The losing trade I saw directly that it was dead …

I stopped the strategy to optimize it. It is imperative that the strategy cuts at 11:00 p.m. – midnight. For example, last night a position was opened on the DAX to play the performance of WALL STREET. From midnight profit taking and correction …The trade ends up losing at the exit.

Breakeven and stoploss must be adapted according to the position period.

– Between 12:15 am and 7:00 am

– Between 08:00 and 12:00.

– Between 12:00 p.m. and 3:30 p.m.

– Between 3.30 p.m. and 7 p.m.

-Between 7:00 p.m. and 11:45 p.m.

EXIT 11:45 PM

I work on the strategy in this direction

Florian

Please “none”…

A bullish versión, and bearish versión to dax.

@Fran55

Why don’t you try to make your own version? just like Florian did. There are all the necessary materials on the website to improve your coding skills 😉

Why i dont programmer man.

@nonetheless

for the moment your strategy is very perfect and seems to me really robust for different markets, greetings ! well done

imperative that the strategy cuts at 11:00 p.m

Hi Florian, I came to the same conclusion. But are you running DAX v1? v2 is much improved, including time limit 00 – 23

Hi,

First of all. Thank you

@nonetheless for sharing, and everyoneelse helping out.

Anyone testing this live right now? Did you get any positions yesterday or today on dax – v.2 and dow – v.4? Just want to know if i did anything wrong. It works on the backtest..

Hi

Linus, in the past couple of days (Apr 6, 7) i’ve had 7 trades on the DOW and 4 on the DAX, all wins.

Thanks for the info @

nonetheless , Any clue why it does not take a poss?

(Just do doublecheck, was the last trade on dow : 23:15 6 and closed 02:40 7 april Or anyone more then that?

Elso there is the code:

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

//Money Management DOW

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = .4

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE factor2 = 20 // tier 2 factor

ONCE margin = (close*.05) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor2*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor2*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

TIMEFRAME(2 hours,updateonclose)

Periodh= 515

inner = 2*weightedaverage[round( Periodh/2)](typicalprice)-weightedaverage[Periodh](typicalprice)

HULL = weightedaverage[round(sqrt(Periodh))](inner)

cnd1 = HULL > HULL[1]

cnd2 = HULL < HULL[1]

indicator1 = SuperTrend[6,10]

cnd3 = (close > indicator1)

cnd4 = (close < indicator1)

indicator4 = CALL "Moving Average Slope"[55,3](close)

cnd5 = (indicator4 > 0)

cnd6 = (indicator4 < 0)

//PRC_Stochastic RSI | indicator

lengthRSI = 16 //RSI period

lengthStoch = 10 //Stochastic period

smoothK = 11 //Smooth signal of stochastic RSI

smoothD = 3 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

Ka = average[smoothK](stochrsi)*100

Da = average[smoothD](Ka)

cnd7 = Ka>Da

cnd8 = Ka<Da

TIMEFRAME(15 minutes,updateonclose)

indicator2 = Average[4](typicalPrice)

indicator3 = Average[8](typicalPrice)

cnd9 = (indicator2 > indicator3)

cnd10 = (indicator2 < indicator3)

Period2h= 23

inner2 = 2*weightedaverage[round( Period2h/2)](typicalprice)-weightedaverage[Period2h](typicalprice)

HULL2 = weightedaverage[round(sqrt(Period2h))](inner2)

cnd11 = HULL2 > HULL2[1]

cnd12 = HULL2 < HULL2[1]

indicator5 = CALL "Moving Average Slope"[20,2](close)

cnd13 = (indicator5 > 0)

cnd14 = (indicator5 < 0)

TIMEFRAME(5 minutes)

Period3= 15

inner3 = 2*weightedaverage[round( Period3/2)](typicalprice)-weightedaverage[Period3](typicalprice)

HULL3 = weightedaverage[round(sqrt(Period3))](inner3)

cnd15 = HULL3 > HULL3[1]and HULL3[1]<HULL3[2]

cnd16 = HULL3 < HULL3[1]and HULL3[1]>HULL3[2]

// Conditions to enter long positions

IF cnd1 AND cnd3 AND cnd5 and cnd7 and cnd9 and cnd11 and cnd13 and cnd15 THEN

BUY positionsize CONTRACT AT MARKET

ENDIF

// Conditions to enter short positions

IF cnd2 AND cnd4 AND cnd6 and cnd8 and cnd10 and cnd12 and cnd14 and cnd16 THEN

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

SET STOP %LOSS 2.2

SET TARGET %PROFIT 2.1

//================== exit in profit

if longonmarket and cnd16 and cnd10 and close>positionprice then

sell at market

endif

If shortonmarket and cnd15 and cnd9 and close<positionprice then

exitshort at market

endif

//==============exit at loss

if longonmarket AND cnd2 and cnd16 and close<positionprice then

sell at market

endif

If shortonmarket and cnd1 and cnd15 and close>positionprice then

exitshort at market

endif

//trailing stop function

trailingPercent = .26

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailinstart points profit

trailingstep = 3 //trailing step to move the "stoploss"

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

hello Nonetheless, which version you work with please?

@

Linus, I’m running a slightly different version so I didn’t get that trade. Note, if you’re going to use the MM you have to change the details in lines 13,14,15,16. See the market info tab to find the max position for each tier and the leverage (convert the % to a decimal).

@

bertrandpinoy attached is the latest version, but changes are fairly minor.

As always, thank you

@nonetheless !

Did you apply theses minor changes to the DAX et SP versions ?

@

ArnoldB no, they’re all built slightly differently so no changes to DAX v2 or SP v2

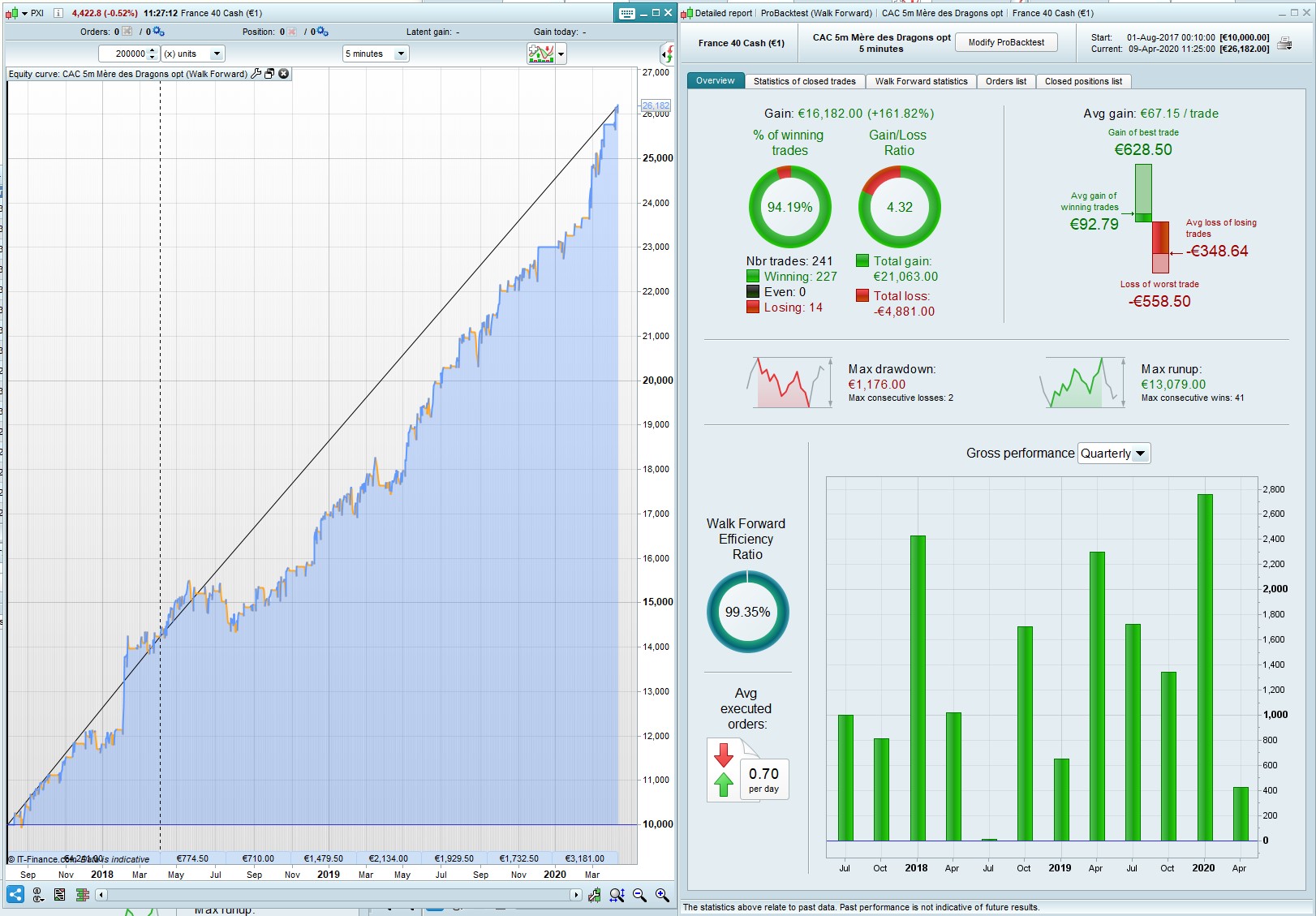

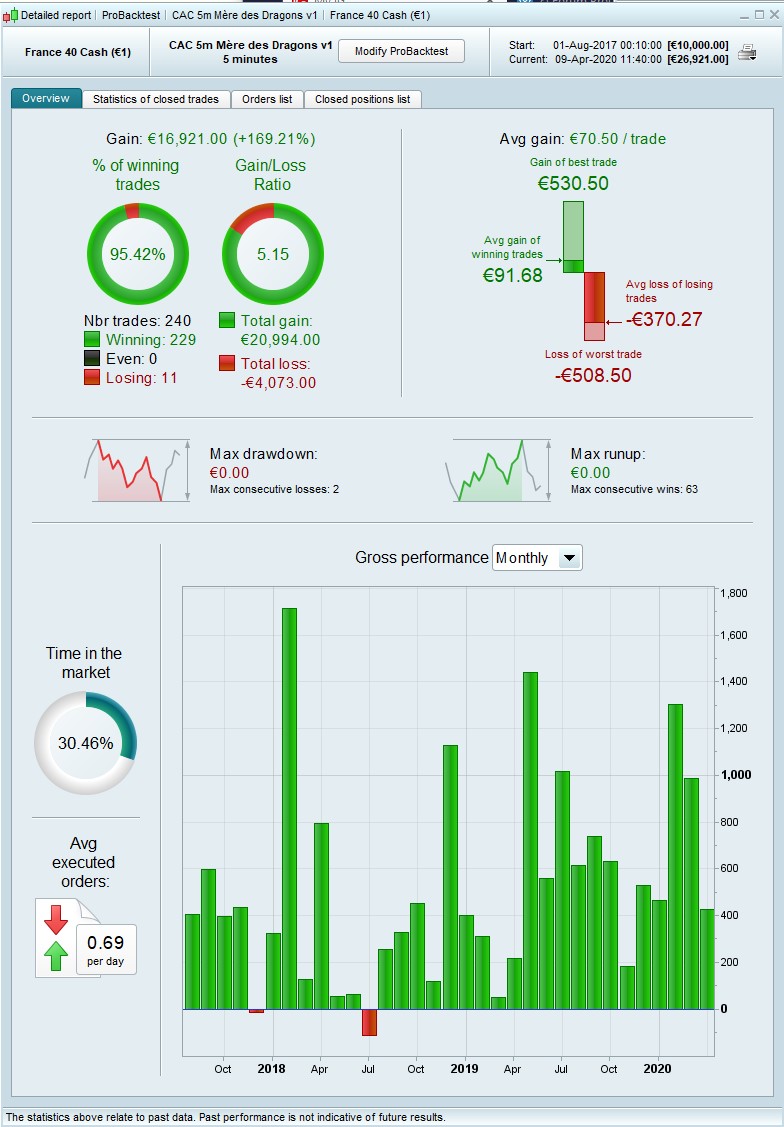

Tant de français ici … but no one wants to code for the CAC40 ? (could it be something in the name? In any European language ‘CAC’ sounds … well, uninspiring to say the least).

Never mind. Here’s an offer to redress the balance.