OK now I understand that the variables should be adapted only for the period. The results will be interesting, but we will have to be prudent because of the less number of positions in this case: if the backtest begins 10 years before, it means in fact only 10 month backtest; and if it begins in 1979, the old datas might be not relevant because of the prices of instruments that were sometimes extremely different than today. So the variables adapted for the whole year might be more secure… in fact everyone will have to choose.

Mark

MarkParticipant

Senior

Can somebody check this for me? FTSE (Jan2)

Im unsure how to create an ITF file so here is the code…

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily high/low crossings with smart position management

// Version 2 - long only

// Instrument: ??? mini 1D, ? points spread, account size 10.000 ?

// Rating ?

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 8

// define filter parameter

ONCE periodLongMA = 11

// define position and money management parameter

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

positionSize = 1

ONCE stopLossLong = 10 // in %

ONCE takeProfitLong = 7 // in %

maxPositionSizeLong = MAX(15,

Alco

AlcoParticipant

Senior

But for example, sugar has 6 zero’s from feb – april. So I don’t have to make an itf file for that period?

Are the variables for each month not quite similar as there are 3 months in green in a row? For example US500. It has 6 green boxes from march – may and one in june.

AlcoParticipant

Senior

@mbaker,

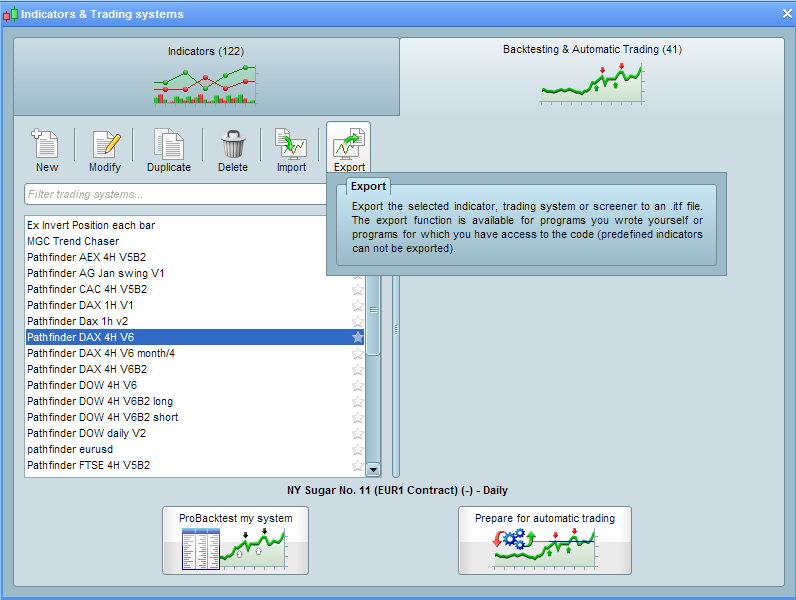

You have an export button in the indicator screen. Thats how you make an itf file.

AlcoParticipant

Senior

I found out, when you did all the variables. Do it once again! You get better results if you do it twice.

@mbaker

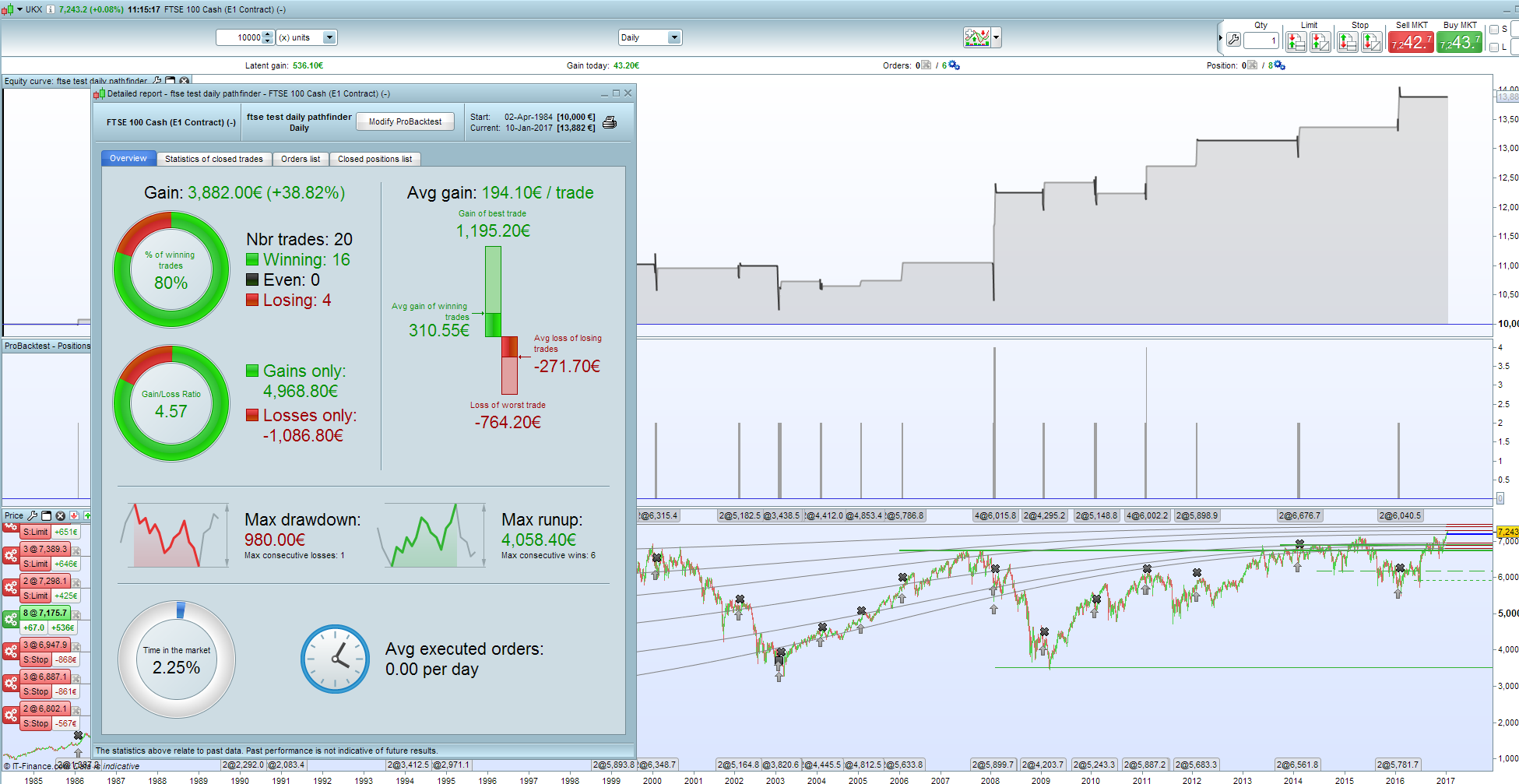

This is my result with ftse jan2

MarkParticipant

Senior

Ah, so go through your variables and set them, then go through them all again with the new variables. i get it

wp01

wp01Participant

Master

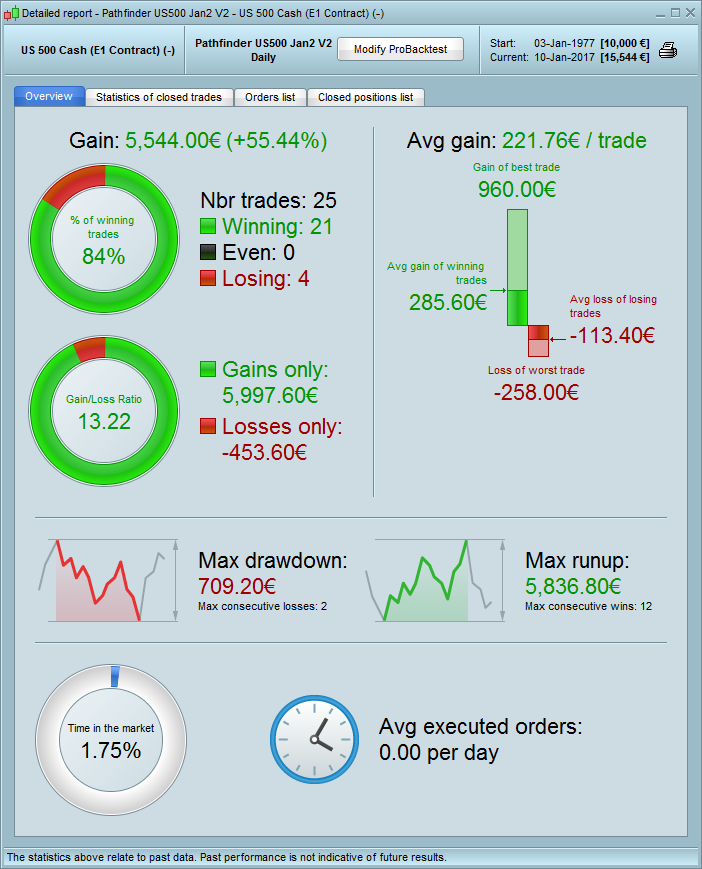

Attached US500 for Jan2.

Winning trades: 84%

Drawdown: 6,02%

I hope someone can check the results before using it.

Regards,

Patrick

MarkParticipant

Senior

@ALCO

I still don’t get your results

AlcoParticipant

Senior

@Patrick,

I’ve checked them. Looking good!

@mbaker

Have you tried my itf file? I made directly some changes from your file.

MarkParticipant

Senior

@Alco

Ah, you’ve concentrated mainly on least drawdown each variable?

wp01Participant

Master

@Alco

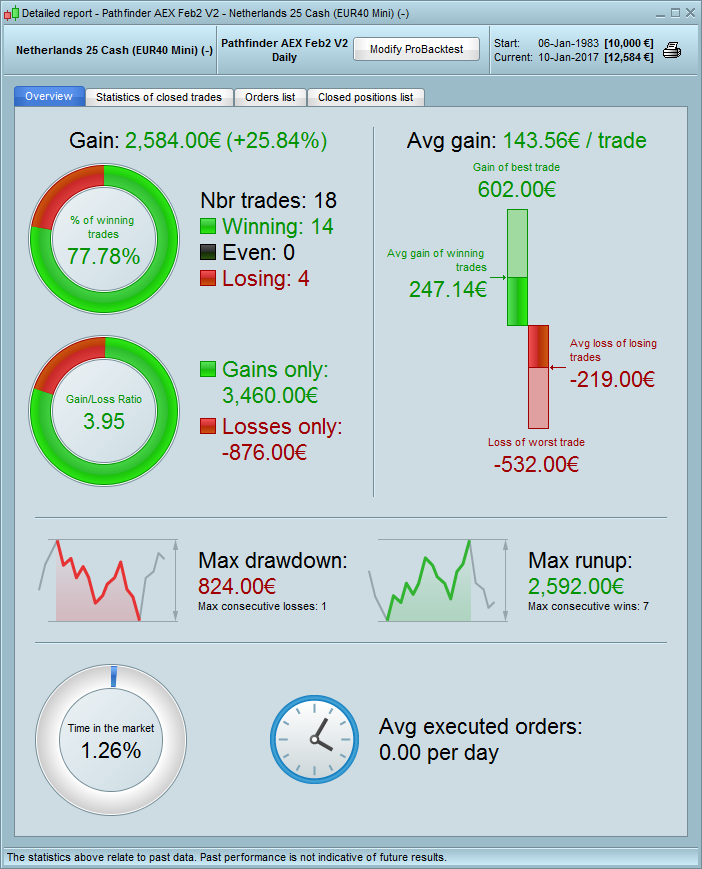

By the way: in your itf file from the ftse there was no spread included of 2 points.

Patrick

AlcoParticipant

Senior

@mbaker

Yes, sometimes you have maybe 100-300 more profit with a much higher drawdown. So then I choose for the lowest drawdown and less profit.

AlcoParticipant

Senior

@Patrick

Sorry I forgot to add it. But with only 20 trades taken in more than 30 years it doesn’t matter that much haha

Hi Guys,

I really like the team spirit here and see the passion you support each other.

Next step is to check your results and make a rating (A-C) of the different setups. I’ll add the robots for the most promising setups for the next period to the first post of this topic so everyone can easyly see the current status of our common project.

Best, Reiner