Hello,

I tried to embed the PP Fractals indicator developed by https://www.prorealcode.com/prorealtime-indicators/pp-fractals/ in a Strategy, where among conditions to go Long (Close> $resistancevalue[z]) and go Short (Close<close < $supportvalue[z]). The backtest works perfectly fine on 100k 1min TF. However, when I put it live, I got this error message twice. It seems to be linked to the number of values in the Arrays. Note: this is the only Array I’ve in my system. Also, I tried with Preload 10000 bars and without Preload and the problem is the same.

I congratulate for his work as the System without this condition generates 40% less Gains!

Any idea on how to overcome this problem?

Thank you.

Hi Khaled,

I don’t understand much of Vonasi’s Indicator code, so the only hint I can give you is that an array can’t contain more than 1M elements. And the message you show seems to be about that.

An other hint could be that the indicator is a kind of lame (not decent) in not being able to find a “base” for its signal, as Vonasi explains himself. So you could have run into that situation where it needs to go back further than the array size allows for.

Please keep in mind that my text may not make any sense because I really can’t follow what is going on in his code (up to my thinking that it can’t work at all 😐 ).

Hopefully others can help more; the 1M max elements is key …

What I would attempt :

a = a + 1

All such situations (also for b and z at first glance) could be written like this :

if a < 999999 then // 1 extra to be on the safe side.

a = a + 1

endif

This will stop going back further than technically possible, but don’t ask me for the reliability of the result and its impact. But at least it won’t fail.

On a (not so unimportant) side note :

You may have read (elsewhere) me questioning what would or could happen in LIVE when the progression of time may cross the threshold of the boundaries of arrays. But this (erroring-out) would require 1M bars plus the amount of looking back first. Anyway, this would be a “feature” of Live which BackTesting would not allow for (it won’t go wrong when time passes).

Hope this helps !

Thank you Peter. I’ll give it a try and let you know.

Dear Peter, Just Brilliant !!!! I tried your suggestion and so far it seems to work. I must admit that Arrays are way beyond my PRT skills.

Thanks a million and have a good day!

I worked one time, then same problem again and again. Anyone has a different idea please?

Please post the strategy code, we dont know how you have implemented the code into the strategy. I assume you want to trade the last segment breakout? If so, then most of the indicator code is not necessary.

Thank you Nicolas for your time. Indeed, I’d like to get signals on the last segment breakout.

Below the code run on SP500 – 100k – 1min TF – spread 0.6

DEFPARAM CUMULATEORDERS = FALSE

TIMEFRAME(60 minutes)

LongConso=0

ShortConso= 0

Long=0

Short=0

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

//PRC_SwingLine Ron Black | indicator by Nicolas

if upsw=1 then

if high>hH then

hH=high

endif

if low>hL then

hL=low

endif

if high<hL then

upsw=0

lL=low

lH=high

endif

endif

if upsw=0 then

if low<lL then

lL=low

endif

if high<lH then

lH=high

endif

if low>lH then

upsw=1

hH=high

hL=low

endif

endif

if upsw=1 then

swingline=hL

else

swingline=lH

endif

if close>open then

iRange = abs(close-open)

elsif close<open then

iRange = abs(open-close)

endif

if close>open then

UpWick = high - close

LoWick = open-low

elsif close<open then

UpWick = high-open

LoWick = close-low

endif

// LONG

if close>open then

if close[1]>open[1] then

if close>close[1] then

long1=1

endif

endif

endif

if close>open then

if close[1]<open[1] then

if close>open[1] then

long2=1

endif

endif

endif

if iRange>UpWick or LoWick>UpWick then

long3 = 1

endif

//if close>close[1] and close[2]>close[1] then

//long4 = 1

//endif

if high>high[1] or low>low[1] then

long5=1

endif

if (long1 or long2) and long3 and long5 and close>swingline then

Long=1

endif

// SHORT

if close<open then

if close[1]>open[1] then

if close<open[1] then

short1=1

endif

endif

endif

if close<open then

if close[1]<open[1] then

if close<close[1] then

short2=1

endif

endif

endif

if iRange>LoWick or LoWick<UpWick then

short3 = 1

endif

//if close<close[1] and close[2]<close[1] then

//short4 = 1

//endif

if high<high[1] or low<low[1] then

short5=1

endif

if (Short1 or short2) and short3 and short5 and close<swingline then

Short=-1

endif

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// SR PP Fractal Lines by Vonasi

//BarsBefore = 1

//BarsAfter = 1

Support = 1

Resistance = 1

Points = 1

//Make sure all settings are valid ones

BarsBefore = max(BarsBefore,1)

BarsAfter = max(BarsAfter,1)

StartBack = max(0,startback)

if barindex >= barsbefore + barsafter then

//Look for a low fractal

BarLookBack = BarsAfter + 1

if low[BarsAfter] < lowest[BarsBefore](low)[BarLookBack] THEN

if low[BarsAfter] = lowest[BarLookBack](low) THEN

if a<99999 then

a = a + 1

endif

$supportbar[a] = barindex[barsafter]

$supportvalue[a] = low[barsafter]

endif

endif

//Look for a high fractal

if high[BarsAfter] > highest[BarsBefore](high)[BarLookBack] THEN

if high[BarsAfter] = highest[BarLookBack](high) THEN

if b<99999 then

b = b + 1

endif

$resistancebar[b] = barindex[barsafter]

$resistancevalue[b] = high[barsafter]

endif

endif

if islastbarupdate then

//support line

if a >= 2 then

if support then

flag = 0

zz = 0

for z = a-zz downto 1

for xx = 1 to a

if z-xx < 1 then

break

endif

if $supportvalue[z] > $supportvalue[z-xx] then

if points then

endif

flag = 1

break

endif

if zz<99999 then

zz = zz + 1

endif

next

if flag = 1 then

break

endif

zz = 0

next

endif

endif

//resistance line

if b >= 2 then

if resistance then

flag = 0

zz = 0

for z = b-zz downto 1

for xx = 1 to b

if z-xx < 1 then

break

endif

if $resistancevalue[z] < $resistancevalue[z-xx] then

if points then

endif

flag = 1

break

endif

if zz<99999 then

zz = zz + 1

endif

next

if flag = 1 then

break

endif

zz = 0

next

endif

endif

endif

endif

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

LongConso = long=1 and close > $resistancevalue[z]

ShortConso = short=-1 and close < $supportvalue[z]

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME(5 minutes, UPDATEONCLOSE)

nLots = min(10,round((2000+STRATEGYPROFIT)/(close*.5*.1),1))

IF NOT LongOnMarket AND LongConso THEN

BUY nLots CONTRACTS AT MARKET

ENDIF

IF NOT ShortOnMarket AND ShortConso THEN

SELLSHORT nLots CONTRACTS AT MARKET

ENDIF

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

If LongOnMarket AND ShortConso THEN

SELL AT MARKET

SELLSHORT nLots CONTRACTS AT MARKET

ENDIF

IF ShortOnMarket AND LongConso THEN

EXITSHORT AT MARKET

BUY nLots CONTRACTS AT MARKET

ENDIF

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME(1 minute)

SET STOP %LOSS .3 //SL

SET TARGET %PROFIT 1.6 //TP

Ok, so arrays are not useful anymore, there was useful in case of plotting them on the chart in the past.

Here is the code, not a real breakout, your condition is testing a price superior or inferior.

DEFPARAM CUMULATEORDERS = FALSE

TIMEFRAME(60 minutes)

LongConso=0

ShortConso= 0

Long=0

Short=0

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

//PRC_SwingLine Ron Black | indicator by Nicolas

if upsw=1 then

if high>hH then

hH=high

endif

if low>hL then

hL=low

endif

if high<hL then

upsw=0

lL=low

lH=high

endif

endif

if upsw=0 then

if low<lL then

lL=low

endif

if high<lH then

lH=high

endif

if low>lH then

upsw=1

hH=high

hL=low

endif

endif

if upsw=1 then

swingline=hL

else

swingline=lH

endif

if close>open then

iRange = abs(close-open)

elsif close<open then

iRange = abs(open-close)

endif

if close>open then

UpWick = high - close

LoWick = open-low

elsif close<open then

UpWick = high-open

LoWick = close-low

endif

// LONG

if close>open then

if close[1]>open[1] then

if close>close[1] then

long1=1

endif

endif

endif

if close>open then

if close[1]<open[1] then

if close>open[1] then

long2=1

endif

endif

endif

if iRange>UpWick or LoWick>UpWick then

long3 = 1

endif

//if close>close[1] and close[2]>close[1] then

//long4 = 1

//endif

if high>high[1] or low>low[1] then

long5=1

endif

if (long1 or long2) and long3 and long5 and close>swingline then

Long=1

endif

// SHORT

if close<open then

if close[1]>open[1] then

if close<open[1] then

short1=1

endif

endif

endif

if close<open then

if close[1]<open[1] then

if close<close[1] then

short2=1

endif

endif

endif

if iRange>LoWick or LoWick<UpWick then

short3 = 1

endif

//if close<close[1] and close[2]<close[1] then

//short4 = 1

//endif

if high<high[1] or low<low[1] then

short5=1

endif

if (Short1 or short2) and short3 and short5 and close<swingline then

Short=-1

endif

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// SR PP Fractal Lines by Vonasi

//BarsBefore = 1

//BarsAfter = 1

Support = 1

Resistance = 1

Points = 1

//Make sure all settings are valid ones

BarsBefore = max(BarsBefore,1)

BarsAfter = max(BarsAfter,1)

StartBack = max(0,startback)

if barindex >= barsbefore + barsafter then

//Look for a low fractal

BarLookBack = BarsAfter + 1

if low[BarsAfter] < lowest[BarsBefore](low)[BarLookBack] THEN

if low[BarsAfter] = lowest[BarLookBack](low) THEN

//if a<99999 then

//a = a + 1

//endif

//$supportbar[a] = barindex[barsafter]

//$supportvalue[a] = low[barsafter]

supportvalue = low[barsafter]

endif

endif

//Look for a high fractal

if high[BarsAfter] > highest[BarsBefore](high)[BarLookBack] THEN

if high[BarsAfter] = highest[BarLookBack](high) THEN

//if b<99999 then

//b = b + 1

//endif

//$resistancebar[b] = barindex[barsafter]

//$resistancevalue[b] = high[barsafter]

resistancevalue = high[barsafter]

endif

endif

//if islastbarupdate then

////support line

//if a >= 2 then

//if support then

//flag = 0

//zz = 0

//for z = a-zz downto 1

//for xx = 1 to a

//if z-xx < 1 then

//break

//endif

//if $supportvalue[z] > $supportvalue[z-xx] then

//if points then

//endif

//flag = 1

//break

//endif

//if zz<99999 then

//zz = zz + 1

//endif

//next

//if flag = 1 then

//break

//endif

//zz = 0

//next

//endif

//endif

//

////resistance line

//if b >= 2 then

//if resistance then

//flag = 0

//zz = 0

//for z = b-zz downto 1

//for xx = 1 to b

//if z-xx < 1 then

//break

//endif

//if $resistancevalue[z] < $resistancevalue[z-xx] then

//if points then

//endif

//flag = 1

//break

//endif

//if zz<99999 then

//zz = zz + 1

//endif

//next

//if flag = 1 then

//break

//endif

//zz = 0

//next

//endif

//endif

//endif

endif

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

LongConso = long=1 and close > resistancevalue//$resistancevalue[z]

ShortConso = short=-1 and close < supportvalue//$supportvalue[z]

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME(5 minutes, UPDATEONCLOSE)

nLots = min(10,round((2000+STRATEGYPROFIT)/(close*.5*.1),1))

IF NOT LongOnMarket AND LongConso THEN

BUY nLots CONTRACTS AT MARKET

ENDIF

IF NOT ShortOnMarket AND ShortConso THEN

SELLSHORT nLots CONTRACTS AT MARKET

ENDIF

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

If LongOnMarket AND ShortConso THEN

SELL AT MARKET

SELLSHORT nLots CONTRACTS AT MARKET

ENDIF

IF ShortOnMarket AND LongConso THEN

EXITSHORT AT MARKET

BUY nLots CONTRACTS AT MARKET

ENDIF

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME(1 minute)

SET STOP %LOSS .3 //SL

SET TARGET %PROFIT 1.6 //TP

Thank you Nicolas.

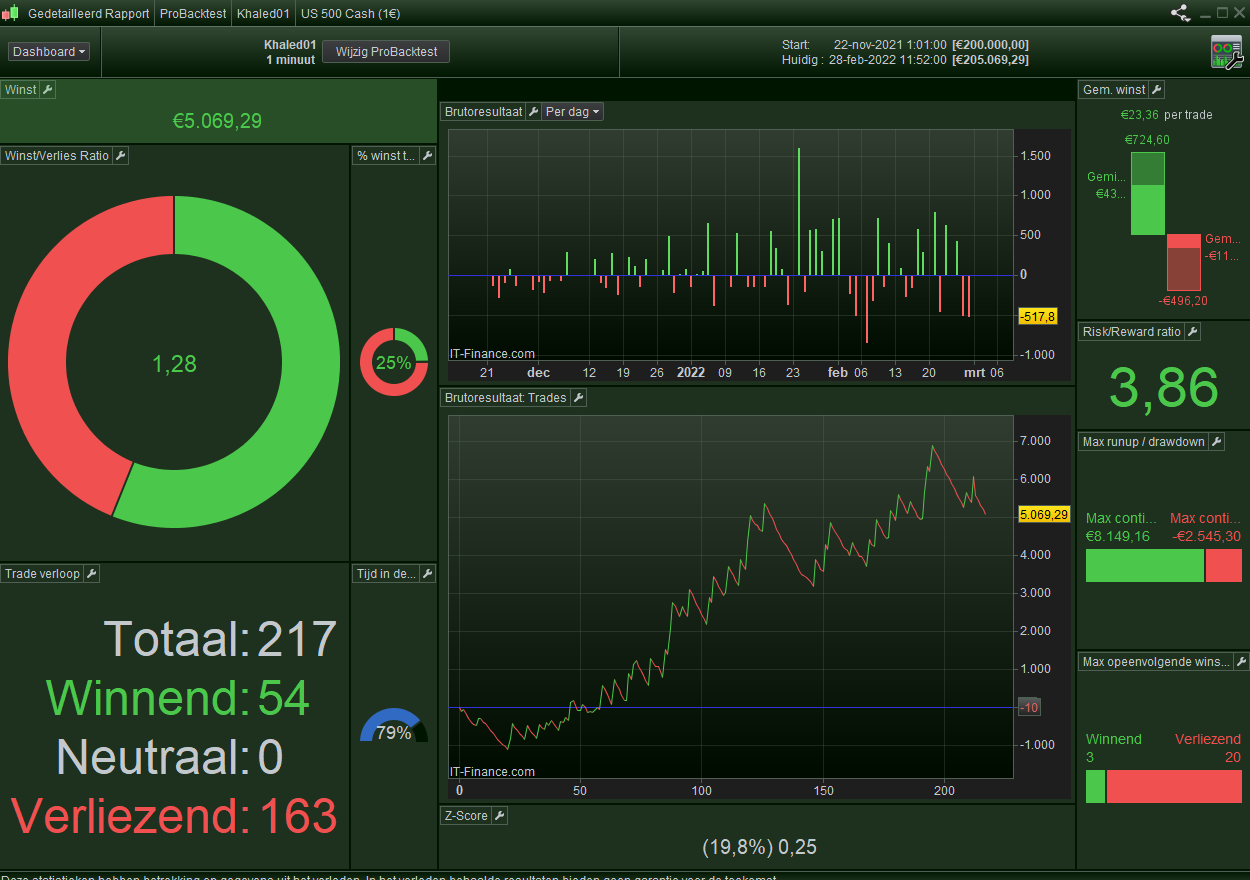

The code I provided generates in backtest a net gain of 5,328 with a WinRate of 25% and a Drawdown of -2500.

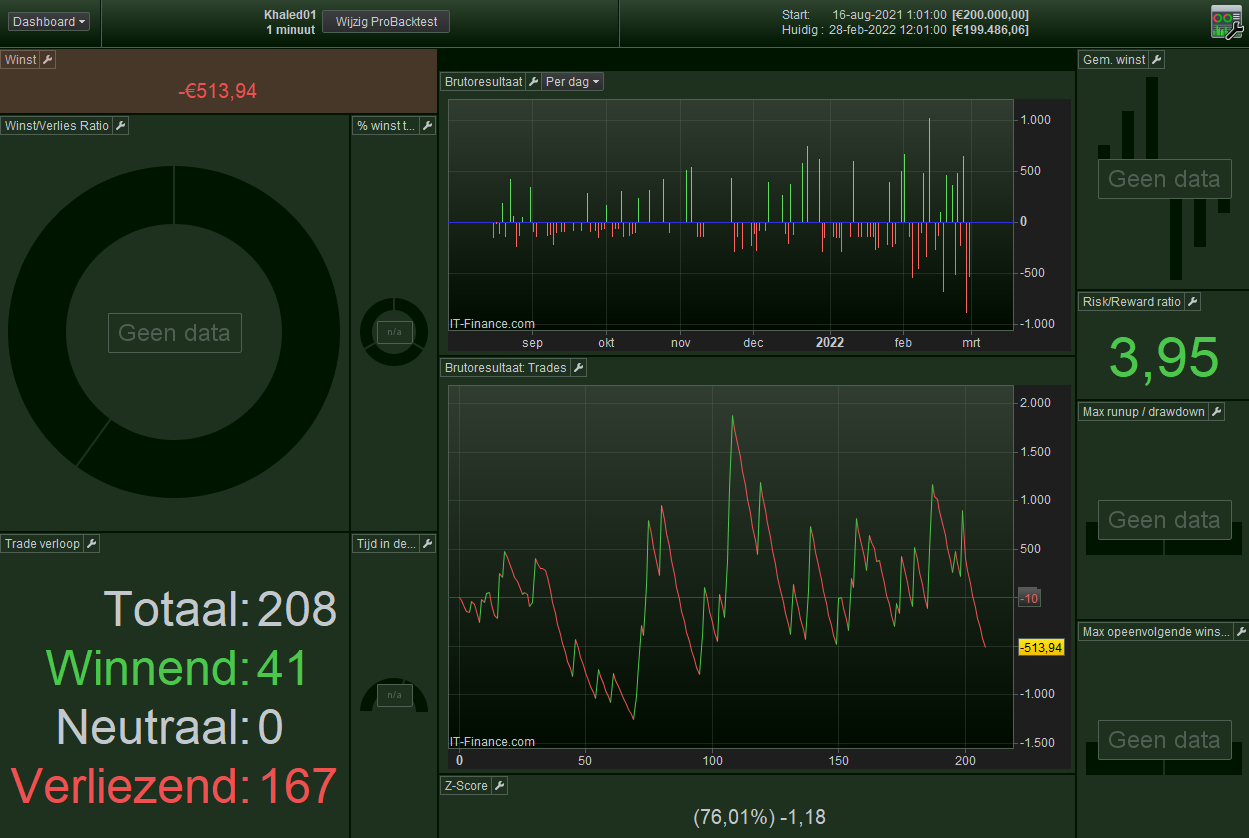

Without changing parameters such as SL, TP, Barsbefore, Barsafter, the code with your changes generates in backtest over the same period a net loss of -1,806 with a WinRate of 23% and a Drawdown of -1897.

So there is something in the original code that was certainly useful.

How can we please just overcome the problem of 1,000,000 values in the Array of the first code?

Much appreciated.

Hi Khaled,

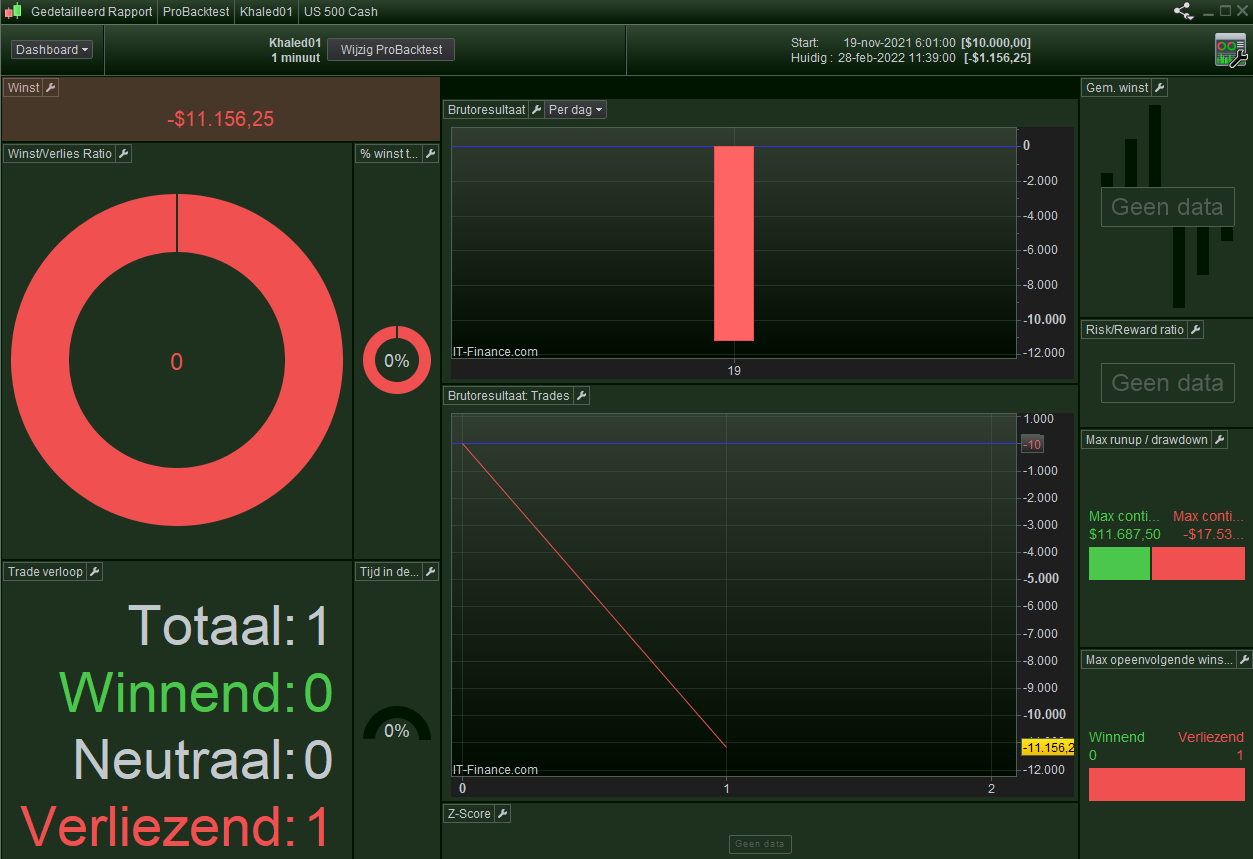

What did you mean “it works one time” ? One trade only like you see below ?

Otherwise I copied your code given to Nicoalas and this is the result. Can I be doing something wrong ?

All right. There is is. It required the correct 1euro instrument.

But no error messages (yet), and I removed the If 99999 WHICH btw has one 9 too few (I suggested 999999).

What’s next ?

🙂

In case you want to pursue this further : It doesn’t seem to be resilient to more normal markets (pre-Inflation – this is 200K).

N.b.: 1M fails on the “500” error @nonetheless also receives. This is not related to the arrays, as it seems.

Peter, thanks for taking the time.

What I meant by “worked one time”, the Algo took live 4 LONG trades in a row (entry and exit properly with small profit), then at the 5th Signal, I had again the same error message. I tried again and again and it’s the same error message.

The Backtest works fine.

The error appears only when I put it Live.

I suspect the solution is what you suggested earlier, limit the number of values in the Array table. May be it should be at the very beginning of the PP Fractals code so that no calculation is performed beyond 999,999

Much appreciated

limit the number of values in the Array table.

Because I don’t understand what it (the arrays) is doing there anyway, I suggest that we better interpret what @Nicolas is saying. So to me it now seems that he (from his own code ever back ?) tells that the arrays were only there for graphing, while you don’t graph anything. So just eliminate the code concerned (?).

Otherwise your error in Live (I missed that one – apologies) could be related to the 500-error I receive with the 1M backtest.