s83

s83Participant

Junior

Now its fixed! I was running both L and S 🙈

Can you help me with my other problem too?

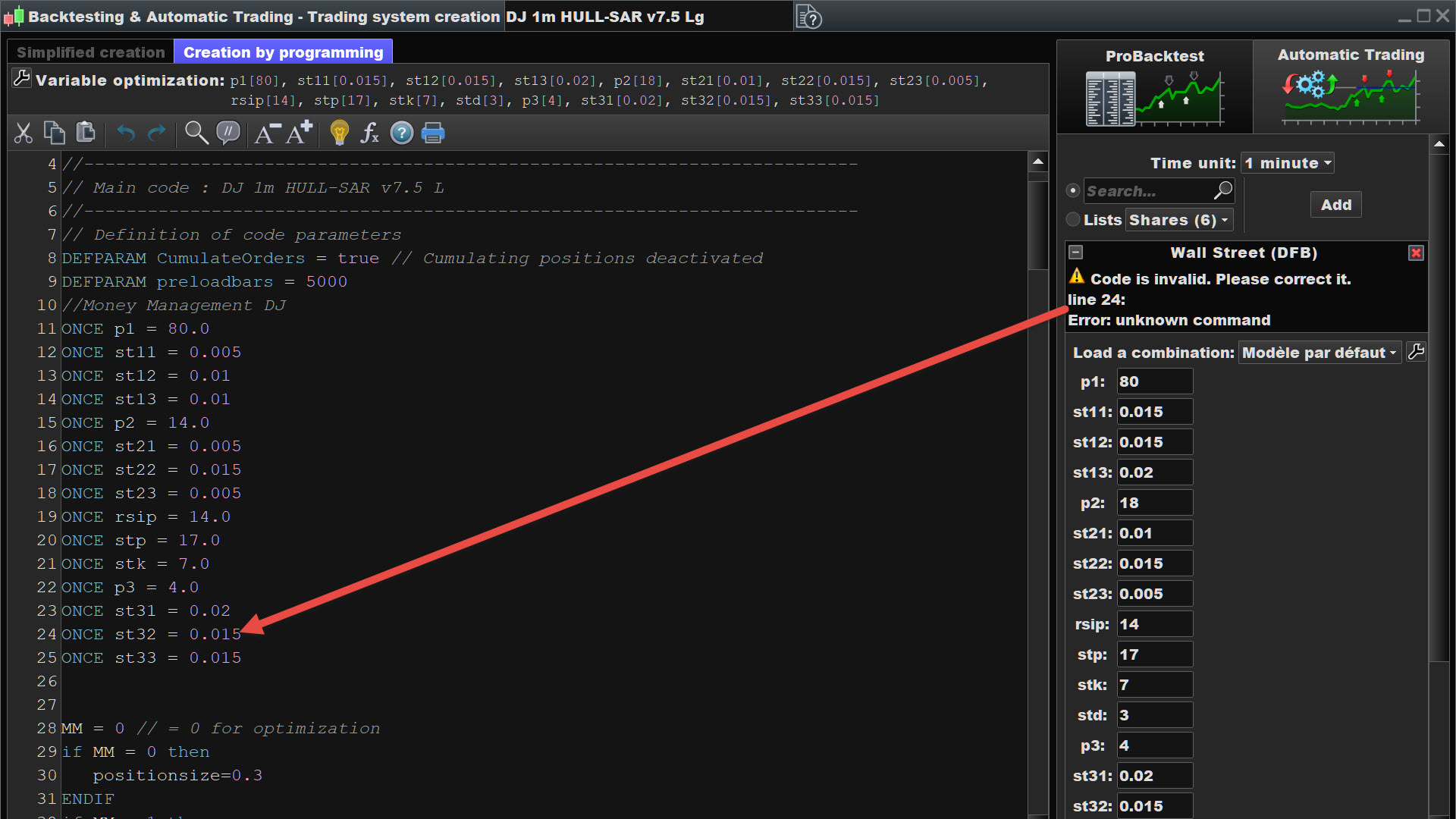

DJ 1m HULL-SAR v7.5 L

//-------------------------------------------------------------------------

// Main code : DJ 1m HULL-SAR v7.5 L

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Main code : DJ 1m HULL-SAR v7.5 L

//-------------------------------------------------------------------------

// Definition of code parameters

DEFPARAM CumulateOrders = true // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

//Money Management DJ

ONCE p1 = 80.0

ONCE st11 = 0.005

ONCE st12 = 0.01

ONCE st13 = 0.01

ONCE p2 = 14.0

ONCE st21 = 0.005

ONCE st22 = 0.015

ONCE st23 = 0.005

ONCE rsip = 14.0

ONCE stp = 17.0

ONCE stk = 7.0

ONCE p3 = 4.0

ONCE st31 = 0.02

ONCE st32 = 0.015

ONCE st33 = 0.015

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=0.3

ENDIF

if MM = 1 then

ONCE startpositionsize = .2

ONCE factor = 20 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.008) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // IG first tier margin limit

ONCE maxpositionsize = 550 // IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF StrategyProfit <> StrategyProfit[1] THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

Ctime = time >=153000 and time <220000

TIMEFRAME(15 minutes)

Period= p1 //105

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1] or HULLb > HULLa

c2 = HULLa < HULLa[1] or HULLb < HULLa

ST1 = SAR[st11,st12,st13] //0.01, 0.015, 0.015

c1a = (close > ST1)

c2a = (close < ST1)

TIMEFRAME(5 minutes)

Periodb= p2 //20

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c3 = HULLb > HULLb[1]

c4 = HULLb < HULLb[1]

c3b = HULLb > HULLb[1] and HULLb[1] < HULLb[2]

c4b = HULLb < HULLb[1] and HULLb[1] > HULLb[2]

ST2 = SAR[st21,st22,st23] // 0.005, 0.015, 0.005

c3a = (close > ST2)

c4a = (close < ST2)

//Stochastic RSI | indicator

lengthRSI = rsip //RSI period 15

lengthStoch = stp //Stochastic period 14

smoothK = stk //Smooth signal of stochastic RSI 7

smoothD = std //Smooth signal of smoothed stochastic RSI 3

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c3c = K>D

c4c = K<D

TIMEFRAME(default)

Periodc= p3 //4

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c5 = HULLc > HULLc[1] and HULLc[1] < HULLc[2]

c6 = HULLc < HULLc[1] and HULLc[1] > HULLc[2]

c5b = HULLc > HULLc[1]

c6b = HULLc < HULLc[1]

ST3 = SAR[st31,st32,st33] //0.02, 0.015, 0.015

c5a = (close > ST3)

c6a = (close < ST3)

Once MaxPositionsAllowed = 1*positionsize

// Conditions to enter long positions

IF not longonmarket and Ctime and c1 and c1a AND C3a and c3b and c3c AND C5a and c5b THEN

BUY positionsize CONTRACT AT MARKET

elsif longonmarket and Ctime and c1 and c1a and c3 and c3a and c5 and COUNTOFLONGSHARES < MaxPositionsAllowed then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.1

SET TARGET %PROFIT 1.6

ENDIF

// Conditions to enter short positions

IF not shortonmarket and Ctime and c2 and c2a AND C4a and c4b and c4c AND C6a and c6b THEN

sellshort positionsize*0 CONTRACT AT MARKET

elsif shortonmarket and Ctime and c2 and c2a and c4 and c4a and c6 and COUNTOFSHORTSHARES < MaxPositionsAllowed then

sellshort positionsize*0 CONTRACT AT MARKET

SET STOP %LOSS 1

SET TARGET %PROFIT 1.4

ENDIF

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

once trailingpercentlong = 0.35 // %

once trailingpercentshort = 0.38 // %

once accelerator = 0.03 // 1 = default; always > 0 (i.e. 0.5-3)

once accelerator2 = 0.1 // 1 = default; always > 0 (i.e. 0.5-3)

once ts2sensitivity = 0 // [0]close;[1]high/low;[2]low;high

//====================

once steppercentlong = (trailingpercentlong/10)*accelerator

once steppercentshort = (trailingpercentshort/10)*accelerator2

if onmarket then

trailingstartlong = positionprice[1]*(trailingpercentlong/100)

trailingstartshort = positionprice[1]*(trailingpercentshort/100)

trailingsteplong = positionprice[1]*(steppercentlong/100)

trailingstepshort = positionprice[1]*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=2 then

ts2sensitivitylong=low

ts2sensitivityshort=high

else

ts2sensitivitylong=close

ts2sensitivityshort=close

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

s83Participant

Junior

@murre87

nu varnar den för rad 24 istället då jag kopierade av den du la in nyss 🤔😔🙈

Kan ju inte påstå att jag är duktig på detta, men jag brukar iaf få det att fungera. Baktesten fungerar att köra.

s83Participant

Junior

@grahal try this and see if it works for you.

s83Participant

Junior

Can someone link codes that works with V11? I have tried many hulls now but ill get error messages when i try to start an automatic trade.

Backtest is working.

Yep same for me, error code now referring to Line 24, see attached.

I dont remeber witch one i started but choose one on DJ-1.. from “View all attachments”

We assumed the version you posted the full code for above is the version that works for you (in ProOrder) with no errors … are you now saying this is not the case?

Have you got DJ 1m HULL-SAR v7.5 L runnng in ProOrder murre87?

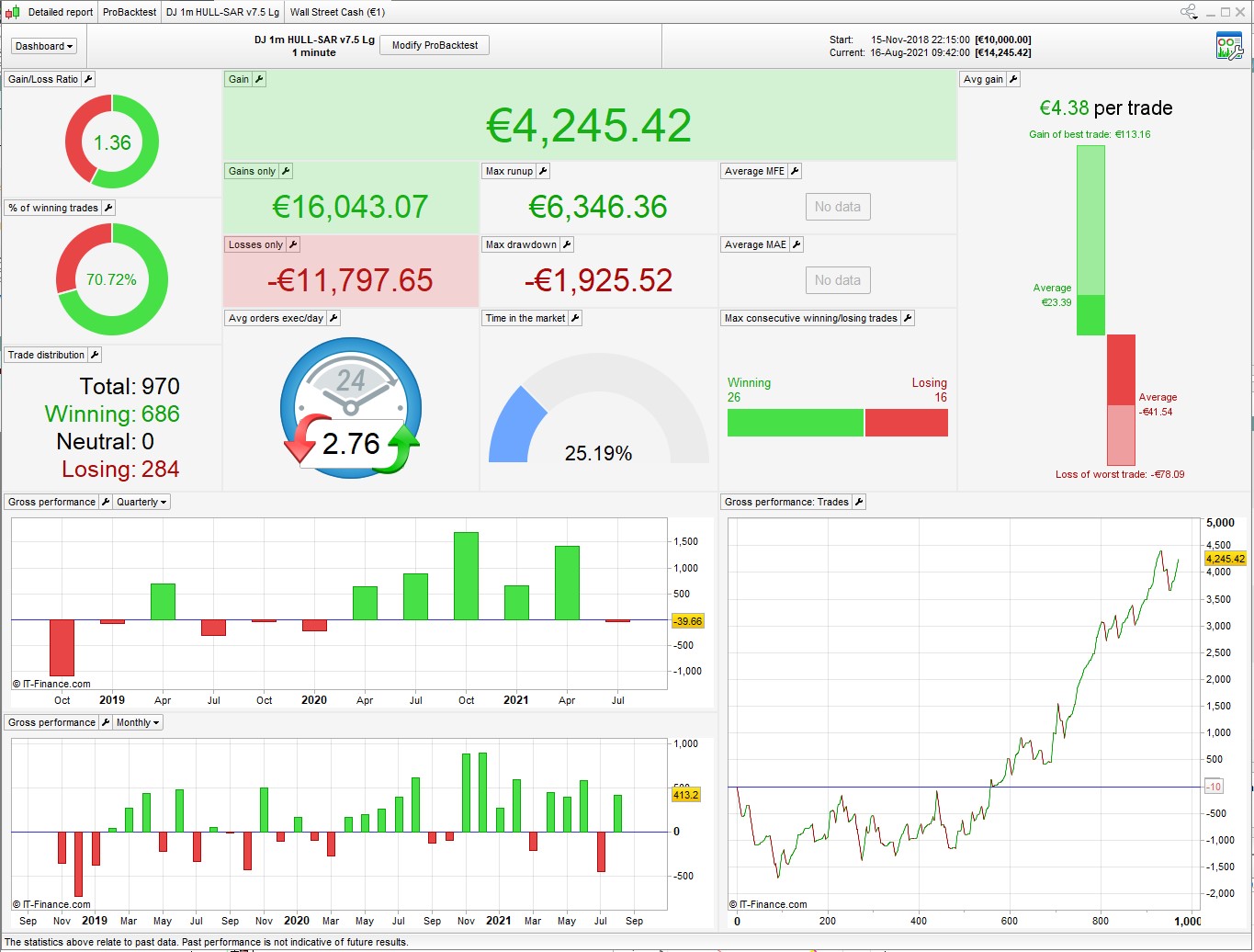

this is the 1m bar backtest of DJ 1m HULL-SAR v7.5 Lg (as posted here Free profitable strategies )

It looks like a variation of a code that i built in v10.3 on a 200k backtest but rejected after v11 came along. Then someone else made alterations to it and errors have been introduced.

I’ll have a look at it when I get a chance but frankly it looks like a dog to me and probably not worth it.

The code that Murre87 has posted above as DJ 1m HULL-SAR v7.5 L looks like a re-optimisation with max positions = 1

Does that also give errors?

Murre87 has posted above as DJ 1m HULL-SAR v7.5 L

Yes the above version gives a Line 24 error (but doubt it is LIne 24, see my screenshot above) when trying to start on ProOrder.

Ok, one problem I just noticed is in the stochasticRSI:

smoothD = std //Smooth signal of smoothed stochastic RSI 3

std is a reserved term for standard deviation (also sexually transmitted disease), so can’t be used as a variable. Try changing this to sd (or anything else) and re-run the optimisation. Using std there will completely warp the results.

problem number 2

// Conditions to enter long positions

IF not longonmarket and Ctime and c1 and c1a AND C3a and c3b and c3c AND C5a and c5b THEN

BUY positionsize CONTRACT AT MARKET

elsif longonmarket and Ctime and c1 and c1a and c3 and c3a and c5 and COUNTOFLONGSHARES < MaxPositionsAllowed then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.1

SET TARGET %PROFIT 1.6

ENDIF

The stop and target are in the elsif command for additional positions, but because MaxPositionsAllowed = 1 the elsif never happens, so the stop never registers. This is why it appears to be so successful, positions just stay open until they get into profit – sometimes for months with massive drawdown. If you want to run it with MaxPositionsAllowed = 1 (or CumulateOrders = false) then the elsif should be removed, or try:

// Conditions to enter long positions

IF not longonmarket and Ctime and c1 and c1a AND C3a and c3b and c3c AND C5a and c5b THEN

BUY positionsize CONTRACT AT MARKET

elsif longonmarket and Ctime and c1 and c1a and c3 and c3a and c5 and COUNTOFLONGSHARES < MaxPositionsAllowed then

BUY positionsize CONTRACT AT MARKET

ENDIF

IF longonmarket then

SET STOP %LOSS 1.1

SET TARGET %PROFIT 1.6

endif

Hi. If you got one dj 1 min-algo woring. Pls post all code at once or itf-file

bege

begeParticipant

Average

Hi!

Can someone backtest “NAS 1m HULL-SAR v4.5” with 1M bars? On 200k it looks really good!