ALE

ALEModerator

Master

Yes of course are Numbers, but i find good result using close bias..

as you know, close level it is a foundamental level in trading letterature … not else

ALEModerator

Master

About typicalprice maybe that i have had test .. i dont remember

as you know there’s infinite bias to entry in the market, the different could be to manage exit

ALEModerator

Master

In prt using ig data, it’s important to avoid strategy depending in tick data.

I tried a quick test of TypicalPrice instead of close but did not see an improvement.

I agree that entry is generally very easy but getting out with a profit is the tough bit!

Why do you say that IG and strategies that use tick data are a problem? Are you saying that backtest results that get in and out on the same candle cannot be relied upon?

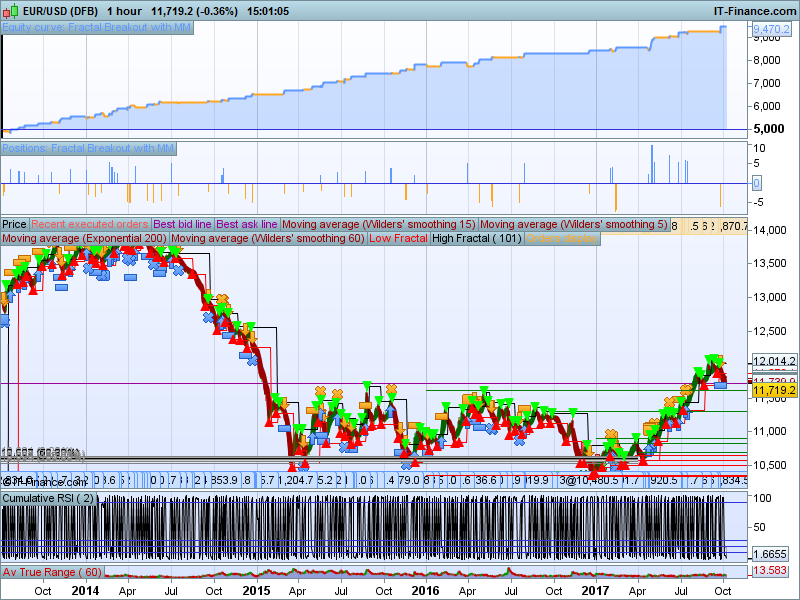

On a separate note…. I don’t generally like adding extra filters to a working strategy but I have recently began to like the Cumulative RSI[2] so I added it as a filter to your Fractal Breakout strategy and first impressions were that it seemed to give a higher success rate at the price of less bets obviously. The higher the CumRSI2 for a BUY the better the odds of a win were and the reverse for a SELL so I even tried increasing or reducing the bet size depending upon the CumRSI2 level at the time of entry. Seemed to work quite well. Just an idea that you might want to play with.

Vonasi: Could you upload that code? I tried to add RSI to a strategy but couldn’t get it to work…

I’m playing around with it at the moment but will try to post something when I’ve tidied it up a bit!

//EURUSD(-) - IG MARKET

// TIME FRAME 1H

// PROBACKTEST TICK by TICK - 200.000 bars

// SPREAD 0.6 PIP

// ALE - KASPER - modified by Vonasi

DEFPARAM CumulateOrders = false

CP = 101 //Fractal Period

Ave = 7 //AverageTrueRange Period

TGLMult = 0.6 //ATR multipier for TGL

STPMult = 1.8 //ATR multiplier for StopLoss

AddOn = 1.1 //Added to STPMult for TakeProfit

//KASPER CODE OF REINVESTMENT

Reinvest=1

if reinvest then

Capital = 5000

Risk = 1//0.1//in % pr position

StopLoss = AverageTrueRange[Ave] * STPMult

TakeProfit = AverageTrueRange[Ave] * STPMult + AddOn

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = (equity*(Risk/100))

MAXpositionsize=Capital

MINpositionsize=1

Positionsize= MAX(MINpositionsize,MIN(MAXpositionsize,abs(((maxrisk/StopLoss)))))

else

Positionsize=1

StopLoss = Stoploss

Endif

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

if Close[cp] >= highest[2*cp+1](Close) then

LH = 1

else

LH = 0

endif

if Close[cp] <= lowest[2*cp+1](Close) then

LL = -1

else

LL = 0

endif

if LH = 1 then

HIL = Close[cp]

endif

if LL = -1 then

LOL = Close[cp]

endif

//CumulativeRSI2

RSI2 = (SUMMATION[2](RSI[2](Close)))/2

RSILow = RSI2 < 20

RSIHigh = RSI2 > 80

//LONG and SHORT CONDITIONS

if (time >=100000 and time < 230000) then

C1 = (close CROSSES OVER HIL)

D1 = (close CROSSES UNDER LOL)

IF c1 and NOT ShortOnMarket and RSIHigh THEN

PositionMultiple = (RSI2/100) + 1//Increase PositionSize depending on CumRSI2 level

PositionSize = PositionSize * PositionMultiple

PositionSize = Round(PositionSize * 100)

PositionSize = PositionSize / 100

BUY positionsize CONTRACT AT MARKET

ENDIF

IF D1 and NOT LongOnMarket and RSILow THEN

PositionMultiple = ((100-RSI2)/100) + 1//Increase PositionSize depending on CumRSI2 level

PositionSize = PositionSize * PositionMultiple

PositionSize = Round(PositionSize * 100)

PositionSize = PositionSize / 100

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

ENDIF

//TRAILING STOP

TGL = AverageTrueRange[Ave] * TGLMult

TGS = TGL

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PriceExit = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PriceExit = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PriceExit = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PriceExit>0 then

EXITSHORT AT PriceExit STOP

SELL AT PriceExit STOP

ENDIF

// DONCHIAN STOP

DC=20

e= Highest[DC](high)

f=Lowest[DC](low)

if longonmarket then

laststop = f[1]

endif

if shortonmarket then

laststop = e[1]

endif

if onmarket then

sell at laststop stop

exitshort at laststop stop

endif

set target pprofit TakeProfit

set stop loss stoploss*pointsize

OK here you go ozz87 – please be gentle with me as this is the first code I’ve posted. I’ve modified ALE’s code with a Cumulative RSI2 filter. Long trades are entered only if CumRSI2 is above a certain level. The higher the level the better the win rate (testing has shown) – but also obviously fewer bets due to the added filter. Short trades are the opposite and only entered if CumRSI2 is below a certain level. The PositionSize is multiplied by a factor depending upon how high or low the CumRSI2 is – so the higher the probability of a win the higher the stake. I have also attempted to base the StopLoss and TakeProfit and Trailing StopLoss on Average True Range but this is a work in progress! I tested it with a 0.9 spread rather than the 0.6 ALE used.

Vonasi: Thanks! Trying to find what’s wrong when i try backtest, I don’t get any results (eur/usd mini, 1 hour)

ALEModerator

Master

Thanks Vonasi, Good Idea.

I want to explain my opinion:

I think that we don’t look for a multiplied position to increase our profit, but to find other forex pair.

Cumrsi could be a good filter, but I’d try to optimize period instead of 2 , because on 1 h time frame it’s too fast, usually it’s very good on dailytime frame.

About Stop loss and Take profit: Atr it’s very volatily so I can suggest to average it.

We coul’d try to add an long average to filter position.

Not sure why that would be ozz87. I’m on an IG PRT account – are you? Maybe something to do with CONTRACT. I’m no expert! – maybe someone else can help?

ALEModerator

Master

About IG tick data, the problem is not the same candle, but tick data. Many test with low time frame show that date tick of probacktest are different on real market. For example in backtest you touch a trailing stop and close position, while in real it not happend, etc etc… To survive with this problem it’s necessary to have a strategy that doesn’t depend from tick data .

ALEModerator

Master

@ ozz what’s the problem?

ALEModerator

Master

I notice that Vonasi is using a different market ? It’s correct?

ALE – I’m not a fan of MA filtering – way too much lag and confusion when price is near the MA. The Cumulative RSI2 is fast and that is what I like about it. Having said that I have not tried stretching the period out but on every other strategy I have tried that on I have have always found 2 to be the best period.

I tested the strategy with and without the positionsize multiplying and it was a definite improvement to profits with it. I maybe need to scale the sizing back as the starting bet size is too big the way it is at the moment. If it increases profitability I think it should stay and then move on to other possible pairs.

On a separate note I have tried coding a similar strategy that looks for bounces/tests of fractal levels rather than breakout but breakout seems more consistent and profitable so far.

ALEModerator

Master

Very good

a suggest ma because i’m using it with cumrsi2 in Other daily strategies.. but with 1 h tf I dont know, and i’m agre with you.

as soon as possibile i start ti improve fravtal strategy..