Hello,

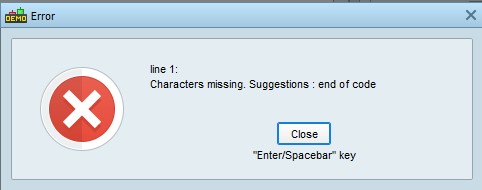

I have added risk and money management to my strategy as shown below but which is resulting in error message attached .

Kindly help to fix the errors , or it may be how i arrange the codes or something else.

—-Backtest——-

MyLongConditions = close CROSSES OVER BollingerDOWN[20]

MyShortConditions = close CROSSES UNDER BollingerUP[20]

MinWidth = 0.006 //max percentage of distance between the two bands

MyBandWidth = BollingerBandWidth[20](close)

p = 20

upper = bollingerup[p]

lower = bollingerdown[p]

middle = average[p]

BandwidthAbs= upper-lower

BandwidthCentage= (BandwidthAbs/middle)*100

//Bandwidth% should be adjusted based on securities and timeframes

IF MyLongConditions THEN

IF BandwidthCentage > 0.00 THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

ELSIF MyShortConditions THEN

IF BandwidthCentage > 2.00 THEN

SELL AT MARKET

ENDIF

ENDIF

——–Risk_Money_Management———-

// DrawDown calculation

ONCE MinPoint = Capital

ONCE MaxPoint = 0

ONCE MaxRU = 0

ONCE MaxDD = 0

IF StrategyProfit <> 0 THEN

Equity = Capital + StrategyProfit

TempProfit = PositionPerf * PositionPrice / PipSize

TempEquity = Equity + TempProfit

MaxPoint = max(MaxPoint,TempEquity)

DD = MaxPoint – TempEquity

MaxDD = max(MaxDD,DD)

ENDIF

//——————————————

// LARRY WILLIAMS’ formula (+margin)

MinSize = 0.5 //Minimum lot size allowed

Margin = high / 100 * 0.5 //Margin required 0.5%

Risk = 5 //Risk per trade 2%

TempLotSize = max(MinSize,(Equity * Risk / 100) / (MaxDD + Margin))

LotSize = round((TempLotSize * 10) – 0.5) / 10 //only 1 decimal digit allowed

//——————————————

// ATR Profit Target & Stop Loss

Atr = AverageTrueRange[14](Close)

SET STOP LOSS Atr

SET TARGET PROFIT Atr * 1.8

SET TARGET PROFIT Atr * 1.8

Comment out text lines like “—-Backtest——-” and “——–Risk_Money_Management———-“.

@Rotertogozzi.

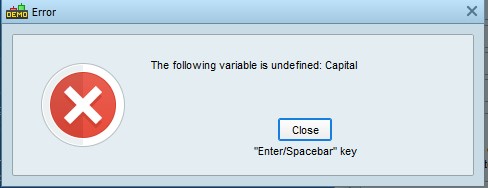

Thanks very much for the information, i have done exactly as you directed but still having the attached error relating to the variable capital.

Hope you can go through the entire code ( especially the Risk management section) to help fix the issues.

//—-Backtest——-

MyLongConditions = close CROSSES OVER BollingerDOWN[20]

MyShortConditions = close CROSSES UNDER BollingerUP[20]

MinWidth = 0.006 //max percentage of distance between the two bands

MyBandWidth = BollingerBandWidth[20](close)

p = 20

upper = bollingerup[p]

lower = bollingerdown[p]

middle = average[p]

BandwidthAbs= upper-lower

BandwidthCentage= (BandwidthAbs/middle)*100

//Bandwidth% should be adjusted based on securities and timeframes

IF MyLongConditions THEN

IF BandwidthCentage > 0.00 THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

ELSIF MyShortConditions THEN

IF BandwidthCentage > 2.00 THEN

SELL AT MARKET

ENDIF

ENDIF

//——-Risk_Money_Management———-

// DrawDown calculation

ONCE MinPoint = Capital

ONCE MaxPoint = 0

ONCE MaxRU = 0

ONCE MaxDD = 0

IF StrategyProfit <> 0 THEN

Equity = Capital + StrategyProfit

TempProfit = PositionPerf * PositionPrice / PipSize

TempEquity = Equity + TempProfit

MaxPoint = max(MaxPoint,TempEquity)

DD = MaxPoint – TempEquity

MaxDD = max(MaxDD,DD)

ENDIF

//——————————————

// LARRY WILLIAMS’ formula (+margin)

MinSize = 0.5 //Minimum lot size allowed

Margin = high / 100 * 0.5 //Margin required 0.5%

Risk = 5 //Risk per trade 2%

TempLotSize = max(MinSize,(Equity * Risk / 100) / (MaxDD + Margin))

LotSize = round((TempLotSize * 10) – 0.5) / 10 //only 1 decimal digit allowed

//——————————————

// ATR Profit Target & Stop Loss

Atr = AverageTrueRange[14](Close)

SET STOP LOSS Atr

SET TARGET PROFIT Atr * 1.8

SET TARGET PROFIT Atr * 1.8

You have to define the CAPITAL you plan to use for your strategy. Add this line BEFORE the start of the Risk Money Management:

ONCE Capital = 10000

10000 is just an example, you have to replace it with the amount that you really would invest to trade this code on a real account.

You can start with a large amount (you can even write 100K or 100M), the reduce it to a correct size after finding out the actual DrawDown.

@Rotertogozzi.,

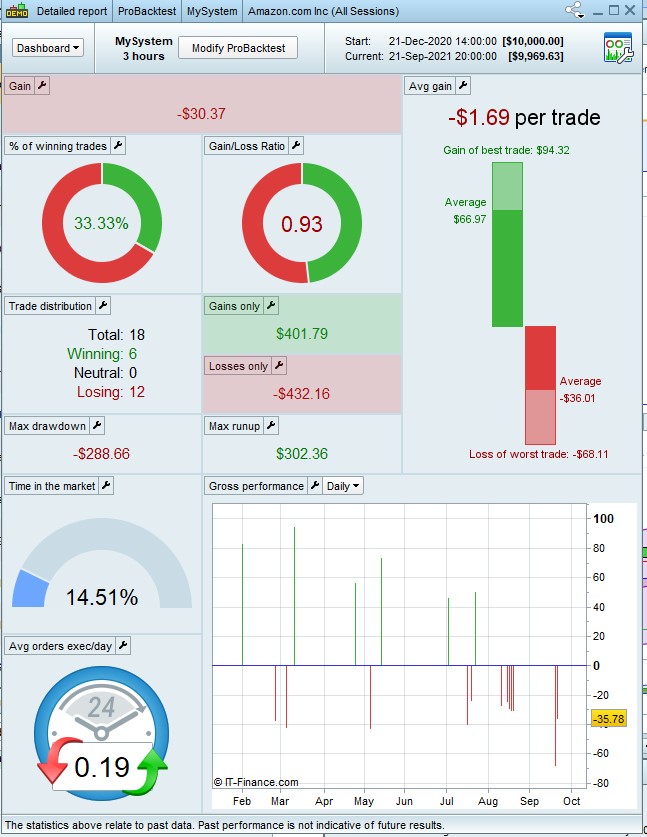

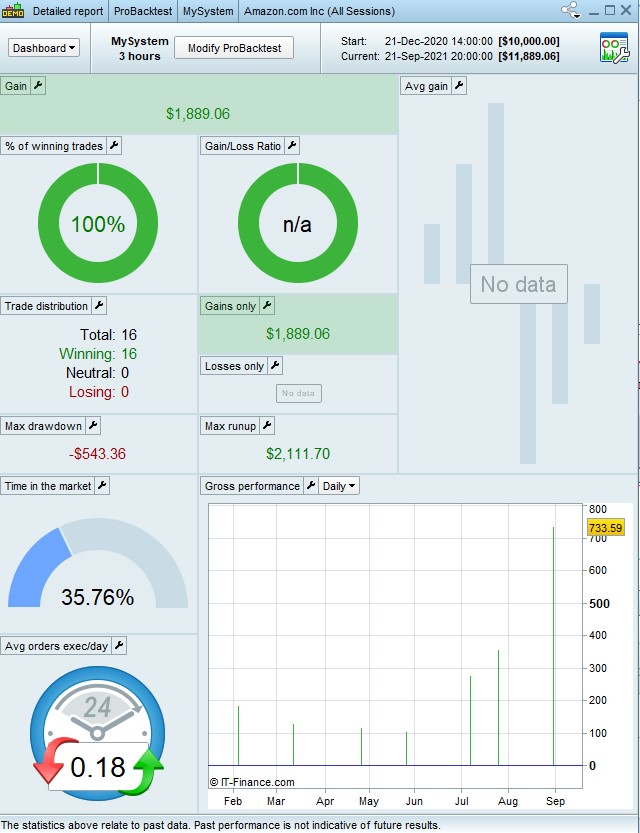

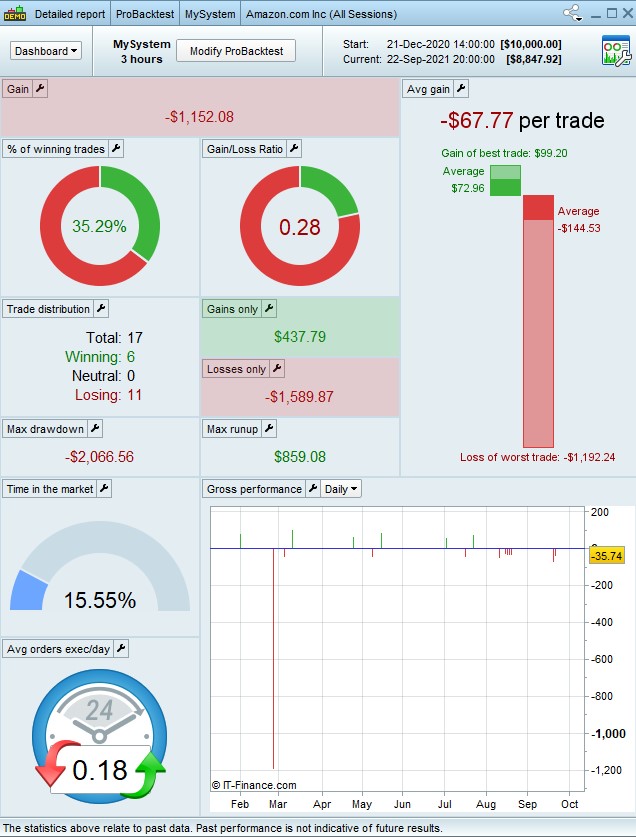

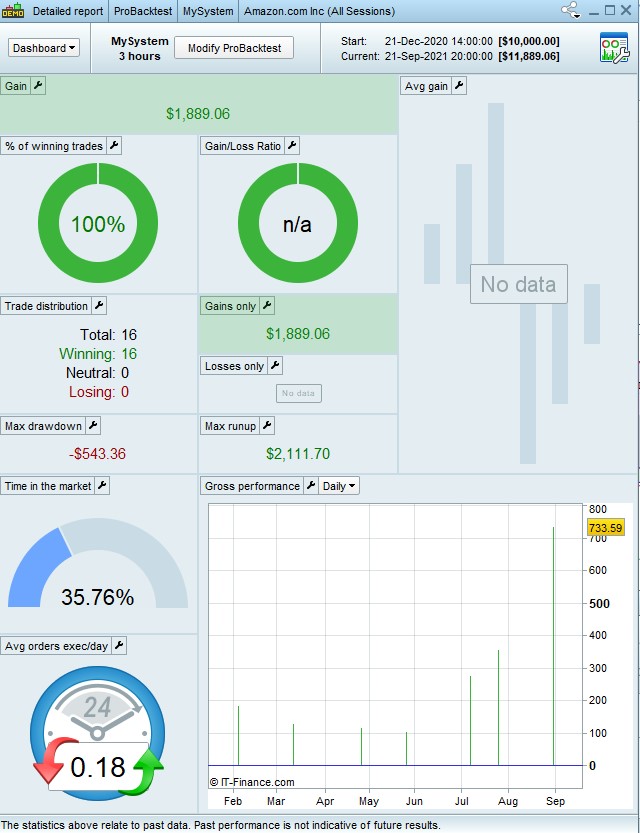

I have done exactly as you have instructed, please see attached backtest results Before and After adding the Risk management.

Am not able to analyse the results in terms of whether there is improvement or not.

I need your help.

regards.

This code works the same with and without Risk Managent:

//——-Risk_Money_Management———-

// DrawDown calculation

ONCE Capital = 10000

ONCE MinPoint = Capital

ONCE MaxPoint = 0

ONCE MaxRU = 0

ONCE MaxDD = 0

ONCE LotSize = 1

IF StrategyProfit <> 0 THEN

Equity = Capital + StrategyProfit

TempProfit = PositionPerf * PositionPrice / PipSize

TempEquity = Equity + TempProfit

MaxPoint = max(MaxPoint,TempEquity)

DD = MaxPoint - TempEquity

MaxDD = max(MaxDD,DD)

//——————————————

// LARRY WILLIAMS’ formula (+margin)

MinSize = 1 //Minimum lot size allowed

Margin = high / 100 * 0.5 //Margin required 0.5%

Risk = 5 //Risk per trade 2%

TempLotSize = max(MinSize,(Equity * Risk / 100) / (MaxDD + Margin))

LotSize = round((TempLotSize * 10) - 0.5) / 10 //only 1 decimal digit allowed

LotSize = max(MinSize,LotSize)

ENDIF

//LotSize = 1

//——————————————

//—-Backtest——-

p = 20

MyLongConditions = close CROSSES OVER BollingerDOWN[p]

MyShortConditions = close CROSSES UNDER BollingerUP[p]

//MinWidth = 0.01 //max percentage of distance between the two bands

MyBandWidth = BollingerBandWidth[p](close)

upper = bollingerup[p]

lower = bollingerdown[p]

middle = average[p]

BandwidthAbs= upper-lower

BandwidthCentage= (BandwidthAbs/middle)*100

//Bandwidth% should be adjusted based on securities and timeframes

// ATR Profit Target & Stop Loss

Atr = AverageTrueRange[14](Close)

IF MyLongConditions AND Not OnMarket AND BandwidthCentage > 2.00 THEN

BUY LotSize CONTRACTS AT MARKET

SET STOP LOSS Atr

SET TARGET PROFIT Atr * 1.8

//SET TARGET PROFIT Atr * 1.8

ENDIF

IF MyShortConditions AND LongOnMarket AND BandwidthCentage > 2.00 THEN

SELL AT MARKET

ENDIF

//

//graph Atr

//graph Atr * 1.8

//graph StrategyProfit

//graph BandwidthCentage

//graph LotSize

//graph MyLongConditions

Uncomment line 25 to disable Risk Management.

@Rotertogozzi

Thanks, i have run the codes in previous message but it appears to give results far worse that what i initially reported about.

Please have a look as attached.

Also is tis possible you explain what i should be expecting the metrics and performance to be after implementing Risk and money management to the strategy.

You don’t need to post again the pics you had already posted. Posting them twice won’t help.

The risk management code simply calculates the number of lots you can trade.

It doesn’t add anything to the conditions to enter and exit a trade. The metric are a calculation of the number of lots you can trade according to:

- your capital

- your risk

- drawdown.

@Rotertogozzi

Thanks very much, but you appear to suggest that i should not pay attention to the backtest results. If that is the case then how you a trader know whether his strategy’s performance is acceptable or not.

In other words if my strategy performance was 100% say for winning, but after adding lot size , capital, risks and drawdown the performance now drops to as low as 35% and drawdown also dropped massively based on backtest results wbat explanation can be given to this scenario?

Is it advisable to ignore these inconsistencies and go ahead with live trading?

Hello , please i will be most grateful to have response to the issues i have explained in previous messages.

I have been doing a lot of googling and research but found no answers and looks as if am completely standing still now.

I urgently need to continue , i dont want to abandon the strategy after putting in so much.

Is it advisable to ignore these inconsistencies and go ahead with live trading?

No, but you can run your Algo on your Demo account under Live running conditions using virtual money.

Have you got / enabled your Demo Account?

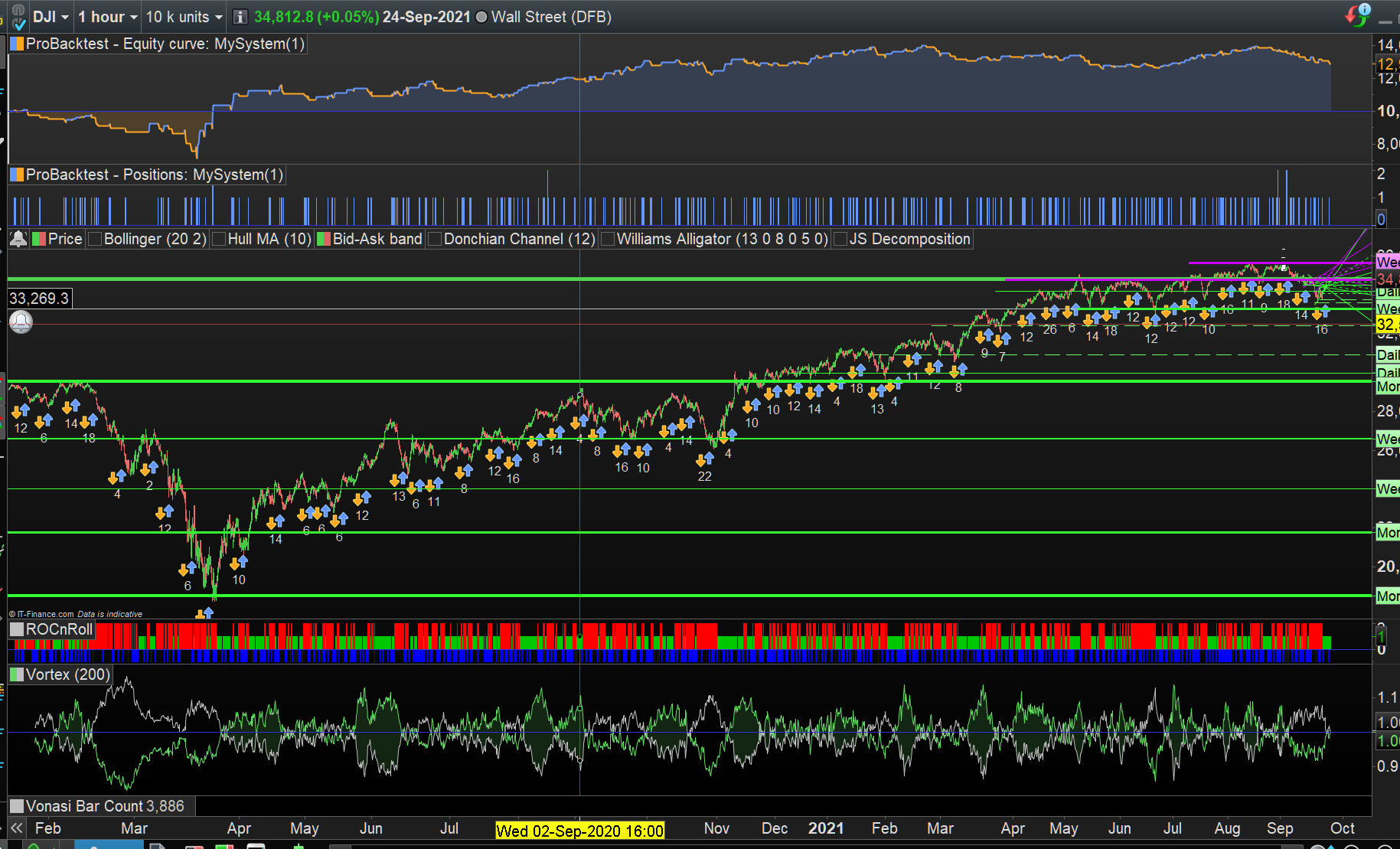

Attached is what I see on backtest of your Algo (spread = 2)

The code in you second post was missing the Capital, please add it to make it work and post it again.

I want to test your code exactly as you did. You tested it on AMAZON (alla sessions), 3h TF, 1K units, didn’t you?

GraHal

Please i dont understand your question.

All the screenshots i have been attaching and sending in my messages concerning my strategies and backtesting are all coming from my Demo account, so am a bit confused when you asked “Have you got / enabled your Demo Account?”

Also you seem to agree that it is NOT advisable to ignore these inconsistencies and go ahead with live trading, but the question that still remains is how do we remove the inconsistencies.

Are these inconsistencies general issues with PRT or is just specific to my strategy?

Attached is what I see on backtest of your Algo (spread = 2)

Sorry i dont understand these screenshot, the charts i have been using is different from the one you have. How do i find same chart types and how can i interpret them?

Please can you also go ahead to generate the corresponding backtest for this chart/strategy since the main issues relate to inconsistencies in the backtest results.

Regards.