Hi

Even after i increase the defparam preloadbars = 5000 i still get the error message and my automatic code is rejected. I have tried setting to 0 and also removed it totally and my code still stops. The error message is the basic …please increase the number off preloaded bars with instruction DEFPARAM etc etc

Code works fine on back test – has also previously worked as automatic code before i have increase some filters in the code which is now causing the problem.

Try to increase to 10,000 (max. allowed).

In case you use very high period numbers for indicators, try decreasing them.

As a final resort you should post your full code to be able to replicate those messages.

Roberto , detailed code below as tried the solutions and still rejects code.

//pending orders version

//version (c):

//mid bollinger cancel and closing time of pending orders

//version (d):

//max loss + breakeven + std conditions

defparam flatafter=205500 //close opened orders and delete pending ones at that time

defparam cumulateorders=false

defparam preloadbars= 10000

// --- settings

amount = 3 //amount of contract/lot/shares to open for each order

StartTime = 143000 //start time of the strategy to look for a spike outside BB

EndTime = 205500 //end time of the strategy

BreakAboveBelowBB = 2//Break above/below BB (3points)

BreakBarDistance = 2//Break below low/high of reference bar (2points)

StopL = 1//Stop (2 point break of reference bar)

TargetP = 95 //Target (Mid Bollinger 95%)

MinTarget = 8//Minimum target for NO trade(10 points)

MaxLoss = tp //Maximum loss in points for any order

BreakevenStart = 60//breakeven activation at x% of target achieved

PointsToKeep = 5 //how much pips/points to keep in profit above of below our entry price when the breakeven is activated (beware of spread)

MaxSTD = 14 //max standard deviation level to activate/cancel the orders

STDperiod = 10//standard deviation period used for calculation

MaxADX = 18

ADXperiod = 16

adxp=adxp

indicator1 = ADX[adxp]

indicator2 = ADXR[adxp]

c1 = (indicator1 < indicator2)

// Conditions to enter short positions

indicator3 = ADX[adxp]

indicator4 = ADXR[adxp]

c2 = (indicator3 < indicator4)

// --- end of settings

tcondition = opentime>=starttime and time<=endtime

dcondition = OpenDayOfWeek = 6

bbup = BollingerUp[20](close)

bbdn = BollingerDown[20](close)

mid = average[20]

istd = std[STDperiod]

iadx = adx[ADXperiod]

//reset ref bar

if longonmarket then

hhrefbar=0

endif

if shortonmarket then

llrefbar=0

endif

if not tcondition then

hhrefbar=0

llrefbar=0

endif

if not longonmarket and hhrefbar>0 and high crosses over mid then

hhrefbar=0

endif

if not shortonmarket and llrefbar>0 and low crosses under mid then

llrefbar=0

endif

if tcondition and not dcondition then

if not shortonmarket then

//find first new BB+ ref bar = SHORT ORDER

if llrefbar=0 then //first ref

if high>=bbup+BreakAboveBelowBB*pointsize then

ll=low

sellsl=high+StopL*pointsize

llrefbar=barindex

lastref=-1

endif

else //next ref

if high>high[max(1,barindex-llrefbar)] then //compute new reference bar

ll=low

sellsl=high+StopL*pointsize

llrefbar=barindex

lastref=-1

endif

endif

endif

if not longonmarket then

//find first new BB- ref bar = BUY ORDER

if hhrefbar=0 then //first ref

if low<=bbdn-BreakAboveBelowBB*pointsize then

hh=high

buysl=low-StopL*pointsize

hhrefbar=barindex

lastref=1

endif

else //next ref

if low<low[max(1,barindex-hhrefbar)] then //compute new reference bar

hh=high

buysl=low-StopL*pointsize

hhrefbar=barindex

lastref=1

endif

endif

endif

//break ref bar and open orders

//case buy

if not longonmarket and lastref>=0 and barindex>=hhrefbar and hhrefbar>0 then //and high>=hh+BreakBarDistance*pointsize then

avg = average[20](close)

tp = (avg-(hh+BreakBarDistance*pointsize))*(TargetP/100)

allowtarget = tp>=MinTarget*pointsize

if allowtarget and istd<maxstd*pointsize or iadx<maxadx and c1 then

buy amount contract at hh+BreakBarDistance*pointsize stop

//hhrefbar=0 //reset ref bar

set stop loss min(maxloss*pointsize,close-buysl)

set target profit tp

endif

endif

//case sell

if not shortonmarket and lastref<=0 and barindex>=llrefbar and llrefbar>0 then // and low<=ll-BreakBarDistance*pointsize then

avg = average[20](close)

tp = ((ll-BreakBarDistance*pointsize)-avg)*(TargetP/100)

allowtarget = tp>=MinTarget*pointsize

if allowtarget and istd<maxstd*pointsize or iadx<maxadx and c2 then

sellshort amount contract at ll-BreakBarDistance*pointsize stop

//llrefbar=0 //reset ref bar

set stop loss min(maxloss*pointsize,sellsl-close)

set target profit tp

endif

endif

endif

startBreakeven = (BreakevenStart/100)*tp //how much pips/points in gain to activate the breakeven function?

//reset the breakevenLevel when no trade are on market

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

// --- SELL SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF SHORTONMARKET AND tradeprice(1)-close>=startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

// --- end of SELL SIDE ---

//graph tp

//graph hh+BreakBarDistance*pointsize coloured(0,255,0) as "reference buy"

//graph ll-BreakBarDistance*pointsize coloured(255,0,0) as "reference sell"

//graph allowtarget

//graph close as "price Close"

//graph not longonmarket and hhrefbar>0 and high crosses over mid

//graph breakevenlevel

I tested your code on Eur/Usd, 5-minute TF, and I get no error, no matter what PRELOADBAR I write.

It runs smoothly. Backtest is very slow, instead!

Try shutting down your platform and reopen it, even after restarting your PC.

Restarted everything and reloaded and error happens again .

I can back test no problem with the code without errors its when i then put it live – it loads it then rejects it after a few minutes.

im running it on the DOW on 1 and 3 minute time frames.

It must be due to extremely slow code, but I could not spot why.

I suggest that you use Ctrl+M from the platform to ask assistance.

Backtest is very slow, instead!

I agree … maybe the OP just chose the wrong Username! 🙂 🙂

I will try it on Demo Forward test and Report back!

EDIT / PS

Yep rejected 3 times with and without the PreLoad bars I get same error message … Increase PreLoad bars etc etc.

I reckon it’s timing out on Forward Test (code taking too long etc) and the error message is meaningless?

On Backtest there is probably a longer time out period and that is why the code eventually gets there in Backtest??

Basis for an easy worded Tech Report? I suggest …

- System won’t run on Forward Test … please can you tell me why?

So u suggest I ask tech support with that so I therefore will with yr suggested comments . back testing is very slow due to all the requirements it has to test … let’s see if they have a solution .. ? Seems strange to me

Yeah we all learn more when we make mistakes, we need to know what the limits are on time for code to run and PRT may learn something also during the investigation ?

It may be something simple anyway that is making it real slow?

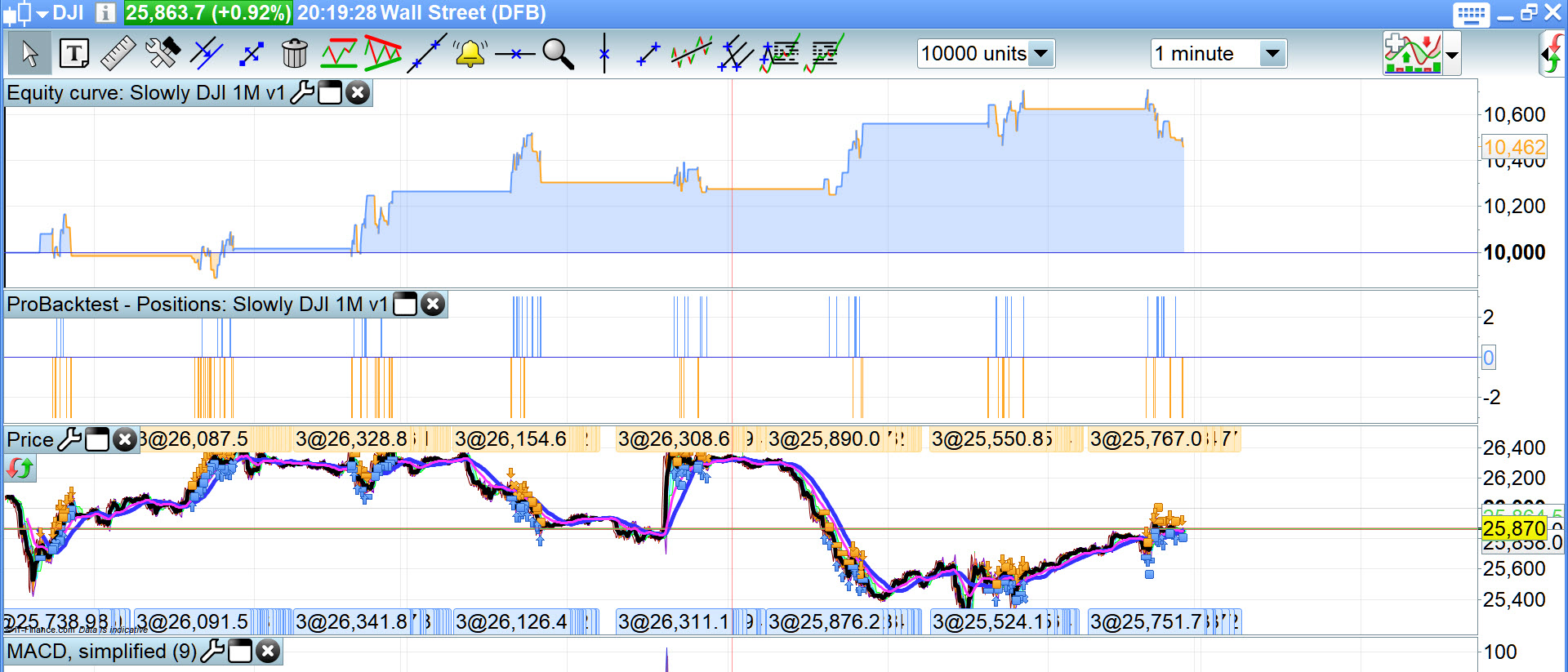

Results (attached) look promising on DJI 1M, spread = 4 attached so it is worth keeping the code as is if it will run okay?

Press Ctrl + M when you are seeing a Chart on the screen and follow the bottom option … Tech Report.

There is no reason to extend the preloadbars according to the code, I don’t understand why you get that error message. BTW, that code reminds me something 😉

There is something odd about that code even outside of PRT … as soon as have it up on my screen in this Forum and I am scrolling over the code … my scroll button works real slow like when I am running out of RAM.

I reckon it’s that Username the OP has … he’s jinxed himself!!! (joke! 🙂 )

But not joking about the slow mouse scroll.

Any reply from PRT yet @Slowlyslowly??

It’s still doing the same type Rejection due to not enough data history etc.

I am curious if it will make money if we get it going!!?? 🙂

Just spent the last hour or so removing various snippets / conditions / variables etc in an effort to stop this System being rejected and showing an error message that has nothing to do with the rejection!

Below is the fix. Seems it maybe was timeout error as I had suggested above?

Code was using ADXPeriod and ADXp for the same value, but ADXp was not defined anywhere in the code.

Line 36

adxp=adxperiod (not adxp=adxp)