Hey guys!

When i trade manually I use the RSI indicator with self adjusting bands tho it´s much more accurate than the standard RSI. Is there someone who whant to help me code a automatic trading with this indicator.

Something that i think had been nice is that for example: To buy long = Rsi have to be 28 and when it goes up to 31 then buy long.

And the same for short. First 72 and when it crosses under 69 then sellshort.

Anyone who has an idea how to do this? 🙂

Ok so what you are thinking about is a trading strategy that :

SELLSHORT when RSI crosses under the higher band and BUY when RSI crosses over the lower band? Am I right?

Thanks for your response Nicolas.

That´s right. I want the code to registrate when price hits rsi 32 and after that have happened and when price hits rsi 28 i want it to buy long. – Exit long when rsi hits 70.

And I want the code to registrate when price hits rsi 72 and after when it hits rsi 69 then sellshort. Exit short when rsi hits 30.

I think that I have seen a similar code somewhere before but I don´t remember where, the big difference as I see it is also that I want to do it with RSI with self adjusting band.

Ok so it’s a bit more complicated than a simple cross of the higher and lower bands. If you need to “registrate” that RSI has already visit a level before taking the decision to launch a trade, we need to make a loop in the past to see if it’s true. So what we also need is how much bars in the past would you like to fetch is the RSI has visited the 72 level for example?

Hmm… good question. I dont know. It feels like something we have to test until we come up with something reasonable. But if we start with five bars then we have something to work with.

Ok, it were just a simple question. I’ll add a variable we can change for testing purpose. It’s on my list.

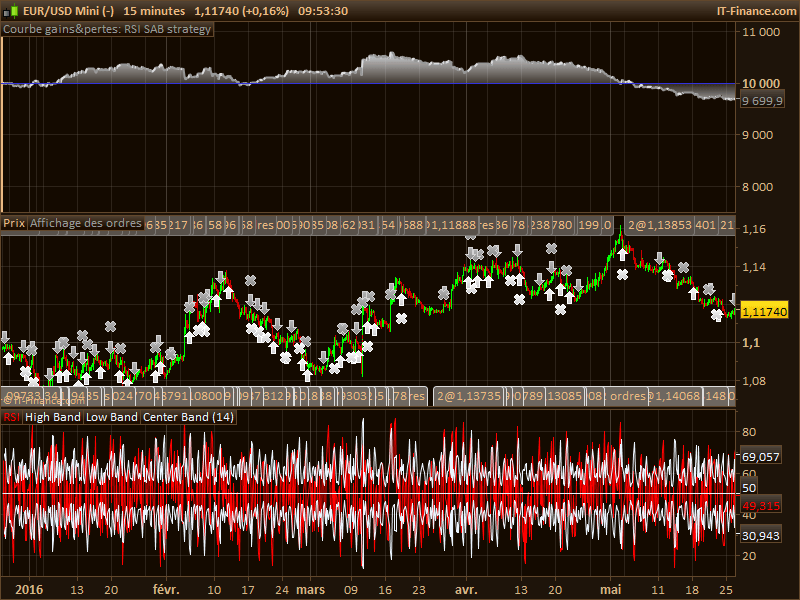

Hello, here is the code of this strategy. I like mean reversion, this is my favourite concept in trading, I’m not so in love with trend following I must admit.

Your idea to count how much bars were above or below the auto-adjusted bands which act as dynamic overbought/oversold levels is quiet interesting. Please find below and attached the code. I let you test and propose improvement if any.

defparam cumulateorders = false

//parameters

P = 14 //RSI period

dev = 1.8 //deviation factor

minbarcount = 5 //quantity of bars that the RSI needs to be above or below its bands

//RSI SAB

rsiplus = RSI[P](close)

bsup = 50+ (dev*STD(rsiplus))

binf = 50 - (dev*STD(rsiplus))

//RSI above buylevel and selllevel count

countB = 0

countS = 0

for i = 0 to minbarcount do

if rsiplus[i]>bsup[i] then

countB=countB+1

elsif rsiplus[i]<binf[i] then

countS=countS+1

endif

next

//case BUY

if rsiplus crosses over binf and countS>=minbarcount then

BUY 1 SHARE AT MARKET

endif

if longonmarket and rsiplus>=70 then

SELL AT MARKET

endif

//case SELL

if rsiplus crosses under bsup and countB>=minbarcount then

SELLSHORT 1 SHARE AT MARKET

endif

if shortonmarket and rsiplus<=30 then

EXITSHORT AT MARKET

endif

Hello again!

Sorry for late answer. Thanks alot! I´ve looked at the code and it looks good. If you switch buy-sell with sellshort-exitshort you will get a better result.

I came up with an another idea that i think will work better.

Since the self adjusting Rsi adjust its upper and lower band when the price is oversold or overbought it dosen´t really make sense to have any RSI numbers in the code. It should be something like=

//Longside

If price cross under lowerband and within 5 bars cross over lowerband then

Buy one contract

If price cross over upperband then

Sell one contract

//Shortside

If price cross over upperband and within 5 bars cross under upperband then

Sellshort one contract

If price cross under lowerband then

Exitshort one contract

What do you think about that?

Well, it would not make a lot of difference I believe, but here is the code changed accordingly to this modified exit rule:

defparam cumulateorders = false

//parameters

P = 14 //RSI period

dev = 1.8 //deviation factor

minbarcount = 5 //quantity of bars that the RSI needs to be above or below its bands

//RSI SAB

rsiplus = RSI[P](close)

bsup = 50+ (dev*STD(rsiplus))

binf = 50 - (dev*STD(rsiplus))

//RSI above buylevel and selllevel count

countB = 0

countS = 0

for i = 0 to minbarcount do

if rsiplus[i]>bsup[i] then

countB=countB+1

elsif rsiplus[i]<binf[i] then

countS=countS+1

endif

next

//case BUY

if rsiplus crosses over binf and countS>=minbarcount then

BUY 1 SHARE AT MARKET

endif

if longonmarket and rsiplus>=bsup then

SELL AT MARKET

endif

//case SELL

if rsiplus crosses under bsup and countB>=minbarcount then

SELLSHORT 1 SHARE AT MARKET

endif

if shortonmarket and rsiplus<=binf then

EXITSHORT AT MARKET

endif