Use of filters can certainly help and there are indicators which are extremely useful. The problem I have with using too many filters is that the number of trades end up going down which can significantly affect ‘statistical significance’. Staistical significance I view as extremely important… although I am not sure what constitutes a significant amount of trades over a particular time period?

Hi Jim,

I talked about this only a few days ago in some post (maybe you read it) but what you say there is indeed the most important;

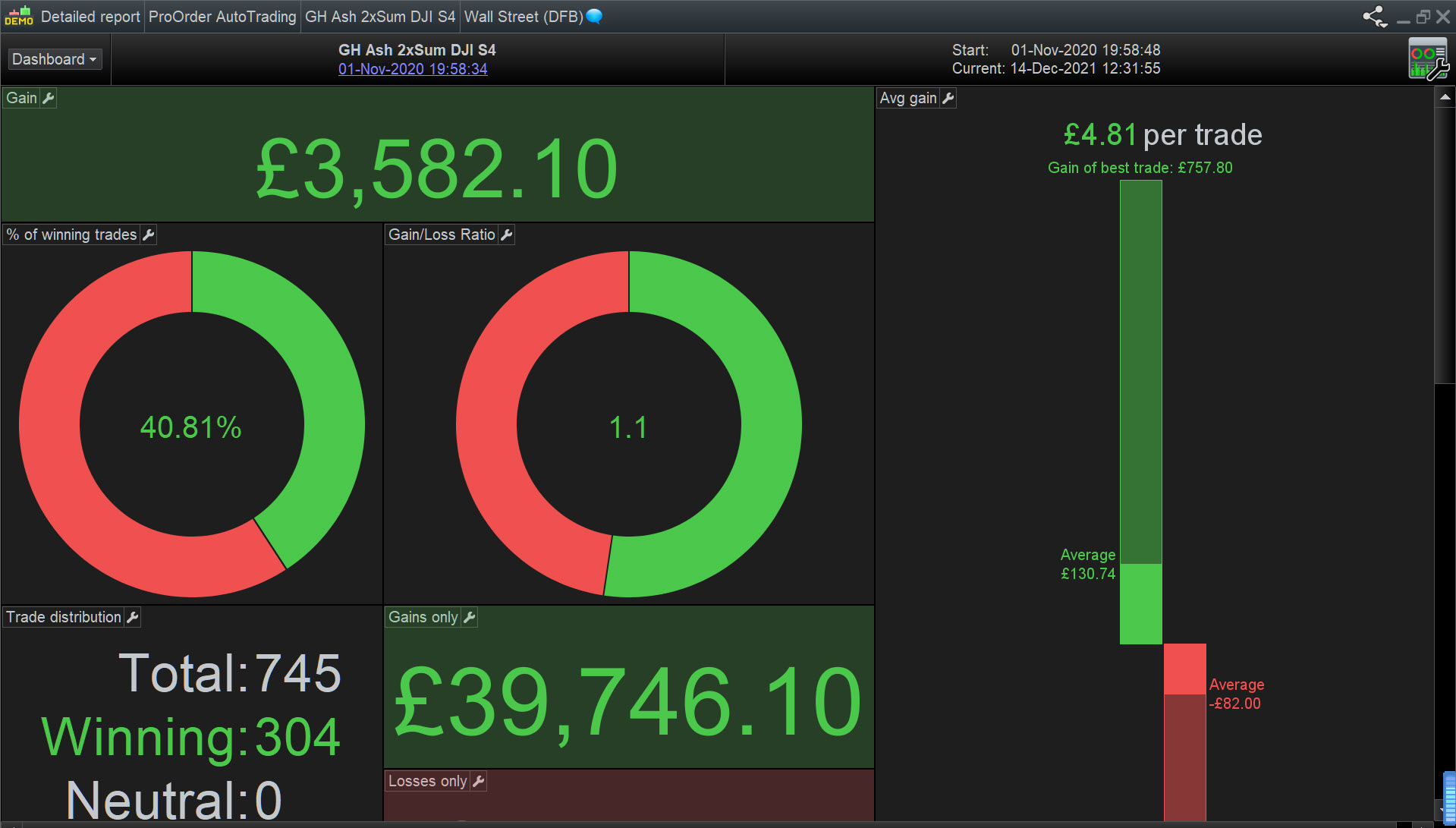

I just put live a system which was forward tested only 48 hours – see attachment – this started Monday 5am and was just stopped and changed to Live. Btw, it is 1second TF.

My understanding is that WFA (when used correctly) is the ‘gold standard’ when it come to robustness testing.

One could attest that this 48 hours is way too few for WF testing, and normally it obviously is. However, this strategy had changes applied to it and after “ages” of testing it and running it Live, for me this is enough to know its (relative) behaviour. But as I said, it takes literally years. It takes years to simply know that this specific system (the way it has been set up) is robust when its losing vs winning rate is ~ 1:10 (see the 4:39).

Would I back test this over 1M candles, which is only one month, it should come up with ~650 trades and something like 75 losses. I just know this is fine without looking at the real profit. This is the law of the big numbers … with also the notice that currently there’s “ultra low” volatility, which in my opinion is way difficult for any strategy and which is exactly what this version was adapted to. N.b.: My previous post about this showed losses in the last 3 days and they were caused by low volatility. That part now wins too. **

Forward testing this longer than e.g. 48 hours, is “useless” because it won’t bring other news. Crucial, for me, seems to be the fact that if the forward testing would turn out to be losing after e.g. 3 months, what would I need to do to improve on it ? Also, how much would it have my continuous attention when it was only “testing” ?

And so the testing happens in Live. Now it will have my full attention, because now it is about real $. I watch its behaviour (during this typing and all) and that really is the best “forward testing” IMO.

This is all easy to say when you have a winning strategy in the first place, right ?

**) I think that observing the past by means of back testing against Live data, is enormously valuable. Thus, if I suddenly observe losses in subsequent days, it is my idea to counter-attack that specific part, quit the Live system and replace it with the improvement. And Yes, this seems very ad-hoc stuff, but this is exactly what the ultra-low TF system can do for you (once you have something of value).

Developing a system like this is almost 100% based on empirical finding. I mean, I don’t work with mathematics of any sort, but I observe reality and what my system does with it. It should to what I would do myself, meaning that it should press the buttons how I would press them, with the difference of the system lacking emotion. So there it should be better than me …

What can one learn from this blahblah ? well, not really much I am afraid. Except for the one thing I already told : it takes years. And this investment is – or at least should be worth while;

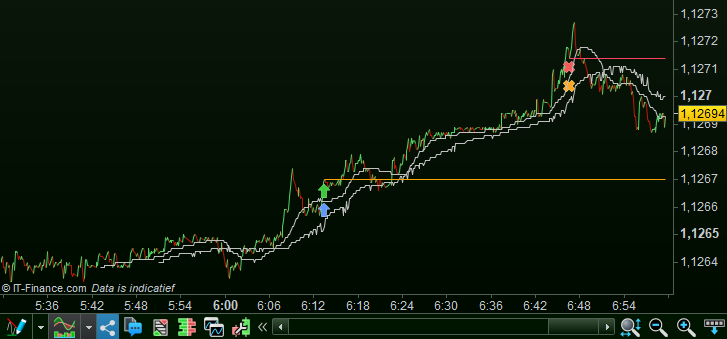

2nd attachment is its first trade which by now turned into a profit (my phone somewere tells me “ka-tsing !” which is the best part of it all – haha.).

… And the fun of the law of the big numbers are the big numbers themselves. Thus, many trades with if all is right, many wins. This should also mean many $. But alas.

I now recall that my previous post about this system was about losses. Thus, the losses will be there. And in my opinion you should try to beat the losses – and most certainly not the number of them (that would be the first so-easy-to-make mistake with back testing). Fact remains (and you speak about that) that the Entry is crucial. Thus, how to make the trade not turn into a loss. This is very different than backtest until all the losses have vanished. Or, how to minimise the loss when it will be there anyway. This too is very different from backtesting it out all together (I repeat : the biggest mistake). … And you can do this only with the fastest responding system (obviously ?).

Last thing – see 3rd attachment. As I type, I am watching the price development and am a sort of praying that the thing should not go Short on me. Why ? well, because I feel (experience) that the trend is up. I thus also feel that the system must think the same. But *if* it goes short after all, it should g-d win and know better than myself. Still at this moment I am sure it should not go short. So it really is about that. How to let it behave like I would do it myself. Fun is also that this forward -Live- testing is quite emotional, especially with low volatility. And this part of the fun too, can only be achieved with the lower TF.