Hi Maz, yes you are right, it’s in yen. I think it has something to do with the ploss stoploss 70.. I have before experianced that the pipsize or pointvalue has sometimes an odd way in yen- even though it shouldn’t matter. I will take a look later.

Cheers Kasper

First, cheers to all of you who have paid interest in my topic!

And thanks a lot Maz for helping me out with turning my beginner coding into something more functional!! I’ll have a look at the changes made and try to play around with it 🙂

I’m sorry Kasper but I have no clue what could be wrong. Luckily I think you got some suggested from Maz with regards to what might be wrong.

@ Kasper on the new version from Maz you need to change the value on stoplossmode which is currently 2.

stopLossMode = 2 // 1: Static | 2: Dynamic

I got the same result at you first but when I changed to a higher value I got a positiv result.

Correction -> Try the static stop (1) instead of the dynamic

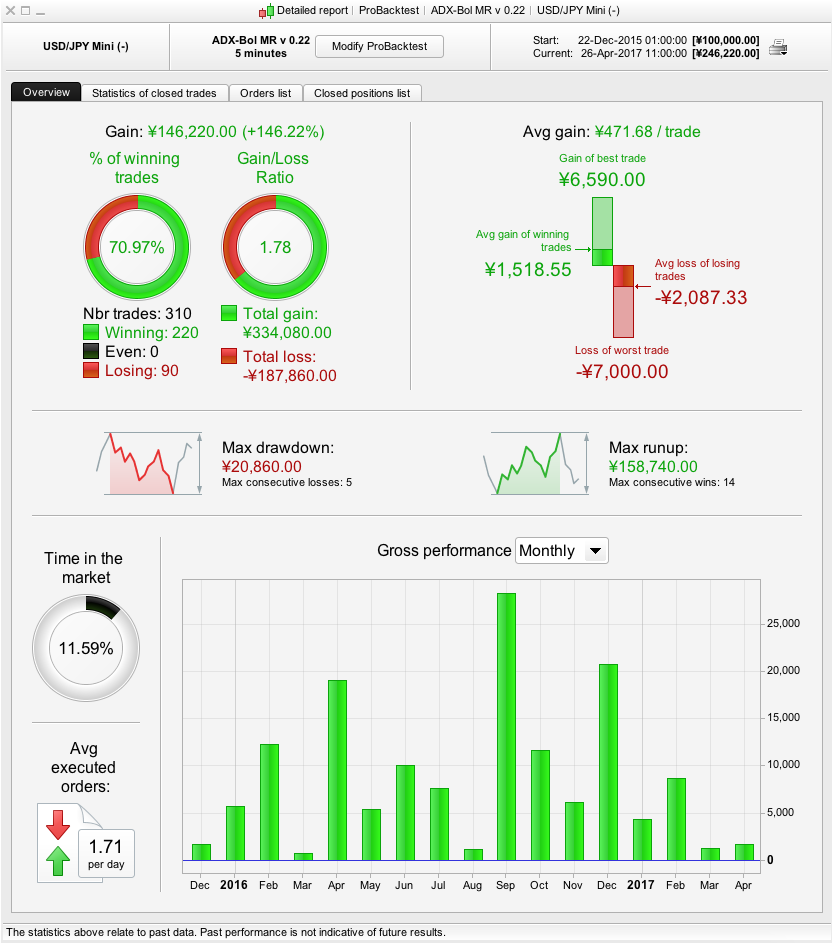

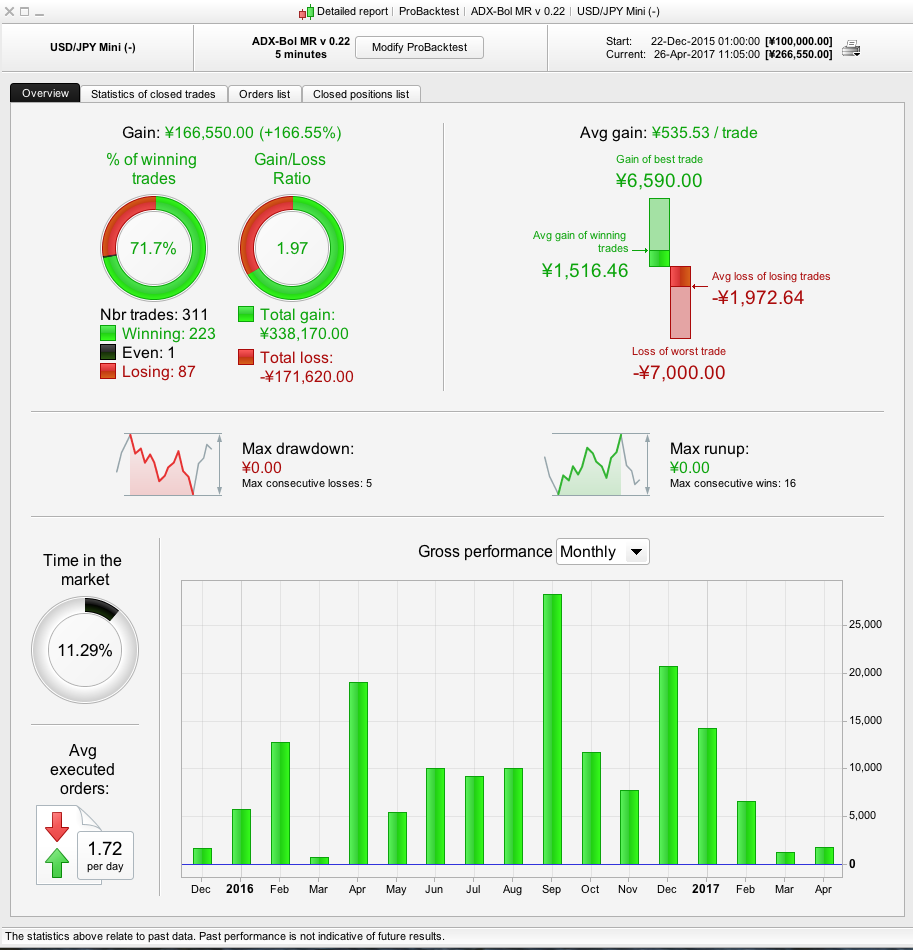

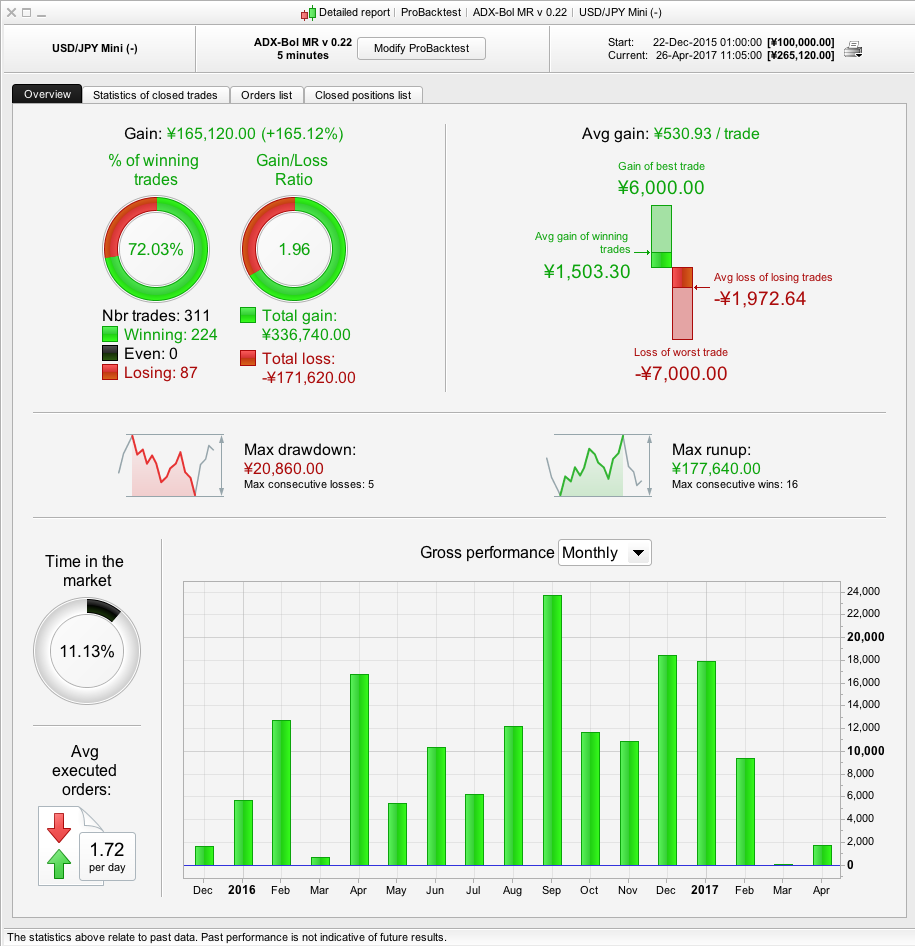

Here are the results with different kind of stops. I couldn’t get any nice result from an ATR stop. I still haven’t tried a time stop.

Maz

MazParticipant

Veteran

For the ATR stop try:

SET STOP pLOSS (atr * slATRmultiple) * pointSize

??

SET STOP pLOSS (atr * slATRmultiple) /pointsize

Now it works 🙂

This is the updated version for EURUSD 5M

Defparam Cumulateorders = false

Defparam Preloadbars = 300

//------ Trading hours-------

Starttime = 100000

Endtime = 240000

fridayEndTime = 225000

// --------Indicators------

blow = Bollingerdown[20]

bhigh = Bollingerup[20]

MA1 = Average[8]

MA2 = Average[200]

ad = adx[24]

adlevel = 14

atr = averageTrueRange[40]

slATRmultiple = 5

targetATRmultiple = 3

stopLossMode = 1 // 1: Static | 2: Dynamic | 3: DONCHIAN STOP

DC = 20

strailing = 1 // 0=off 1=on

strailingstart = 20

isLateFriday = (dayOfWeek = 5 and time >= fridayEndTime)

// ------ ENTRY CONDITIONS LONG-----

cb1 = (low < blow and close < blow)

cb2 = (MA1 > MA2)

cb3 = (currenttime > Starttime and currenttime < Endtime)

cb4 = (ad > adlevel)

c5 = cb1 and cb2 and cb3 and cb4

IF NOT Longonmarket and c5 THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// ------ EXIT CONDITIONS LONG-----

cb9 = LONGONMARKET AND ((close > bhigh) OR isLateFriday)

IF cb9 Then

sell at market

endif

// ------ ENTRY CONDITIONS SHORT-----

cs1 = (high > bhigh and close > bhigh)

cs2 = (MA1 < MA2)

cs3 = (currenttime > Starttime and currenttime < Endtime)

cs4 = (ad > adlevel)

cs6 = cs1 and cs2 and cs3 and cs4

IF NOT Shortonmarket and cs6 THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// ------ ENTRY CONDITIONS SHORT----

cs9 = SHORTONMARKET AND ((close < blow) OR isLateFriday)

IF cs9 Then

Exitshort at market

endif

//------ STOP AND TARGETS -----------

if stopLossMode = 1 then

SET STOP pLOSS 65

//SET TARGET pPROFIT 30

elsif stopLossMode = 2 then

SET STOP pLOSS (atr * slATRmultiple)/pointsize

SET TARGET pPROFIT (atr * targetATRmultiple)/pointsize

elsif stopLossMode = 3 then

e= Highest[DC](high)

f=Lowest[DC](low)

if longonmarket then

laststop = f[1]

endif

if shortonmarket then

laststop = e[1]

endif

if onmarket then

sell at laststop stop

exitshort at laststop stop

endif

endif

if strailing = 1 then

//trailing stop

trailingstop = strailingstart

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

endif

MazParticipant

Veteran

Cool. Just a thought – have you tried using combinations stop modes together? For example rather than selection stop mode 1, 2 or 3; being able to switch 1, 2 and 3 on and off separately?

Very useful Maz the timezone offset variable

It may be less confusing for everyone if the timezone offset variable is labelled and set at the World Universal Time which is called UTC. (UK is not at GMT in the Summer, but is at BST or GMT+1).

UTC overcomes confusion as it is the accepted World Standard … a Universal Time Clock.

UK is UTC+1

Kasper is UTC+2

Just a suggestion for improvement, but credit goes to you Maz for a great idea … hope others follow your lead.

GraHal

MazParticipant

Veteran

Good point @GraHal. A shared UTC offset snippet that can be plugged into anyone’s code would be useful.

sorry guys but I skipped adding the time zon for EURUSD but it’s more or less a copy past form the USDJPY.

@Maz – do you mean for example having a fixed target combined with an dynamic stop? That I’ve not yet tried.

MazParticipant

Veteran

Yes, that’s what I was referring to.

Thanks for the idea Maz.

I tried the ATR based target to the trailing stop function which showed the best result and it did improve the return. I also tried the an ATR based starting point for the trailing stop but it left the return, win-rate etc unchanged. I’ve attached the latest code.

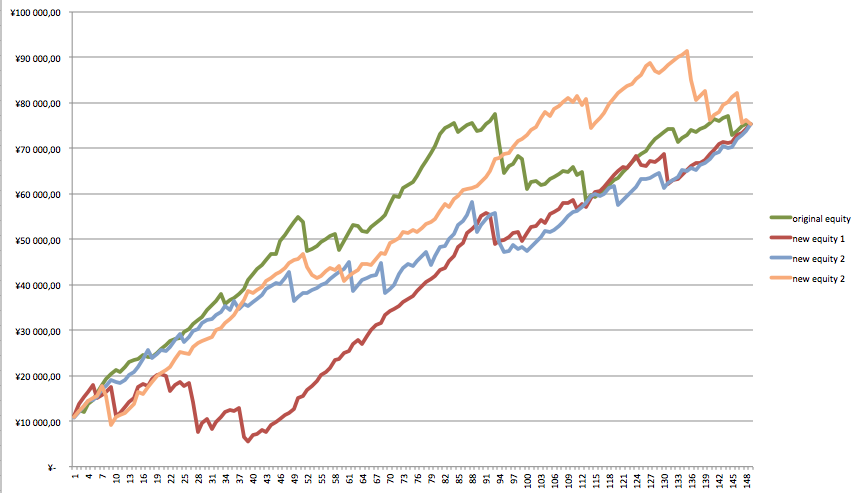

I tired to make a small monte carlo on the long side for USDJPY and the result looks like attached file.