I have various strategies on test in demo and one of them (Reiners Pathfinder V8) just closed out a seven positions so I thought I’d check in both the strategy performance detailed report and my overall performance detailed report and see how they did. The results in each are very different for the same trades and they don’t add up to the same value. There is a £0.03 difference. Why is this?

How is the Abs Perf calculated and what apart from the difference between buy and sell price is in the calculation?

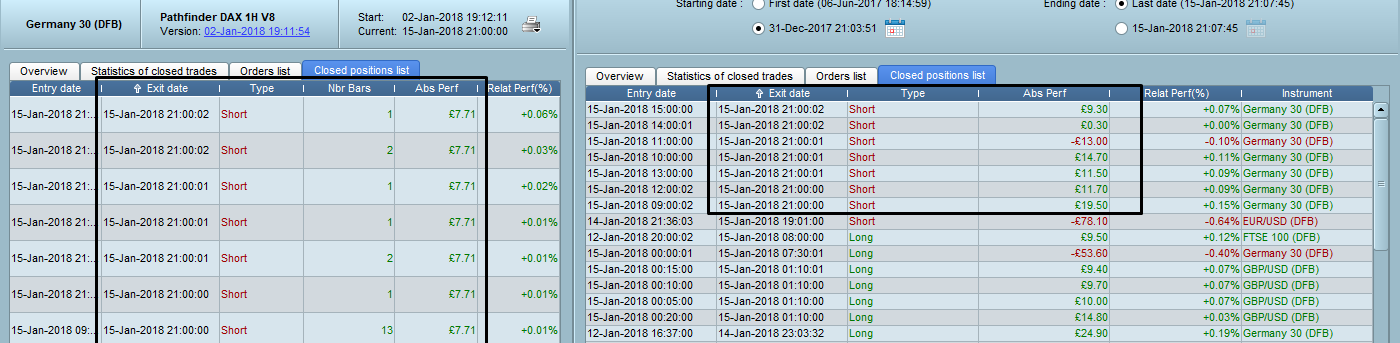

Image attached.

AVT

AVTParticipant

Senior

Are there different entry times?

Yes. The times shown in the strategy performance report are one at 0900 and the rest at 2100 to within two seconds. If you look at the image in the first post then you will see that the entry times in the overall report are all over the shop.

AVTParticipant

Senior

Ok let me put it this way: I understand this abreviation “Abs Perf” standing for “Absolute Performance” – in this context it would surely not be “absolutely perfect” or “absence of perfection”. Mathematically the absolute performance of a trade is entry/exit difference DOT. If there were commisions or something alike to be added, that’s called the adjusted performance; and if we look at it with regard to the capital we had before we started the trade, that is (one kind of) relative performance.

I would think that for clarity a position should be considered a position when you enter and the ABS PERF (Absence of Perfection – fabtastic AVT!) easily calculated as the difference when you close. Why do the two screens of strategy performance and overall performance have to display it differently? One clearly has divided the amount won/lost between the number of positions closed at the same time and the other has shown the more accurate individually closed positions. Somewhere on the way 3 pence has been lost. If I lose 3 pence in the pound accuracy in calculation for every seven pounds worth of positions closed then the result become very difficult to interpret.

Hello Vonasi,

We have tried to understand your issue based on the information available on this post. However, for this kind of problematic, it is really necessary for us to have access to the code of your strategy in order to test the strategy in exactly the same conditions as you did. For this reason, even on this occasion, I have to ask you to send us a technical report. I write here again the instructions to send us a report with authorisation to analyse your code:

– As soon as you encounter the issue, go to the “Help” menu on the ProRealTime toolbar.

– Click on “Technical support”

– Giving as many details as possible, explain the issue you are having in the text box and mention the name of the code you are referring to.

– To receive in depth assistance, it is necessary to analyze the code itself which is encrypted on our servers. To allow our technicians temporary access, please check the box marked “I authorize the decryption of the codes…”

– Click “Send report”

Many thanks,

Best wishes,

Ilaria

ProRealTime

Hello again Ilaria. This is not really something that needs access to other peoples codes. Look at the image in the first post and you see two reports. One is from the individual strategy performance report accessed by clicking ‘View Performance’ in the ProOrder Autotrading window and the other is the same trades but shown in the Detailed Report window that shows overall performance of all strategies that have been run to date. The same trades are shown differently. One appears to have the total profit/loss divided amongst the trades evenly whilst the other shows the individual trades with different values. There is also a difference in the total value of all the trades in each report of 3p. Run any strategy with cumulate positions and you will most likely see a similar difference or just run the same Pathfinder V8 strategy that can be easily found on this forum.

At the moment there are many greater issues with PRT than this (although in my mind any return of incorrect results makes users lose confidence in PRT’s ability to be relied upon for autotrading) and I think that from our recent communications PRT’s engineers are struggling to solve any of them – so I think it is best that they concentrate on the really major issues first rather than this one and then maybe just one of them will be fixed 🙂

There must be a rounding calculation issue somewhere ..

Or maybe is it related? https://www.prorealcode.com/topic/ig-vs-prt-differences-in-profitloss/

There must be a rounding calculation issue somewhere .. Or maybe is it related? https://www.prorealcode.com/topic/ig-vs-prt-differences-in-profitloss/

Yes I’m sure that is just something as simple as a rounding issue for the 3p difference and this is a concern as that is a large percentage of a series of small wins. I see in the other post you mention that there is something in the order of £120 difference in a year so it all adds up to a lot of inaccuracy in test results.

On the other issue I do not understand why the presentation of the trades closed has to be completely different between the two reports. It is almost as if two different people were tasked with the same job in two different parts of PRT and both decided upon a different solution to the same problem.

Hello again Vonasi,

Thank you for your message. However, I strongly suggest you send us a technical report in order to allow us to analyse your issue.

Thank you for your comprehension.

Best wishes,

Ilaria

ProRealTime