I’m sure PeterSt will have some more to say,

Well, he’s intrigued.

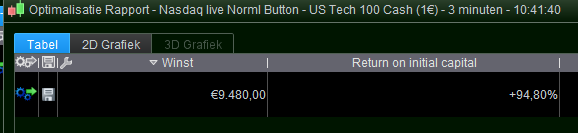

At least this Strategy is independent of the “sequence” I mentioned (scalping works too “strict” for it to deviate at the 3 minute interval).

First off : a deep hats off to GraHal who has been “able” to find the differentiation by means of using those separate buttons. Without that, no dice ! (and only the winning strategy).

Next, of course an apology to Jos because all I said is not in order / applicable.

Then :

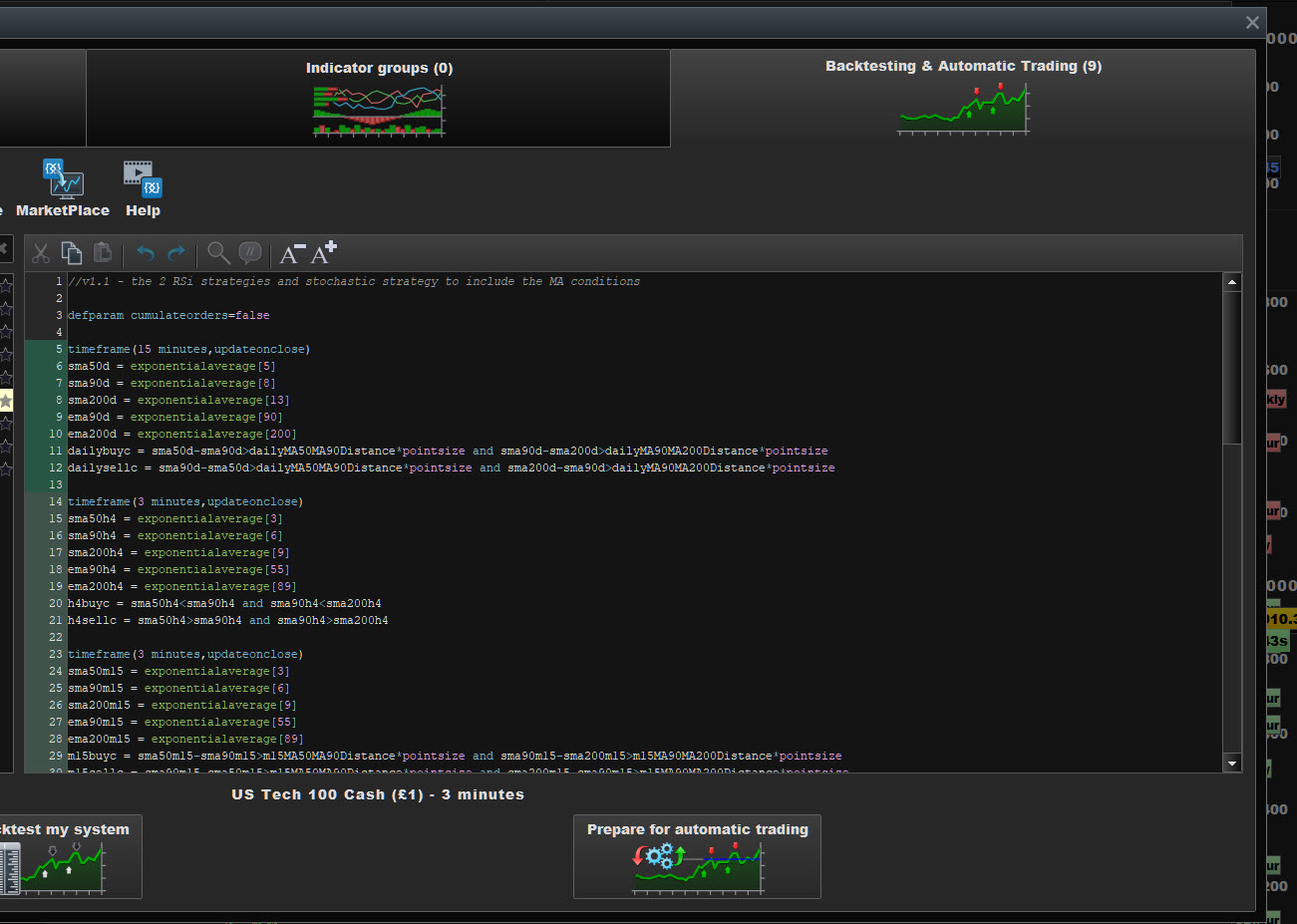

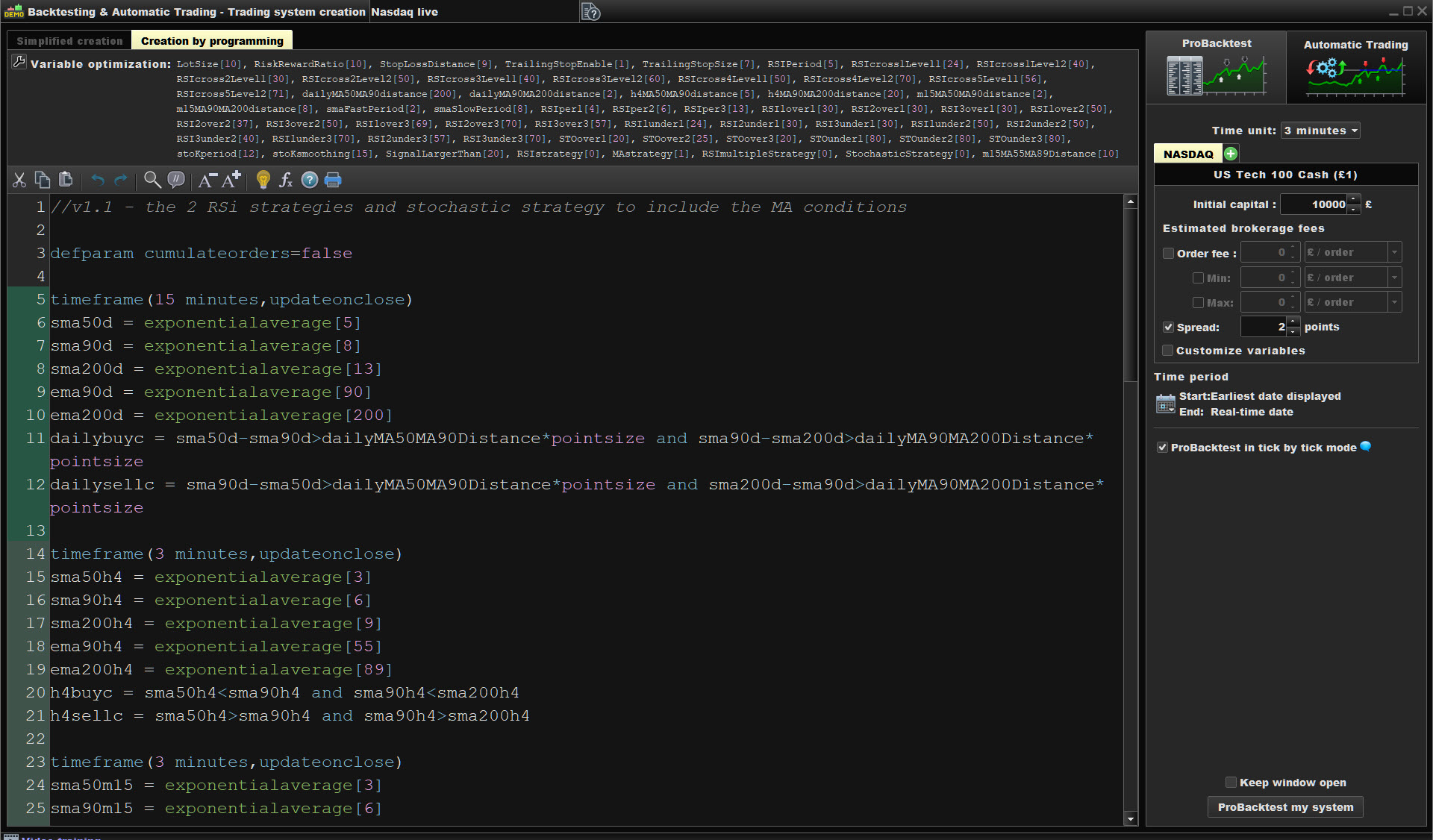

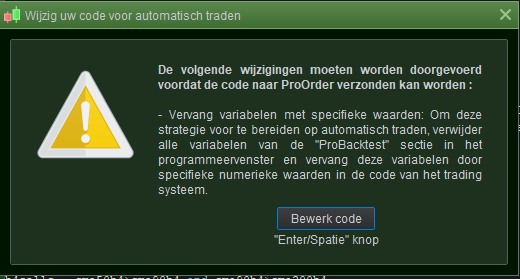

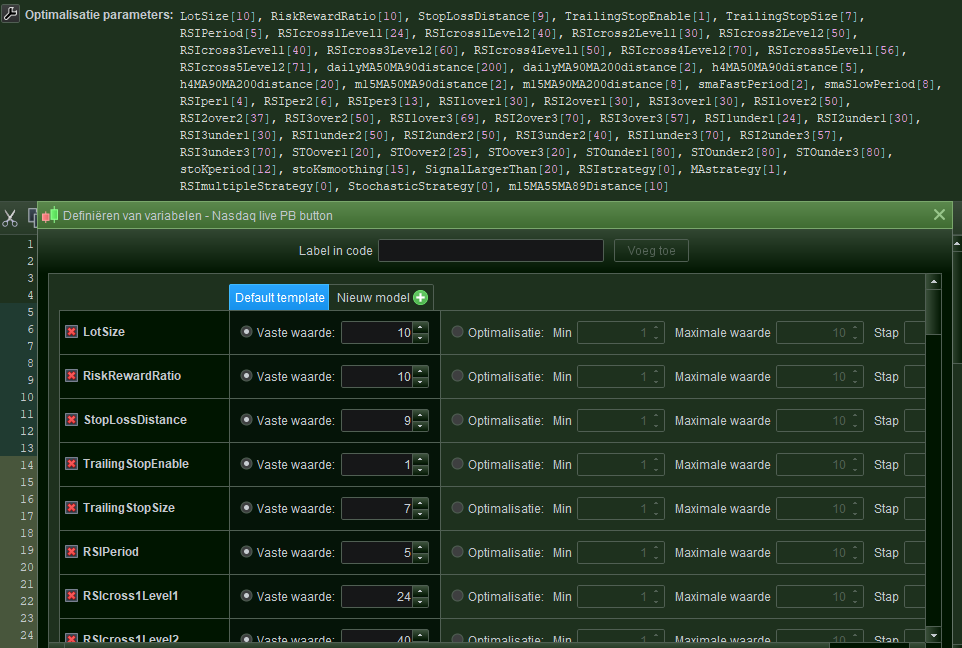

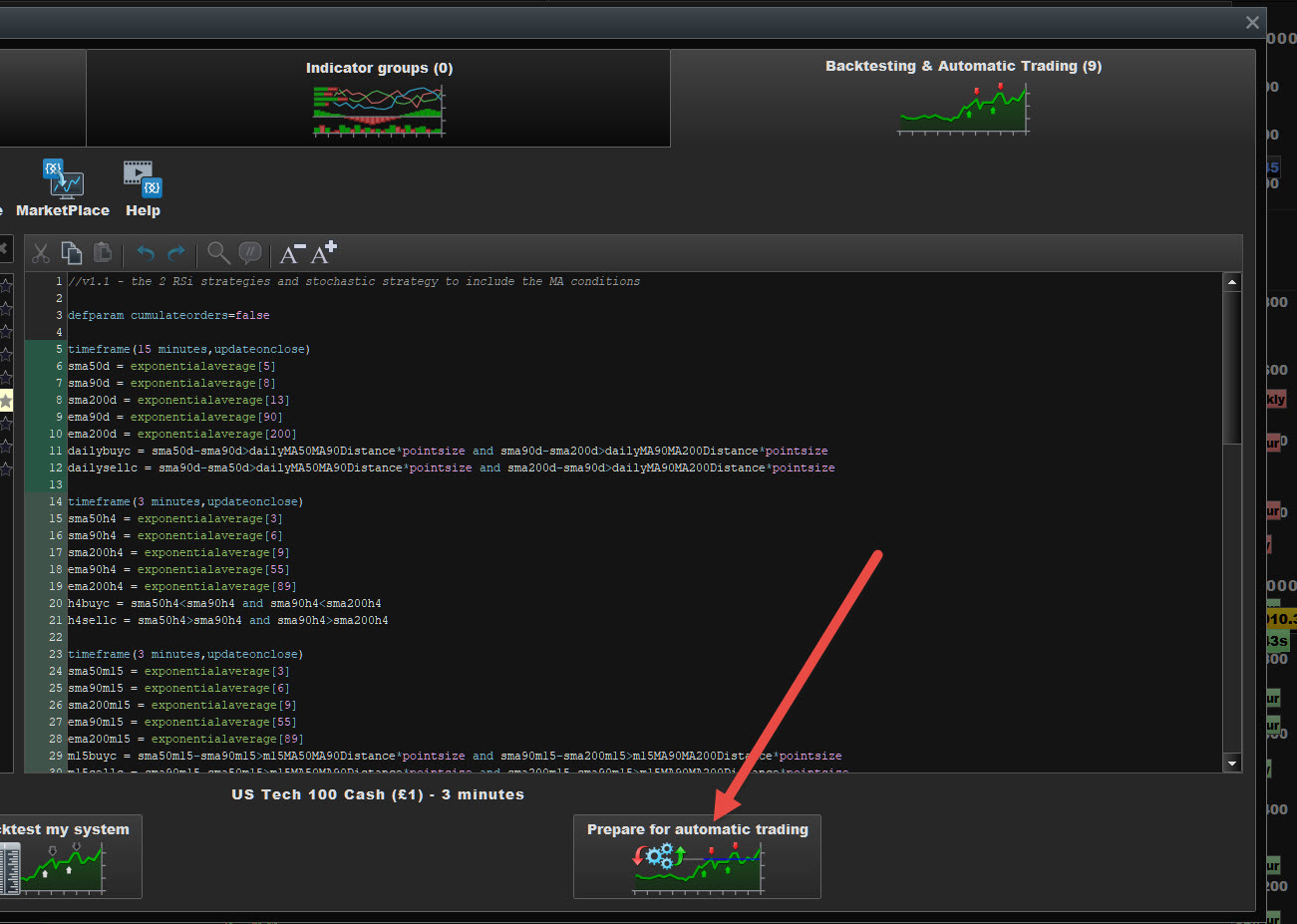

When using the button for Preparing the Strategy for AutoTrading, we receive the message in the 2nd attachment, and it tells us to replace the Optimisation Variables with direct assignments in the code. And well, I can’t be 100% sure yet, but it seems to go wrong there. Regarding this, the message should not be there in the first place, that is, not that I know of because PRT will replace them with ONCE assignment in “my” normal situation. So what I am saying is that what you see in the 3rd attachment is a perfectly normal situation to exist, even meant to fill (change) the parameters to the Strategy at handing the Strategy to the AutoTrading system. Thus, I could change LotSize to 15 when I hand it to Autotrading. PRT will make this of it in the top of the code :

ONCE LotSize = 10

or when I changed it to 15 :

ONCE LotSize = 15

All the parameters to the Strategy (yes, it’s “parameters” now) are set like this with ONCE statements. And it is here where something will go bananas, already because this message (2nd attachment) appears. Jos will be doing similar (though possibly (??) not with ONCE statements but normal assignments (LotSize = 10)) and now the Strategy won’t work because the virtual ONCE’s will not be there and a variable may accumulate instead of starting at its initial value at each call when the 3 minute bar is closed.

(hey, this is ad-hoc reasoning 😉 )

Because that message should not appear anyway, I think the intelligence of the PRT AutoTrading engine can see in advance that something is ambiguous. This can easily be because of the TimeFrame commands (it is not that, see more below). Regarding this, also notice that the ONCE assignments will (and can only) be inserted at the top of the code, while you might need some to be under an other TimeFrame (like under line 14).

For better understanding of my reasoning, please notice that with normal BackTesting, the ONCE statements will be be there just the same, but we can never see that. When Prepared (for AutoTrading) we can by clicking the link in the window with our Strategies. In this particular case it won’t come that far because the message orders us to inject those statements ourselves. Maybe one, maybe two, maybe all.

Jos, or anyone, I suspect that if you’d insert those statements yourself, there will be a difference between ONCE and the normal assignments. And if PRT would kindly provide a copy-paste facility from the Optimisation Variables, then I would be very happy with it anyway, but I would also have done it myself (no lust to copy them by means of typing and making typo’s, at this time). And Jos, you will already have done that, so you may want to paste them in a next post (or I do it myself anyway because I am too eager for the result).

A year or so back I have created a topic somewhere named “Something is fundamentally wrong with Optimisation Variables” (or something of that order). This is about (for example)

LotSize = LotSize + 1

Giving unpredictable results in the variable itself. Thus, internally this will be

ONCE LotSize = 10

LotSize = LotSize + 1

And the system can’t cope with that. However, when *you* insert it like you see right above here, it will be fine.

Lastly … I got the hunch of commenting-out the TimeFrate statements. And wonder oh wonder, the result is exactly the same for both (GraHal’s) buttons. This was not to be expected at least for the winning situation. No change ?? Does Jos recognise that this can be ? (I didn’t look into the functional code itself at all).