Bard

BardParticipant

Master

Hi there,

I was wondering if anyone can explain why since the upgrades of PRT last year I have the John Ehler’s MESA series of indicators that constantly reload/recalculates?

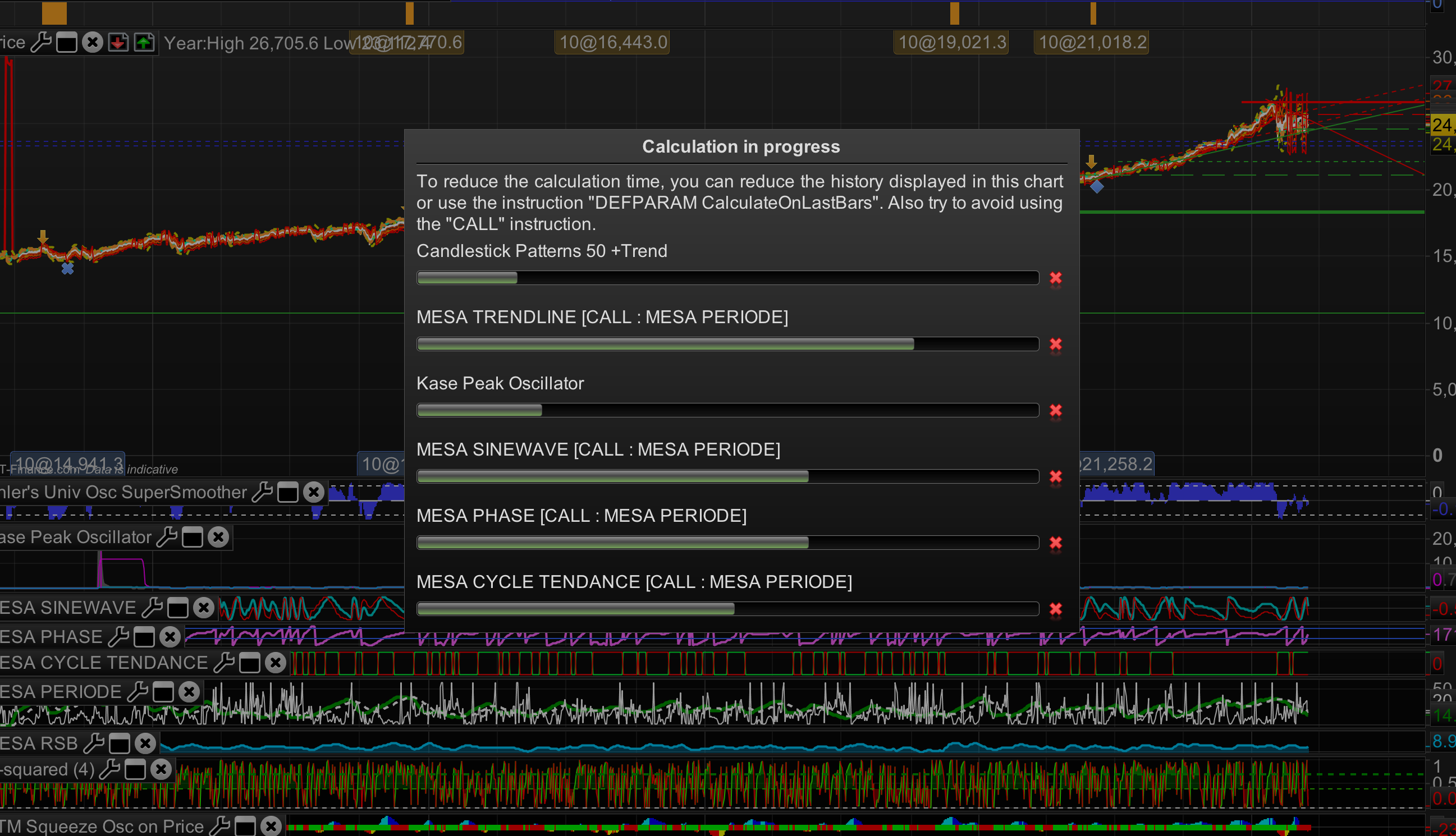

This happened the other day on the Hour Chart of the Dow Jones charts after setting units from 1,000 to 10,000? (On 1,000 units the chart does not reload/recalculate)

If I recall correctly this was pinpointed by PRT Tech last year as being an issue with my 2.4ghz MacBook 17” 16GB although it never redrew the charts every couple of minutes when using the v10.2 (or it might have been v10.1). This only happened after the PRT upgrade. (Otherwise this PRT platform just keeps getting better and better).

I now have the MacBook 15” 3.1ghz with 4.1ghz Turbo Boost, 16 GB but it’s still redrawing on longer unit settings (which, just to clarify it never did before updates to PRT)?

Any ideas?

Thanks very much,

Bard

Hi Bard,

I advise to send a technical report by following these instructions:

– As soon as you encounter the issue, go to the “Help” menu on the ProRealTime toolbar.

– Click on “Technical support”

– Select “Code”

– Giving as many details as possible, explain the issue you are having in the text box and mention the name of the code you are referring to.

– To receive in depth assistance, it is necessary to analyze the code itself which is encrypted on our servers. To allow our technicians temporary access, please check the box marked “I authorize the decryption of the codes…”

– Click “Send report”

This will send a report containing technical information concerning your platform, which will allow the technical team to run a diagnostic analysis of the issue you have come across.

Many thanks in advance,

Ulrike

BardParticipant

Master

Thanks Ulrike

I have already done this via PRT help window in March 2018.

I got a reply from IG Index in early March saying that IT-Finance does not support custom indicators and that I should address the problem to the PRT Forum, which I did above. I was informed that it was a glitch with the PRT software by IG Index support.

I have just resubmitted my support request via the PRT help window again.

Fingers crossed that PRT can finally fix the issue as it makes using the charts with MESA impossible to use with the constant re-load issue.

Cheers

Bard

Hi Bard,

could you please send your IG account number to “contact@prorealtime.com” including a link to this post, please?

I will then get in touch with the technical team in order to see if I can get any further information.

Best,

Ulrike

BardParticipant

Master

Hi Ulrike,

Have you had any feedback from PRT?

I replied by email to contact@prorealtime.com on the 16th April with my account details.

Thanks

Bard

Hi Bard,

The ticket is taken care of by our programming team.

I hope to have a quick answer and will revert to you asap.

Best,

Ulrike

BardParticipant

Master

Hi Ulrike,

I was wondering if there had been any progress on this ticket?

I would like to be able to use the MESA charts with a longer look back than the minimum look back unit setting I’m currently having to use (because the charts re-load themselves over and over with longer units).

Thanks

Bard

Dear Bard,

Our technical team is still working on the issue.

We will come back to you you shortly.

Best regards,

BardParticipant

Master

Much appreciated Ingrid, it’d be great to get back to using MESA as an automated trading tool on the latest version of PRT.

Cheers

Bard

Dear Bard,

Our technical team confirms that the problem with the Ehler’s MESA indicators has been resolved. The last test on the DOW instrument in 4 hours timeframe and with 1 000 units did not show any recalculation.

If the situation occurs again, please send us a technical report following these instructions:

– As soon as you encounter the issue, go to the “Help” menu on the ProRealTime toolbar.

– Please assure that the window concerned by this issue is open.

– Click on “Technical support”

– Choose the category (e.g. “Data” for a spike)

– Select the concerned window in the drop-down menu.

– Giving as much detail as possible, explain the issue you are having in the text box.

– Click “Send report”

Best Regards,

BardParticipant

Master

Thank you very much Ingrid and PRT Techs, it’s really appreciated as this is much better. 1,000 units works well with the Daily chart as well as the 4 hour chart.

I still notice though that if the 4 hour chart is set to 10,000 units, I still get recalculating of the MESA RSB indicator every 15 seconds and if set to Daily, 10,000 units (for backtesting) all of the 5 MESA indicators still recalculate every 15 secs?

Cheers

Bard

Hello,

The problem is corrected. If it persists on your platform, I would thank you for sending us a new technical report.

Regards,

Carine

BardParticipant

Master

Thanks Carine, I have sent another report concerning using higher unit values like 10,000 of eg: Daily charts using MESA.

Dear Bard,

The ticket is taken care of by our programming team.

They will revert to you asap.

Best regards,