Hey traders,

Long time no speak, I have been waiting for MTF to become available but it seem to take longer and longer.

However here is an early christmas gift. The below update is fairly useful on low-medium timframes such as M15 but when using aggregating orders (of course we can stick with single orders too) we need to run it on low TF such as M1 or lower to be able to rely on our SL or BB exit since it kicks in at close of candle and too much can happen during a M15 candle and cause much larger losses during the 15 minutes it takes for the candle too close hence I recommend setting a low maximum number of orders and monitor the system manually while it is up and running.

The update is based on Squeeze (from BB Squeeze but only the squeeze function and not the momentum) and Heiken Ashi. Squeeze need to be off (blue bar) and Heiken Ashi decide the direction of the trade either by change of color or by the current color when Squeeze changes to off (for change of color “HAC crosses over 0” and for current direction “HAC >0” for long) on line 31.

First the required indicators, HA Change;

//Heikin-Ashi

xClose = (Open+High+Low+Close)/4

if(barindex>2) then

xOpen = (xOpen[1] + xClose[1])/2

endif

changeToGreencandle = xClose>xOpen AND xClose[1]<xOpen[1]

ChangeToRedcandle = xClose<xOpen AND xClose[1]>xOpen[1]

Greencandle=xclose>xopen

redcandle=xclose<xopen

If changeToGreencandle then

Indicator1=1

elsif greencandle then

indicator1=0.5

elsif Changetoredcandle then

indicator1=-1

elsif redcandle then

indicator1=-0.5

Else

Indicator1=0

Endif

Return indicator1

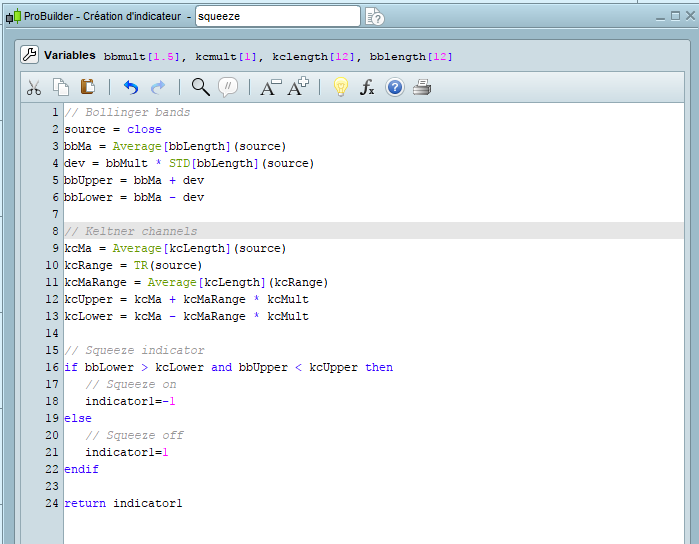

And Squeeze;

// Bollinger bands

source = close

bbMa = Average[bbLength](source)

dev = bbMult * STD[bbLength](source)

bbUpper = bbMa + dev

bbLower = bbMa - dev

// Keltner channels

kcMa = Average[kcLength](source)

kcRange = TR(source)

kcMaRange = Average[kcLength](kcRange)

kcUpper = kcMa + kcMaRange * kcMult

kcLower = kcMa - kcMaRange * kcMult

// Squeeze indicator

if bbLower > kcLower and bbUpper < kcUpper then

// Squeeze on

indicator1=-1

else

// Squeeze off

indicator1=1

endif

return indicator1

The strategy for longs;

/// Definition of code parameters

defparam preloadbars =10000

DEFPARAM CumulateOrders = true // Cumulating positions deactivated

SQ= call "Squeeze"[12, 1.5, 12, 1]

HAC= call "HA Change"

once RRreached = 0

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 1 //whole account risk in percent%

amount = 1 //lot amount to open each trade

rr = 1 //risk reward ratio (set to 0 disable this function)

sd = 0.25 //standard deviation of MA floating profit

//dynamic step grid

minSTEP = 20 //minimal step of the grid

maxSTEP = 50 //maximal step of the grid

ATRcurrentPeriod = 150 //recent volatility 'instant' period

ATRhistoPeriod = 3000 //historical volatility period

ATR = averagetruerange[ATRcurrentPeriod]

histoATR= highest[ATRhistoPeriod](ATR)

resultMAX = MAX(minSTEP*pipsize,histoATR - ATR)

resultMIN = MIN(resultMAX,maxSTEP*pipsize)

gridstep = (resultMIN)

// Conditions to enter long positions

c1 = (SQ > 0)

c2 = (HAC CROSSES OVER 0)

//first trade whatever condition, for one cycle only add "AND STRATEGYPROFIT=0" on lne 34

if NOT ONMARKET AND (c1)=1 AND (c2)=1 then

BUY amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep then

BUY amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize

//actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*sd

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

SELL AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

And shorts;

/// Definition of code parameters

defparam preloadbars =10000

DEFPARAM CumulateOrders = true // Cumulating positions deactivated

SQ= call "Squeeze"[12, 1.5, 12, 1]

HAC= call "HA Change"

once RRreached = 0

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 1 //whole account risk in percent%

amount = 1 //lot amount to open each trade

rr = 2 //risk reward ratio (set to 0 disable this function)

sd = 0.25 //standard deviation of MA floating profit

//dynamic step grid

minSTEP = 20 //minimal step of the grid

maxSTEP = 50 //maximal step of the grid

ATRcurrentPeriod = 150 //recent volatility 'instant' period

ATRhistoPeriod = 3000 //historical volatility period

ATR = averagetruerange[ATRcurrentPeriod]

histoATR= highest[ATRhistoPeriod](ATR)

resultMAX = MAX(minSTEP*pipsize,histoATR - ATR)

resultMIN = MIN(resultMAX,maxSTEP*pipsize)

gridstep = (resultMIN)

// Conditions to enter short positions

c11 = (SQ > 0)

c12 = (HAC CROSSES UNDER 0)

//first trade whatever condition, for only one cycle add "AND STRATEGYPROFIT=0" on line 34

if NOT ONMARKET AND (c11)=1 AND (c12)=1 then

SELLSHORT amount LOT AT MARKET

endif

// case SELL - add orders on the same trend

if shortonmarket and tradeprice(1)-close>=gridstep then

SELLSHORT amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize

//actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*sd

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

EXITSHORT AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

Remember to be mindful of line 34 to set or avoid recurring cycles, recurring is great for testing but risky for live trading, also note to increase most parameters if using on very low TF.

I hope you will find it useful 🙂