In the 2 weeks that I’ve been running it, the first trades were 12700, 12687, 12691 within 16 minutes between the first and last (Dec 21).

The second entries were 12681, 12706, 12715 about 40 minutes apart (dec 24).

Then one position opened on the 29th at 12914, still open.

Is that what you’ve got?

Judging from previous versions, this seems typical. If the entries were more widely spaced then either you’d be buying at a much worse price, or it’s fallen so far that the broader conditions are no longer met – in which case it may well be a losing trade and you’ll be pleased that there’s only one entry.

As I write I just started it a few days ago.

It took 3 trades (all Long) on Dec 28 at 12828 (17:14), 12835 (17:20) and 12836 (17:28), those were all closed (with a profit) on Dec 29 at 07:55.

Then it took 3 trades (all Long) on Dec 29 at 12914 (14:34), 12917,8 (14:42) and 12917,0 (14:52). Those were sold with a loss today at 15:38. Strange that it only took 1 trade for you, but 3 trades for me.

At 15:38 it just immediately opened a Short after it closed the positions above.

So you are correct. The trades are not taken immediately after eachother, they are spaced 6-10 minutes apart, or something like that. Does the behaviour seem accurate you think?

I’m talking about

- NAS-2m-HULL-SAR-v5.3L.itf

which is long only. Which algo are you running?

Also, did you adjust the Ctime settings for Sweden?

I am running HULL-SAR v3b.3, which seems to have shorts, right? I have not changed any time-setting as I am running ProRealTime with GMT time.

Would you advice I change to the version you link above?

v3b.3 was developed with just a 1 year backtest, so I wouldn’t recommend.

v5.3L is built on 6 years of data 75/25 so should be more reliable (in theory) and making it Long only improved performance dramatically. If you’re on GMT then it should be good to go with no changes.

Thanks for this! Will change!

Hi @Paul, I’ve been working on an ATR TS version of this in combination with your breakeven code but I’m finding that it doesn’t want to move the stop. This is the code I’m using:

// break even stop incl. cumulative positions

once enablebe = 1

if enablebe then

//====================

once besg = 0.3 //% break even stop gain

once besl = 0.04 //% break even stop level (+ or -)

besensitivity = 2 // [1] default [2] hl [3] lh [4]typicalprice(not use once)

//====================

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

benewsl=0

mypositionpricebe = 0

endif

positioncountbe = abs(countofposition)

if benewsl > 0 then

if positioncountbe > positioncountbe[1] then

if longonmarket then

benewsl = max(benewsl,positionprice * benewsl / mypositionpricebe)

else

benewsl = min(benewsl,positionprice * benewsl / mypositionpricebe)

endif

endif

endif

if besensitivity=1 then

besensitivitylong=close

besensitivityshort=close

elsif besensitivity=2 then

besensitivitylong=high

besensitivityshort=low

elsif besensitivity=3 then

besensitivitylong=low

besensitivityshort=high

elsif besensitivity=4 then

besensitivitylong=typicalprice

besensitivityshort=typicalprice

endif

if longonmarket then

if besensitivitylong-positionprice>=((positionprice/100)*besg)*pointsize then

benewsl=positionprice+((positionprice/100)*besl)*pointsize

endif

endif

if shortonmarket then

if positionprice-besensitivityshort>=((positionprice/100)*besg)*pointsize then

benewsl=positionprice-((positionprice/100)*besl)*pointsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if benewsl>0 then

sell at benewsl stop

endif

if benewsl>0 then

if low crosses under benewsl then

sell at market

endif

endif

endif

if shortonmarket then

if benewsl>0 then

exitshort at benewsl stop

endif

if benewsl>0 then

if high crosses over benewsl then

exitshort at market

endif

endif

endif

endif

mypositionpricebe = positionprice

endif

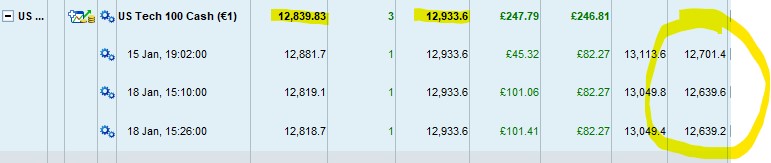

but if you look at the attached image, the stop should have moved when the price hit 12878.3, no?

Not anything to do with IG min Ts distance? They are quite high i think, like 10 points in spreadbet. Idk about CFD.

No, the min distance on the NAS is only 4. This should go to b/e after about 40 points, but it went over 90 and still nothing.

I always feel better once i know a position is all locked up and can’t lose money.

thanks a lot for this algo! Did you tried to adapt it on DJ?

Still working on it, but doesn’t look quite as promising as the NAS.

Paul

PaulParticipant

Master

hi nonetheless , I didn’t saw your previous post with the question regarding the breakeven. I haven’t looked into this, but it’s probably not relevant anymore now you ‘ve the code from Roberto. I’am curious how it would perform on this strategy.

Thanks Paul, I’ve been playing around with all different TS for this, and yes now Roberto’s is another option – still tinkering with that one.

Curious about your breakeven + ATR TS, it seems to behave properly (ie positions do close as if the stop had moved) but it’s not indicated in the open positions window. Also on the IG web platform, the SL display never changes but then the position will mysteriously close, as if the stop had moved.

Have you ever seen this?

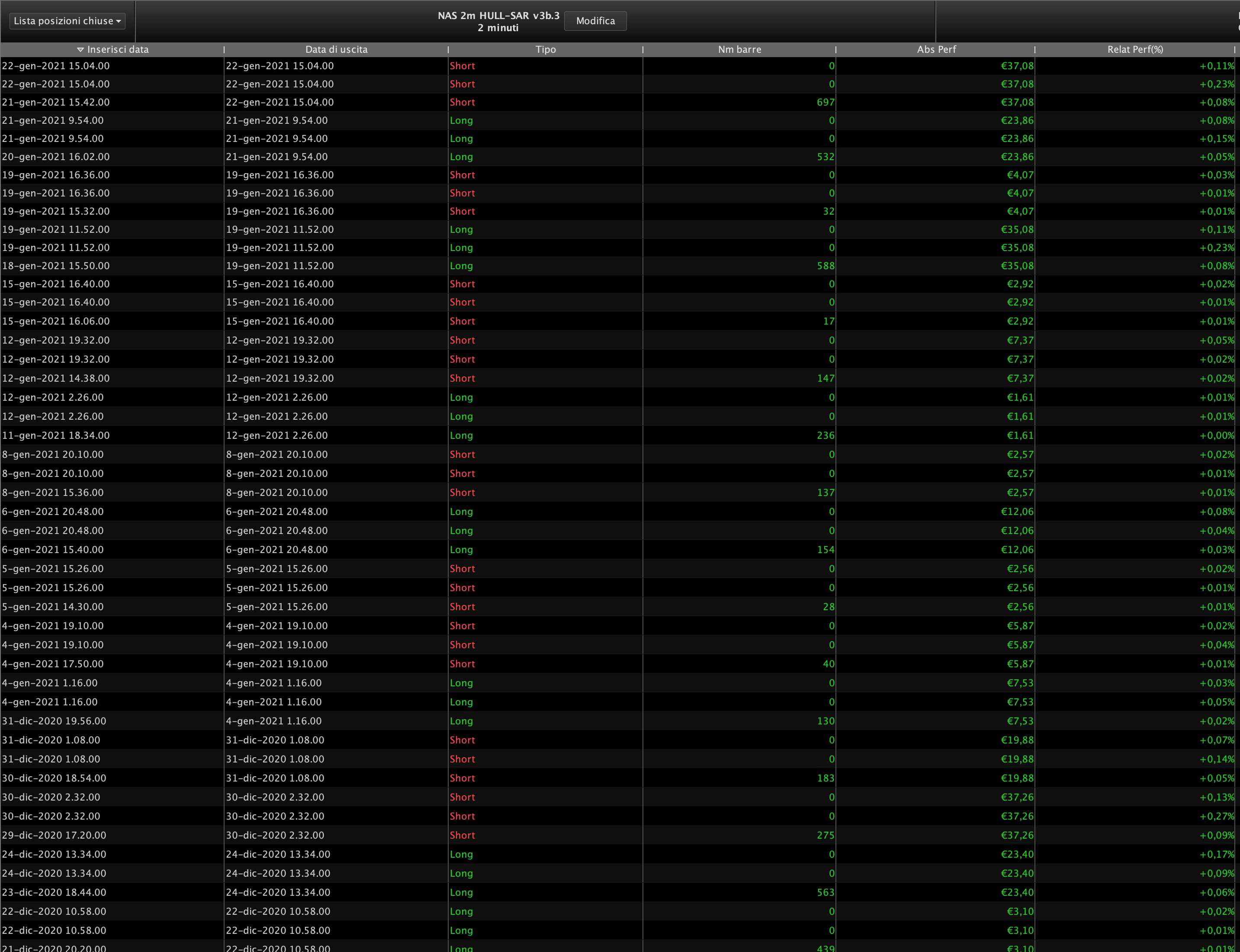

Hi guys, I did a small backtest on the Dax time frame 2 minutes with excellent results even if only for a month, but the real time strategy I tested on Friday 22 January did not open any positions, while the backtest shows 2 open positions. Can anyone explain to me why and if there is an error to correct? Thanks.