Ciao Francesco, here’s a second version if you wouldn’t mind backtesting on 200k. MM is disabled but the DrawdownNeededToQuit might still be operative … not sure.

I added another layer of filters at the 15m level. It performs better than v1 over 100k — higher profit from fewer trades — so curious to know if it’s still just fit it to that data set.

Dita incrociate…

nonetheless – could you post the code so that we don’t have to download the ITF file please?

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

Capital = 10000

MinSize = 1 //The minimum position size allowed for the instrument.

MM1stType = 0 //Starting type of moneymanagement. Set to 0 for level stakes. Set to 1 for increasing stake size as profits increase and decreasing stake size as profits decrease. Set to 2 for increasing stake size as profits increase with stake size never being decreased.

MM2ndType = 0 //Type of money management to switch to after TradesQtyForSwitch number of trades and ProfitNeededForSwitch profit has occurred

TradesQtyForSwitch = 15 //Quantity of trades required before switching to second money management choice.

ProfitNeededForSwitch = 2 //% profit needed before allowing a money management type change to MM2ndType.

DrawdownNeededToSwitch = 8 //% draw down from max equity needed before money management type is changed back to MM1stType.

DrawdownNeededToQuit = 25 //% draw down from max equity needed to stop strategy

Once MoneyManagement = MM1stType

Equity = Capital + StrategyProfit

maxequity = max(equity,maxequity)

if equity < maxequity * (1 - (DrawdownNeededToSwitch/100)) then

enoughtrades = 0

tradecount = 0

moneymanagement = MM1stType

endif

if equity < maxequity * (1 - (DrawdownNeededToQuit/100)) then

quit

endif

if not EnoughTrades then

if abs(countofposition) > abs(countofposition[1]) then

tradecount = tradecount + 1

endif

if tradecount > TradesQtyForSwitch and maxequity >= Capital * (1 + (ProfitNeededForSwitch/100)) then

EnoughTrades = 1

MoneyManagement = MM2ndType

endif

endif

IF MoneyManagement = 1 THEN

PositionSize = Max(MinSize, Equity * (MinSize/Capital))

ENDIF

IF MoneyManagement = 2 THEN

PositionSize = Max(LastSize, Equity * (MinSize/Capital))

LastSize = PositionSize

ENDIF

IF MoneyManagement <> 1 and MoneyManagement <> 2 THEN

PositionSize = MinSize

ENDIF

PositionSize = Round(PositionSize*100)

PositionSize = PositionSize/100

// Size of POSITIONS

PositionSizeLong = 1 * positionsize

PositionSizeShort = 1 * positionsize

TIMEFRAME(120 minutes)

Period= 520

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[5,21]

c3 = (close > indicator1)

c4 = (close < indicator1)

TIMEFRAME(15 minutes)

indicator2 = Average[6](typicalPrice)

indicator3 = Average[11](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

Periodc= 17

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(5 minutes)

Periodb= 22

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

// Conditions to enter long positions

IF c1 AND C3 AND C5 and c7 and c9 THEN

BUY PositionSizeLong CONTRACT AT MARKET

SET STOP %LOSS 2.1

SET TARGET %PROFIT 1

ENDIF

// Conditions to enter short positions

IF c2 AND C4 AND C6 and c8 and c10 THEN

SELLSHORT PositionSizeShort CONTRACT AT MARKET

SET STOP %LOSS 1.2

SET TARGET %PROFIT 1

ENDIF

//trailing stop function

trailingstart = 81 //trailing will start @trailinstart points profit

trailingstep = 3 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

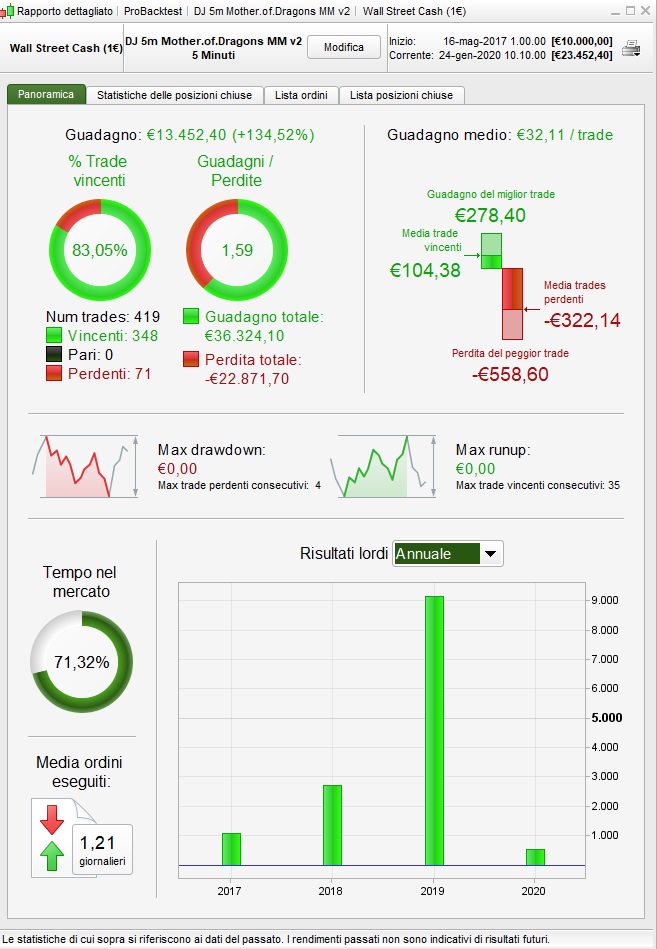

Thanks Francesco … sadly not any better than the first one. Only really works for 2019.

May need to rethink this. We all know how it ended for the mother of dragons.

Hope the next will not be Oberyn trading strategy 😀

May need to rethink this

Least it wouldn’t have blown the Account in the 1st 100k bars (as many Systems do for OOS periods).

Maybe a Filter to prevent trading when Price is ranging and also in a downtrend.

If you look at the equity curve … in 2017 when price was rising (from Sep 17 to Jan 18) your System made money then lost it when price was in a downtrend (Feb 18 to May 18) then hovered around zero when price was ranging from May 18 until 2019 when it got going again.

It is worth trying a few tweaks and then if Franseco tests again over 200k bars.

But really you need tweak then optimise else you not know if the tweak worked. How about trying it on 100k x 10 min TF as then back to June 2017 should be included??

Just a few thoughts anyway.

TBH, I’m inclined to give it a rest until we get v11. 100k just isn’t enough data to work with unless you’re using +1h TFs.

I changed line

61

74

131

Add a stop from the line

113

I would do well a multi position if the position wins.

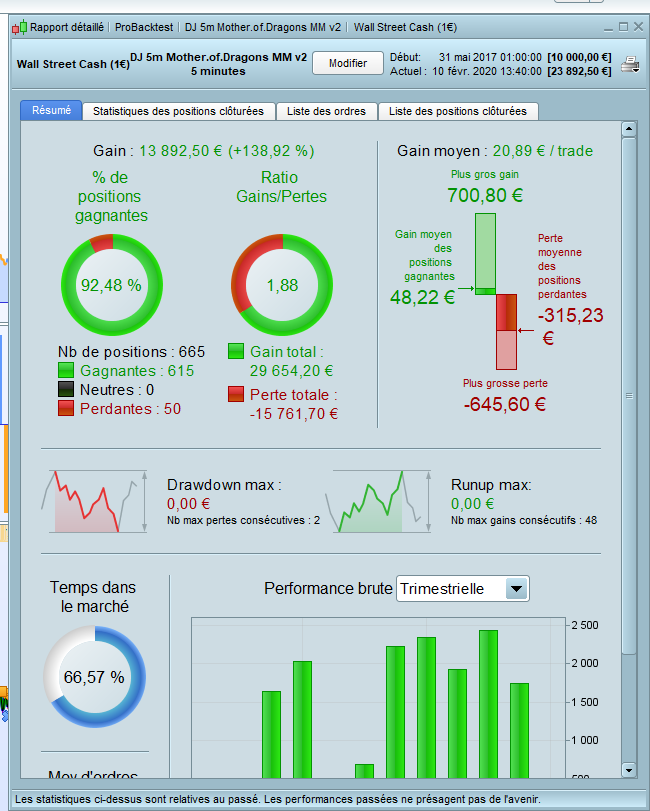

Hey Fifi, a few tweaks and suddenly it looks so much better – thanks for that!

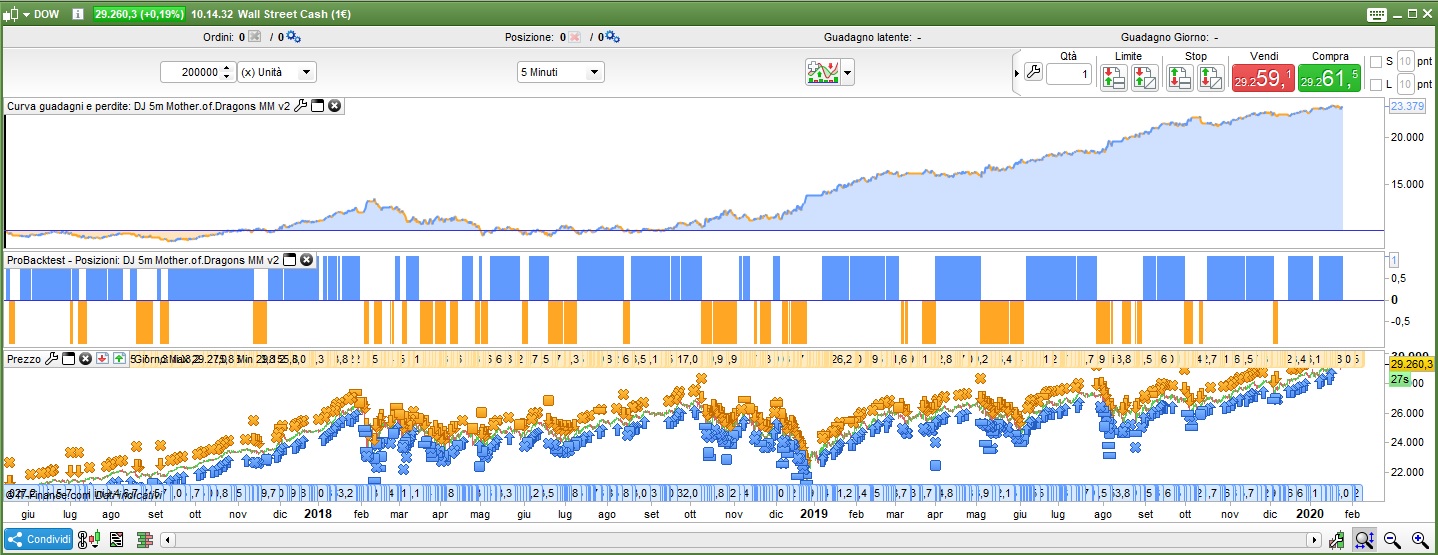

Your backtest is 200k, yes? How does the curve look for 2017, 2018? The previous version only really came alive in 2019.

That is a much better line, steady increase over almost the whole period. I tried to break it into separate long and short but the result is worse; your version works better as one code going both ways. A couple of big losses in Jan/Feb 2020 but over the long term looks like it could work – génial!

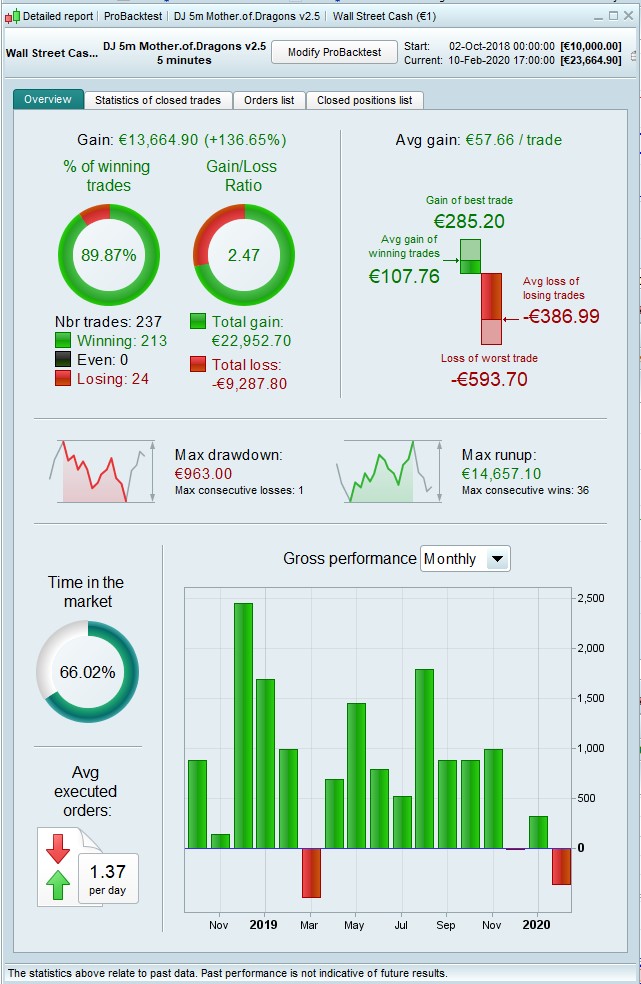

This is another version I had been working on, with a couple of extra filters in the 2h TF to help confirm the primary trend. What do you think? My guess is that yours is probably more stable…

here’s the code:

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

Capital = 10000

MinSize = 1 //The minimum position size allowed for the instrument.

MM1stType = 0 //Starting type of moneymanagement. Set to 0 for level stakes. Set to 1 for increasing stake size as profits increase and decreasing stake size as profits decrease. Set to 2 for increasing stake size as profits increase with stake size never being decreased.

MM2ndType = 0 //Type of money management to switch to after TradesQtyForSwitch number of trades and ProfitNeededForSwitch profit has occurred

TradesQtyForSwitch = 8 //Quantity of trades required before switching to second money management choice.

ProfitNeededForSwitch = 2 //% profit needed before allowing a money management type change to MM2ndType.

DrawdownNeededToSwitch = 8 //% draw down from max equity needed before money management type is changed back to MM1stType.

DrawdownNeededToQuit = 25 //% draw down from max equity needed to stop strategy

Once MoneyManagement = MM1stType

Equity = Capital + StrategyProfit

maxequity = max(equity,maxequity)

if equity < maxequity * (1 - (DrawdownNeededToSwitch/100)) then

enoughtrades = 0

tradecount = 0

moneymanagement = MM1stType

endif

if equity < maxequity * (1 - (DrawdownNeededToQuit/100)) then

quit

endif

if not EnoughTrades then

if abs(countofposition) > abs(countofposition[1]) then

tradecount = tradecount + 1

endif

if tradecount > TradesQtyForSwitch and maxequity >= Capital * (1 + (ProfitNeededForSwitch/100)) then

EnoughTrades = 1

MoneyManagement = MM2ndType

endif

endif

IF MoneyManagement = 1 THEN

PositionSize = Max(MinSize, Equity * (MinSize/Capital))

ENDIF

IF MoneyManagement = 2 THEN

PositionSize = Max(LastSize, Equity * (MinSize/Capital))

LastSize = PositionSize

ENDIF

IF MoneyManagement <> 1 and MoneyManagement <> 2 THEN

PositionSize = MinSize

ENDIF

PositionSize = Round(PositionSize*100)

PositionSize = PositionSize/100

// Size of POSITIONS

PositionSizeLong = 1 * positionsize

PositionSizeShort = 1 * positionsize

TIMEFRAME(120 minutes)

Period= 480

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[5,21]

c3 = (close > indicator1)

c4 = (close < indicator1)

indicator4 = CALL "Moving Average Slope"[75,1](close)

c11 = (indicator4 > 0)

c12 = (indicator4 < 0)

Sinewave, ignored, ignored, ignored = CALL "Ehlers Even Better Sinewave"[100,.8, -.8]

c13 = (Sinewave > -8)

c14 = (Sinewave < .8)

TIMEFRAME(15 minutes)

indicator2 = Average[6](typicalPrice)

indicator3 = Average[11](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

Periodc= 17

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(5 minutes)

Periodb= 22

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

// Conditions to enter long positions

IF c1 AND C3 AND C5 and c7 and c9 and c11 and c13 THEN

BUY PositionSizeLong CONTRACT AT MARKET

SET STOP %LOSS 1.9

SET TARGET %PROFIT 1

ENDIF

// Conditions to enter short positions

IF c2 AND C4 AND C6 and c8 and c10 and c12 and c14 THEN

SELLSHORT PositionSizeShort CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 1

ENDIF

//trailing stop function

trailingstart = 81 //trailing will start @trailinstart points profit

trailingstep = 3 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

I tried to break it into separate long and short but the result is worse; your version works better as one code going both ways

For me that would start ringing an alarm bell. If an entry condition and exit condition are good then they should be good whether you have opposite direction trades in the strategy or not.

There wasn’t much in it – less than 10% difference, but better as one code doing both long and short. (I’m talking about Fifi’s version, posted above as v2_MOD – my original worked better as separate long and short).