ALE

ALEModerator

Master

Hello Maxgomma

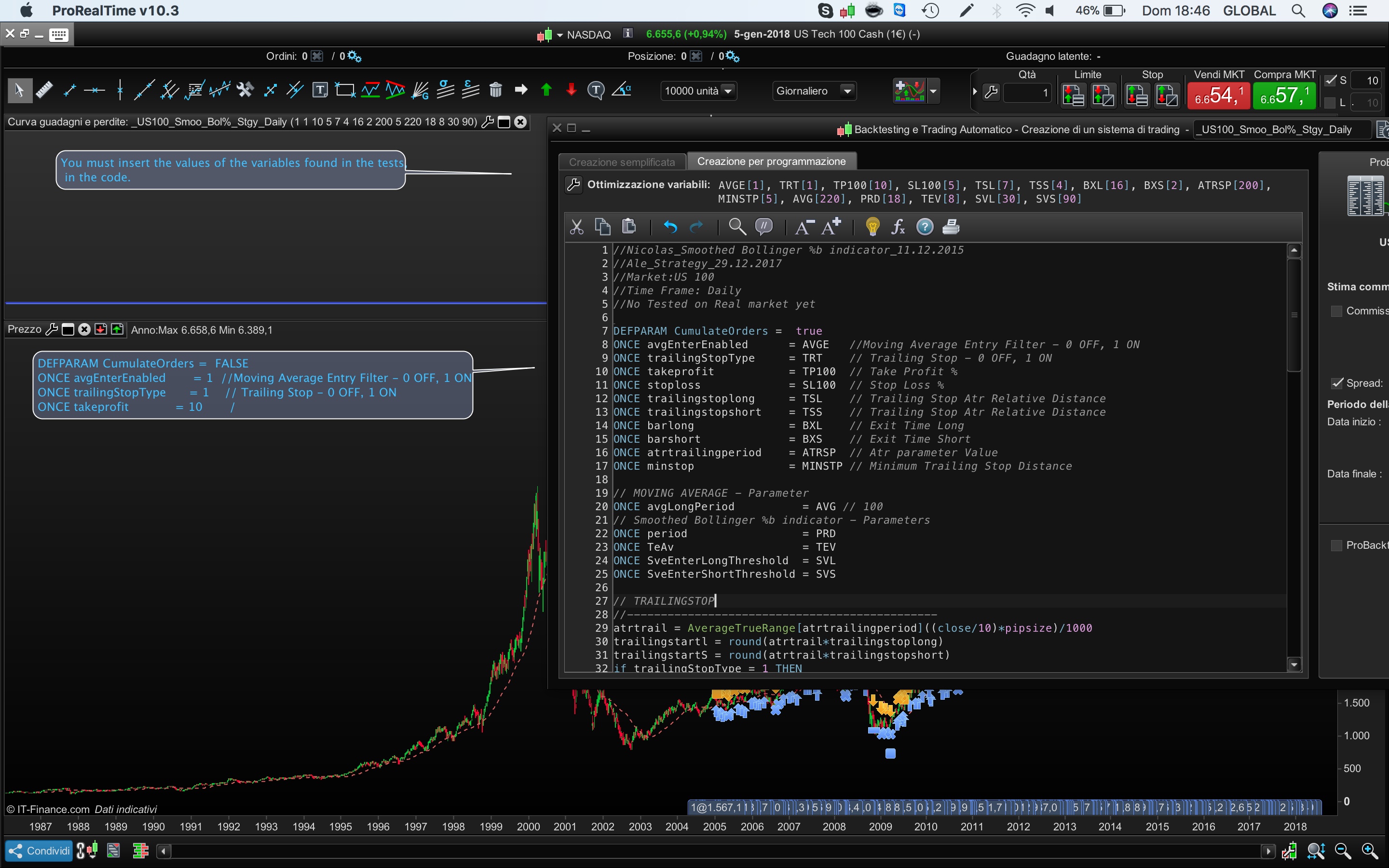

You must insert the values of the variables found in the tests, in the code.

I’ve attached picture with description.

Grazie Ale..ma per il Graph in fondo al codice? come devo cambiarlo?

Hi maxgomma

I think it would benefit you tons (many $$$$ maybe!? :)) if you read the PRT Help Manuals, or at least read the respective pages that contain information on whatever topic you don’t understand.

Follow the link as shown in attached or below.

https://www.prorealtime.com/en/partner_redirect.phtml?pr_page=help/quick_tour&pr_from=PRT_IG&version=v10.3.20171104030008

Hope this helps so you can move on and make $$$$$? 🙂

GraHal

ALEModerator

Master

@MAXGOMMA,

That Graph function makes the value of Variable visible on the Graph to check it

wp01

wp01Participant

Master

@Ale,

Thank you very much for your bollinger strategy.

One question regarding the Dow. You are using three additional variables which do not return in the code.

For the result in the backtest it doesn’t matter if i remove them, but you seem to have thought about it to add them, otherwise they wouldn’t be there.

My question is: what is the purpose of these variables and what were your thoughts about it?

Attached a copy of the variables.

Thanks in advance for your reply.

Kind regards,

ALEModerator

Master

Very Very Sorry just yesterday I’ve noted that variables, but you must cancel it, they are only for the indicator.

I can suggest to all to look for other indicator to add in the strategy to increase number of operations, like CCI or RSI or CUMMULATIVE RSI OR UNIVERSAL … etc..

Pere

PereParticipant

Veteran

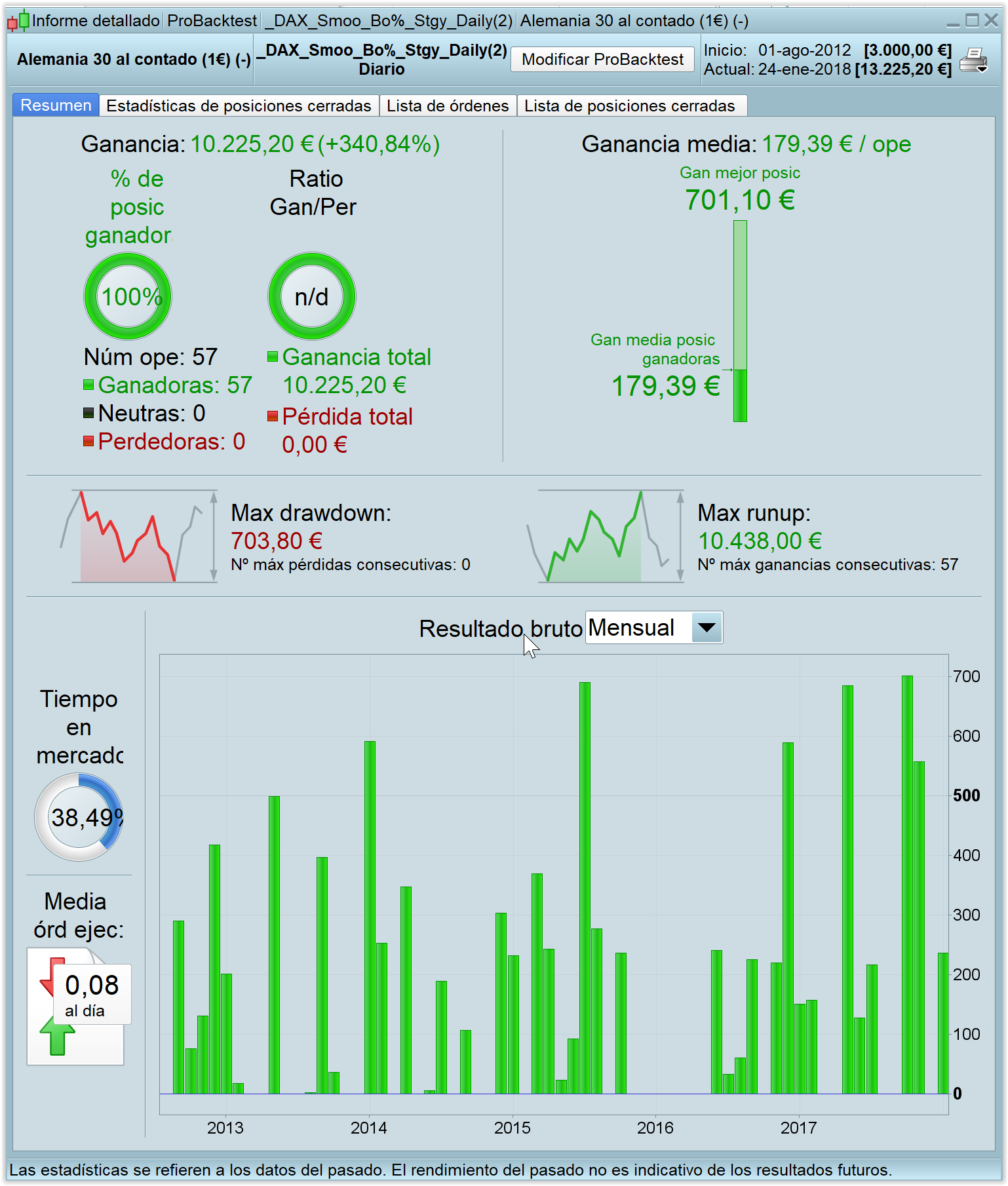

Hi. Please find hereby my optimized DAX strategy. Results are nice.

Hi Ale, thanks for sharing the strategy.

It looks really consistent, although I am very cautious of strategies with so many ‘optimized’ variables, the danger of curve fitting becomes very real here.

Have you tried testing using WF analysis or maybe across different instruments using the same variables?

I will do some WF analysis and Monte Carlo and see what I get.

ALEModerator

Master

Hello juanj

on daily timeframe, on a long history test, many variables to managed position are correct. The variables could be change without big problem.

please study this template with others pattern also, and let me know your impression, Im happy to work together

ALEModerator

Master

@pere

your optimization was good in the past, but result out of the sample it will change , so try to test it since 2000 and work around your optimization, consider an average of value of variables found by WF analysis

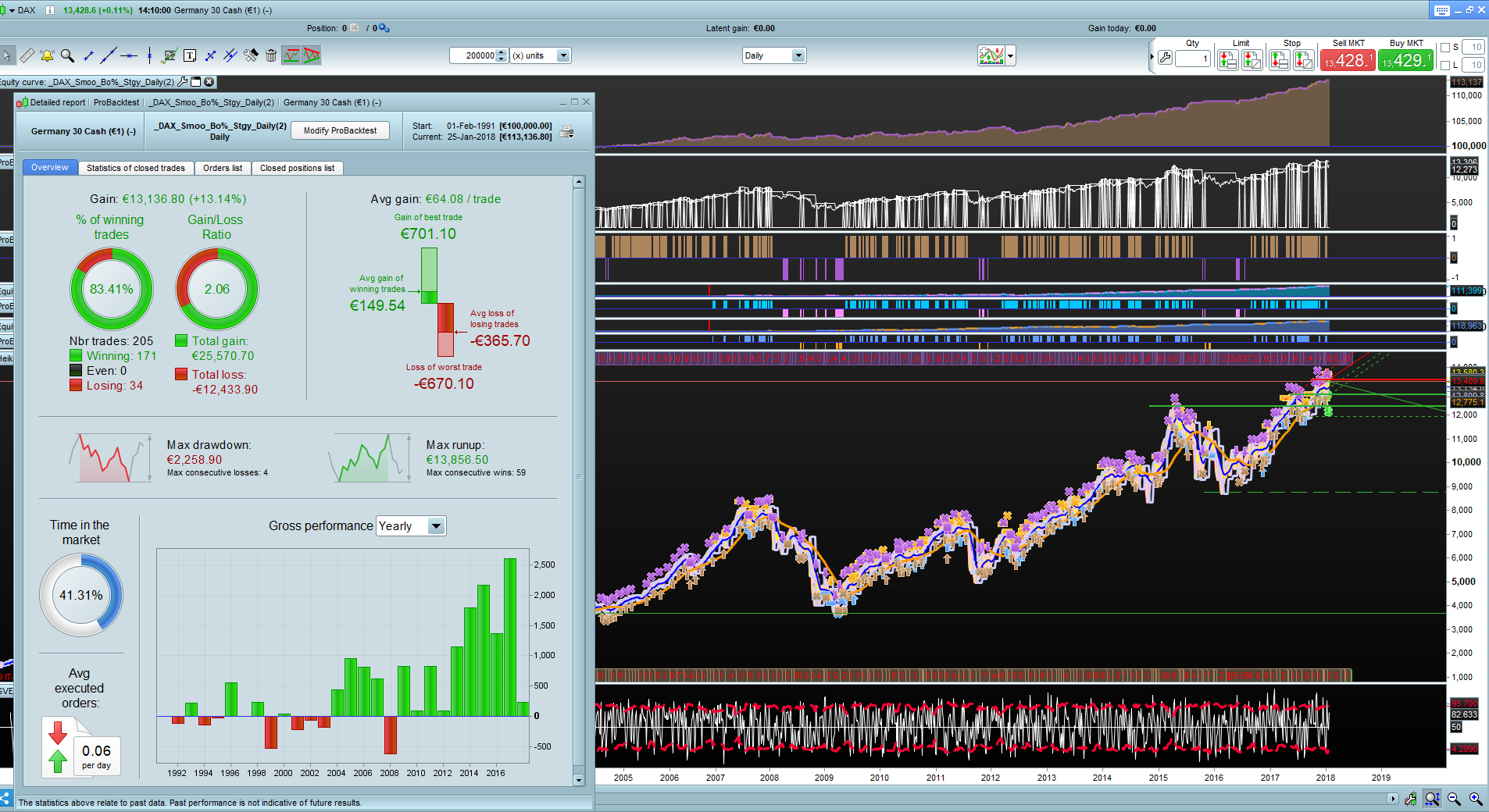

Thank you Pere … looks good, this could be the one for my grandchildren Trust Fund!!! 🙂 🙂

Please might somebody be able to post Detailed Report and Equity Curve over 200,000 bars on the .itf attached (it runs real fast!)?

Thank You

GraHal

ALEModerator

Master

@Pere@all

Pere’s optimization seem to work well!

goood!

Optimisation

Hi Ale, thanks for your contribution.

I'd like to test your trading system on more assets, but there're many variables.

What method do you follow to optimise this kind of trading system?

ALEModerator

Master

@Alberto

1 Observe the market, and establish Take profit, stop loss, trailing stop and set them.

2 Set trailing stop distance for forex

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)

or Set trailing Stop for indices

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

3 Set Broker’s Minimum stop distance for the market

4 Set moving average filter period to a real value of compromise, you will optimize later around 200 period

5 Set exit time to a real value of compromise, you will optimize later

5 Set Indicator Smooted Bollinger with the original value, you will optimize later

// variables :

// period = 18

// TeAv = 8

Then observe results and on the graph and look for the best real compromise avoid overfitting