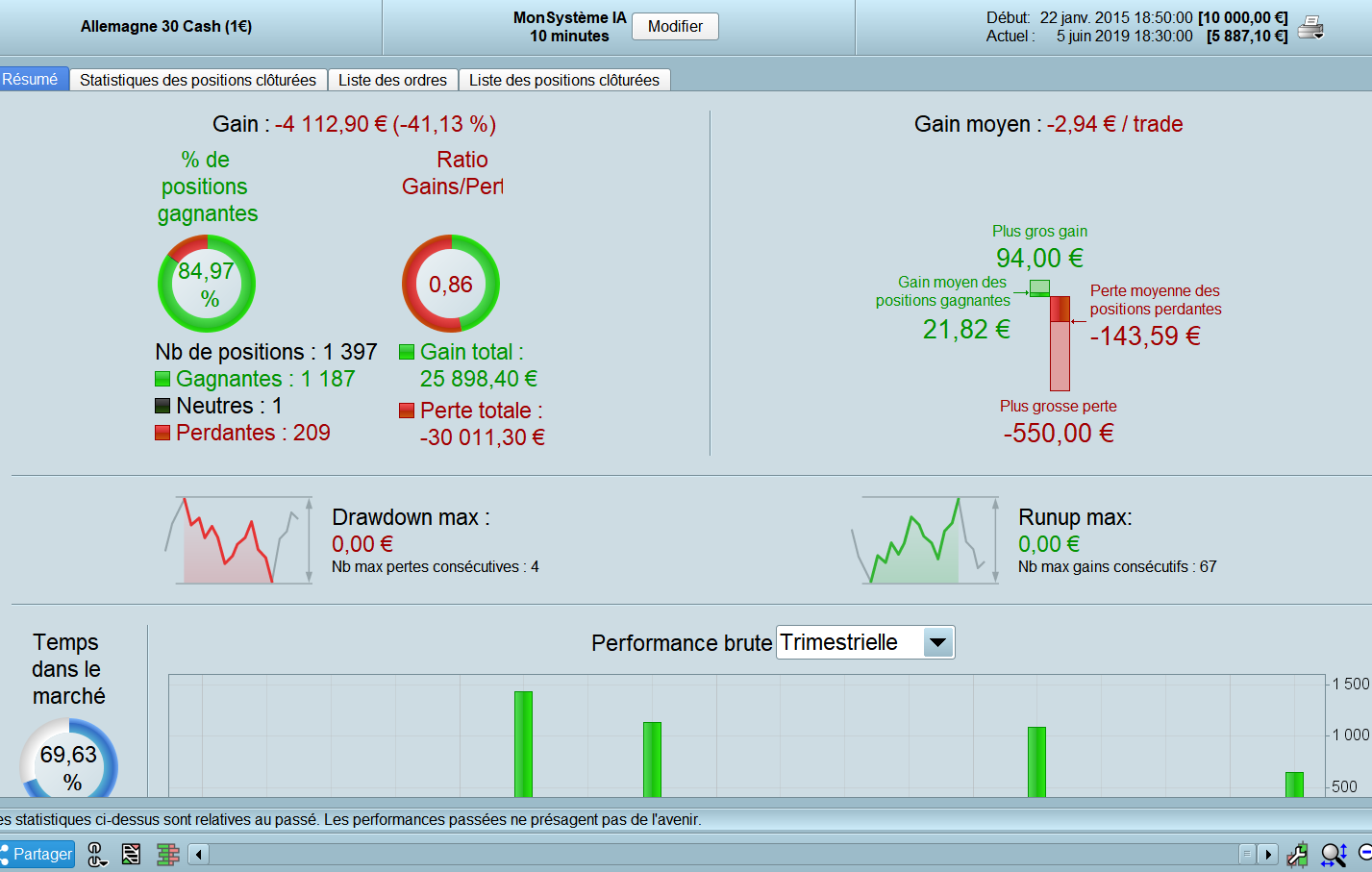

Déjà nous avons un problème, voici une capture d’écran de ton dernier code posté, les résultats ne sont pas vraiment les mêmes (spread = à 0), cela donne :

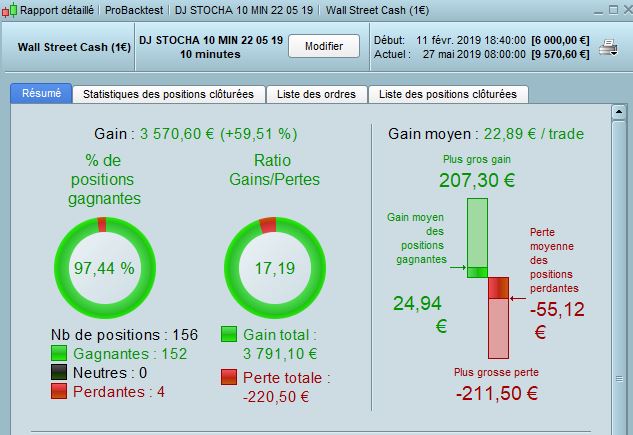

Bonjour Turame,

En effet on n’obtient pas les mêmes résultats , je viens de refaire un backtest ce 27 mai à 9h00 que je joins.

Aussi, chaque backtest est différent en fonction du point de départ

Mais là je trouve qu’il y a beaucoup d’écart par rapport à celui que je viens de faire

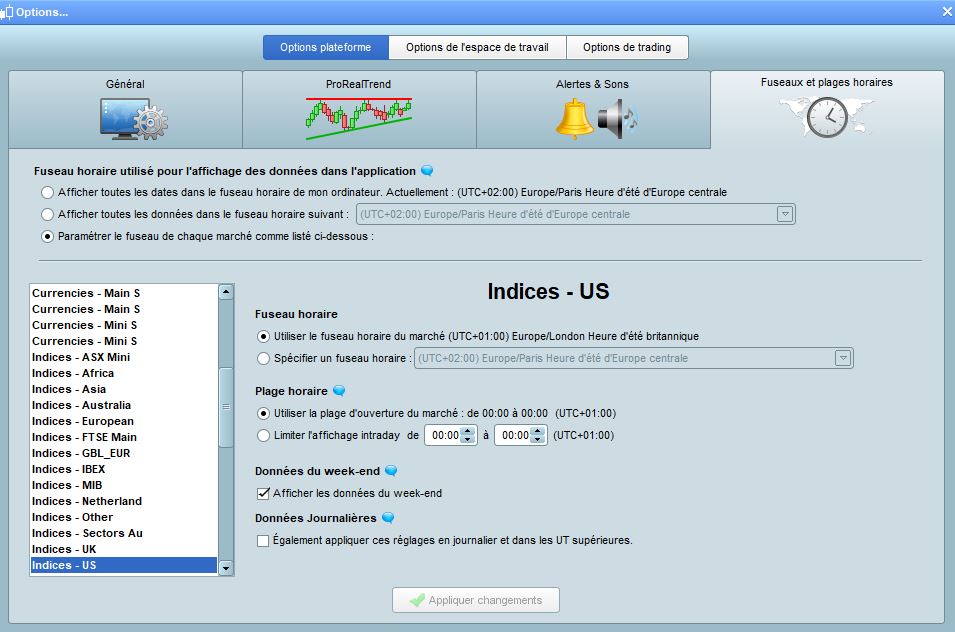

Est ce bien la dernière version complète qui est affichée sur ce post en 2ème publication ?

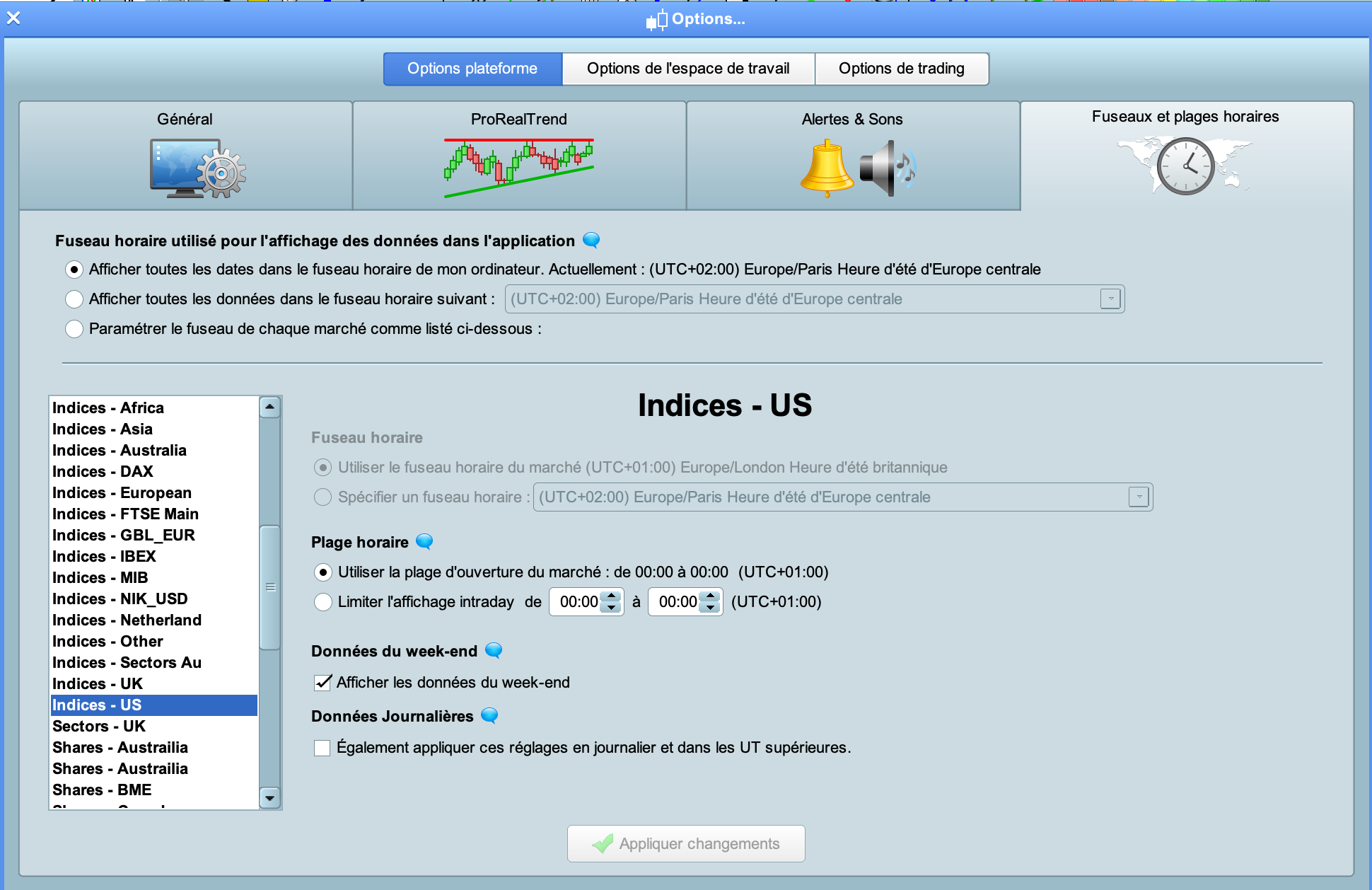

Faut vérifier si on a les mêmes réglages horaires dans le fichier attaché

Bonjour Yannchev,

Effectivement, la différence venait du fait que les réglages horaires étaient différents.

Mais quel est le bon réglage, le tien ou le mien ?

Je viens d’effectuer une simulation selon tes réglages horaires (plus avantageux que les mien).

Voici les résultats (sans aucun frais de spread)… à méditer.

Bonjour Yannchev,

Merci pour ton partage. Effectivement, travailler sur la notion de répétition et de cycle est constructif (on retrouve dans ton code des nombres de Gann). Je

m’y intéresse aussi.

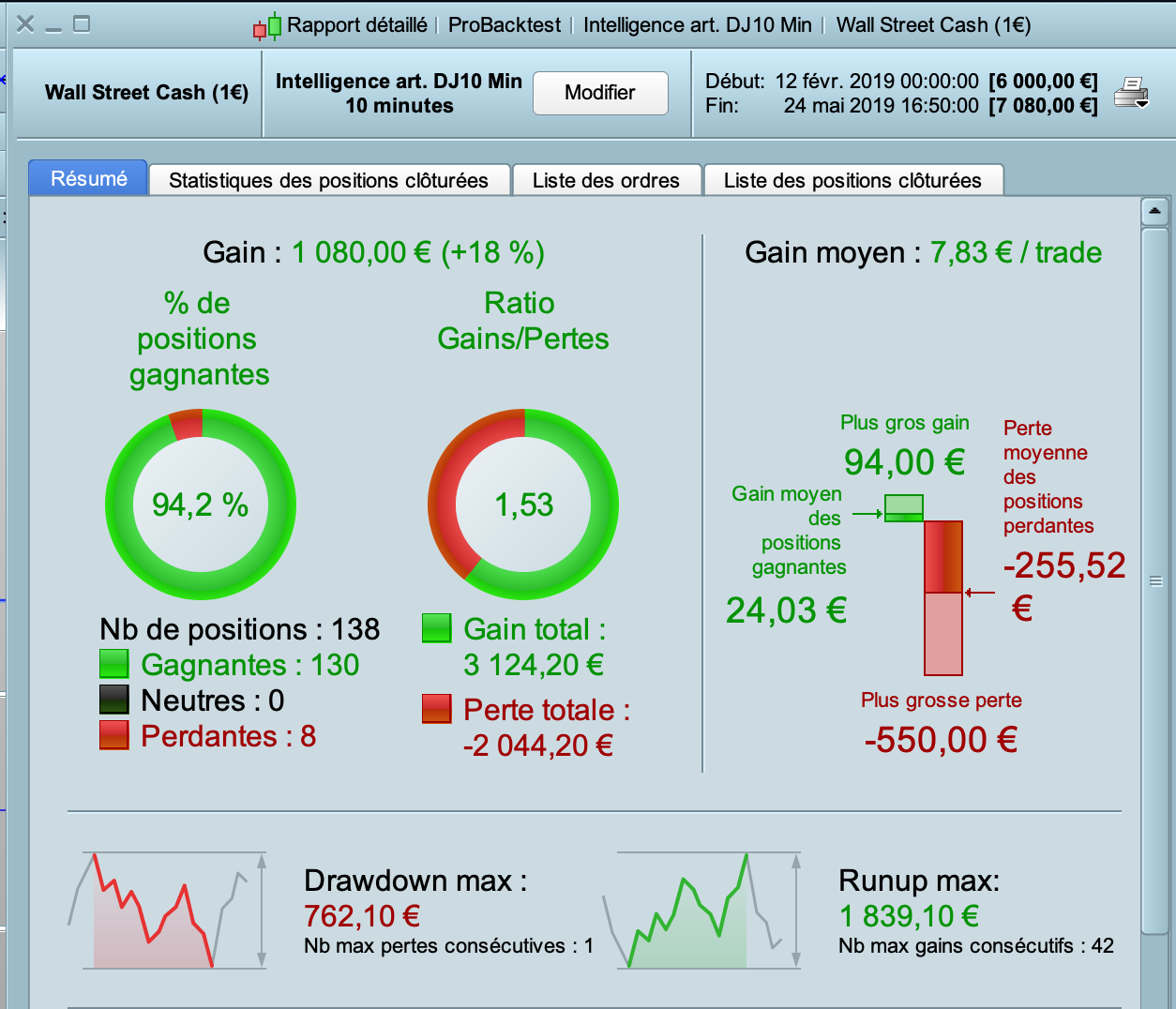

J’ai testé ton code sur le dax 30 en 10 mn, spread de 2 mais en fait le spread varie selon les horaires chez IG donc ce n’est pas totalement juste notamment pour la nuit ni la journée. Le résultat n’est pas positif sur 200 000 unités mais il est pertinent d’analyser dans le détail, de revoir peut-être le TP car dans plusieurs cas ton MFE est supérieur aux gains.

Le code est long, ne serait- ce pas possible de le simplifier aussi ?

Je reste à ta disposition pour échanger