ALE

ALEModerator

Master

I’m very ecited by this Group!!

Hey Reiner,

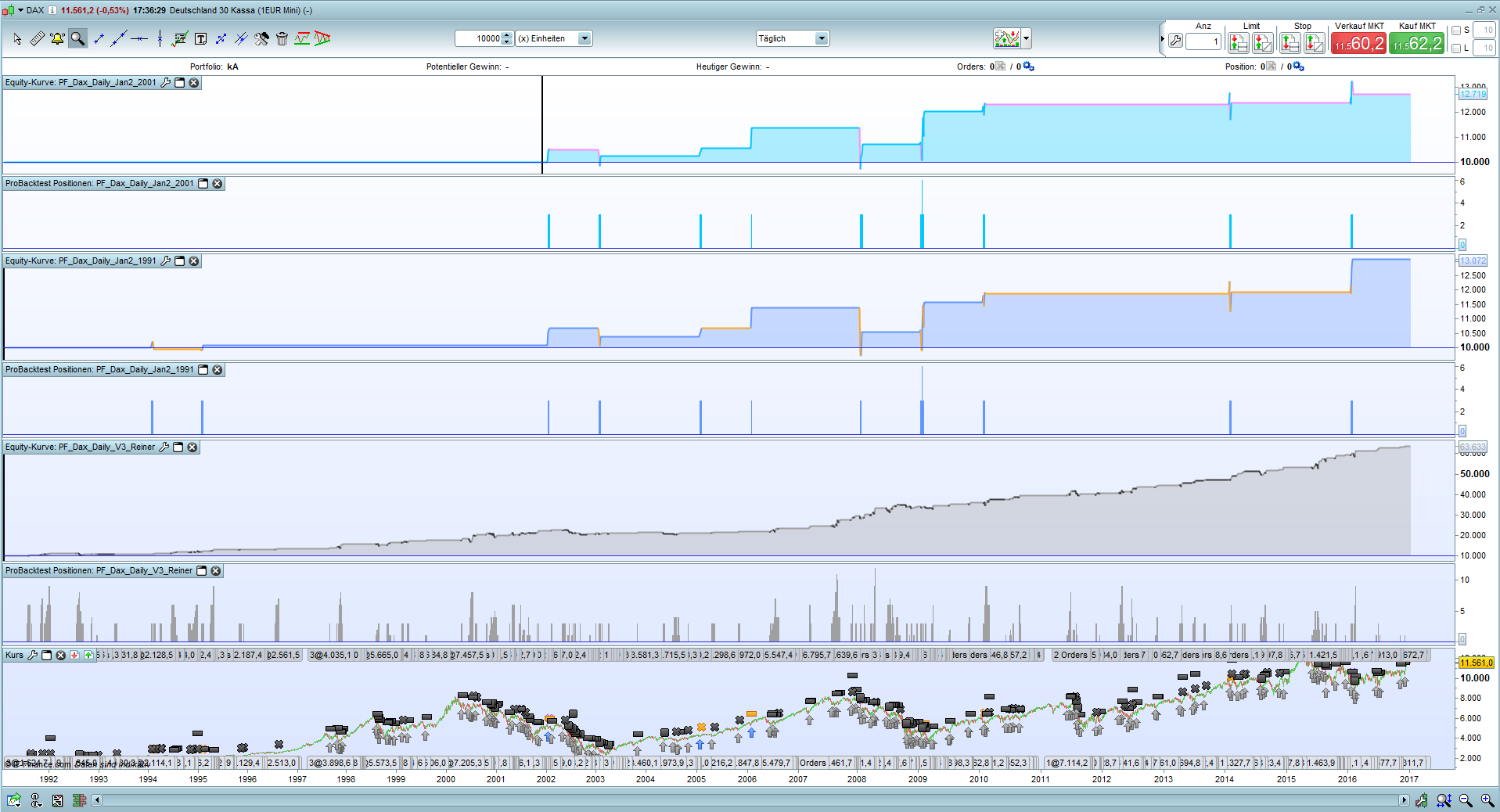

I am not sure how big the influence is, but in the system there are some Zero-Bar Trades… at least within the dax system.

hopefully we are able to use the version 10.3 soon, but until we need to work with this suboptimal solution.

Flo

Hey Reiner,

Is this what you had in mind?

Alco

AlcoParticipant

Senior

Hi Flowsen,

I’ve watched the video you posted.. I’m just a beginner and I still do not understand how to start with the optimization. Maybe it is to much to ask.. But it would be great if someone could make a video how they edit pathfinder for each instrument. Only one example is enough.

sorry for the spam today… zero bars seems to be no problem. if you get a new demo account, you will be able to work with prorealcode v10.3.(at least in germany).

and there the result is even better, than it is on v10.2 – so the system seems to be valid 🙂

@ Alco – could you be more specific at what step you are struggeling? the whole process of optimization takes some time, so a video is not my favorite solution 🙂

flo

AlcoParticipant

Senior

Ok I will try.

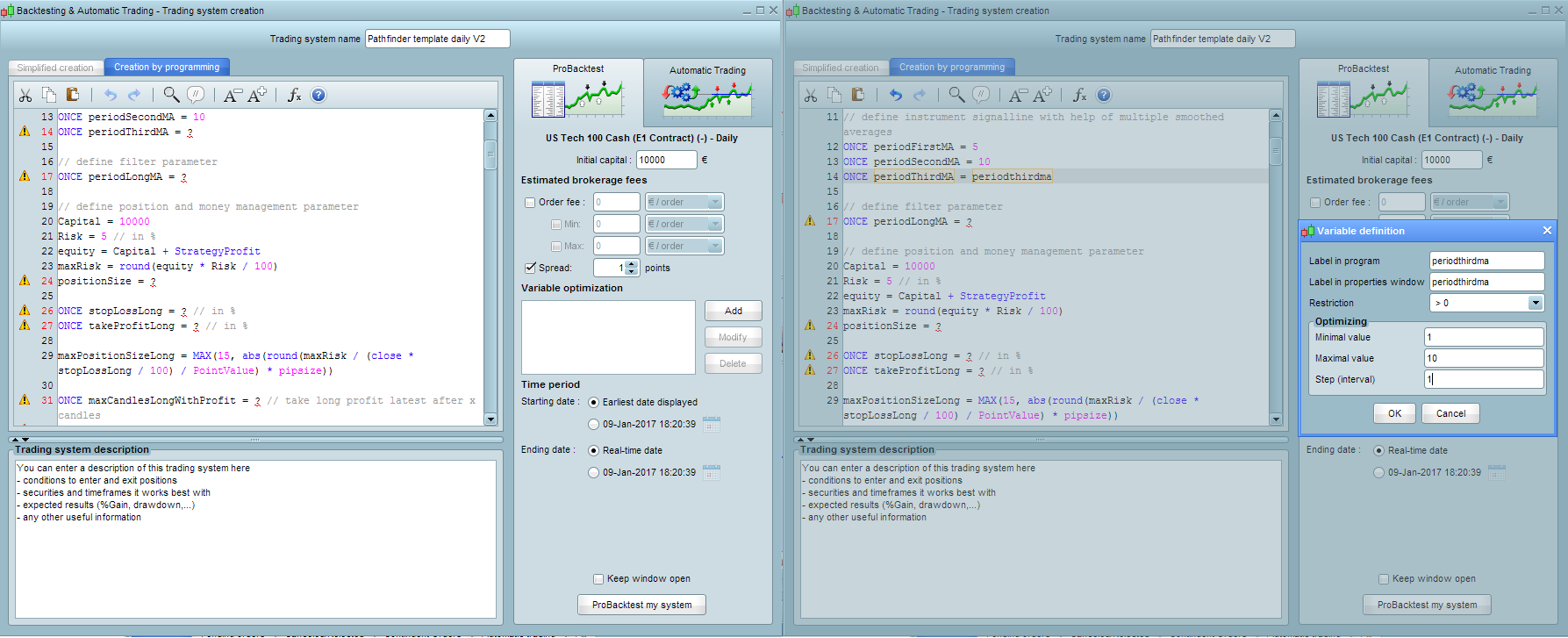

To change the variables, is this the way how to do it?

For example. You see: ONCE periodlongMA = ?

Then I change it to: ONCE periodlongMA = periodlongMA and add the variable.

Then I will add the numbers Reiner has given us for the seasonal multiplier.

@Arco: I do it this way:

– replace all the ? values with a default value e.g. 5

– replace the seasonal ? values with the values from reiners excel sheet, but just put in those for the next seasons, rest with 0

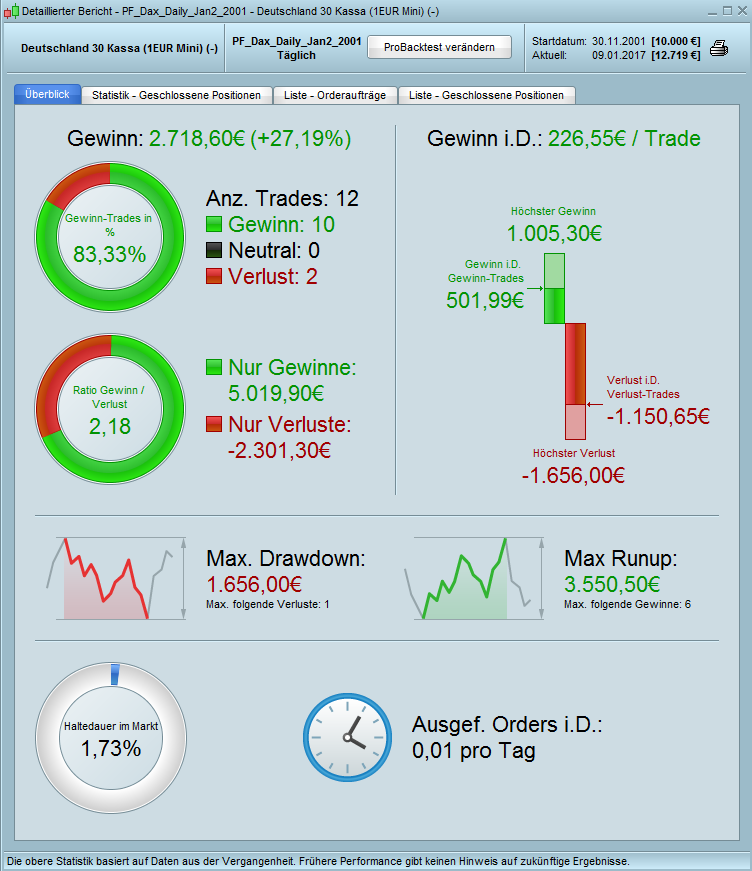

– can you run the program without errors? it should return an equity curve, with the tool-sign atop of the equity curve you can also open the “detailed report”

– now create a variable x with a range 1-20 and stepsize 1

– replace the first default value 5 with x, and let it run again

– choose from the result list the value with the highest winning trades and check the drawdown/max. loss in the detailed window

– replace x with the chosen value, continue to next default value

Hope this helps.

ALEModerator

Master

Hello Guys,

here the best solution is to make a specific video example to pathfinder daily optimization…

ALEModerator

Master

@reiner,

in your xls files SL coloumn mean signal line? If yes, it’s thirdperiodma? Because also firstma and secondma partecipate to build signal line, isn’t?

thanks

Ale

Hi ALE,

I have understood the same as you, but I think Reiner only take into account thirdperiodma for the optimization..but i don’t know why..

Hi Ale, yes, please verify only the third ma and let first (5) and second (10) unchanged.

Mark

MarkParticipant

Senior

I agree if someone could record a default video it would help.

or a different idea…

If Reiner could put together a list of instructions/check sheet detailing how to optimise the system and upload it as a file, i understand this will eat up some of your valuable time but this way you would only need to do it once then everyone could work from it without having to pester you with questions. Also i might add, if we are all running our optimisation slightly different then this is going to give inaccurate results, we all need to be following the same rules when testing to give the best result do you agree?

Mark

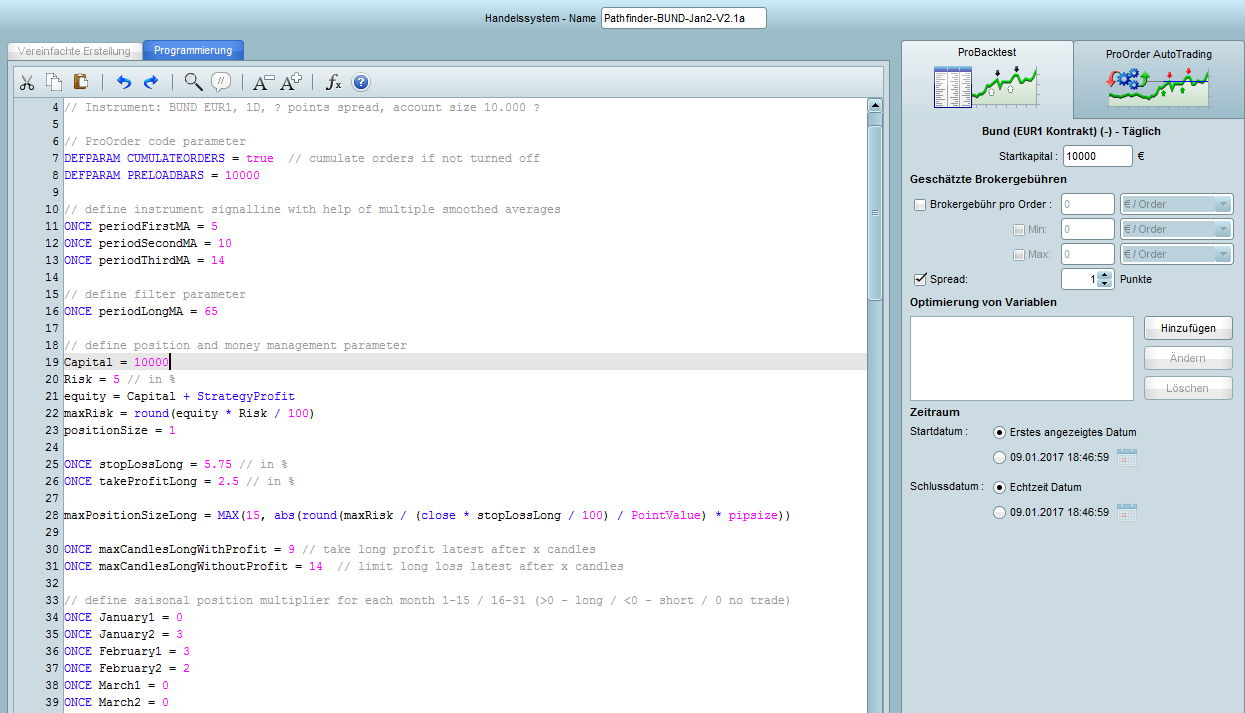

BUND / FGBL v2.1a

Here is the code for BUND … not my favorite. :-/

Only few trades, low profits, choppy equity curve. I think there are better instruments.

And since Yellen started to raise interest rates we wont see a lot of long signals here in the future.

Rating B?

AlcoParticipant

Senior

Ok guys, I finished Nasdaq. Please correct me if I did something wrong or need to change.