Does anyone know of any reason why one shouldn’t trade with this enabled?

Maybe the reason is, that the profit/equity curve for a longer period is not better than without cumulation. Other reason could be a higher DD,but I can´check it, because my longest period in 5m TF is only 15 month.

Does anyone know of any reason why one shouldn’t trade with this enabled?

Would be scary if one morning you woke up and the System had accumulated 20 trades (position size is 20) and you were close to or on a margin call??

Thank you VinzentVega and GraHal for your feedback. Whilst the extensive parameters required to generate a signal mean that there don’t appear to be many triggered, the point of waking up to 20 positions on at once remains a reality.

I found this post by Vonasi which I shall incorporate into the latest version to negate the risk and set a max position allowed;

https://www.prorealcode.com/topic/using-true-cumulating-positions/#post-97661

Thanks again everyone, much appreciated.

I’m recently new to this thread and have read over all the content and quite impressed on what has been put together in this strategy. I ran a few versions (as below) on my IG demo account and am pleased with the results so far, 6 wins and 2 losses. The two losses were also quite minimal especially in comparison to the gains made on the winning trades. I wanted to ask you all of which charts each of these should be getting loaded into. Have I loaded these to the correct charts?

DAX MoD V2.2a Loaded On 5 Min Germany 30 Cash (5 EURO) i.e. not the futures.

DOW MoD V4.7 Loaded On 5 Min DJI Wall Street Cash ($10) DOW Main

DJ MoD V4.7a Loaded On 5 Min DJI Wall Street Cash ($10) DOW Main

I noticed there is also a NAS Version of NAS MoD V3. Is this to be loaded onto the USTech 100 ($1) NASDAQ Futures?

Hello, do you have the same thing as me?

@pat95162

English only in this topic please!

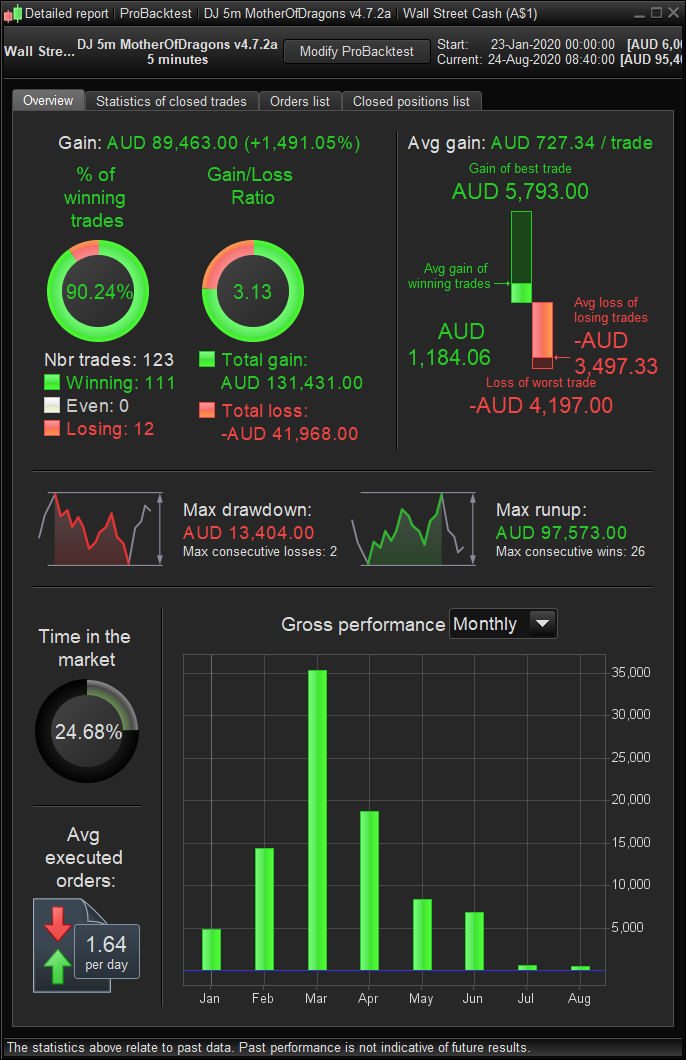

No, I have had mine on Wall Street Cash A$1 with these results. I have been quite impressed. This backtest was done with 10 x $1 contracts and 1 pip spread but the number of contracts is up to your own risk plan/management.

I have been testing these MoD algos with a few colleagues, with some other commercial algorithms we had headaches regarding time zone settings needing to be set in a particular country/time zone or they would not work. The procedure when loading could not use the individual exchange time zones but we needed to change the time zone for PRT completely whilst loading the algorithm.

When using the DAX V2.2a, DJI V4.7a and NAS V3 algorithms, which time zone settings are required?

@nonetheless @dowjones Am tagging you guys as you had posted the versions of the strategy that I am using.

DAX V2.2a, DJI V4.7a and NAS V3 algorithms, which time zone settings are required?

DAX V2.2a = UTC + 2

DJI V4.7.2a = UTC + 8

I didn’t use NAS, so I’m not sure…

Hi all,

Iv’e tried to use the Mother of Dragons for setting up a system for Brent. Im wondering if anyone else have a system running that isn’t stopped on a regular basis?

The error message is:

“The trading system was stopped due to a division by zero during the evaluation of the last candlestick. You can add protections to your code to prevent divisions by zero then backtest the system to check the correction.”

Found a old post about this regarding one or two value RSI and ghost bars but can’t seem to figure out what would cause it since the RSI is above

After a lot of trial and error im not 100% who to credit for the code and there for the header misses correct credits. Sorry for that but a lot of thanks for the work everybody put in to this and thanks for sharing!

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 10000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize = 1

ENDIF

//code re-invest

Capital = 1000 // initial capital

Equity = Capital + StrategyProfit

if MM = 1 then

positionsize = Max(1, Equity * (1/Capital))

positionsize = Round(positionsize*100)

positionsize = positionsize/100

// change from "1" to "position" in buy/sell conditions to use re-invest

//********************

ENDIF

//code quit strategy

maxequity = max(equity,maxequity)

DrawdownNeededToQuit = 20 // percent drawdown from max equity to stop strategy

if equity < maxequity * (1 - (DrawdownNeededToQuit/100)) then

quit

endif

// Time management

Ctime = not (time >= 205959 or time < 070000)

// Friday 22:00 Close ALL operations.

IF DayOfWeek = 5 AND time = 220000 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

// Settings

//Timeframe 2h

//Period weightedaverage

Q1 = 44 // 1-600

//Supertrend

q2 = 6 // 1 - 10

q3 = 6 // 1- 10

// MA average

q4 = 7 // 1- 100

q5 = 4 // 0-6

// RSI

q6 = 20

q7 = 10

q8 = 6

q9 = 2

// 30 min

// Average

q10 = 2 // 1- 10

q11 = 5 // 1- 10

// 15 min

// Average

q12 = 3 // 1- 10

q13 = 4 // 1- 10

// Periodc

q14 = 42

// 10 min

// supertrend

q15 = 2 //na

q16 = 7 // na

// 5 min

//RSI

q17 = 8

q18 = 3

q19 = 12

q20 = 11

//ma average

q21 = 17

q22 = 5

//Periodb

q23 = 17

//Long SL

q24 = 7

//Long TP

q25 = 9

//Short SL

q26 = 7

//Short TP

q27 = 9

TIMEFRAME(2 hours,updateonclose)

Period= Q1

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[q2,q3]

c3 = (close > indicator1)

c4 = (close < indicator1)

ma = average[q4,q5](close)

c11 = ma > ma[1]

c12 = ma < ma[1]

//Stochastic RSI | indicator

lengthRSI = q6 //RSI period

lengthStoch = q7 //Stochastic period

smoothK = q8 //Smooth signal of stochastic RSI

smoothD = q9 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c13 = K>D

c14 = K<D

TIMEFRAME(30 minutes,updateonclose)

indicator5 = Average[q10](typicalPrice)

indicator6 = Average[q11](typicalPrice)

c15 = (indicator5 > indicator6)

c16 = (indicator5 < indicator6)

TIMEFRAME(15 minutes,updateonclose)

indicator2 = Average[q12](typicalPrice)

indicator3 = Average[q13](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

Periodc= q14

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(10 minutes)

indicator1a = SuperTrend[q15,q16]

c19 = (close > indicator1a)

c20 = (close < indicator1a)

TIMEFRAME(5 minutes)

//Stochastic RSI | indicator

lengthRSIa = q17 //RSI period

lengthStocha = q18 //Stochastic period

smoothKa = q19 //Smooth signal of stochastic RSI

smoothDa = q20 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ma3 = average[q21,q22](close)

c21 = ma3 > ma3[1]

c22 = ma3 < ma3[1]

Periodb= q23

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

//Long target and stoploss

LSL = Q24 /10

LTP = Q25 /10

// Conditions to enter long positions

IF Ctime and dhigh(0)-high<250 and c1 AND C3 AND C5 and c7 and c9 and c11 and c13 and c15 and c19 and c21 and c23 THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS LSL

SET TARGET %PROFIT LTP

ENDIF

//Short target and stoploss

SSL = Q26/10

STP = Q27/10

// Conditions to enter short positions

IF Ctime and low-dlow(0)<700 and c2 AND C4 AND C6 and c8 and c10 and c12 and c14 and c16 and c20 and c22 and c24 THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS SSL

SET TARGET %PROFIT STP

ENDIF

//================== exit in profit

if longonmarket and C6 and c8 and close>positionprice then

sell at market

endif

If shortonmarket and C5 and c7 and close<positionprice then

exitshort at market

endif

//==============exit at loss

if longonmarket AND c2 and c6 and close<positionprice then

sell at market

endif

If shortonmarket and c1 and c5 and close>positionprice then

exitshort at market

endif

//%trailing stop function

trailingPercent = .26

stepPercent = .014

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailingstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

IF longonmarket and barindex-tradeindex>1800 and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex>610 and close>positionprice then

exitshort at market

endif

//=============================================

if longonmarket and abs(open-close)<1 and high[1]>high and close>positionprice and high-close>10then

sell at market

endif

if shortonmarket and abs(open-close)<1 and low[1]>low and close-low>13 and close<positionprice then

exitshort at market

endif

//===================================

myrsiM5=rsi[14](close)

//

if myrsiM5<30 and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsiM5>70 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

once openStrongLong = 0

once openStrongShort = 0

if (time <= 223000 - USDLS and time >= 050000 - USDLS) then

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 40

once tradeMin = 1500

IF (time >= 223500 - USDLS) AND (time <= 223500 + tradeMin - USDLS) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

once bollperiod = 20

once bollMAType = 1

once s = 2

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

once trendPeriod = 70

once trendPeriodResume = 30

once trendGap = 3

once trendResumeGap = 6

if not onmarket then

fullySupported = 0

fullyResisteded = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisteded = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisteded = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisteded = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//

//Started real wrong direction

once strongTrend = 60

once strongPeriod = 8

once strongTrendGap = 2

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod - strongTrendGap then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod - strongTrendGap then

sell at market

ENDIF

anyone else have a system running that isn’t stopped on a regular basis

I have run both MoD DAX and DJI for many months, no such issue for me.

For your issue, in my experience, to debug the issue, better to take note when the issue reported, so you can build indicator or GRAPH the suspected division method to check. The problem is Probacktest doesn’t report issue with zero division, I did a dummy test before to purposely divide by zero and backtest still can complete successfully.

I have run both MoD DAX and DJI for many months, no such issue for me.

Yes it works great for with all indexes but can’t get it to run on Brent Crude oil. Tried several setups and always get the zero division error message or the suggestion of preloading bars (can’t remember the error message on top of my head)

I worked with a strategy on Brent but realized I had to scrap it because of constant zero division error. You can forget about oil for automated trading.

Out of curiosity… what are the values you use for you 5M RSI calculations?

Out of curiosity… what are the values you use for you 5M RSI calculations?

This test (have done a few) 8, 3, 12, 11

I worked with a strategy on Brent but realized I had to scrap it because of constant zero division error. You can forget about oil for automated trading.

Thanks for confirming that i’m not mad