Thank you very much. Here I attach an AUD/USD optimised cross (tick by tick).

I’m from Italy too, not from Sweden.

Hi and thanks for this strategy ALE. Nice and solid foundation to keep working from and adapt to more markets etc.

Just a though regarding the minstop, correct me if wrong. I guess the variable minstop is supposed to be set in pips, but there is no pointsize multiplier in the row “if MAXPRICE–tradeprice(1)>=MINSTOP then“. Makes no difference in the indexes since pipsize is 1, but if used on currency pairs this might distort the results. I see that in the posted eurusd version of the strategy this error has not been detected, so the if condition above is never true, which makes the trailing stop consistently being set to minimum according to row “PREZZOUSCITA = MAXPRICE – MINSTOP*pointsize“.

Above comment applies to short as well as long part of the trailing stop.

Best Regards, Tedvin

ALE

ALEModerator

Master

@Alberto,

also if I’ll never use on real account the following optimization I’ve attached anothe version for AUD/USD

Thank you for your optimised AUD/USD. I’ll try to search a better version, but I think this cross is a hard one. I don’t like the declining curve at the end.

Are you running this automated strategy live with any asset?

ALEModerator

Master

Hello Alberto,

I’m busy with others but I could consider major market like Nasdaq, Dax etc. in real

Hello

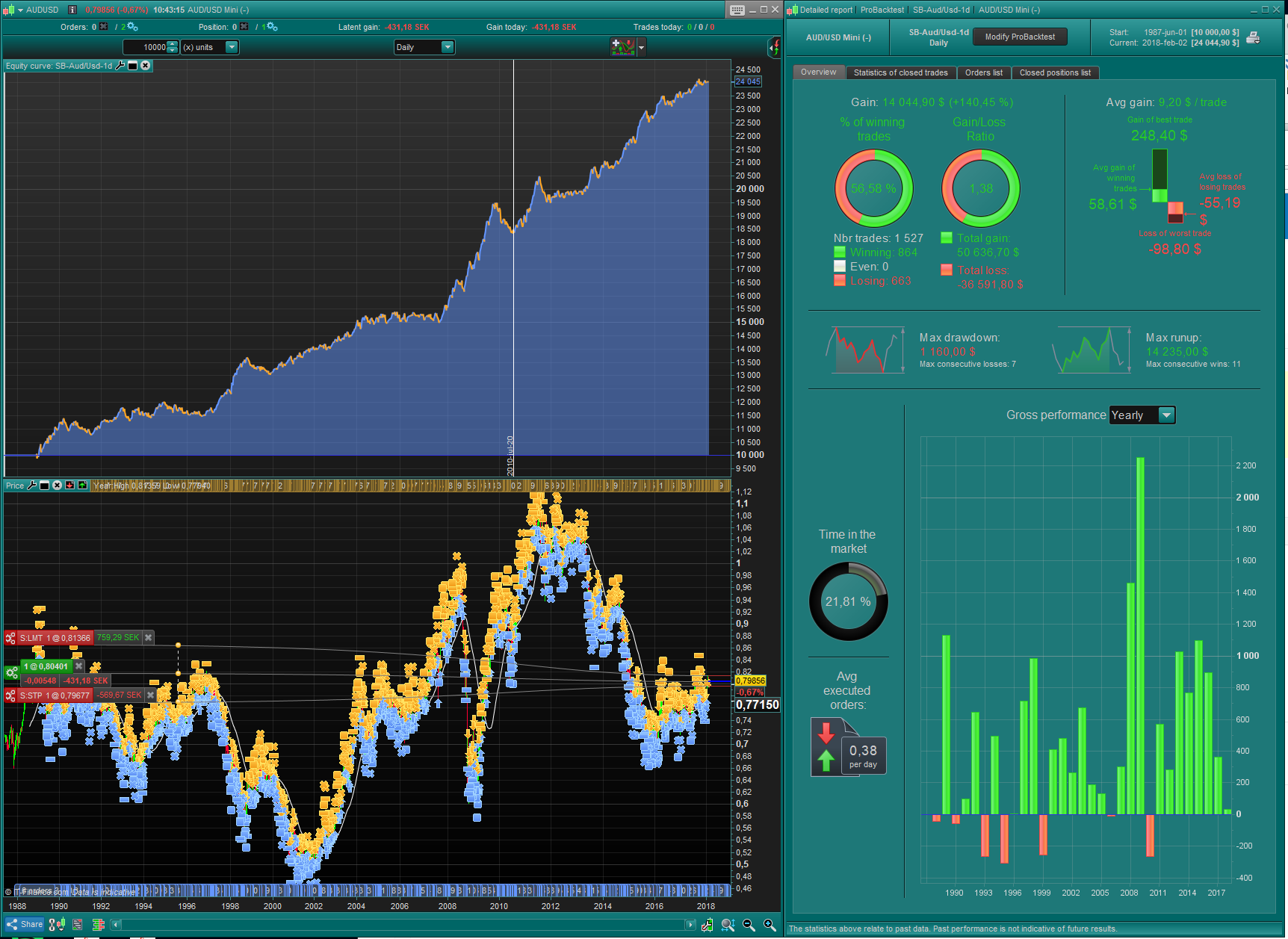

I´ve been testing this code on some different fx pairs and some other markets and have gotten some amazing results. Is this code really legit? I see that many of the trades are closed within the first bar (0 bar). But tested with t-b-t this shouldn´t be a problem.

Can´t see anything that looks non legit except for the result… What do you think?

You can see some of my backtest down below. I´ve optimized on the latest 5-10 years and the rest is OOS.

Are you sure you were testing them tick by tick? In ProRealTime the tick-by-tick test starts from 2010, whereas your screenshots start previously.

I´m getting the same result in tick by tick.

Sorry for dubbel posting but here´s the code for aud/Usd for example. Optimized from 2010-07-20 to 2018-02-01 (see the line in the picture). 1988-2010 is all oss.

DEFPARAM CumulateOrders = FALSE

ONCE avgEnterEnabled = 2 //Moving Average Entry Filter - 0 OFF, 1 ON

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE takeprofit = 1.2 // Take Profit %

ONCE stoploss = 0.9 // Stop Loss %

ONCE trailingstoplong = 23 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 9 // Trailing Stop Atr Relative Distance

ONCE barlong = 1 // Exit Time Long

ONCE barshort = 3 // Exit Time Short

ONCE atrtrailingperiod = 380 // Atr parameter Value

ONCE minstop = 3 // Minimum Trailing Stop Distance

// MOVING AVERAGE - Parameter

ONCE avgLongPeriod = 200 // 100

// Smoothed Bollinger %b indicator - Parameters

ONCE period = 3

ONCE TeAv = 1

ONCE SveEnterLongThreshold = 35

ONCE SveEnterShortThreshold = 65

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

//--------------------------------------------------------------------------------------------------

// FILTER SETTINGS

//--------------------------------------------------------------------------------------------------

//MOVING AVERAGE

longAvg = Average[avgLongPeriod] (close)

avgFilterEnterLong = (close>longAvg OR NOT avgEnterEnabled)

avgFilterEnterShort = (close<longAvg OR NOT avgEnterEnabled)

//Smoothed Bollinger %b indicator

haOpen = ((Open[1]+High[1]+Low[1]+Close[1])/4 + (Open[2]+High[2]+Low[2]+Close[2]))/2

haC = ((Open+High+Low+Close)/4 + haOpen + Max(high,haOpen) + Min(low,haOpen)) /4

TMA1 = tema[TeAv](haC)

TMA2 = tema[TeAv](TMA1)

Diff = TMA1-TMA2

ZlHA = TMA1+Diff

percb = (tema[TeAv](ZLHA)+2*STD[period](tema[TeAv](ZLHA))-weightedaverage[period](tema[TeAv](ZLHA))) / (4*STD[period](tema[TeAv](ZLHA)))*100

SveFilterEnterLong = (percb < SveEnterLongThreshold )

SveFilterEnterShort = (percb > SveEnterShortThreshold )

// STRATEGY

//--------------------------------------------------------------------------------------------------

IF NOT LongOnMarket AND avgFilterEnterLong AND SvEFilterEnterLong THEN

BUY 1 CONTRACT AT MARKET

ENDIF

IF NOT ShortOnMarket AND avgFilterEnterShort AND SveFilterEnterShort THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

IF POSITIONPERF<0 THEN

IF LongOnMarket AND BARINDEX-TRADEINDEX(1)>= barLong THEN

SELL AT MARKET

ENDIF

ENDIF

IF POSITIONPERF<0 THEN

IF shortOnMarket AND BARINDEX-TRADEINDEX(1)>= barshort THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

SET STOP %LOSS stoploss

SET TARGET %PROFIT Takeprofit

///GRAPH TGL

Compliments for your optimisation. Much better than mine. I’ve tried it and I get more or less the same results.

I’m optimising other assets, but it’s a little difficult. There are a lot of variables to set in advance.

Good job guys! Nice to see you are using OOS validation for your optimized variables settings.

@ale congratulations for the strategy

Thanks Alberto and Nicolas.

The only problem I´ve noticed so far is that the code dosen´t seem to like to have a open position over the weekend. As you can see in the picture below the code is turning it self off.

Does anyone have an idea of what the problem could be?

Cheers

ALEModerator

Master

This problem is over this strategy, i’d like to know why