Nel codice trovato in libreria (allego) ho aggiunto un loss e profit, ma essendo il TF giornaliero , gli stessi operano a fine giornata e il drawdown è veramente alto. Vorrei limitarlo agendo sul loss e profit che dovrebbero agire dentro la candela, ma non so se è possibile.

Grazie a chi mi può aiutare.

//Universal XBody STrategy

// instrument: DAX

// timeframe : Daily

// Spread: 4

// created and coded by davidelaferla

//————————————————————————-

//————————————————————————-

defparam cumulateorders=false

//***********************************************************************************************************

N = 1

//—————— SYSTEM VARIABLES—————————————

//CAC40 Values: ——————————————– Ottimization info

period=per// Optimize best value for each Symbol, range=1-1000, with step=1

mode=md// Optimize the best trading mode , range=1-4, with step=1

invertsignal=inv// 1=positive signal, -1=negative signal, range=-1-1, with step=2

//***********************************************************************************************

//—————— SYSTEM FILTER—————————————

filter1=fl1// to set after the variable optimization, range=1-100, with step=1

filter2=fl2// to set after the variable optimization, range=0-100, with step=1

//—————— INDICATOR —————————————

body=close-open

var=(body-body[1])

sumvar=summation[period](var)

if sumvar>filter1*pipsize then

green=(sumvar)

endif

if sumvar<-filter2*pipsize then

red=(sumvar)

endif

if mode=1 then

c1=red<red[1]

c2=green>green[1]

endif

if mode=2 then

c1=red>red[1]

c2=green<green[1]

endif

if mode=3 then

c1=red<red[1]

c2=green<green[1]

endif

if mode=4 then

c1=red>red[1]

c2=green>green[1]

endif

if c1 then

signal=1*invertsignal

elsif c2 then

signal=-1*invertsignal

endif

// Conditions for entering long positions and exit short positions

IF signal>0 then

BUY n contract AT market

ENDIF

// Conditions for entering short positions and exit long positions

IF signal<0 THEN

SELLSHORT n CONTRACTs AT market

SET STOP LOSS l*AverageTrueRange[10](close)

SET TARGET PROFIT p*AverageTrueRange[12](close)

ENDIF

secondo me l’unico modo è inserire un TF diverso sulla parte di esecuzione e inserire un timeframe giornaliero sull’indicatore, per esempio:

//Universal XBody STrategy

// instrument: DAX

// timeframe : Daily

// Spread: 4

// created and coded by davidelaferla

//————————————————————————-

//————————————————————————-

defparam cumulateorders=false

Timeframe ( 1 day, updateonclose)

//***********************************************************************************************************

N = 1

//—————— SYSTEM VARIABLES—————————————

//CAC40 Values: ——————————————– Ottimization info

period=per// Optimize best value for each Symbol, range=1-1000, with step=1

mode=md// Optimize the best trading mode , range=1-4, with step=1

invertsignal=inv// 1=positive signal, -1=negative signal, range=-1-1, with step=2

//***********************************************************************************************

//—————— SYSTEM FILTER—————————————

filter1=fl1// to set after the variable optimization, range=1-100, with step=1

filter2=fl2// to set after the variable optimization, range=0-100, with step=1

//—————— INDICATOR —————————————

body=close-open

var=(body-body[1])

sumvar=summation[period](var)

if sumvar>filter1*pipsize then

green=(sumvar)

endif

if sumvar<-filter2*pipsize then

red=(sumvar)

endif

if mode=1 then

c1=red<red[1]

c2=green>green[1]

endif

if mode=2 then

c1=red>red[1]

c2=green<green[1]

endif

if mode=3 then

c1=red<red[1]

c2=green<green[1]

endif

if mode=4 then

c1=red>red[1]

c2=green>green[1]

endif

if c1 then

signal=1*invertsignal

elsif c2 then

signal=-1*invertsignal

endif

Timeframe ( 1 hour, default)

// Conditions for entering long positions and exit short positions

IF signal>0 then

BUY n contract AT market

ENDIF

// Conditions for entering short positions and exit long positions

IF signal<0 THEN

SELLSHORT n CONTRACTs AT market

SET STOP LOSS l*AverageTrueRange[10](close)

SET TARGET PROFIT p*AverageTrueRange[12](close)

ENDIF

da adattare i valori di AverageTrueRange, perchè lavoranso ull’orario, quidni da moltiplicare per 24 presumo

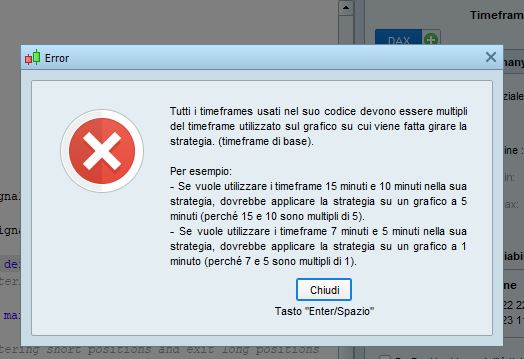

Lo sto provando, ma mi da l’errore che allego

Devi usare un TF di 1 ora o minore (però se minore, bisogna che 60, che sono i minuti di un’ora ne siano multipli).