Hi Juan I have an inefficiency zone on my daily chart which is from 1855 to 1840 which has been partially filled. Please can you confirm the time frame you are using for the inefficiency zone you are referring to in your technical analysis.

Yes that is the one on Daily, that opened up on 10-Feb.

What does the original version look like?

Previous version is the same. The new version did not change anything in terms of entries or exits, it only affect the way in which it handles the performance curve long term.

In fact if you look at the attached backtest of the new version we could actually have avoided the loss on Monday, if it had run from beginning of the year. The reason for this as explained in a previous post, is that it requires at least 30 trades to generate sufficient data to know what the ‘equity curve’ typically looks like. This means that after the loss on Friday it would have detected we are below 1 sigma from the norm and hence temporarily halt trading on Monday. Which is actually a testament of how the new version (running live for long enough) will help us generate better overall performance going forward.

Good Day Everyone, herewith the latest update and FULL Live Results Disclosure:

It has unfortunately been another bad month for the strategy as we are clearly facing a drawdown. I also just want to take the opportunity to encourage everyone to not give up on the strategy. I want to remind everyone that I am personally invested in this strategy, so I am feeling the pinch alongside everyone facing the drawdown right now and have in fact taken a painfull and disproportionate loss compared to my previous success of the strategy over the past 16 months as I increased my exposure with the release of the previous version just as we entered into this drawdown.

The upside of this is that I remain fully commited to look for ways to improve the strategy. And despite the recent drawdown it is worth noting that the strategy has been running Live and OOS for an entire year and a half now and considering consistent exposure would still be showing decent results. The strategy is in actual fact at a very mature stage and the edge remains entirely valid so I maintain high hopes for future performance and will continute to provide live updates.

I have also just released a new update to the strategy via the Marketplace where I improved the virtual entry algorithm and also added a ‘manual override’ option to temporarily disable the linear regression algorithm for doing faster backtesting. I also added minor safeguards to the stop loss to ensure it stays well defined. The full 200k backtest for the new version is attached.

I will personally be running the new version on my $1000 account starting todat and also decided to scale back on my exposure by setting the position multiplier back to 2.

In order to maintain transparency attached is my live results with the strategy over the last year and a half accross 3 revisions of the strategy using a dedicated $1000 live account. As mentioned the Mar 22 version was ran with much larger exposure and hence shows a disproportionate loss compared to the previous versions.

Untill my next update. Let’s remain positive.

Sincerely,

Juan

Adding to my last update, I have decided to take an even deeper look into the strategy and carefully analyse it’s strengths and weaknesses. Spending many hours today I looked at each and every trade to see if there are anything that I would like to change or improve. Rather surprisingly and actually quite positive is the fact that I did not find anything I felt would benefit from changing at this stage. However, I did identify many situations where the strategy could have made much more money have it stayed in the winning trades for longer.

So rather than changing anything I added a new algorithm to supplement the existing strategy. It very simply works by re-entering trades that resulted in a win before reaching it’s maximum attempts. The new trades are then seperately managed by a pre-defined takeprofit and stop loss which is slightly adjusted depending on the direction of the major higher timeframe trend.

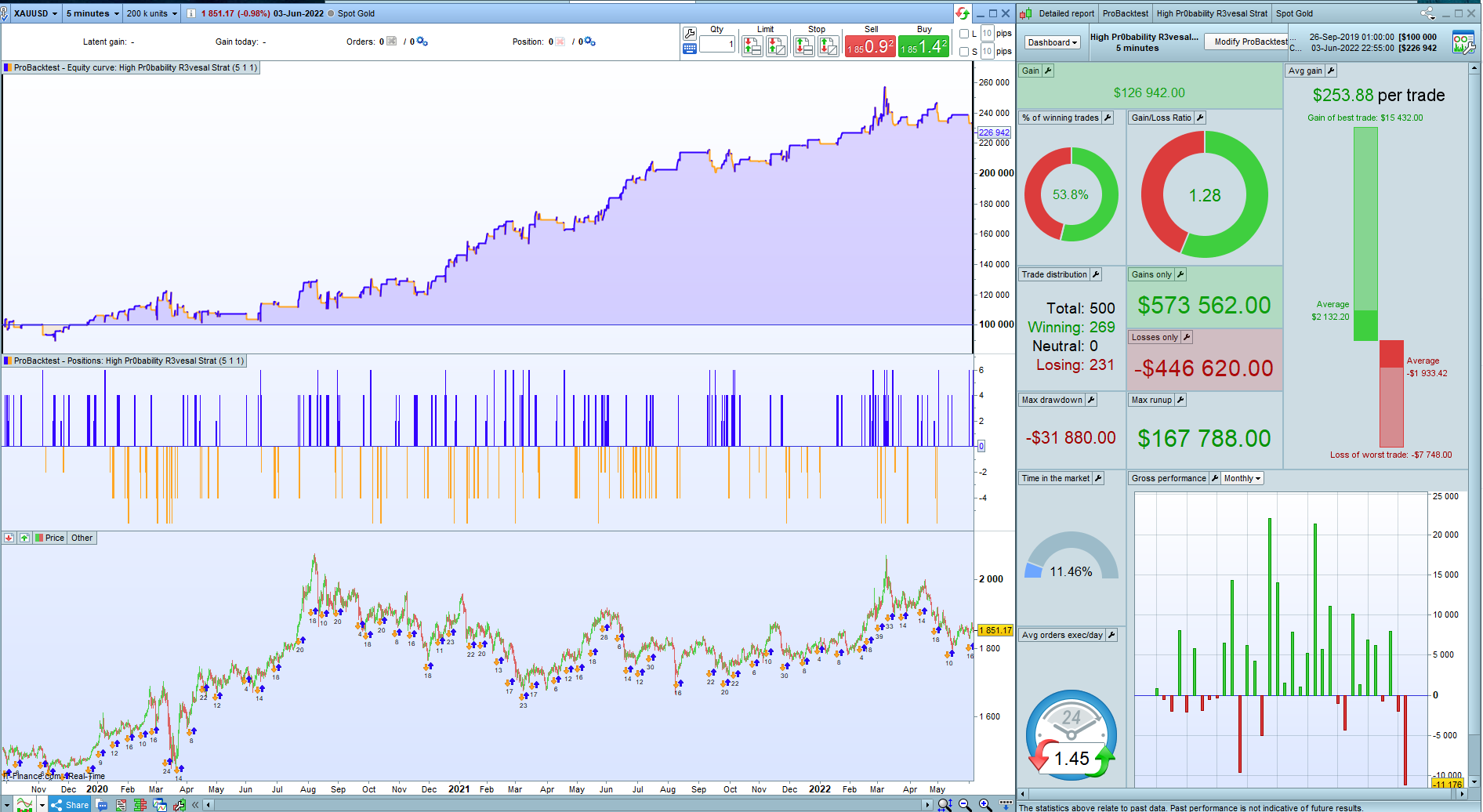

By taking these additional trades directly after a winning position, I have managed to increase both the overall profit and reduce the total drawdown without having to optimize or change anything of the existing strategy. Attached is the full backtest of the new strategy and I am really liking what I see a lot. The additional positions along with the data from linear reversion algorithm seems to completely negate the losses of the recent 3 months.

I will personally be running this improvement for the remainder of the month and release it as an update on the marketplace should everything work as expected.

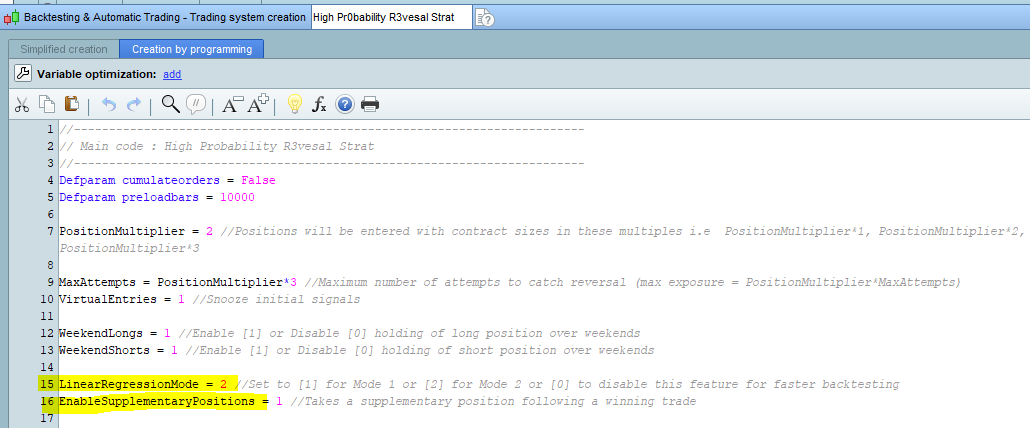

Over the past three days I did further extensive back and forward testing with the new supplementary trading algorithm enabled and decided to release the new version as an update today already considering there will be a option to Enable or Disable it (see attached settings). So for those that want to use it the option is now available.

I have also decided to add an alternative mode to the Linear Regression algorithm discussed in detail on page 6 of this thread. The main reason for this option is that the current Linear Regression algorithm makes it difficult to compare results as it requires at least 30 trades to start and will dynamically change the performance depending on how long the strategy has been running live or how far back it is being backtested. The alternative mode of the algoritm will now calculate the linear regression of the strategy based on the performance of the last 6 trades. This will help to standardize our backtest reports and should theoretically optimize performance sooner since it doesn’r require a minimum of 30 trades before kicking-in. Obviously considering a longer term operation (1 year plus) Mode 1 will likely be superior seeing it will have a much larger dataset to calculate the ‘average’ linear regression of performance.

Attached is two backtests using the Spot Gold instrument (which has much bigger exposure) but allows for double the history to be loaded in the backtest.

- LinearRegressionMode set to 0 (Algorithm Disabled)

- LinearRegressionMode set to 2 (Using Linear Regression of fixed period)

Juan, I have no stake in this whatsoever, but do you really think it is a good idea to make a Strategy “variable” so that out of all the very first thing what will happen is that nobody is able to compare anything with anything else ?

You could be the only person I have a high esteem of, regarding the selling of Automated Strategies. So I hope you will take this as a good advice from someone watching from the sidelines.

I understand that you need to do something, though. So it intrigues ?

Hi Peter, as you probably understand my first priority is to make the strategy as resilient as possible. The variability I spoke about is due to the fact that dpending on the date when the strategy is started be that Live or in a backtest environment, the Linear Regression algorithm keeps track of the ‘normal’ distribution of results and ‘manages’ the strategy when performance no longer appear in-line with the ‘typical’ distribution (be that outperformance or underperformance) and subsequently has the ability to temporarily suspend the strategy, allowing market conditions leading to this behaviour to ‘normalize’. This approach makes a big difference according to my backtested results and is hence the reason for its inclusion.

Regarding the option to allow users of the strategy to manually enable or disable certain features has to do with each persons appetite for risk. I have actually specifically been asked by clients in the past to include some of these options i.e. disallowing the holding of positions over weekends for example. Referring to the new supplementary positions algorithm . The reason I added the option for users to enable or disable it, is because it is a new standalone algorithm that runs alongside the existing strategy and does not have months of Live tested data behind it.

Users of a strategy also prefer to do their own backtests on a strategy and due to the way ProRealTime handles it’s resources, backtesting the strategy when having to calculate linear reversion on each bar can be extremely time consuming (and even sometimes fail to load the entire backtest). So aside from allowing a ‘standarized’ backtest, this is another reason why I added the option for the function to be disabled.

I trust this anwers your question to some extent.

The variability I spoke about is due to the fact that dpending on the date when the strategy is started be that Live or in a backtest environment,

Wouldn’t you be able to incorporate that past data hard-coded in your program (differentiated e.g. per week) ?

So if I understand correctly, the friction lays in the fact a newly started strategy has to re-learn. But this will already happen when a strategy is stopped for a random reason outside of your powers ? Thus in any event that would be counter-attacked when the data is hard-coded in the program (and can be reloaded from your sources) ? … In the Indicator code of course ?

Now you can freely apply / provide updates, once your customers have trust in what you’re doing anyway.

I actually did think of that, but due to the way linear regression is calculated on the equity/performance curve this is unfortunaltely not possible.

The main formula is as follows: LinearRegression[NumberOfTrades](StrategyProfit)

The formula is updated after each trade and is therefore based on the specific number of trades and the specific profit/loss of the strategy since started/backtested.

So for example since I do not know when someone will start the strategy I cannot pre-populate the number of trades. And also since I do not know what exposure everyone uses I won’t know what the strategy profit would be at that stage.

However, it is important to note that this algoritm only serves to enhance the strategy, and we can always get a baseline of the strategy performance by disabling the algorithm providing us a way to compare results.

Hello Juanj, what are the results for this month?

Hi Everyone

Attached is results for teh new version we have been running since begining of teh month. It ended slightly neagtive but mostly flat.

But I do have some good news!

Considering the strategy is currently exclusively trading on Gold and considering the fact that we have not seen the number of favourable opportunities we would have liked, I have decided to launch a second version of the strategy that that will be configured to run on forex. This new strategy will be laoded as seperate product on marketplace and ALL existing customers will get a FREE coupon to purchase it.

The existing Gold strategy remains valid and active considering conditions will likely beome favourable again in the near future.

I aim to launch the FX version of the strategy in the next 2 weeks and will email the coupon code to all existing clients of the Gold version of the strategy as soon as teh product is live.

I will send screenshots of the new strategy within the comming week.

Unfortunately our country is currently experiencing extreme blackouts with power cuts of up to 10 hours each day so everything takes much longer than usual to get done.

Regards,

Juan

Perhaps just to clarify as to why I plan on making the FX version available as a separate and standalone version. Firstly when considering FX is measured in pips vs Gold measured in points I have to make some digit adjustments to the code. Secondly due to FX being heavilly influenced by time zones with trading activity spiking during certain sessions I need to make changes to factor this in.

Finally, not all users are comfortable with changing a bunch of variables to configure the strategy depending on the market they wish to trade it on. This also introduce the chance of introducing mistakes if the wrong settings are changed.

However above changes aside, by simply changing some parameters of the existing strategy we are already able to see positive results on FX. Which is ofcourse excellent news when considering this is a great validation of the strategies trading edge.

Attached is the existing version of the strategy configured for use on EURUSD.

For clients interested, I can make these settings available should you wish to conduct your own tests in the meantime. Simply reach out to me via the contact form on my PRC Store.