Hi

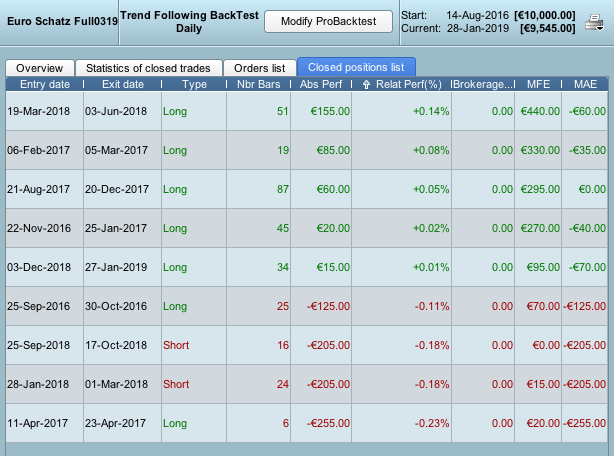

Could anyone tell me how Relative Performance % is calculated in backtests?

Is this the performance of the trade based on the initial capital after each trade? Or is it the cumulative profit plus capital after each trade?

My aim is to backtest several markets and, because I can only do one at a time, I need to stitch the results together to get the trades in date. Therefore, I need a way of calculating the gain or loss on each trade to see how the strategy does over time. If the relative performance is cumulative profit plus capital that should be fine. But if it is based on initial capital then it will skew what I am trying to do with the multiple backtests. Unless you have any other suggestions to stitch several backtests together?

Thanks