Try changing TradePrice in the TS snippets to PositionPrice (is that the correct term for the average trade price of all open positions)?

Just an idea before bed! 🙂

Paul

PaulParticipant

Master

if you limit the number of open positions to i.e 5, an option would be maybe to have separeated individual trailing stops for tradeprice(1),tradeprice(2) etc

ive made in the past a ts for 2 cul. positions in some topic

not a nice way because you get lots of code

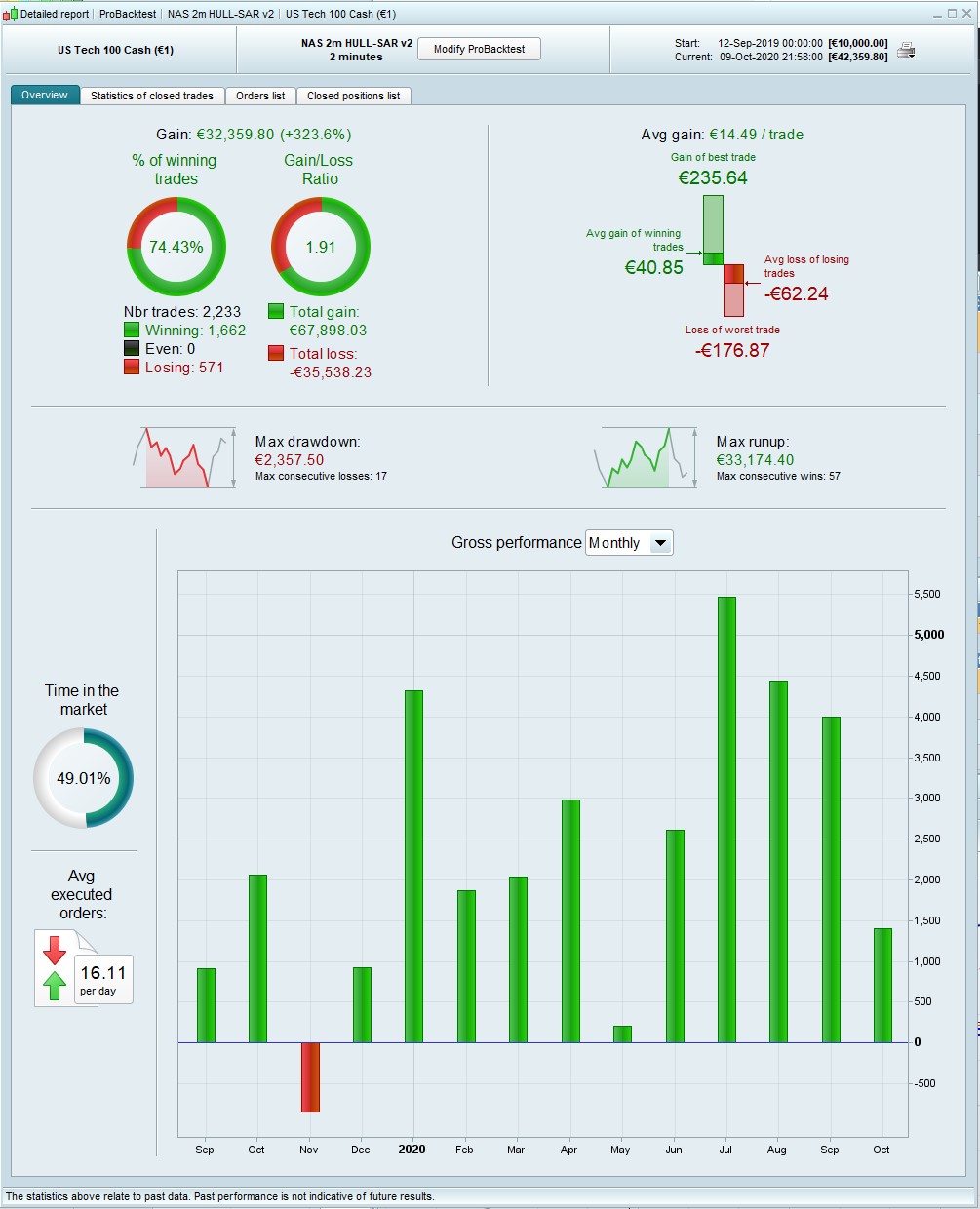

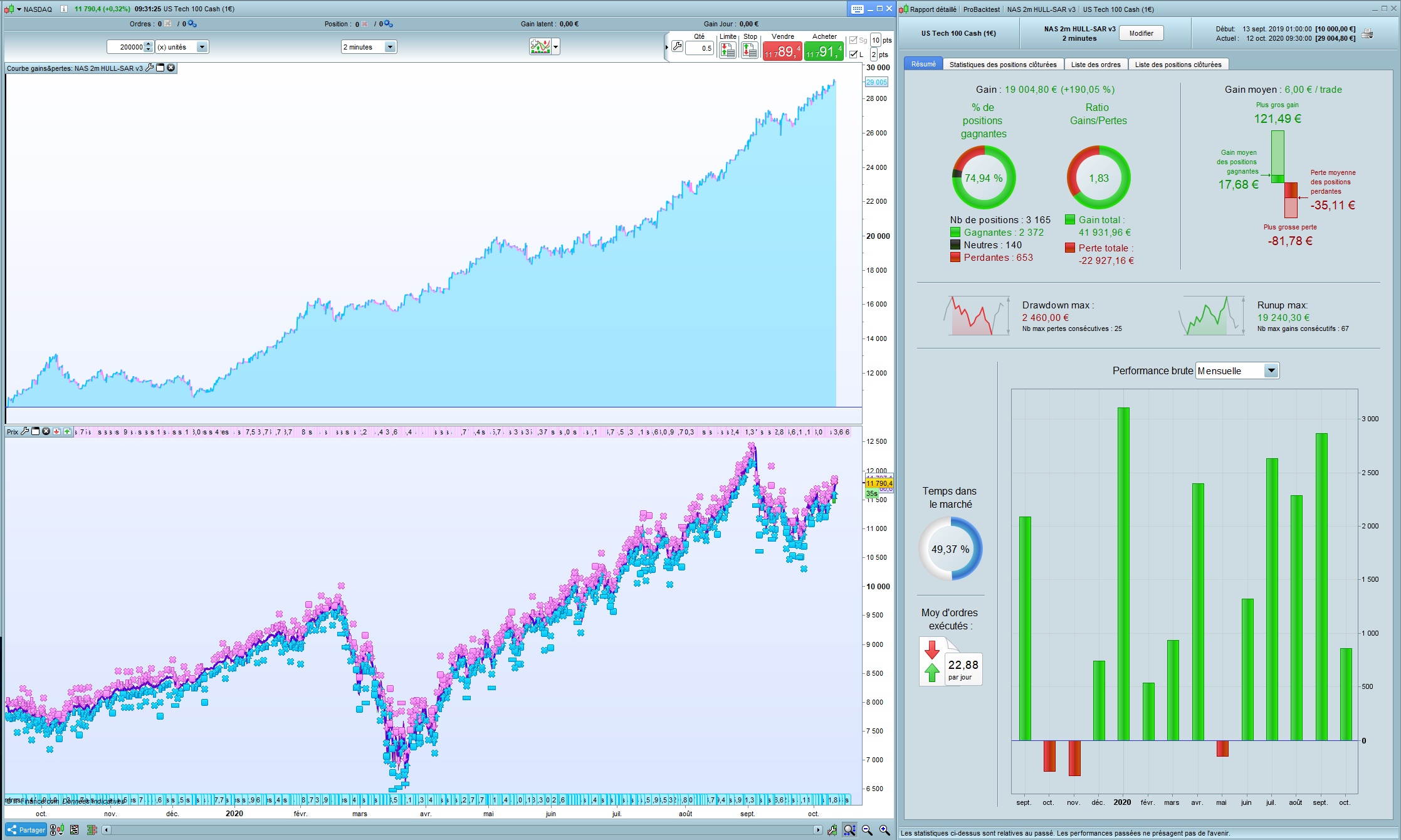

Grahal’s suggestion of using positionprice instead of tradeprice seems to make a big difference. TS should now start from the average price.

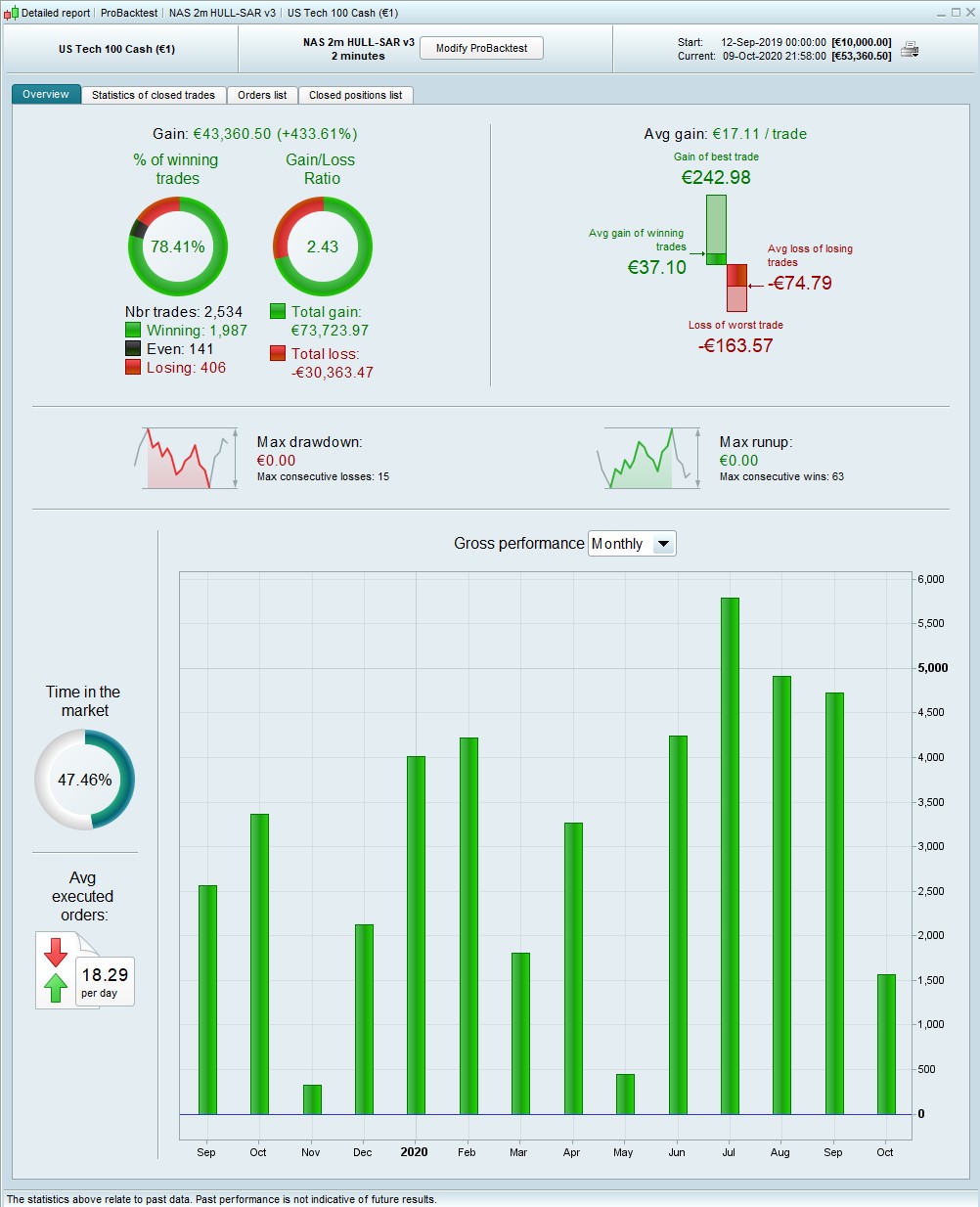

Revised with correction to the TS, tames the excesses – lower profit but better win %, optimized for max pos = 6

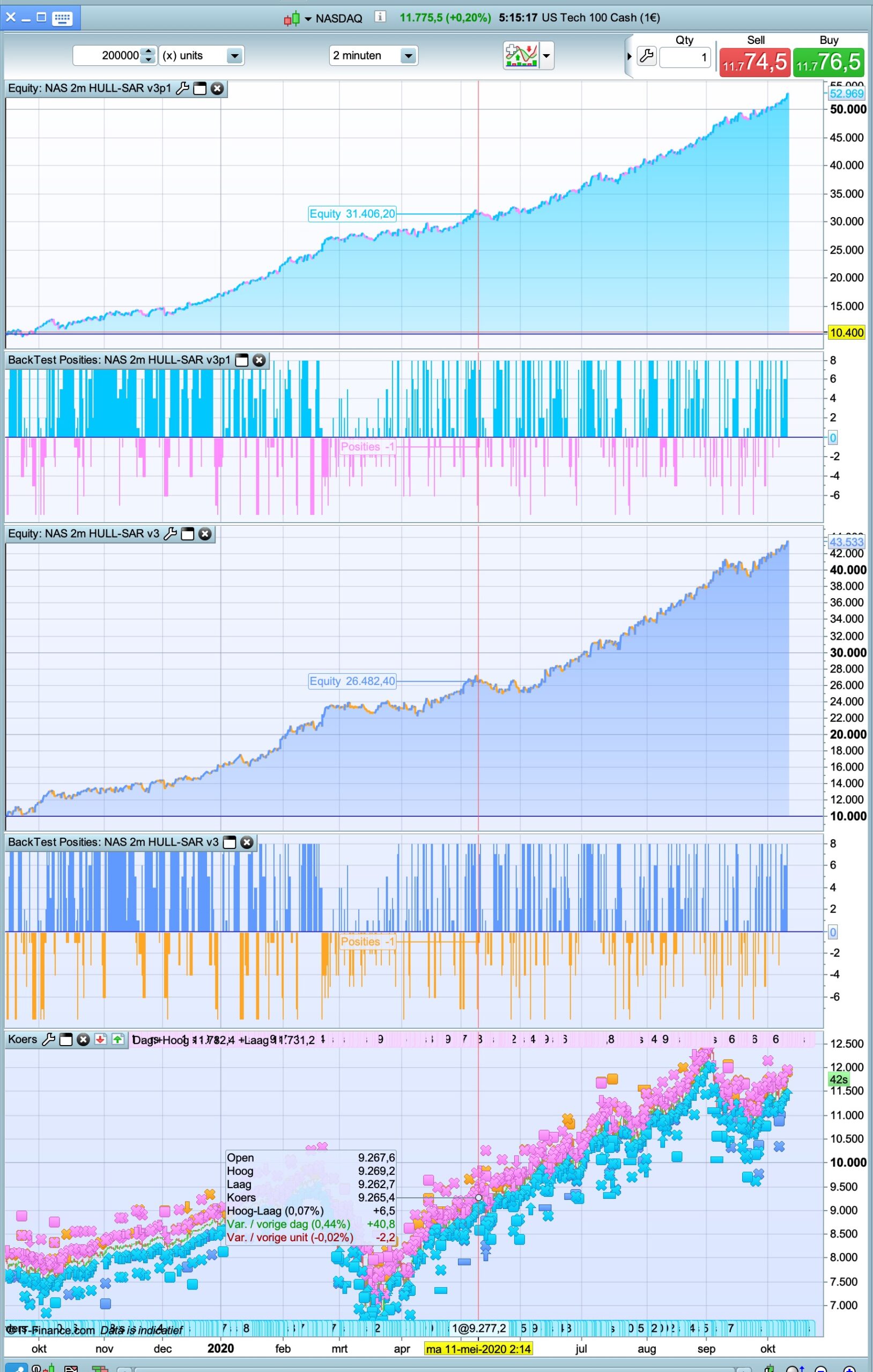

further revision to the TS (grazie Roberto) and re-optimized. Interestingly, there is now a sweet spot for max positions – it starts getting good at 4 and peaks at 8 (attached illustration). Above that performance falls off.

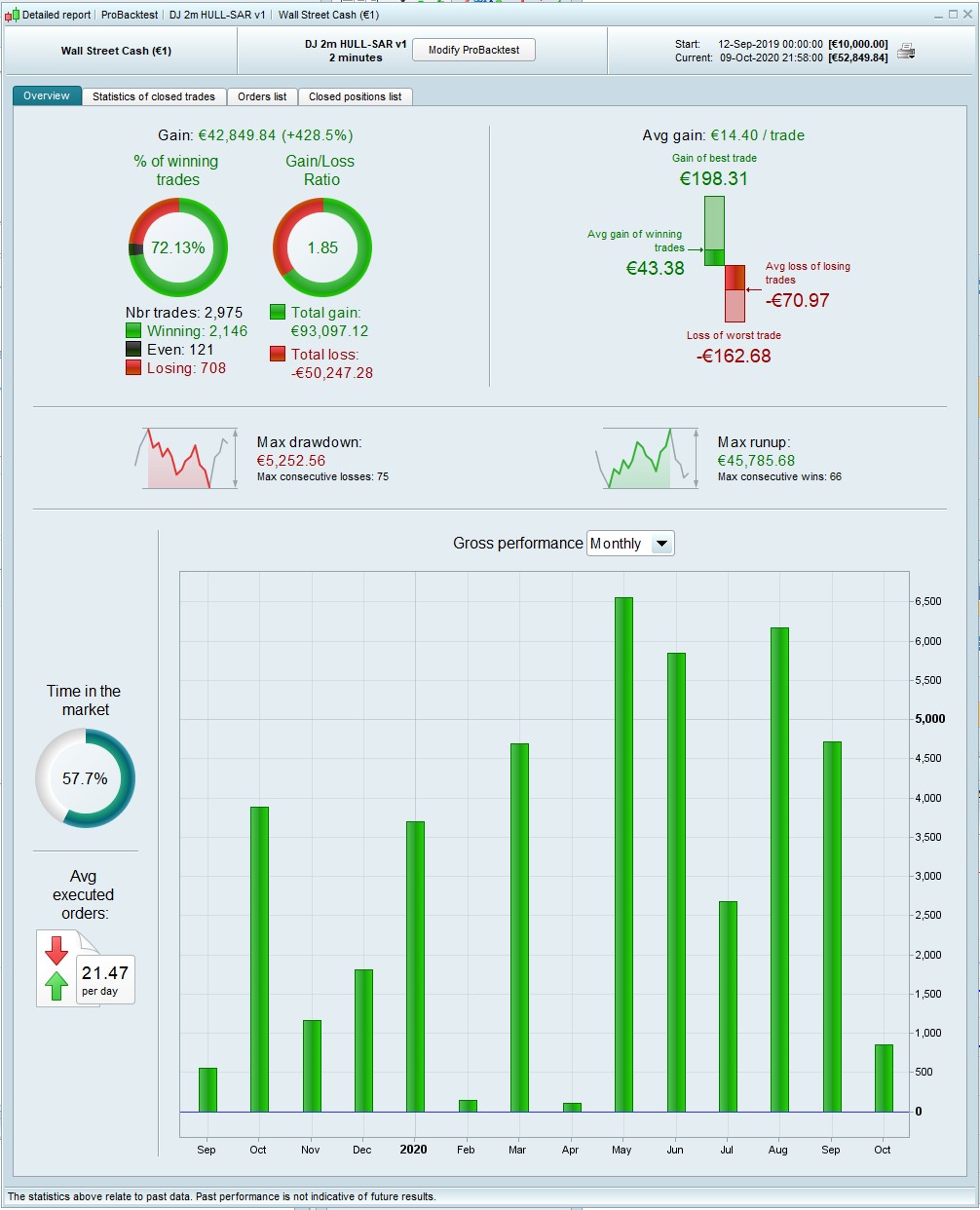

near identical performance on the Dow (equivalent position size =.4), with the advantage of smaller min position.

PaulParticipant

Master

Hi Nonetheless,

I took the excellent cumulative trailingstop snippet of robertogozzi and splitted it for long & short, same as vectorial. This gives another nice improvement overall.

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

once trailingpercentlong = 0.49 // %

once trailingpercentshort = 0.28 // %

once accelerator = 1 // 1 = default; always > 0 (i.e. 0.5-3)

once ts2sensitivity = 0 // [0]close;[1]high/low;[2]low;high

//====================

once steppercentlong = (trailingpercentlong/10)*accelerator

once steppercentshort = (trailingpercentshort/10)*accelerator

if onmarket then

trailingstartlong = positionprice[1]*(trailingpercentlong/100)

trailingstartshort = positionprice[1]*(trailingpercentshort/100)

trailingsteplong = positionprice[1]*(steppercentlong/100)

trailingstepshort = positionprice[1]*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=2 then

ts2sensitivitylong=low

ts2sensitivityshort=high

else

ts2sensitivitylong=close

ts2sensitivityshort=close

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

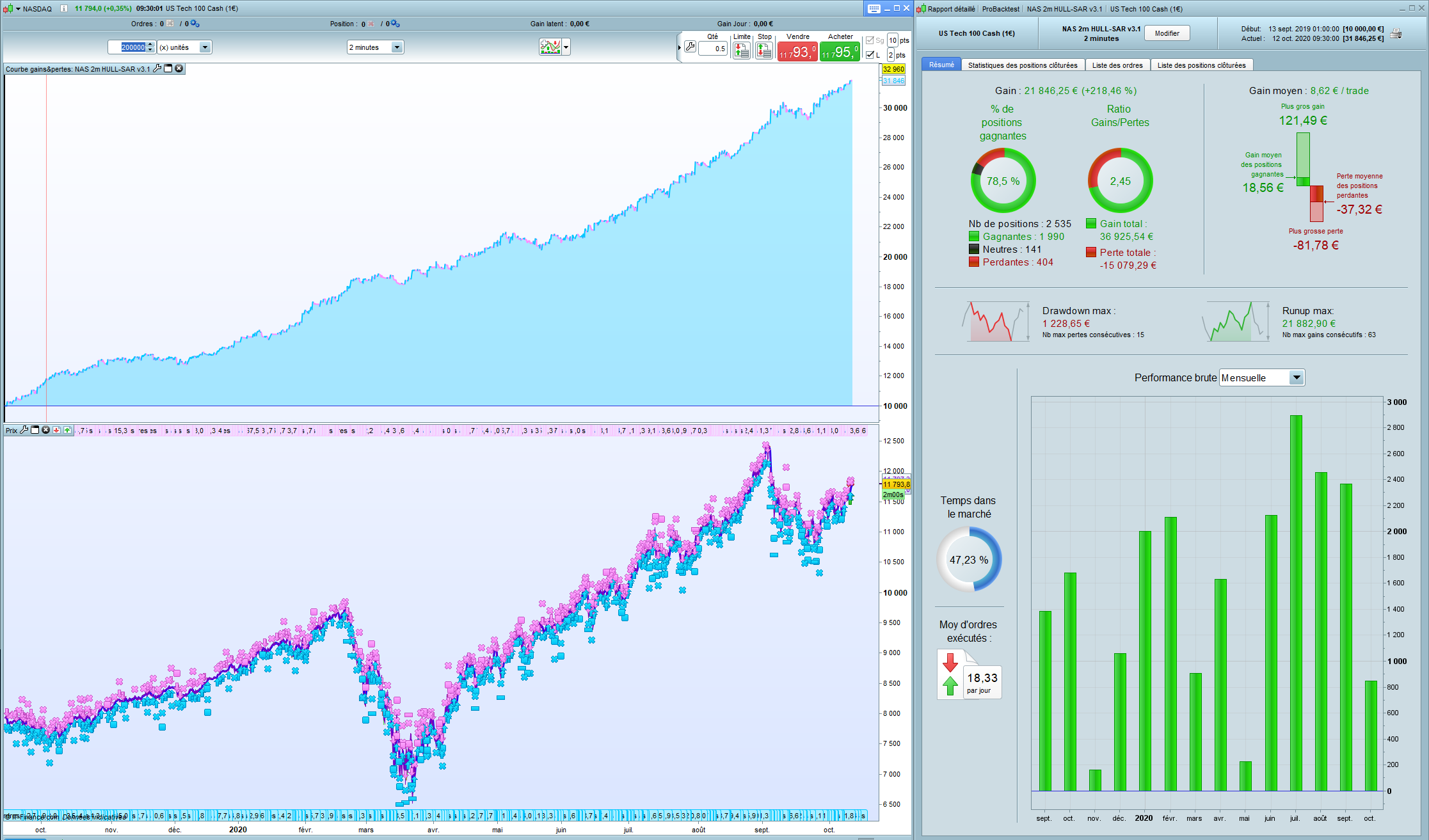

I thought that 8 positions was a bit too big.

I tried to optimized this parameters and the better one was 4 (and for me obviously it decrease the DD)

Results on 200k attached

Nice one Paul! I have also been working on long and short versions – your solution is more elegant, I just made 2 different algos.

But I’m also trying an alteration to the entry code so that the initial position is based on the 6min turnaround, with additional positions based on the 2min. Logically I think this makes more sense – to catch the bottom/top of the 6min run rather than entering anywhere along that trend. I’m running all these versions in demo to see what works better in actual trading.

Ich I have a little bit better results with Paul´s Version with small changes.

Ctime = time >=143000 and time <213000

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.1

SET TARGET %PROFIT 2.0

ENDIF

// Conditions to enter short positions

IF Ctime and c2 and c2a AND C4 and c4a AND C6 and c6a and abs(CountOfPosition) < MaxPositionsAllowed THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.1

SET TARGET %PROFIT 2.0

@VinzentVega

Always use the ‘Insert PRT Code’ button when putting code in your posts to make it easier for others to read and try not to mix/use different languages.

Thanks 🙂

Hi,

All of codes above don’t work for me. The message is : “do you want to restart the backtest in tick by tick mode or without”

Anyone has an idea ?

Thanks in advance.

Hello

I have trust some modification SL and TP

the code :

// Definition of code parameters

DEFPARAM CumulateOrders = true // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

MaxPositionsAllowed = 100

//Money Management NAS

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = 1

ONCE factor = 60 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 200 // IG first tier margin limit

ONCE maxpositionsize = 2000 // IG tier 2 margin limit

ONCE minpositionsize = 1 // enter minimum position allowed

IF StrategyProfit <> StrategyProfit[1] THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

Ctime = time >=143000 and time <210000

TIMEFRAME(18 minutes)

Period= 155

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

ST1 = SAR[.005,.005,.02]

c1a = (close > ST1)

c2a = (close < ST1)

TIMEFRAME(6 minutes)

Periodb= 29

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c3 = HULLb > HULLb[1]

c4 = HULLb < HULLb[1]

ST2 = SAR[.005,.005,.02]

c3a = (close > ST2)

c4a = (close < ST2)

TIMEFRAME(default)

Periodc= 4

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c5 = HULLc > HULLc[1] and HULLc[1] < HULLc[2]

c6 = HULLc < HULLc[1] and HULLc[1] > HULLc[2]

ST3 = SAR[.01,.01,.005]

c5a = (close > ST3)

c6a = (close < ST3)

// Conditions to enter long positions

IF not longonmarket and Ctime and c1 and c1a AND C3 and c3a AND C5 and c5a THEN

BUY positionsize CONTRACT AT MARKET

SET STOP pLOSS 15

SET TARGET pPROFIT 55

elsif longonmarket and Ctime and c1 and c1a AND C3 and c3a AND C5 and c5a and abs(CountOfPosition) < MaxPositionsAllowed THEN

if positionperf(0)*100>0 then

BUY positionsize CONTRACT AT MARKET

SET STOP pLOSS 282

SET TARGET pPROFIT 322

endif

endif

// Conditions to enter short positions

IF not shortonmarket and Ctime and c2 and c2a AND C4 and c4a AND C6 and c6a THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP pLOSS 68

SET TARGET pPROFIT 21

elsif shortonmarket and Ctime and c2 and c2a AND C4 and c4a AND C6 and c6a and abs(CountOfPosition) < MaxPositionsAllowed THEN

if positionperf(0)*100>0 then

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP pLOSS 159

SET TARGET pPROFIT 411

endif

endif

//%trailing stop function

trailingstop = 1

if trailingstop =1 then

once trailingPercent = 0.38

once stepPercent = 0.006

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailingstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

endif