Hello Guys,

Paul, thanks for posting this code. I really like it.

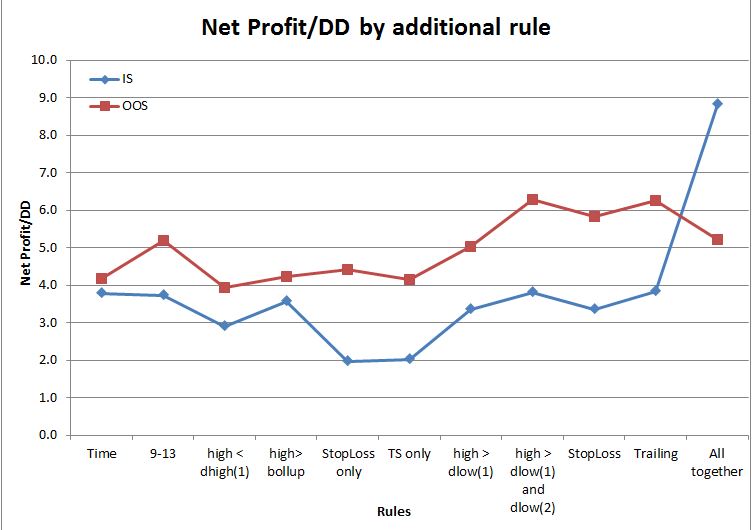

Overall I did a little Analysis and the conditions C1, C2 and C5 are not improving the performance significantly. As Jebus89 already mentioned the strategy is already very profitable by just applying the time condition. In my opinion only rule c3 and C4 adding a substantial surplus which improves the Netprofit/DD ratio.

See the chart attached.

Overall I think it is important not to add too many rules and rise the level of complexity artificially to tweak it until the maximum.

C2 I agree with you. C1 is important. C5 improves a bit.

I tested also on EURJPY with a few changes in the parameters. Profit factor 1.55, so a little too low so far in order for me to test it live.

Using the same time in eurJPY as well? I thought i tried that without good results?

Im running this live using 1 contract just to see what happens, the max DD is so low so its no worries for my account.

Im using all the C rules, but as mentioned by me and other i think im going to review them a bit more and remove the not important ones as stated in earlier comment.

Condition C5 lowers the number of trades and drawdown. Without the condition drawdown is still acceptable. It could be interessant to test other filters that condition C5.

Overall I did a little Analysis

Very interesting, thank you! Not seen this done before.

- Did it take long?

- Is it an analysis you do on other Systems or a first time one-off?

- If not a first time … are results generally similar to findings on the link above?

I’m trying to test the strategy with long trades. The results aren’t as good as short trades. Trading hours between 18h and 20h (UTC+2) improves a bit the strategy and maintain a smoothed equity curve. I’ve only made a test with 100k data. Do you still have an improvement with 200k data?

DEFPARAM CUMULATEORDERS = false

CtimeAchat = time >= 180000 AND time < 200000

//LONGS

if time=200000 then

level=low[1]

endif

c1= close > dopen(0)

c2= low > dlow(1)

c3= level < dhigh(1)

c4= level < dhigh(2)

bu= BollingerUp[20](close)

bd= BollingerDown[20](close)

ba= (bu+bd)/2

c5= ba>ba[1] or low < bu

if CtimeAchat and c1 and c2 and c3 and c4 and c5 THEN

buy 1 contract at market

endif

if LongOnMarket and time=200000 THEN

sell at market

endif

set stop %loss 0.5

Sometimes I will have an optimized variable such as ‘c’ which is used purely to select a set of conditions to use in the back test. This way it is easy to test every possible combination side by side to see which ones have the most benefit. With a lot of conditions it can result in a lot of options but once you have the code then it is a simple thing just to change the c1, c2, c3 conditions to whatever your latest idea uses and paste it into your new strategy.

Something like:

//c = 0 //optimized variable

c1 = open > close

c2 = open > high[1]

c3 = open < low[1]

if c = 1 then

condition = c1 and c2 and c3

endif

if c = 2 then

condition = c1 and c2

endif

if c = 3 then

condition = c1 and c3

endif

if c = 4 then

condition = c2 and c3

endif

if condition then

buy 1 contract at market

endif

I started the algo live now but only 1 contract.

More fun to run it live than on demo.

DD with 1 contract is only 245 dollar..

Im running this live as well with 1 contract barney. lets goo

select a set of conditions to use in the back test.

I added above code to here Snippet Link Library

Running it live too since yesterday. Watching it a bit, I think working on the 5min instead of the 15min (or MTF), and working with limit orders instead of at the market may improve the results. Will try

I’ve got 2 versions (Paul and Paul / Stefou) running on Demo Fwd Test. but not had a trade yesterday or today.

Anybody had trades yesterday or today?

yes me. both days. a small profit and a small loss

Paul

PaulParticipant

Master

The breakeven is a pain to quickly test 200k bars.

An alternative can be to close the position when the Bollingerbands distance are getting smaller.

bu= BollingerUp[20](close)

bd= BollingerDown[20](close)

ba= (bu+bd)/2

br= (bu-bd)

if shortonmarket and time=141500 and positionperf(0)*100<0.3 then

exitshort at market

else

if time> 141500 and br<br[1] and br[1]<br[2] and br[2]<br[3] and br[3]<br[4] then

exitshort at market

endif

endif

Found this quick, perhaps there’s room to improve without a breakeven!

Small one, lower the entrycriteria for the bollingerbands, and use previous bu, instead of the current

c5= ba<ba[1] or high > bu[1]

Hi Grahal,

- It can be quick if one prepared everything on Excel already. There you just need the final result from each added condition

- I just read it in the book (trading systems a new approach to system optimisattion from Jaekle/Tomasini) Was the first time I did it and will continue do to so for future optimisations

Overall I can only recommend to read that book for systematic trading, especially how to optimise

Same is true for the book “Kevin Davey – Building Algorithmic Trading Systems”