Ciao Roberto, ho provato a sostituire set target %profit X in una banale formule (test su cfd Dax 1 ora) ma i risultati non sono equivalenti. Probabilmente c’è qualche difformità nel calcolo della percentuale rggiunta nella formula B (ho provato a cambiare close con high, ma rimangono risultati differenti).

Puoi controllare? Grazie

A)

defParam cumulateOrders = false

cLong = close crosses over average[50](close)

if not longOnMarket and cLong then

buy 1 contract at market

set stop %loss 1

set target %profit 1.5

endif

B)

defParam cumulateOrders = false

cLong = close crosses over average[50](close)

if not longOnMarket and cLong then

buy 1 contract at market

set stop %loss 1

//set target %profit 1.5

endif

targetLong = (close*1.5/100)/pointSize

If not longOnMarket then

myExit = 0

endif

If longOnMarket and (close – tradePrice) > targetLong then

myExit = tradePrice + targetLong

endif

if myExit > 0 then

sell at myExit STOP

endif

Vedo che alla riga 14 verifichi se il target è stato superato, dopodichè piazzi un ordine d’uscita STOP.Scusami, se hai già superato il terget dovresti uscire, perché attendere che il prezzo torni indietro?

Alla riga 10 dovresti usare

targetLong = (close*1.5/100) // /pointSize

in quanto lavori sul prezzo, non sui pips (nel caso di quasi tutti gli indici, al contrario del Forex, questo può non avere conseguenze, ma è logicamente inesatto).

La riga 10 devi spostarla all’interno di IF…ENDIF (cambiando anche la condizione). Inoltre l’uscita è in LIMIT, non STOP, in quanto esci ad un prezzo più vantaggioso rispetto a quello corrente al momento in cui l’ordine viene piazzato.

Anche la variabile TradeLong non serve, puoi usare solo myExit:

// A

defParam cumulateOrders = false

cLong = close crosses over average[50](close)

//

if not longOnMarket and cLong then

buy 1 contract at market

set stop %loss 1

set target %profit 1.5

myExit = close*1.015////myExit = 0

endif

//

graphonprice myEXit

// B

defParam cumulateOrders = false

cLong = close crosses over average[50](close)

if not longOnMarket and cLong then

buy 1 contract at market

set stop %loss 1

//set target %profit 1.5

myExit = close*1.015

endif

if LongOnMarket then

sell at myExit LIMIT

endif

//

graphonprice myEXit

nonostante le modifiche una differenza resta (l’ho provati su 200K unità e ci sono oltre 2K euro di differenza). Ho provato anche ad usare una volta 2 come spread ed una volta 0, ma non cambia.

Provo a fare altre verifiche e ti farò sapere.

Già a 5 k con spread = 1 si vede come nella versione B (quella senza set target…), quasi in ogni operazione profittevole si perde qualcosa.

L’importante è capire quale è più vicina all’operatività reale (quella B in ogni caso essendo svantaggiata è più attendibile).

Aggiungendo un ordine pendente di uscita immediatamente subito dopo il BUY, riduce molto il divario (testato sempre su 200K, Dax, H1).

Resta ancora una differenza. Cercherò di saperne di più.

Ecco il nuovo codice B:

// B

if not longOnMarket and cLong then

buy 1 contract at market

set stop %loss 1

//set target %profit 1.5

myExit = close*1.015

sell at myExit LIMIT

endif

if LongOnMarket then

sell at myExit LIMIT

endif

graphonprice myEXit

Ho visto che in questo modo si riduce il divario. Non capisco però il motivo, non sono due ordini limite uguali?

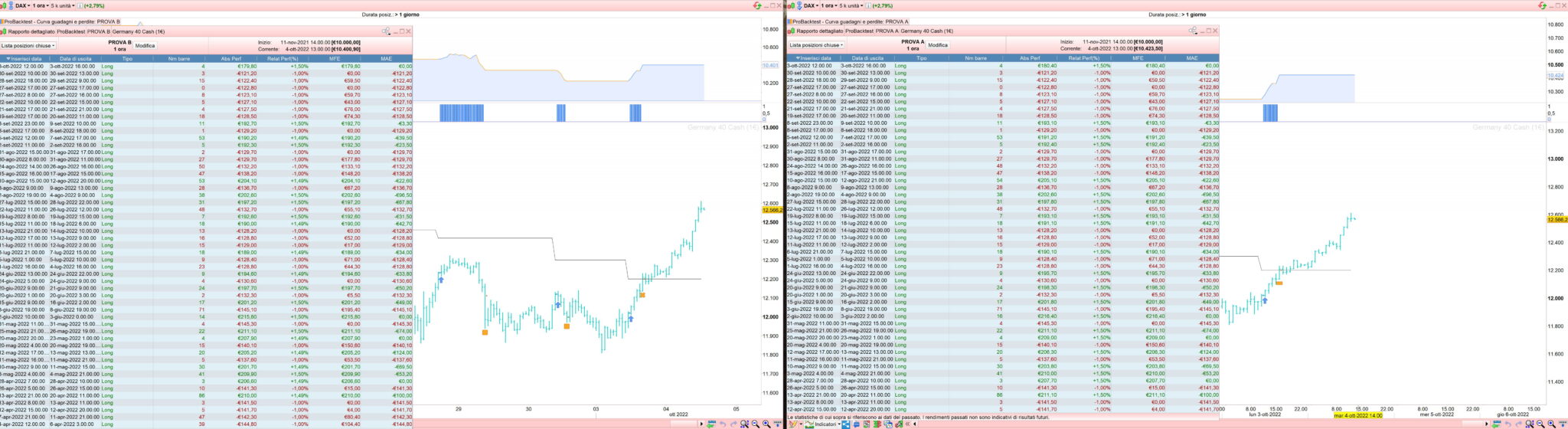

La formula con set ho visto che chiude idealmente, forse in modo irreale dal vivo, sempre con il target a 1.5%, mentre le altre formule chiudono anche a 1.49%, ma anche, ultima tua formula, a 1.64% (15 marzo 2019) o 1.44% (31 dicembre 2018). Vd immagine ( a sx l’ultima formula, a destra quella con “set”).

PS: In generale ho notato, anche in altri codici di TS complessi, che le istruziioni “set” tendono a performare nei backtest di più di quelle cotruite.