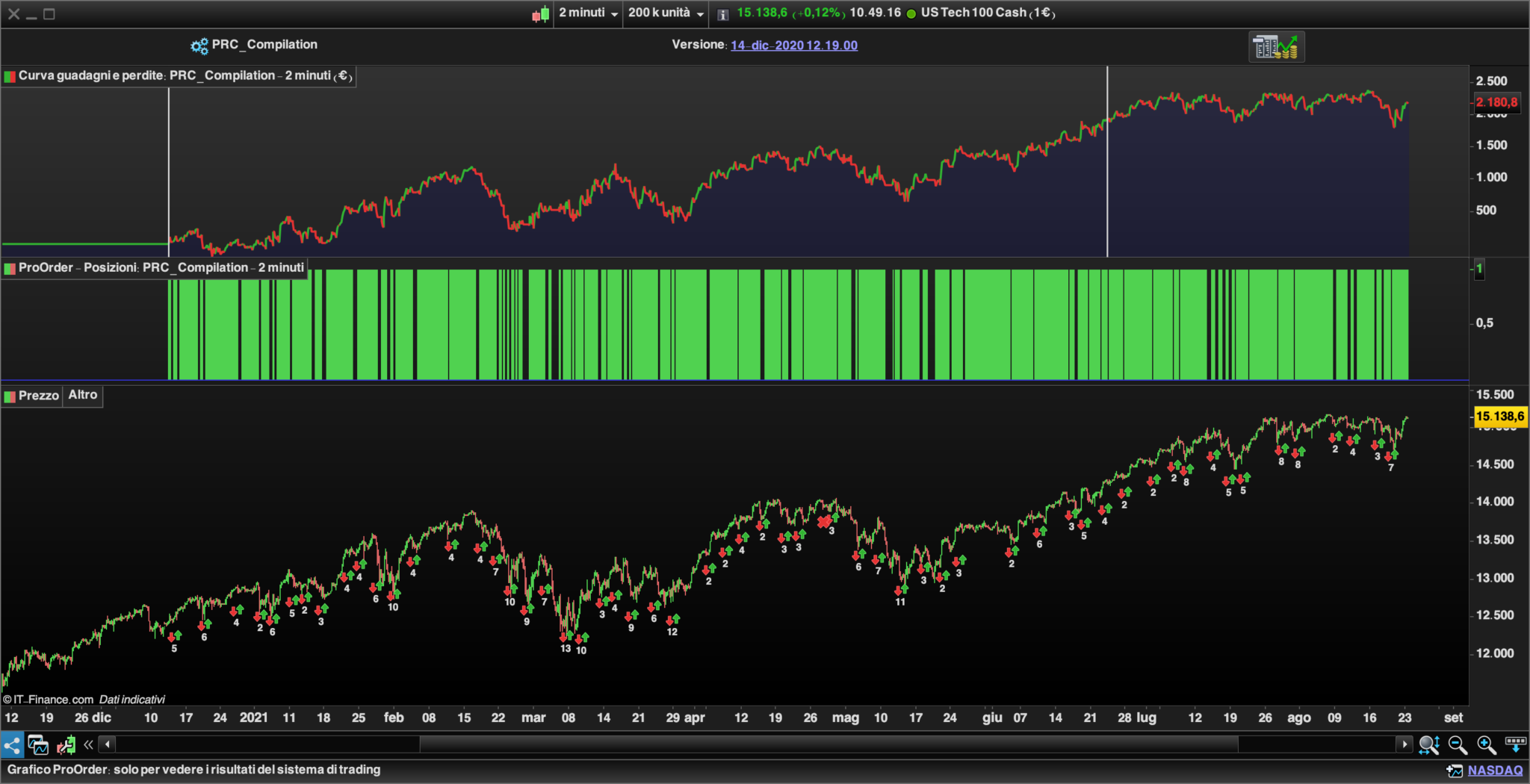

Hi,

This is the combination of the 5 different strategies for the DAX which vschmitt Artificall has previously openly shared. I have simply combined them into one strategy, with some additional code kindly provided by robertogozzi

The majority of the performance comes from the Momentum strategy however, the others smooth out the equity curve through their smaller contributions to the overall performance.

//================================================

// Code: _PRD DAX Combi

// Source: https://artificall.com

// Author: Vivien Schmitt

// Version 2

// Index: DAX

// TF: 10 min

// Notes: v1.1 Momentum only

// Notes: v2 Portfolio of multi strategies

// robertogozzi provided position mgt logic

// v2.1 Added Trend Following

// v2.2 Added Double Bottom

// v2.3 Added Green Hammer

// v2.4 Added Counter Trend

// v2.5 Tested Day of Week - ignore

// v2.5 Optimised position size logic

//================================================

DEFPARAM CUMULATEORDERS = TRUE // only one trade in the same time

DEFPARAM FLATBEFORE = 090000 // avoide entry opening before this hour

DEFPARAM FLATAFTER = 213000 // close entry at this hour

IF NOT OnMarket THEN //Make sure you reset these variables to ZERO when not trading

P1 = 0

P2 = 0

P3 = 0

P4 = 0

P5 = 0

ENDIF

//RISK MANAGEMENT

PositionSize=1

//===================================== MOMENTUM STRATEGY ================================================

//MOMENTUM STRATEGY

// MARKET TREND USING LINEAR REGRESSION

// Set of technical indicators to test

IF P1 < 1 THEN

m10 = momentum[10](close)

m20 = momentum[20](close)

m50 = momentum[50](close)

m100 = momentum[100](close)

m300 = momentum[300](close)

m800 = momentum[800](close)

cM1 = (m10[0]-m10[1]) > 0

cM2 = (m20[0]-m20[1]) > 0

cM3 = (m50[0]-m50[1]) > 0

cM4 = (m100[0]-m100[1]) > 0

cM5 = (m300[0]-m300[1]) > 0

cM6 = (m800[0]-m800[1]) > 0

//--------------------------------------------------------------------------

// ENTRY POINT

//#13

conditionMomentumM = cM1 AND cM2 AND cM3 AND NOT cM4 AND cM5 AND NOT cM6

//--------------------------------------------------------------------------

// MARKET VOLATILITY USING STANDARD DEVIATION

volatility100MaxM = 50

volatility100MinM = 1

volatility100M = STD[100] (close)

conditionMarketVolatilityM = volatility100M < volatility100MaxM AND volatility100M > volatility100MinM

//conditionMarketVolatility=1

//--------------------------------------------------------------------------

// OPEN A LONG ENTRY

IF conditionMomentumM AND conditionMarketVolatilityM THEN

PSTOPLOSSMO = 100

PTARGETMO = PSTOPLOSSMO * 2

SET STOP pLOSS PSTOPLOSSMO

SET TARGET pPROFIT PTARGETMO

BUY PositionSize CONTRACT AT MARKET

P1 = 1

ENDIF

//SHORT ENTRY CONDITIONS

s1 = (m10[0]-m10[1]) < 0

s2 = (m20[0]-m20[1]) < 0

s3 = (m50[0]-m50[1]) < 0

s4 = (m100[0]-m100[1]) < 0

s5 = (m300[0]-m300[1]) < 0

s6 = (m800[0]-m800[1]) < 0

conditionSellMomentum = s1 AND s2 AND s3 AND NOT s4 AND s5 AND NOT s6

// OPEN A SHORT ENTRY

IF conditionSellMomentum AND conditionMarketVolatilityM THEN

PSTOPLOSS = 100

PTARGET = PSTOPLOSS * 2

SET STOP pLOSS PSTOPLOSS

SET TARGET pPROFIT PTARGET

SELLSHORT PositionSize CONTRACT AT MARKET

P1 = 1

ENDIF

ENDIF

//===================================== TREND FOLLOWING ================================================

//TREND FOLLOWING

// MARKET TREND USING LINEAR REGRESSION

IF P2 < 1 THEN

DRL100 = average[10](LinearRegression[100])

slope100 = DRL100[0] - DRL100[1]

DRL300 = average[10](LinearRegression[300])

slope300 = DRL300[0] - DRL300[1]

DRL600 = average[10](LinearRegression[600])

slope600 = DRL600[0] - DRL600[1]

conditionMarketTrend = slope100 > 0 OR slope300 > 0 OR slope600 > 0

//--------------------------------------------------------------------------

// MARKET VOLATILITY USING STANDARD DEVIATION

volatility100Max = 11

volatility100Min = 1

volatility100 = STD[100] (close)

conditionMarketVolatility = volatility100 < volatility100Max AND volatility100 > volatility100Min

//--------------------------------------------------------------------------

// ENTRY POINT

rsi14 = RSI[14] > 30

macd12 = MACD [12,26,9] > 0

stocha10 = Stochastic[10,3](close) > 0

conditionEntryPoint = rsi14 AND macd12 AND stocha10

//--------------------------------------------------------------------------

// OPEN A LONG ENTRY

//IF NOT LongOnMarket AND conditionMarketTrend AND conditionMarketVolatility AND conditionEntryPoint THEN

IF conditionMarketTrend AND conditionMarketVolatility AND conditionEntryPoint THEN

PSTOPLOSSMT = 100

PTARGETMT = PSTOPLOSSMT * 2

SET STOP pLOSS PSTOPLOSSMT

SET TARGET pPROFIT PTARGETMT

BUY PositionSize CONTRACT AT MARKET

P2 = 1

ENDIF

ENDIF

//===================================== DOUBLE BOTTOM RECOGNITION ================================================

// DOUBLE BOTTOM RECOGNITION

IF P3 < 1 THEN

ONCE period = 10

ONCE correlation = 0.8

R = 0

x1 = 10

x2 = 9

x3 = 8

x4 = 9

x5 = 10

x6 = 10

x7 = 9

x8 = 8

x9 = 9

x10 = 10

xBar=(x1+x2+x3+x4+x5+x6+x7+x8+x9+x10)/period

varianceX=(SQUARE(x1-xBar)+SQUARE(x2-xBar)+SQUARE(x3-xBar)+SQUARE(x4-xBar)+SQUARE(x5-xBar)+SQUARE(x6-xBar)+SQUARE(x7-xBar)+SQUARE(x8-xBar)+SQUARE(x9-xBar)+SQUARE(x10-xBar))/(period-1)

ecarTypeX=SQRT(varianceX)

y1 = MAX(Open[9], Close[9])

y2 = MAX(Open[8], Close[8])

y3 = MAX(Open[7], Close[7])

y4 = MAX(Open[6], Close[6])

y5 = MAX(Open[5], Close[5])

y6 = MAX(Open[4], Close[4])

y7 = MAX(Open[3], Close[3])

y8 = MAX(Open[2], Close[2])

y9 = MAX(Open[1], Close[1])

y10 = MAX(Open[0], Close[0])

yBar=Average[period](Close)

ecarTypeY=STD[period](Close)

covarianceXY=((x1-xBar)*(y1-yBar)+(x2-xBar)*(y2-yBar)+(x3-xBar)*(y3-yBar)+(x4-xBar)*(y4-yBar)+(x5-xBar)*(y5-yBar)+(x6-xBar)*(y6-yBar)+(x7-xBar)*(y7-yBar)+(x8-xBar)*(y8-yBar)+(x9-xBar)*(y9-yBar)+(x10-xBar)*(y10-yBar))/(period-1)

R=covarianceXY/(ecarTypeX*ecarTypeY)

IF R < correlation THEN

R = 0

ENDIF

//RETURN R AS "R"

closeY1 = Close[9]

highY5 = high[5]

closeY10 = Close[0]

neckLine = closeY10 => closeY1 AND closeY10 => highY5

conditionDoubleBottom = R AND neckLine

//--------------------------------------------------------------------------

// OPEN A LONG ENTRY

//IF NOT LongOnMarket AND conditionDoubleBottom THEN

IF conditionDoubleBottom THEN

PSTOPLOSSDB = 100

PTARGETDB = PSTOPLOSSDB * 2

SET STOP pLOSS PSTOPLOSSDB

SET TARGET pPROFIT PTARGETDB

BUY PositionSize CONTRACT AT MARKET

P3 = 1

ENDIF

ENDIF

//===================================== GREEN HAMMER ================================================

//GREEN HAMMER

// MARKET VOLATILITY USING STANDARD DEVIATION

IF P4 < 1 THEN

volatility100MaxGH = 20

volatility100MinGH = 1

volatility100GH = STD[100] (close)

conditionMarketVolatilityGH = volatility100GH < volatility100MaxGH AND volatility100GH > volatility100MinGH

//conditionMarketVolatility=1

//--------------------------------------------------------------------------

// ENTRY POINT

// Strategy of the Doji Hammer

hammerBody = high = close AND open < close

hammerTail = low < open AND (open - low) > ((high - open) * 1.5)

dojiHammer = hammerBody AND hammerTail

//--------------------------------------------------------------------------

// OPEN A LONG ENTRY

//IF NOT LongOnMarket AND conditionMarketVolatility AND dojiHammer THEN

IF conditionMarketVolatilityGH AND dojiHammer THEN

PSTOPLOSSGH = 80

PTARGETGH = PSTOPLOSSGH * 2

SET STOP pLOSS PSTOPLOSSGH

SET TARGET pPROFIT PTARGETGH

BUY PositionSize CONTRACT AT MARKET

P4 = 1

ENDIF

ENDIF

//===================================== COUNTERTREND ================================================

//COUNTERTREND

// MARKET TREND USING LINEAR REGRESSION

// Set of technical indicators to test

IF P5 < 1 THEN

c1 = LinearRegressionSlope[10](close) > 0

c2 = LinearRegressionSlope[20](close) > 0

c3 = LinearRegressionSlope[50](close) > 0

c4 = LinearRegressionSlope[100](close) > 0

c5 = LinearRegressionSlope[300](close) > 0

c6 = LinearRegressionSlope[800](close) > 0

//--------------------------------------------------------------------------

// ENTRY POINT

//#13

conditionCounterTrend1 = NOT c1 AND NOT c2 AND c3 AND c4 AND NOT c5 AND NOT c6

conditionCounterTrend = conditionCounterTrend1

//--------------------------------------------------------------------------

// MARKET VOLATILITY USING STANDARD DEVIATION

volatility100MaxCT = 50

volatility100MinCT = 1

volatility100CT = STD[100] (close)

conditionMarketVolatilityCT = volatility100CT < volatility100MaxCT AND volatility100CT > volatility100MinCT

//conditionMarketVolatility=1

//--------------------------------------------------------------------------

// OPEN A LONG ENTRY

//IF NOT LongOnMarket AND conditionCounterTrend AND conditionMarketVolatility THEN

IF conditionCounterTrend AND conditionMarketVolatilityCT THEN

PSTOPLOSS = 100

PTARGET = PSTOPLOSS * 2

SET STOP pLOSS PSTOPLOSS

SET TARGET pPROFIT PTARGET

BUY PositionSize CONTRACT AT MARKET

P5 = 1

ENDIF

ENDIF

ONCE P1 = 0

ONCE P2 = 0

ONCE P3 = 0

ONCE P4 = 0

ONCE P5 = 0

Thanks for ur contribution. Where is the original thread?

I have been using this in a modified form since 08/20. But even the original system still works flawlessly today.

Long only strategy with the TMA channel

Thanks phoentzs.

Something is wrong with ur link.

Whats the different between the orginal and ur modified version? Would be great if u post ur modified version in the linked thread.

Looks like the word “only” dropped from the URL and doesn’t get copied with a straight copy paste from the page, we’ll look at it

Sorry, here is a new link. The link points to the original version, which works fine. I’ll keep my version to myself for now. 😉

Long only strategy with the TMA channel

The link doesn’t work either. Why?

Ok, it’s a known website bug on a very small number of old links apparently, but a tough one to understand why as previous investigations didn’t solve it. Sorry.

As a workaround please click on the faulty link anyway, and in the address box at top of the page, add with keyboard the word “only” in the middle of … long- -strategy … to make it the normal text: … long-only-strategy …

In my opinion should all strategys have their own thread. A better way of discussion and improvements. Maybe coder JohnScher or phoentzs can start one. If not i will tonight.

Or copy the link above and paste direct into browser address bar.

tough one to understand

Links to Topics that don’t work may be due to the Title / Subject of the Topic having been changed after the original link was created (i.e. before the Topic title was changed).

In this particular case it’s a library topic and title wasn’t changed, but I don’t know much more about the subject, it’s in Nicolas’ hands. Also, yes your copy-paste of the “texted” link in the address bar rather than clicking on it would work too.

@samsanpop – regarding _PRD DAX Combi strategy:

Removing or commenting out the sellshort function, essentially making it a long only strategy, creates slightly better results. Thanks for sharing!

Remove this:

//SHORT ENTRY CONDITIONS

s1 = (m10[0]–m10[1]) < 0

s2 = (m20[0]–m20[1]) < 0

s3 = (m50[0]–m50[1]) < 0

s4 = (m100[0]–m100[1]) < 0

s5 = (m300[0]–m300[1]) < 0

s6 = (m800[0]–m800[1]) < 0

conditionSellMomentum = s1 AND s2 AND s3 AND NOT s4 AND s5 AND NOT s6

// OPEN A SHORT ENTRY

IF conditionSellMomentum AND conditionMarketVolatilityM THEN

PSTOPLOSS = 100

PTARGET = PSTOPLOSS * 2

SET STOP pLOSS PSTOPLOSS

SET TARGET pPROFIT PTARGET

SELLSHORT PositionSize CONTRACT AT MARKET

P1 = 1

ENDIF

thanked this post

Hi, Anyone can convert “GBPJPY MINI M15” code itf file in Metatrader 4 file Expert Advisor?

Defparam cumulateorders = false

// TAILLE DES POSITIONS

n = 1

// PARAMETRES

// high ratio = few positions

// AUD/JPY : ratio = 0.5 / SL = 0.8 / TP = 1.2 / Period = 12

// EUR/JPY : ratio = 0.6 / SL = 1 / TP = 0.8 / Period = 8

// GBP/JPY : ratio = 0.5 / SL = 0.6 / TP = 1 / Period = 8

// USD/JPY : ratio = 0.5 / SL = 1 / TP = 0.8 / Period = 12

ratio = 0.6

period = 8

// HORAIRES

startTime = 210000

endTime = 231500

exitLongTime = 210000

exitShortTime = 80000

// BOUGIE REFERENCE à StartTime

if time = startTime THEN

amplitude = highest[Period](high) - lowest[Period](low)

ouverture = close

endif

// LONGS & SHORTS : every day except Fridays

// entre StartTime et EndTime

if time >= startTime and time <= endTime and dayOfWeek <> 5 then

buy n shares at ouverture - amplitude*ratio limit

sellshort n shares at ouverture + amplitude*ratio limit

endif

// Stop Loss & Take Profit

// Stop e target

SET STOP PLOSS 25

SET TARGET PPROFIT 13 //395

//

//trailing stop function

//************************************************************************

// trailing stop function

trailingstart = 19 //10 trailing will start @trailinstart points profit

trailingstep = 24 //5 trailing step to move the "stoploss"

//

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND HIGH-tradeprice(1)>=trailingstart*pipsize THEN //close --> HIGH

newSL = tradeprice(1)+trailingstep*pipsize

// new coding

IF newSL > close THEN //if current closing price is < new SL then exit IMMEDIATELY!

SELL AT newSL LIMIT

ENDIF

// end new coding

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

// new coding

IF newSL > close THEN //if current closing price is < new SL then exit IMMEDIATELY!

SELL AT newSL LIMIT

ENDIF

// end new coding

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-LOW>=trailingstart*pipsize THEN //close --> LOW

newSL = tradeprice(1)-trailingstep*pipsize

// new coding

IF newSL < close THEN //if current closing price is > new SL then exit IMMEDIATELY!

EXITSHORT AT newSL LIMIT

ENDIF

// end new coding

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

// new coding

IF newSL < close THEN //if current closing price is > new SL then exit IMMEDIATELY

EXITSHORT AT MARKET

ENDIF

// end new coding

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT MARKET

ENDIF

// Exit Time

if time = exitLongTime then

sell at market

endif

if time = exitShortTime then

exitshort at market

endif