Hi all

I downloaded the Gann Market Model Strategy from the library and edited out the Probacktest code so as to use it as a screener. I also added daycount code that Nicolas assisted me with a while back but can not get it to count. I only get 1(one) all the time for the daycount result. This daycount code works perfectly on other screeners that I have and the code for the “daycount” part is exactly the same.

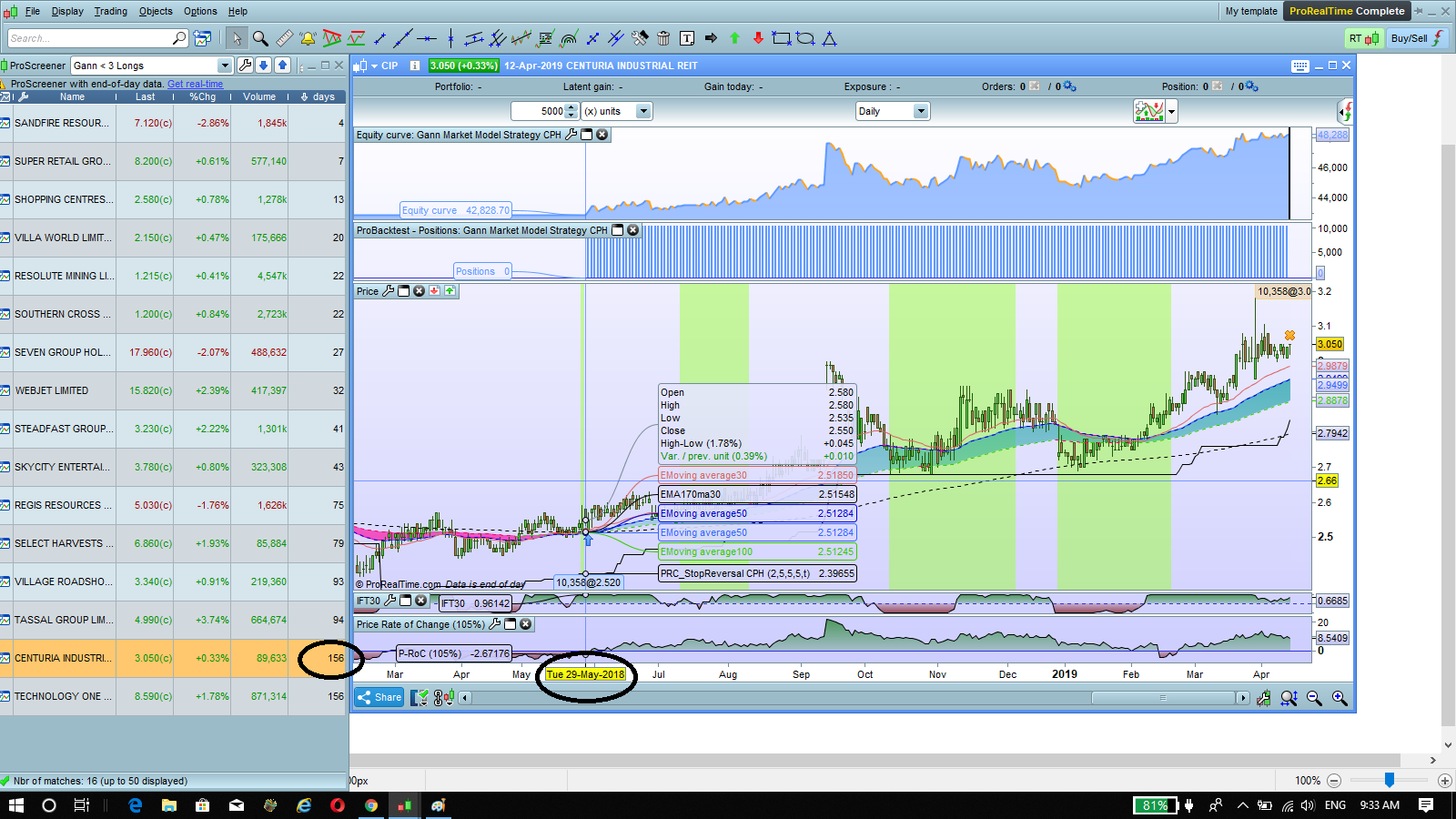

The edited code is as follows and a screen shot of the results with a circled result clearly not matching the Strategy results. Have poured over this and do not know what is wrong. Any help greatly appreciated.

Thanks

Chris

———————————————————

//short term

a1= ExponentialAverage[50](high)[1]

b1=ExponentialAverage[50](low)[1]

if customclose > a1 then

c1 = 1

Else

IF customclose < b1 then

c1=-1

endif

ENDIF

if c1= -1 then

D1 = a1

ELSE

D1=b1

endif

a2= ExponentialAverage[100](high)[1]

b2=ExponentialAverage[100](low)[1]

if customclose > a2 then

c2 = 1

Else

IF customclose < b2 then

c2=-1

endif

ENDIF

if c2= -1 then

D2 = a2

ELSE

D2=b2

endif

a3= ExponentialAverage[200](high)[1]

b3=ExponentialAverage[200](low)[1]

if customclose > a3 then

c3 = 1

Else

IF customclose < b3 then

c3=-1

endif

ENDIF

if c3= -1 then

D3 = a3

ELSE

D3=b3

endif

if D1 < close then

result = 1

else

result = 0

endif

if D2 < close then

resulta = 1

else

resulta = 0

endif

if D3 < close then

resultb = 1

else

resultb = 0

endif

c10 = (result + resulta + resultb)

//Screen for entry condition and start daycount

if c10 > 2 THEN

resultL = 1

daycount = 0

endif

// exit condition

if c10 < 3 THEN

resultL = 0

endif

//count days trade open

once daycount = 0

IF resultL = 1 and savedate<>Date THEN

daycount = daycount + 1

savedate = Date

ENDIF

screener[resultL] (daycount as "days")

—————————————————

You can try this version, I changed a bit the way you are finding the start of the signal “resultL”:

//short term

a1= ExponentialAverage[50](high)[1]

b1=ExponentialAverage[50](low)[1]

if customclose > a1 then

c1 = 1

Else

IF customclose < b1 then

c1=-1

endif

ENDIF

if c1= -1 then

D1 = a1

ELSE

D1=b1

endif

a2= ExponentialAverage[100](high)[1]

b2=ExponentialAverage[100](low)[1]

if customclose > a2 then

c2 = 1

Else

IF customclose < b2 then

c2=-1

endif

ENDIF

if c2= -1 then

D2 = a2

ELSE

D2=b2

endif

a3= ExponentialAverage[200](high)[1]

b3=ExponentialAverage[200](low)[1]

if customclose > a3 then

c3 = 1

Else

IF customclose < b3 then

c3=-1

endif

ENDIF

if c3= -1 then

D3 = a3

ELSE

D3=b3

endif

if D1 < close then

result = 1

else

result = 0

endif

if D2 < close then

resulta = 1

else

resulta = 0

endif

if D3 < close then

resultb = 1

else

resultb = 0

endif

c10 = result and resulta and resultb

//Screen for entry condition and start daycount

if c10 and not c10[1] THEN

resultL = 1

daycount = 0

//startbar=barindex

endif

// exit condition

if not c10 THEN

resultL = 0

endif

//count days trade open

IF resultL = 1 THEN

daycount = daycount + 1

ENDIF

screener[resultL] (daycount as "days")//(barindex-startbar as "days")

I did not compared the days count with the indicator, please do.

Thanks Nicolas. That has got the daycount working (sort of???) It still does not count correctly though. I have attached 2 screen shots showing 2 stocks returning the same 156 days result in the screener.

Problem is their buy dates are about 3 months apart and the strategy shows a continuous hold for these trades. Also I have removed most of the “gann code” and put a simple moving average crossover to buy and my trailing stop to exit to simplify things for this issue.

edited – Just tried changing the long entry from moving averages “greater than” to “crosses over” and got completely different results in the screener – not even the 2 stocks I have attached were in the results. But the strategy with the “crosses over” still shows the same buy dates. what the..

Both the strategy and screener code is below.

DEFPARAM CumulateOrders = False

StopL = call "PRC_StopReversal CPH"[2,5,5,5,1]

long = ExponentialAverage[50](close) > ExponentialAverage[100](close)

IF Long and not long[1] then

BUY n shares AT MARKET

ENDIF

IF (close) < stopL THEN

SELL AT MARKET

ENDIF

StopL = call "PRC_StopReversal CPH"[2,5,5,5,1]

long = ExponentialAverage[50](close) > ExponentialAverage[100](close)

IF long and not long[1] THEN

resultL = 1

daycount = 0

ENDIF

if (close) < stopL THEN

resultL = 0

endif

IF resultL = 1 THEN

daycount = daycount + 1

ENDIF

screener[resultL] (daycount as "days")

Thanks

stuffa – please use the ‘Insert PRT Code’ button when posting code in your replies as it makes it far easier for others to read. I have tidied up your last post for you. 🙂

ProScreener has a limitation of 254 bars of history. That could be a reason of not finding the same results between the indicator, the strategy and the screener.