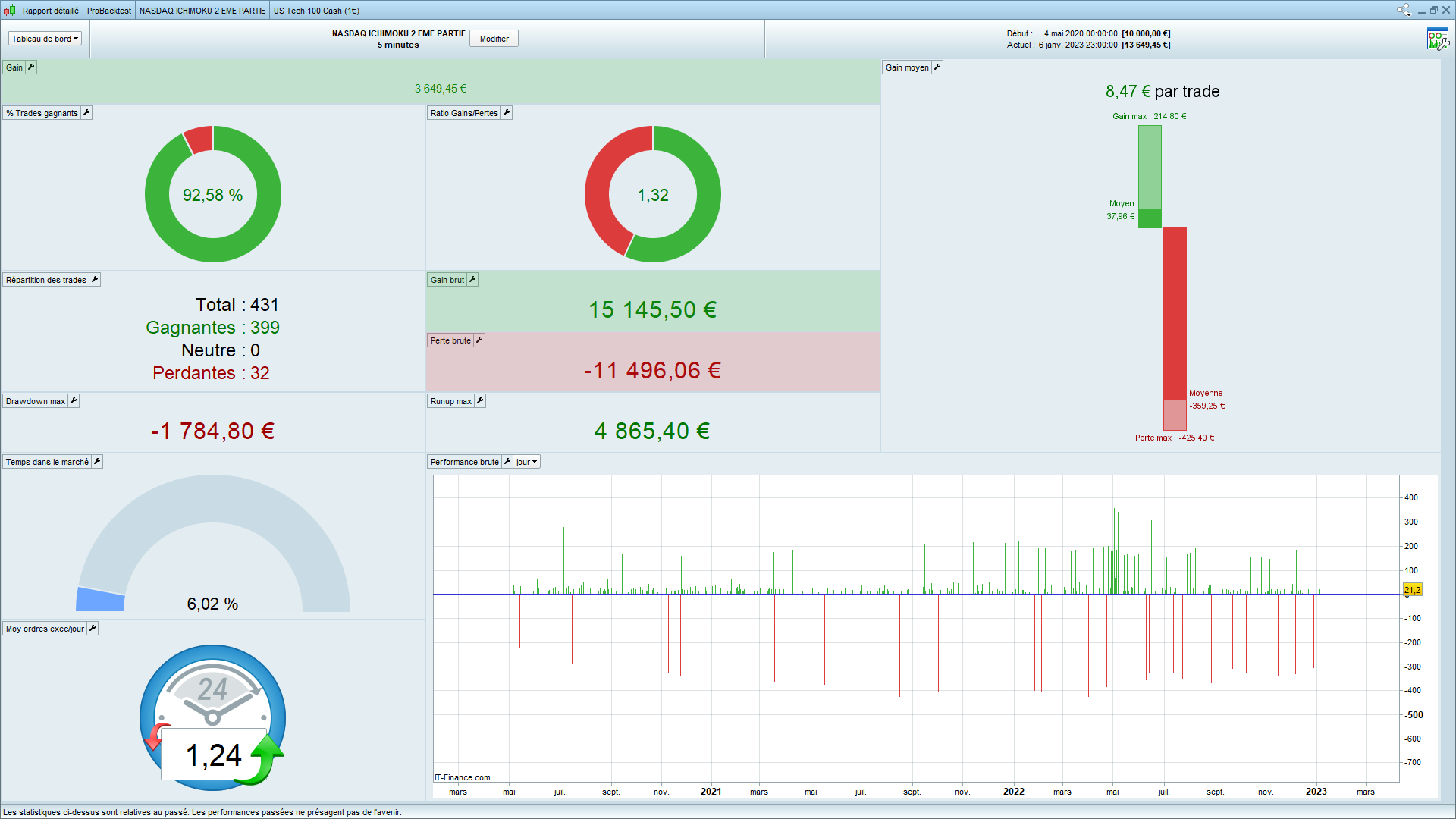

voici le second avec c3

// Définition des paramètres du code

DEFPARAM CumulateOrders = false // pas de cumul de positions

DEFPARAM Preloadbars = 1000000

capital= 50000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 150000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 223000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = SenkouSpanA[9,26,52]

c1 = (close CROSSES OVER indicator1)

indicator2 = SenkouSpanB[9,26,52]

c2 = (close CROSSES OVER indicator2)

c3 = (close > DOpen(0)[1])

IF (c1 AND c2 and c3) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 2 CONTRACT AT MARKET

partial=0

ENDIF

// sortie partielle

if longonmarket and positionperf>1.7/100 and partial=0 then

sell countofposition/9.7 contract at market

partial = 1

endif

if summation[1800](longonmarket)=1800 then

sell at market

endif

if summation[1000](shortonmarket)=1000 then

exitshort at market

endif

// Stops et objectifs

set stop %loss 1.8

set target %profit 1.73

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 65 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

et fifi743 voici un autre avec d’autres paramètre modifié notamment trailstar , le take profit

// Définition des paramètres du code

DEFPARAM CumulateOrders = false // pas de cumul de positions

DEFPARAM Preloadbars = 200000

capital= 50000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 150000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 223000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = SenkouSpanA[9,26,52]

c1 = (close CROSSES OVER indicator1)

indicator2 = SenkouSpanB[9,26,52]

c2 = (close CROSSES OVER indicator2)

c3 = (close > DOpen(0)[1])

IF (c1 AND c2 )AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and tally < maxTrades THEN

BUY 2 CONTRACT AT MARKET

partiel=0

ENDIF

// sortie partielle

if longonmarket and positionperf>0.42/100 and partial=0 then

sell countofposition/9.1 contract at market

partial = 1

endif

//---------------------------------------------------------------------------------------------------------------

once maxTrades = 5 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or ((not onMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or (longOnMarket and ShortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//--------------------------------------------------------------

//---------------------------------------------------------------------------------------------------------------

//Max-Orders per Day

once maxOrdersL = 1 //long

once maxOrdersS = 1 //short

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//--------------------------------------------------------------

// Stops et objectifs

set stop %loss 1.40

set target %profit 0.668

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 5.2 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 1 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

au passage si tu peux partager les tiens et autres avec des performances sur unité de temps plus courtes aussi. Mais celui en 15 et 30 minutes tu peux partager?

les algos sont avec le spread a 1 je précise

Pour eur/usd pour info j’ai réglé take profit à 0.20 et trailstart à 3.0 apres si tu augmentes des pertes apparaissent. exemple 0.22

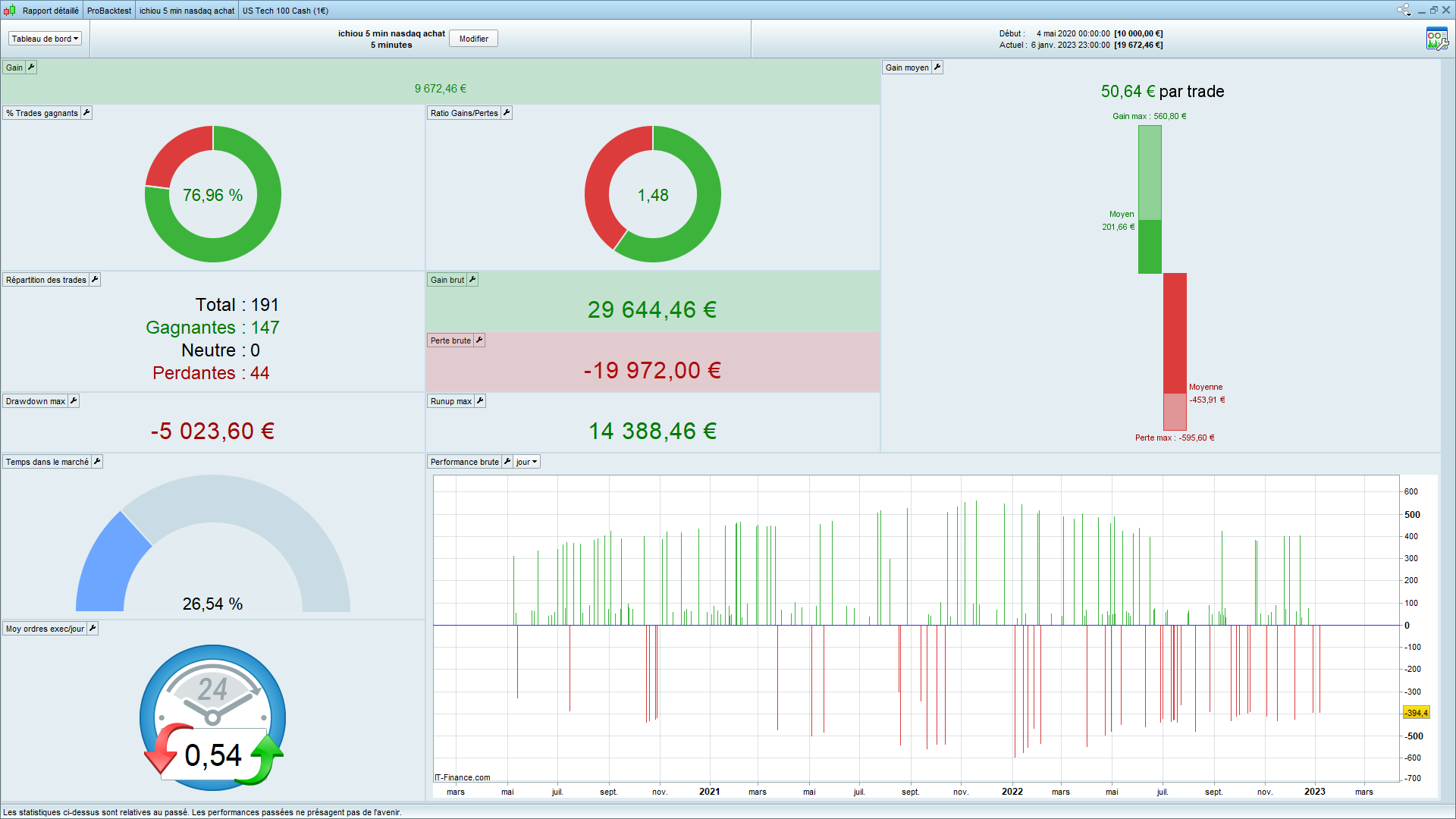

bonjour nasdaq en 5 mnutes posté

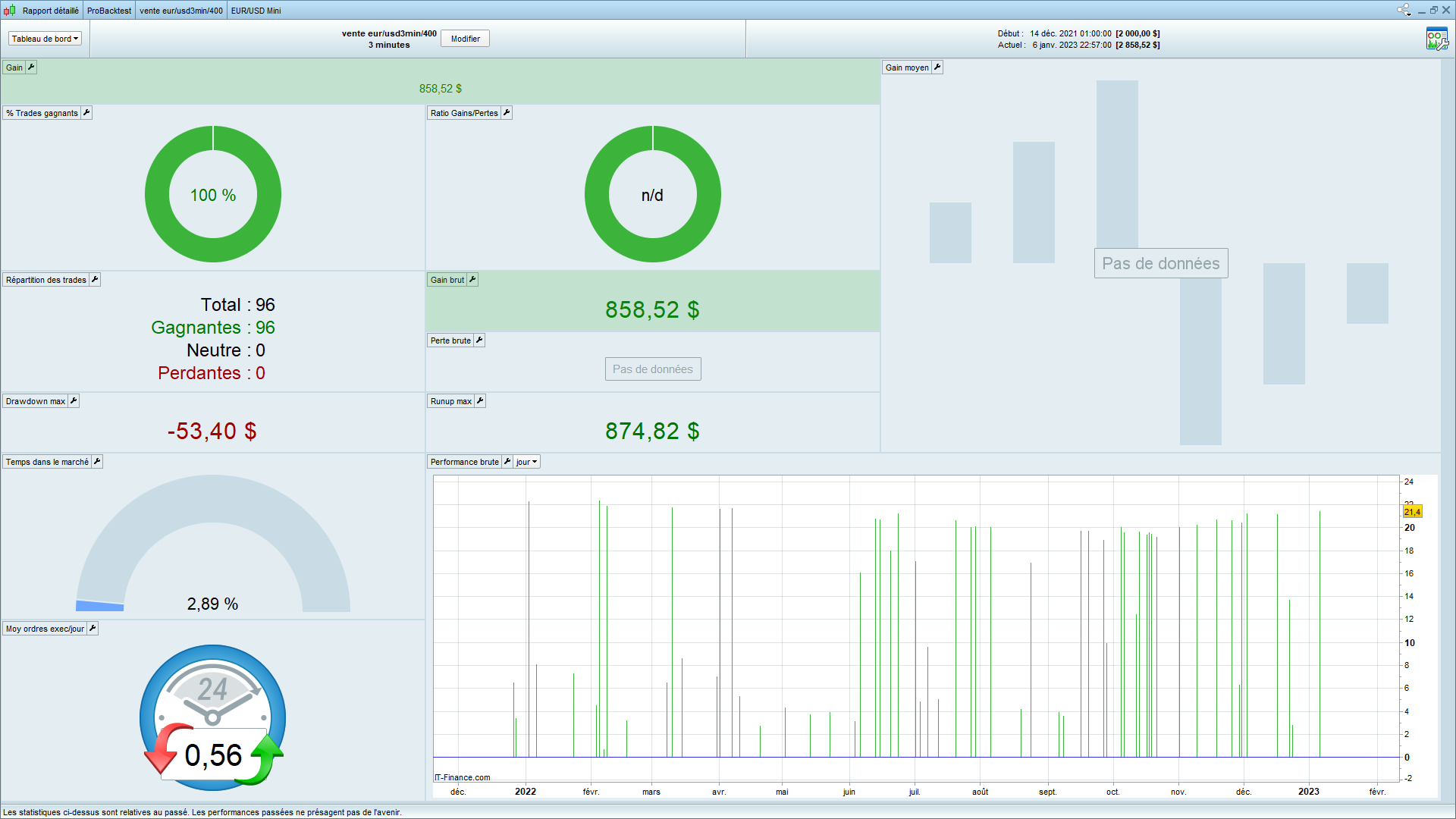

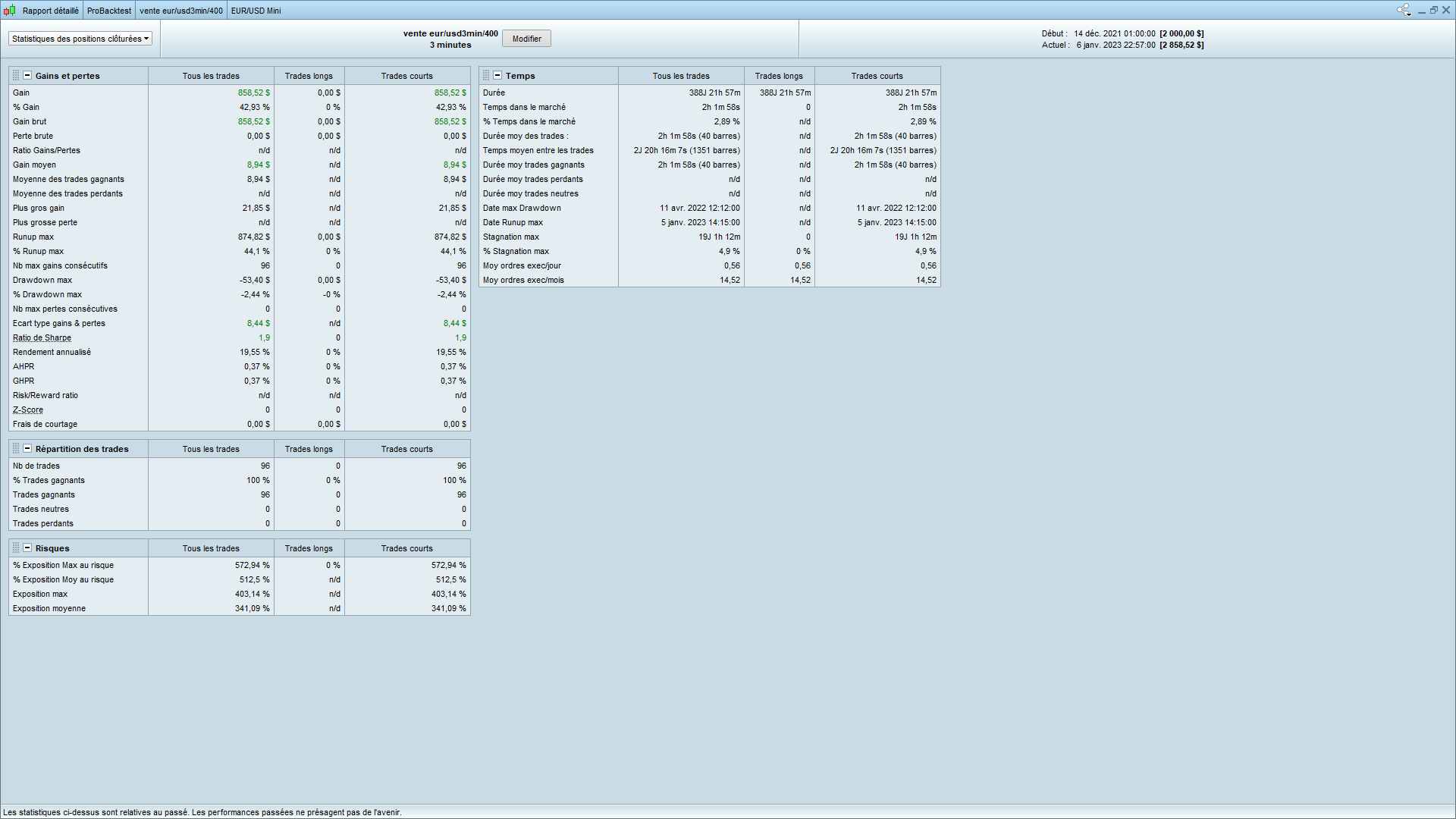

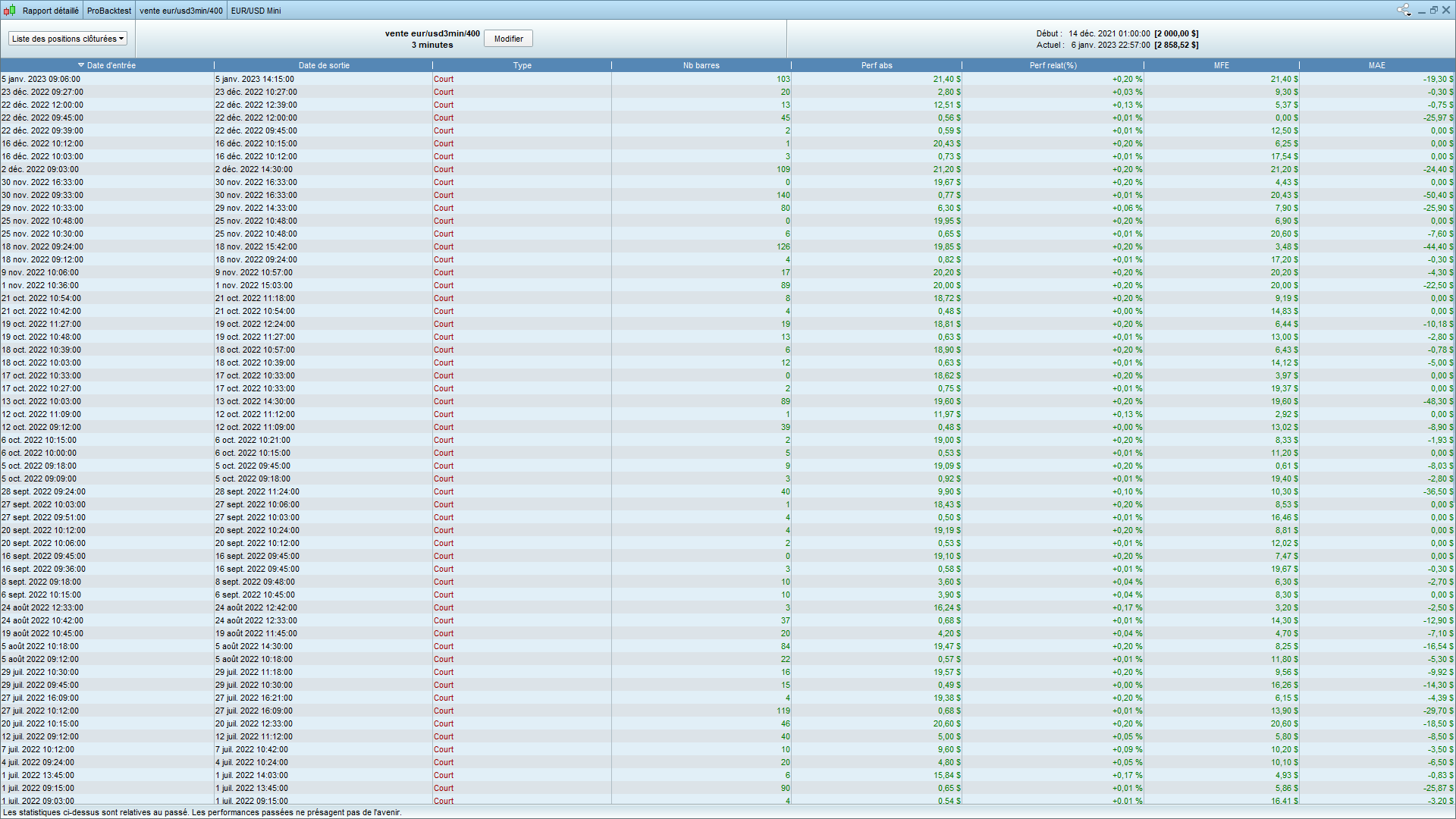

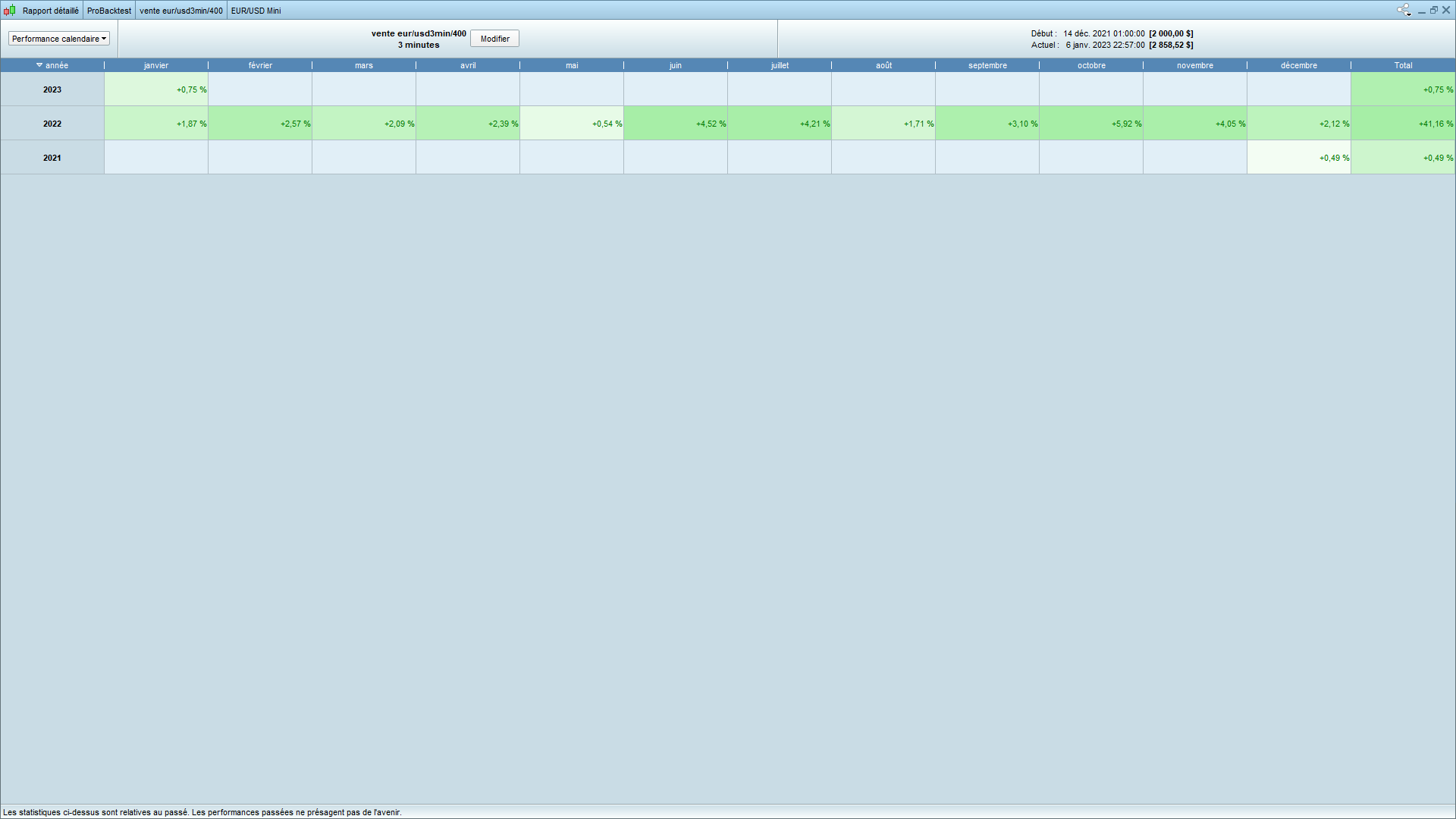

eur/usd time 3 .

avec modification de fiffi743.

// Définition des paramètres du code

DEFPARAM CumulateOrders = False

DEFPARAM PRELOADBARS = 2000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 090000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 110000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position en vente à découvert

// Conditions pour ouvrir une position en vente à découvert

indicator1 = SenkouSpanB[9,26,52]

indicator2 = SenkouSpanA[9,26,52]

c1 = (close CROSSES UNDER indicator1)

c2 = (close CROSSES UNDER indicator2)

indicator3 = Average[400](close)

c3 = (close > indicator3)

IF (c1 AND c2 and (c3 or (high[3]<high[1]and low[3]<low[1] )))AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and tally < maxTrades THEN

sellshort 1 CONTRACT AT MArket

partial=0

endif

// sortie partielle

if shortonmarket and positionperf>0.10/100 and partial=0 then

exitshort 0.05 contract at market

partial = 1

endif

once maxTrades = 10 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or ((not onMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or (longOnMarket and ShortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//------------------------------------------------------------------------------------------------------------------------

//---------------------------------------------------------------------------------------------------------------

//Max-Orders per Day

once maxOrdersL = 1 //long

once maxOrdersS = 1 //short

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//------------------------------------------------------------------------------------------------------------------------

// Stops et objectifs

set stop %loss 0.58

set target %profit 0.20

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 3.0 //30 Start trailing profits from this 1.74

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Qui pourrait le faire dans le sens de l’achat?

Wonderful.

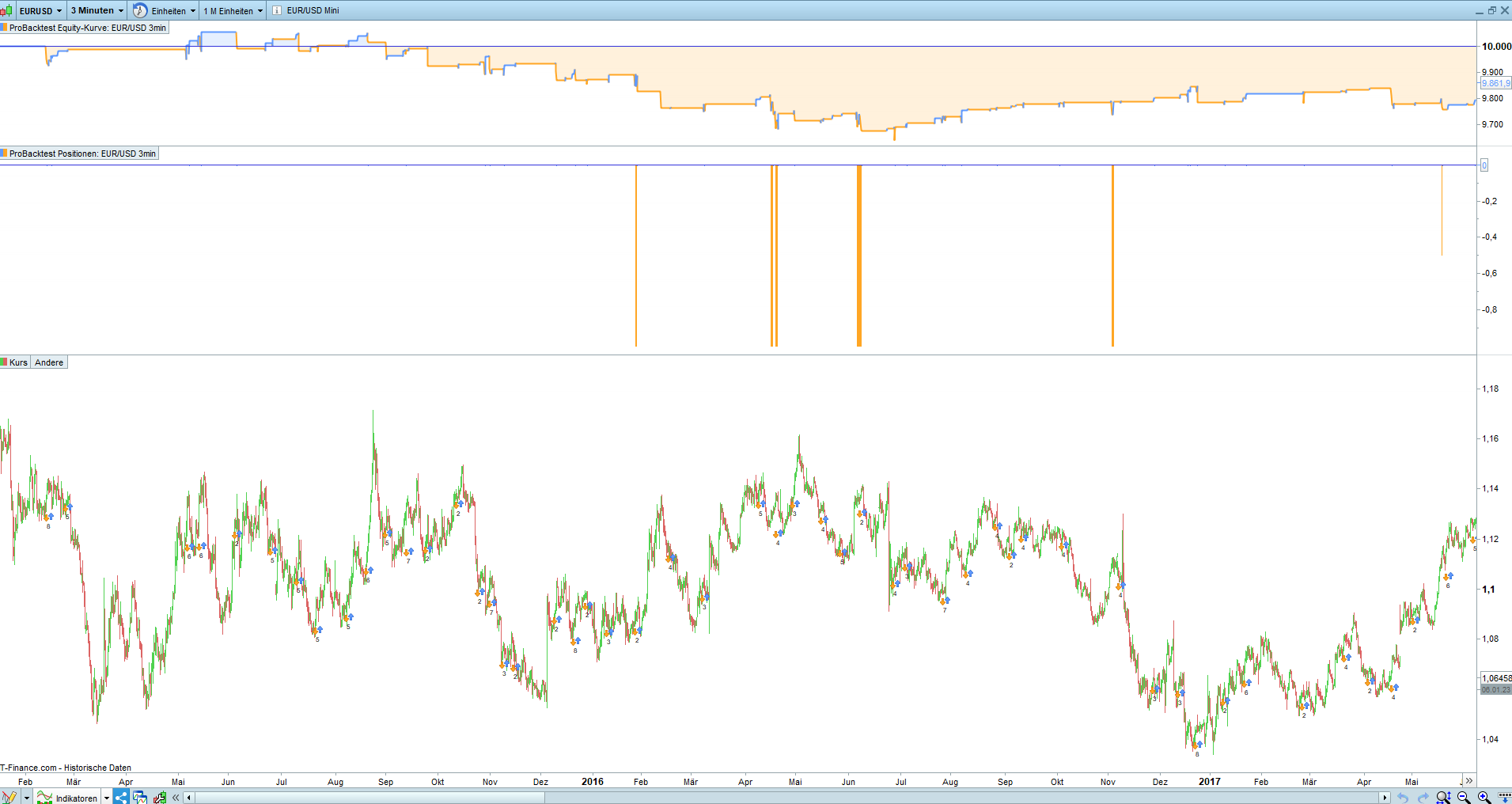

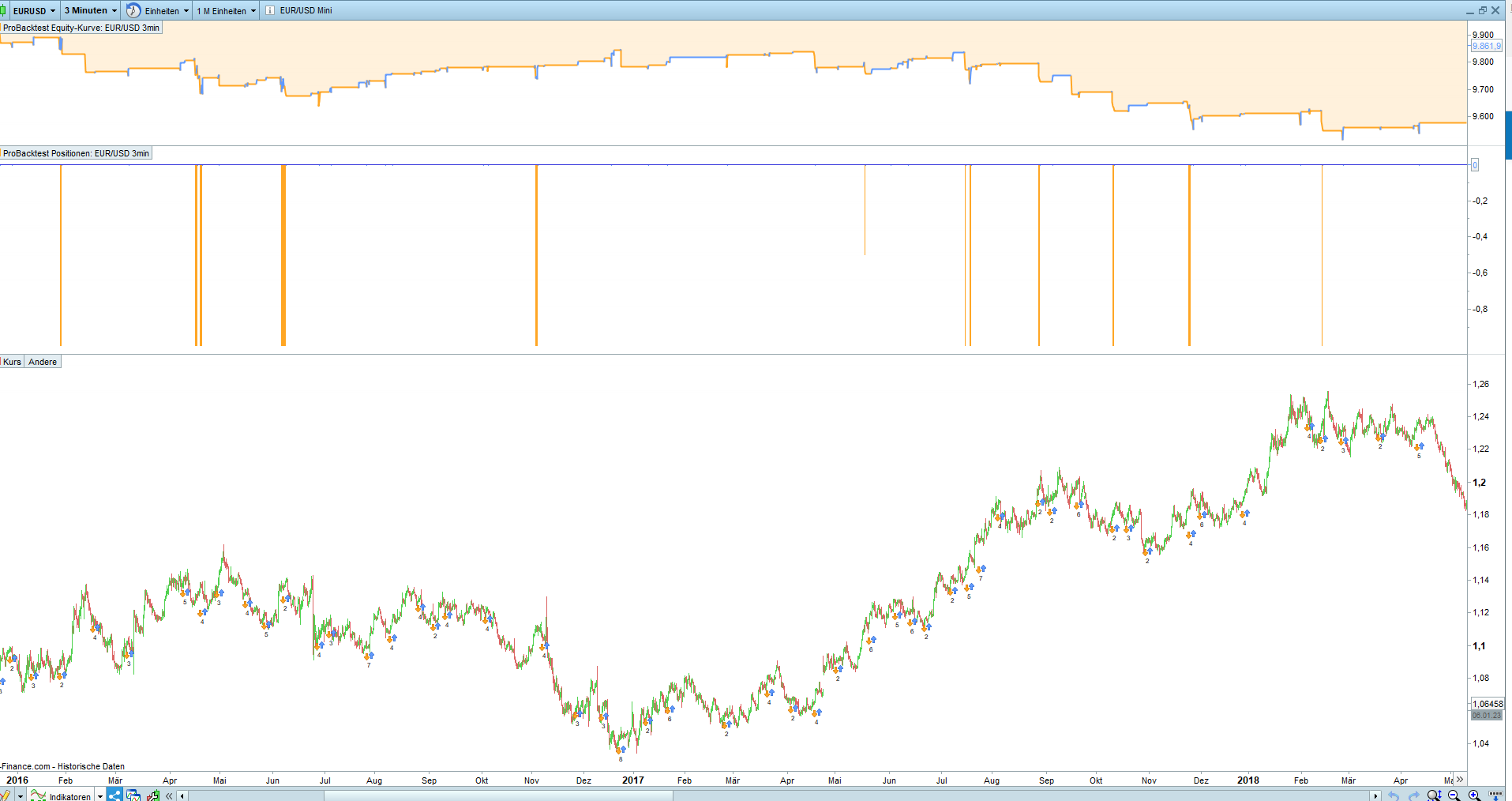

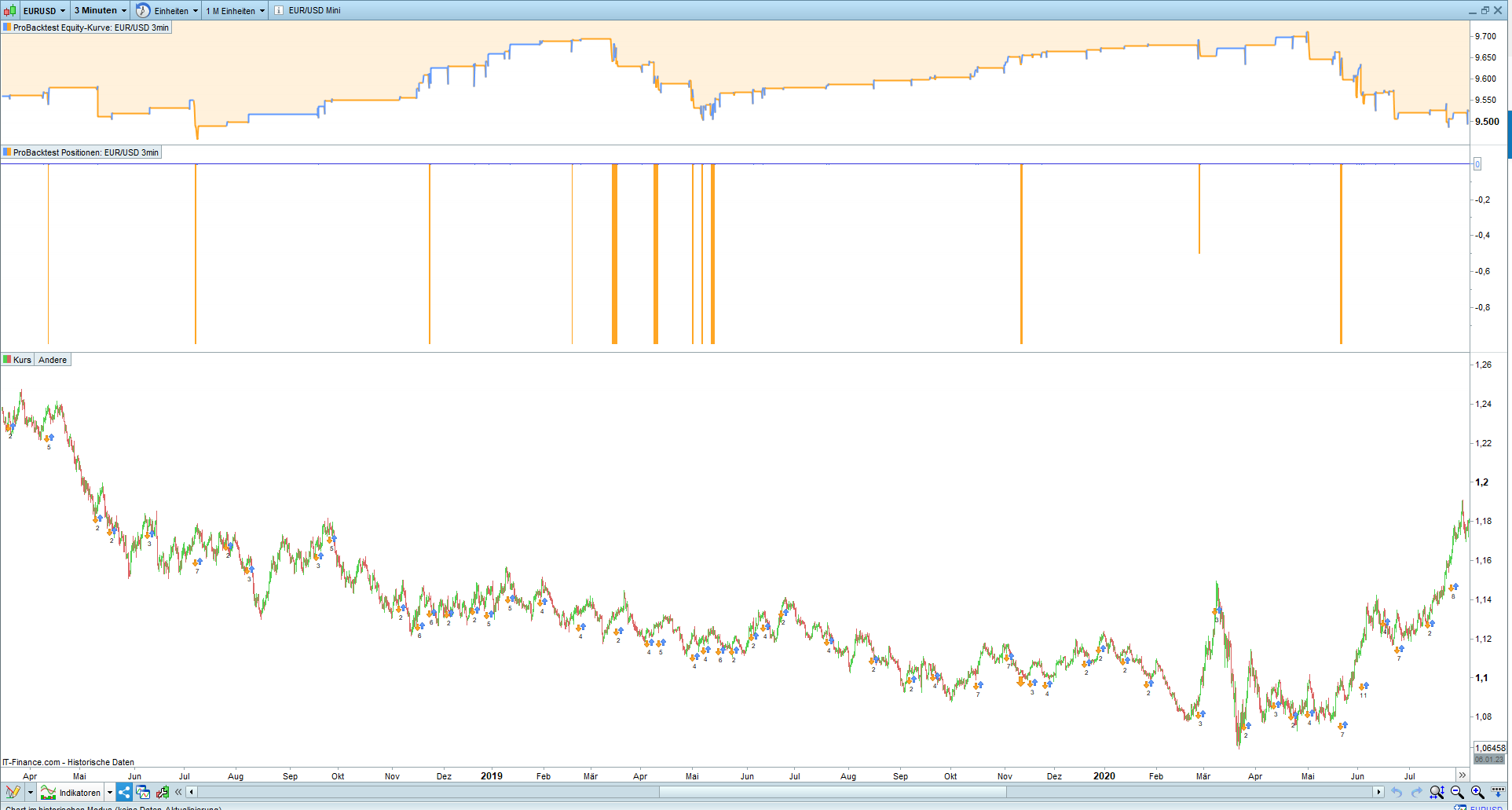

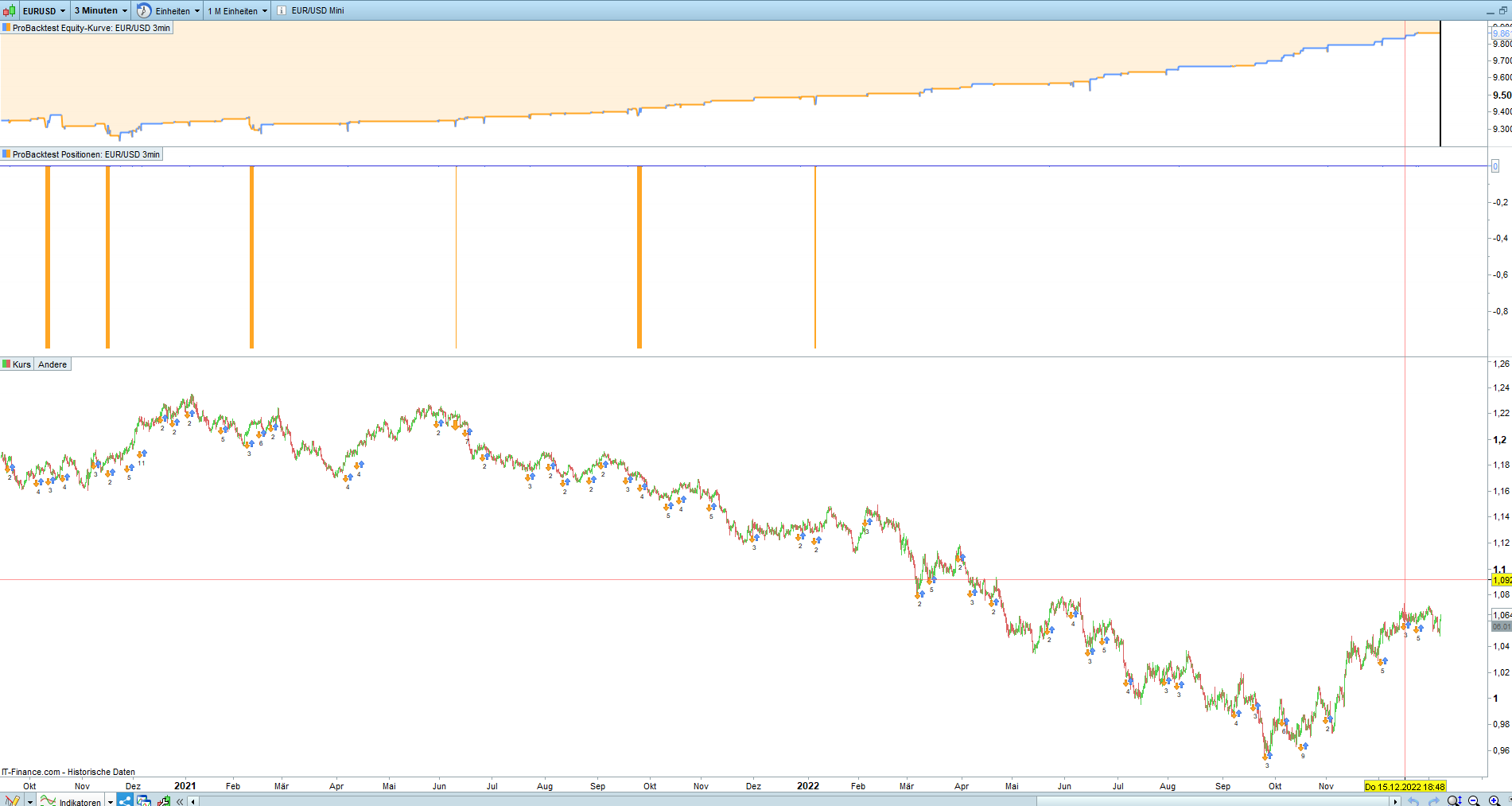

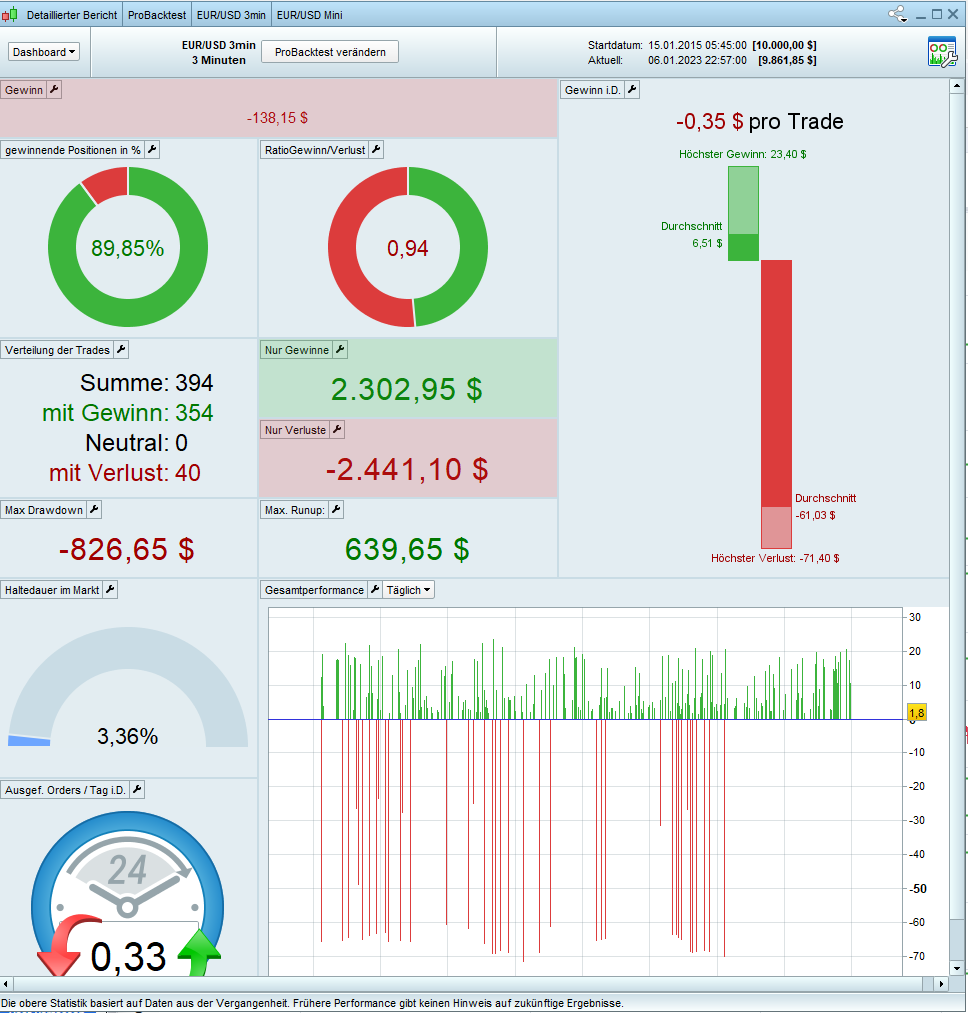

Enclosed the backtest 1Mio units

Enclosed the itf-file with which was tested

tested was the first code which was published, quasi without mods

Ci-joint le fichier itf avec lequel le code a été testé joint le tableau de bord 1 Mio unités

Salut fiffi,

je te dérange 2 minutes , je suis intéressé par tes algo si tu veux bien partager et si tu as fait attention j’ai partagé quelques algo peux tu travailler dessus afin d’améliorer ?

Dans l’attente de te lire.

bonjour,

OK pour l’échange tu me donne ta Ferrari et je te donne ma vielle 2 CV ,elle roule mais elle est sur cale pour l’instant.

Bonjour fifi743 ,

J’ai un algo a tester , voila la stratégie serait quand l’algo eur/usd se met en route je voudrais pouvoir en faire un autre qui puisse démarrer avec les parametres de fibonacci c’est a dire quand leurusd ouvre une position et qu’on prend le dernier plus haut en timeframe 1h ou 4h ou 15 min par exemple et que le cours retrace les 50 ou 60% par rapport a fibonacci , je voudrais qu’il ouvre une position à la vente et que le take profit soit calquer sur celui de l’eurusd et le stop égalment.

Bonjour JohnScher,

je viens vers toi pour une élaborer une technique que je voudrais paramétrer.

Je voudrais en prenant l’algo eur/usd 3 minutes insérer ou faire un autre algo en parallèle à celui la qui utilise fibonacci.

Je voudrais que l’algo démarre quand il retrace par exemple les 50% dans l’unité de temps soit 5ou 15 ou 1h par rapport au trade prix par l’algo eur/usd.

Dans l’attente de te lire

BONJOUR

j’ai remarqué que les pertes se font en tendance haussière … et à l’inverse , les profits se font dans la tendance contraire.

A bon entendeurs salut!