@Paul … comment out Line 144. Also then … 1 less endif should be needed?

My ‘sweating over it’ time may be a benefit to others as I tried just about every conceivable thing possible to get mine to work. Then – when I got it working – I went back over some things I tried to see what difference they should have made! 🙂

Let us know if it works?

Also you need the initialisation below to be inserted in your code at Line 10 …

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

@Paul I got your code to run after making the changes above, but Valuex and ValueY are not changing.

More sweating now! 🙂

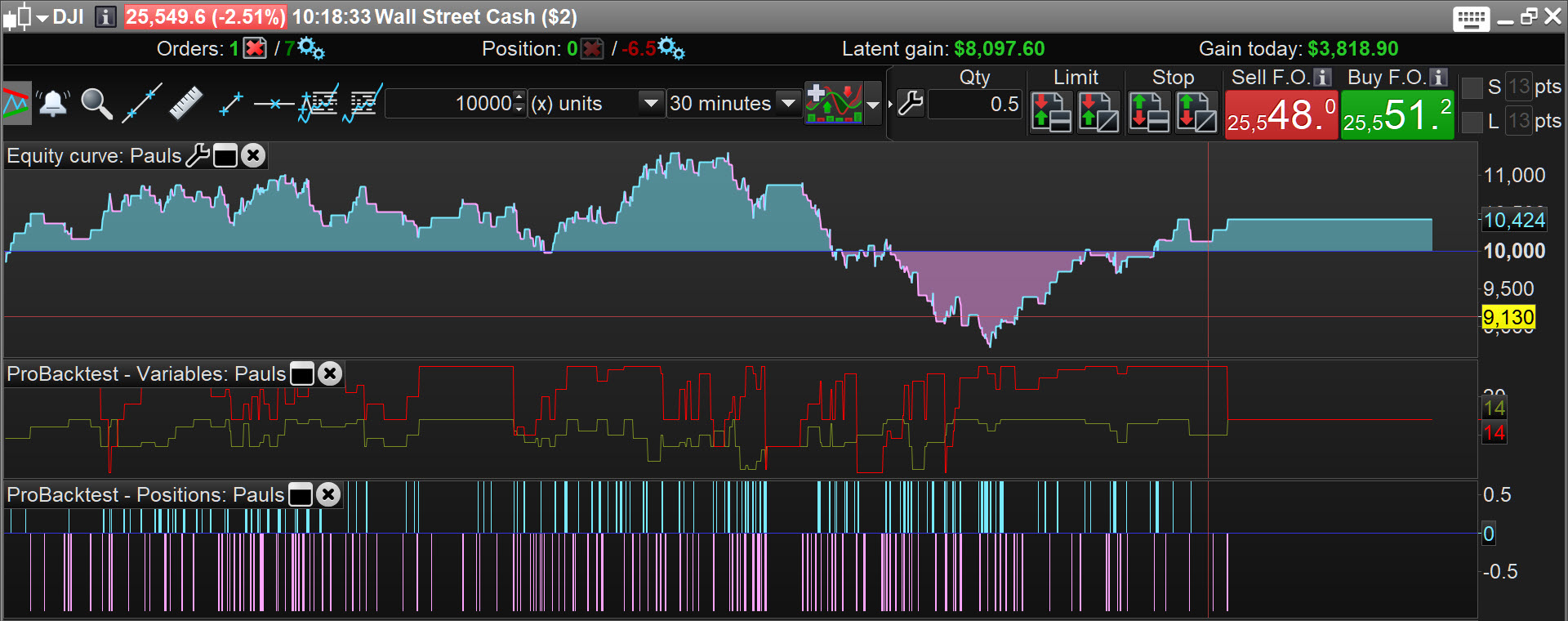

Success … see attached!

I looked at my working System and the only way I got mine to fully spark into life (with ValueX and ValueY changing) … was to NOT include the code below … so there must be something wrong with below or the concept of below does not work??

I guess JuanJ will have to help us with below?

HeuristicsCycleLimit = 2

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

Aha … I just looked at my other fully working working System including the above code … but we do NOT need either lines of code below …

So that’s saved JuanJ a bit more time! 🙂

If HeuristicsAlgo1 = 1 Then

If HeuristicsAlgo2 = 1 Then

EDIT / PS

Comparing results of both my 2 fully functional Systems and Paul’s System with and without the HeuristicsCycle Code above … the results are the same both with and without!

Maybe there could be instances where the HeuristicsCycle Code makes a difference?

Thoughts:

JuanJ noted cross-errors when he tried 2 x Algos together (some time ago) so he kindly provided the HeuristicsCycle Code as a solution.

These cross-errors may have been due to the cross-use (between the 2 x Algos) of certain settings due to the missing ‘2’ from certain settings (of Algo2) which I highlighted and corrected in an earlier post.

we do NOT need either lines of code below …

Away from the screen my brain cleared! 🙂

Without the lines of code below, we have nothing that is controlling / defining Algo1 and Algo2 and so the HeuristicsCycle code is not doing anything? (This is why both sets of results are the same!).

So I am now back to my earlier assertion that HeuristicsCycle code is not working for some reason?

If HeuristicsAlgo1 = 1 Then

If HeuristicsAlgo2 = 1 Then

Francesco did it before ….. he had two different results, but without code we don’t know how he did it.

he had two different results, but without code we don’t know how he did it.

Francesco results were before (without JuanJ code) and after (with JunanJ code).

I have my Systems (and Paul’s) working – with the JuanJ Algo1 and Algo2 – but seemingly not using the code below.

HeuristicsCycleLimit = 2

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

If you remove this part of code, I seem to have understood that the results will not change you …. so there is something else different ….

Either …

- The Cycle code above is not working and therefore achieving no change in the results?

This scenario means that Algo1 and Algo2 are both working at the same time (on the same bar).

OR

2. The Cycle code above is working as designed to do, but the results are the same as without the Cycle code above.

This scenario means that Algo1 and Algo2 are working separately every 2 Cycles (on different bars).

Item 2. is why I think that the Cycle code is not working as the results would not be identical??

Paul

PaulParticipant

Master

A lot of idea’s but i’am stuck at the moment.

@GraHal, I tried many combinations, but to result. Also tried fifi’s idea.

If someone got it to a working version, then please post the whole code.

If someone got it to a working version, then please post the whole code.

Below is your code working and the results attached … you can see Valuex and ValueY as variables changing … under the equity curve.

defparam cumulateorders = false

defparam preloadbars = 10000

defparam flatbefore = 080000

defparam flatafter = 220000

//period1=7

//period2=14

HeuristicsCycleLimit = 2

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

//

//If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

StartingValue = 6

ResetPeriod = 3 //Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 7 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MinValue = 1 //Minimum allowed value

MaxValue = 12 //Maximum allowed value

If monthinit = 1 or monthinit = 3 or monthinit = 5 or monthinit = 7 or monthinit = 8 or monthinit = 10 or monthinit = 12 Then

MonthDays = 31

ElsIf monthinit = 4 or monthinit = 6 or monthinit = 9 or monthinit = 11 Then

MonthDays = 30

ElsIf monthinit = 2 Then

If (yearinit/4 = round(yearinit/4)) or (yearinit/400 = round(yearinit/400)) Then //haha not sure how exactly to do this

MonthDays = 29 //leap year

Else

MonthDays = 28

EndIf

EndIf

If (month = monthinit and day = dayinit + ResetPeriod) or (month = monthinit + 1 and (day + (MonthDays - dayinit)) >= ResetPeriod) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

dayinit = day

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

//ElsIf HeuristicsAlgo2 = 1 Then

//Heuristics Algorithm 2 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize2 = optimize2 + 1

EndIf

StartingValue2 = 16

ResetPeriod2 = 3 //Specify no of months after which to reset optimization

Increment2 = 1

MaxIncrement2 = 7 //Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MinValue2 = 14 //Minimum allowed value

MaxValue2 = 28 //Maximum allowed value

If monthinit2 = 1 or monthinit2 = 3 or monthinit2 = 5 or monthinit2 = 7 or monthinit2 = 8 or monthinit2 = 10 or monthinit2 = 12 Then

MonthDays2 = 31

ElsIf monthinit2 = 4 or monthinit2 = 6 or monthinit2 = 9 or monthinit2 = 11 Then

MonthDays2 = 30

ElsIf monthinit2 = 2 Then

If (yearinit2/4 = round(yearinit2/4)) or (yearinit2/400 = round(yearinit2/400)) Then //haha not sure how exactly to do this

MonthDays2 = 29 //leap year

Else

MonthDays2 = 28

EndIf

EndIf

If (month = monthinit2 and day = dayinit2 + ResetPeriod2) or (month = monthinit2 + 1 and (day + (MonthDays2 - dayinit2)) >= ResetPeriod2) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

dayinit2 = day

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End

//EndIf

c1=average[valuex](close)

c2=average[valuey](close)

//

condbuy =c1 crosses over c2 and rsi[14](close)<70

condsell=c1 crosses under c2 and rsi[14](close)>30

//

if condbuy then

buy at market

endif

if condsell then

sellshort at market

endif

pp=positionperf(0)*100

if pp<-0.125 then

sell at market

exitshort at market

endif

set stop %loss 0.5 // exit sooner on performance criteria above

set target %profit 0.25

graph valuex coloured(121,141,35,255) as "fastperiod1"

graph valuey coloured(255,0,0,255) as "slowperiod"

//endif

//endif

GRAPH HeuristicsAlgo1 coloured(121,141,35,255)

//GRAPH HeuristicsAlgo2 coloured(255,0,0,255)

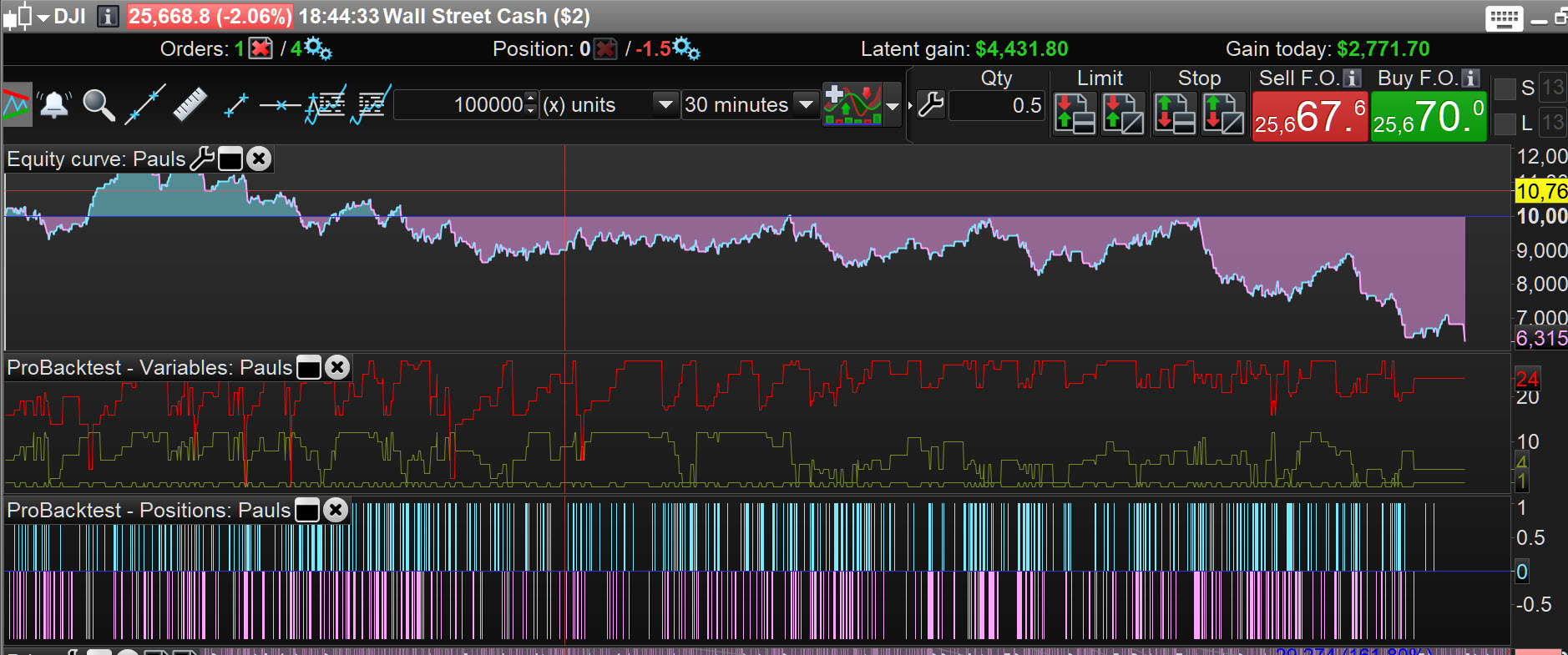

And here is Paul’s code with the HeuristicsCycle all Rem’d out … results on the top equity curve.

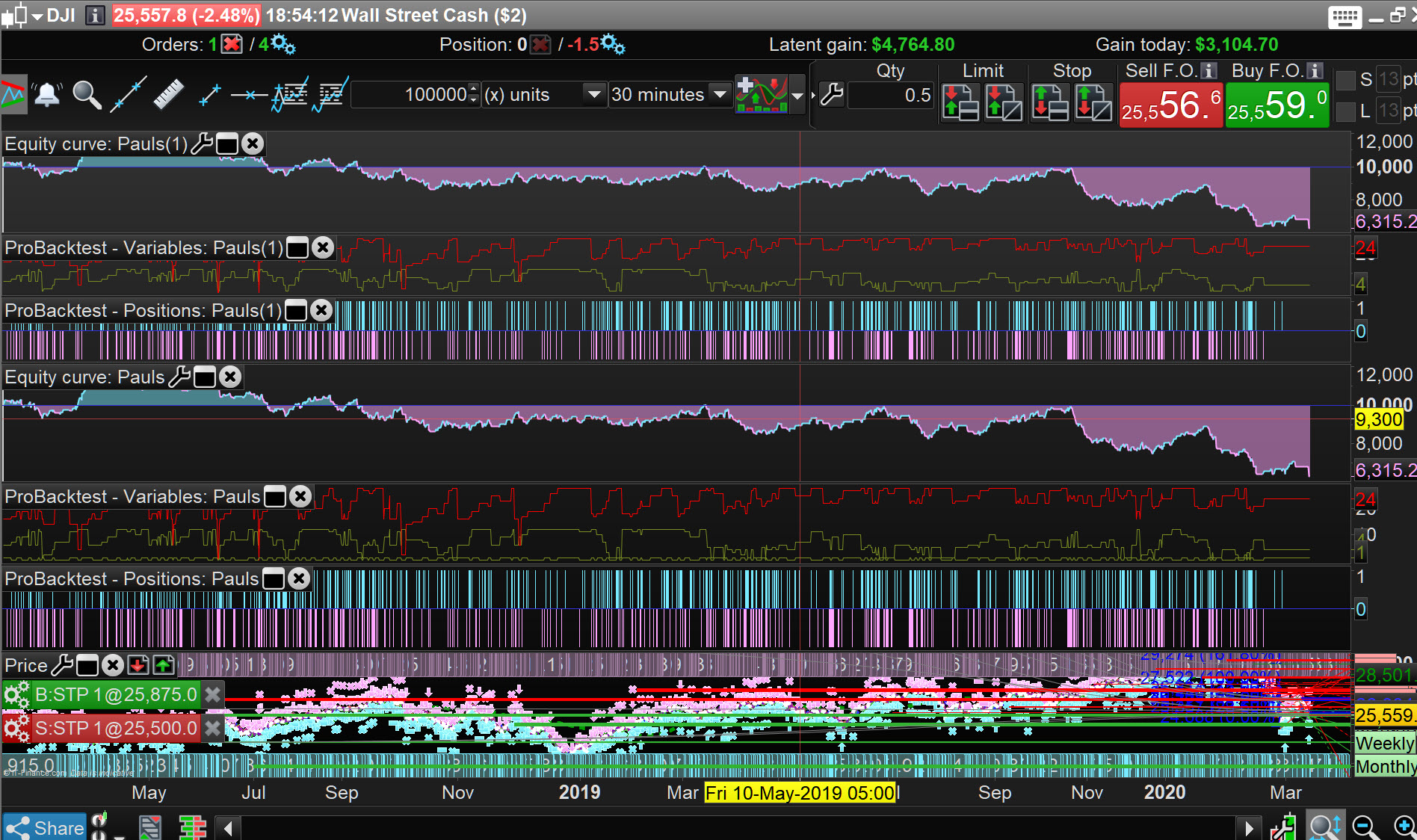

Notice the top equity curve (rem’d out HeuristicsCycle code) results are the same bottom equity curve (included HeuristicsCycle code ). Note: included = opposite of rem’d out.

defparam cumulateorders = false

defparam preloadbars = 10000

defparam flatbefore = 080000

defparam flatafter = 220000

//period1=7

//period2=14

//HeuristicsCycleLimit = 2

//once HeuristicsCycle = 0

//once HeuristicsAlgo1 = 1

//once HeuristicsAlgo2 = 0

//If HeuristicsCycle >= HeuristicsCycleLimit Then

//If HeuristicsAlgo1 = 1 Then

//HeuristicsAlgo2 = 1

//HeuristicsAlgo1 = 0

//ElsIf HeuristicsAlgo2 = 1 Then

//HeuristicsAlgo1 = 1

//HeuristicsAlgo2 = 0

//EndIf

//HeuristicsCycle = 0

//EndIf

////

//If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

StartingValue = 6

ResetPeriod = 3 //Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 7 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MinValue = 1 //Minimum allowed value

MaxValue = 12 //Maximum allowed value

If monthinit = 1 or monthinit = 3 or monthinit = 5 or monthinit = 7 or monthinit = 8 or monthinit = 10 or monthinit = 12 Then

MonthDays = 31

ElsIf monthinit = 4 or monthinit = 6 or monthinit = 9 or monthinit = 11 Then

MonthDays = 30

ElsIf monthinit = 2 Then

If (yearinit/4 = round(yearinit/4)) or (yearinit/400 = round(yearinit/400)) Then //haha not sure how exactly to do this

MonthDays = 29 //leap year

Else

MonthDays = 28

EndIf

EndIf

If (month = monthinit and day = dayinit + ResetPeriod) or (month = monthinit + 1 and (day + (MonthDays - dayinit)) >= ResetPeriod) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

dayinit = day

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

//ElsIf HeuristicsAlgo2 = 1 Then

//Heuristics Algorithm 2 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize2 = optimize2 + 1

EndIf

StartingValue2 = 16

ResetPeriod2 = 3 //Specify no of months after which to reset optimization

Increment2 = 1

MaxIncrement2 = 7 //Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MinValue2 = 14 //Minimum allowed value

MaxValue2 = 28 //Maximum allowed value

If monthinit2 = 1 or monthinit2 = 3 or monthinit2 = 5 or monthinit2 = 7 or monthinit2 = 8 or monthinit2 = 10 or monthinit2 = 12 Then

MonthDays2 = 31

ElsIf monthinit2 = 4 or monthinit2 = 6 or monthinit2 = 9 or monthinit2 = 11 Then

MonthDays2 = 30

ElsIf monthinit2 = 2 Then

If (yearinit2/4 = round(yearinit2/4)) or (yearinit2/400 = round(yearinit2/400)) Then //haha not sure how exactly to do this

MonthDays2 = 29 //leap year

Else

MonthDays2 = 28

EndIf

EndIf

If (month = monthinit2 and day = dayinit2 + ResetPeriod2) or (month = monthinit2 + 1 and (day + (MonthDays2 - dayinit2)) >= ResetPeriod2) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

dayinit2 = day

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End

//EndIf

c1=average[valuex](close)

c2=average[valuey](close)

//

condbuy =c1 crosses over c2 and rsi[14](close)<70

condsell=c1 crosses under c2 and rsi[14](close)>30

//

if condbuy then

buy at market

endif

if condsell then

sellshort at market

endif

pp=positionperf(0)*100

if pp<-0.125 then

sell at market

exitshort at market

endif

set stop %loss 0.5 // exit sooner on performance criteria above

set target %profit 0.25

graph valuex coloured(121,141,35,255) as "fastperiod1"

graph valuey coloured(255,0,0,255) as "slowperiod"

//endif

//endif

//GRAPH HeuristicsAlgo1 coloured(121,141,35,255)

//GRAPH HeuristicsAlgo2 coloured(255,0,0,255)

//endif