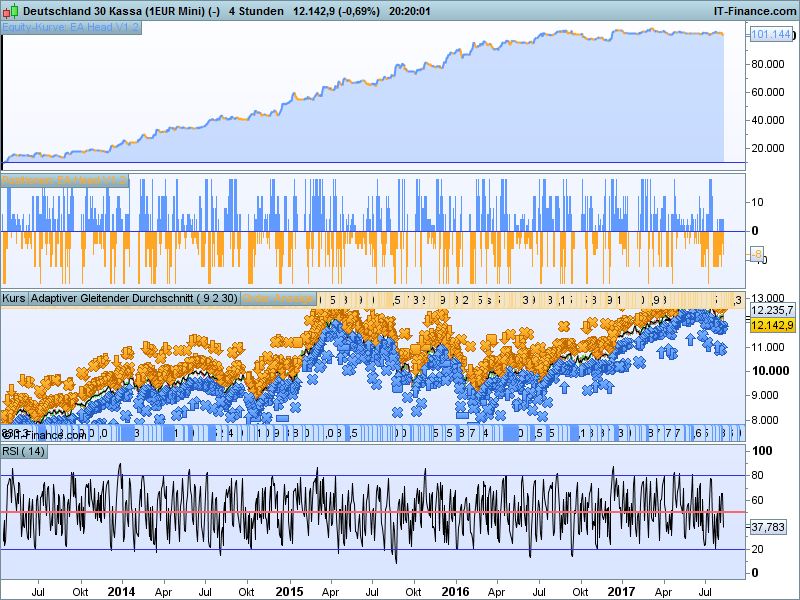

can´t believe backtest

works only on Dax 1 Euro

Spread 2 Euro, test from 01.01.2013

result ~ 350%

maybe comes little help too

//-------------------------------------------------------------------------

// Hauptcode : EA Head PF flat friday 210000

//-------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

// EA Head V.1

// EA Head H4 live PF

// created by JohnScher with help by ProRealCode

// Simple EMA-Strategy, timebased, mixed with some filters and a turbo by pathfinder-systems

// Dax 1 Euro Mini, 2 Points Spread, backtested 01.01.2013 to 29.07.2017 with positiv results

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

// defparam flatafter = 210000 is possibel, if used: winnings are smaller, risks are smaller

// Start Pathfinder-System

// Pathfinder-System not coded by me, code found at ProRealCode

// with define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 0 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 1 //0 risk(1)

ONCE June1 = 1 //1 ok 2

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 0 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = Day

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

Endif

// in original Pathfinder-Systems was used to find out correkt positionsize see following

// period = 14

// atr = AverageTrueRange[period]

// position = round(100/atr/2.1666)

// here i used

position = 1

// End Pathfinder-System

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

// Code Indicator NR7

// just info to integrated on your workstation

//-----------------------------------------------------------------------------------------------------------------------

// C1= Range<Range[1] and Range<Range[2] and Range<Range[3] and Range<Range[4] and Range<Range[5] and Range<Range[6] and Range<Range[7]

// RETURN C1

//-----------------------------------------------------------------------------------------------------------------------

// End Code Indicator Nr7

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

// Start Maincode

// Maincode : EA Head H4 Live PF

//-----------------------------------------------------------------------------------------------------------------------

// Filter

// not proofed for example : williams, atr, ....

// maybe the filters are not in the best settings, but it works in this way

//-------------------------------------------------------------------------

// Code Indicator : nr7

//C1= Range<Range[1] and Range<Range[2] and Range<Range[3] and Range<Range[4] and Range<Range[5] and Range<Range[6] and Range<Range[7]

//RETURN C1

//-------------------------------------------------------------------------

cx = CALL "NR7"

cx1 = cci[11]<80

cx2 = cci[21]>-90

cx3 = Momentum[6](close)>0

cx4 = ADX[11] >15

// cx5 = MoneyFlow[11](close)<0 (not used, maybe for optimizing

cx6 = TR(close) >25

cx7 = PVT(close)<1

cx8 = EaseOfMovement[14]<95

cx9 = SmoothedStochastic[14,3](close)<95

cx10 = PriceOscillator[5,25](close)<0.5

cx11 = LinearRegressionSlope[10](close)>-14

cx12 = AccumDistr(close)>-0.1

cx13 = Chandle [21](close)>-51

cx14 = STD[6](close)<99

//not used for example williams, rsi and so one to get out the tops on losses

// end filter

// timebase

TradingDayShort = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingDayLong = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingTimeShort = time = 090000 or time = 130000 or time = 170000

TradingtimeLong = time = 090000 or time = 130000 or time = 170000

// end timebase

// EMA Strategy with integrated Pathfinder-System, Filter and Timebase

// Short-Trade

IF TradingDayShort and TradingTimeShort Then

If not cx Then

If cx1 and cx4 and cx7 and cx8 and cx9 and cx10 and cx12 and cx14 Then

If ExponentialAverage [1] (close) < ExponentialAverage [2] (close) Then

sellshort position*saisonalPatternMultiplier CONTRACTS AT MARKET

Endif

Endif

Endif

ENDIF

// better to set (needed) : exitshort at end of regular weekly trading-hours

IF dayofweek = 5 and time = 210000 Then

ExitShort at market

ENDIF

// Long-Trade

IF TradingDayLong and TradingTimeLong Then

If cx2 and cx3 and cx6 and cx11 and cx13 Then

If ExponentialAverage [1] (close) > ExponentialAverage [8] (close) THEN

buy position*saisonalPatternMultiplier CONTRACT AT MARKET

Endif

Endif

ENDIF

// better to set (needed) : sell at end of regular weekly trading-hours

IF dayofweek = 5 and time = 210000 Then

sell at market

ENDIF

// can be optimezed

// if i test only long trades i find long: SL 0.75% and TP 1.5% more effectiv

// in test only short trades i find Short: SL 1.0% and TP 2.4% more effektiv

Set Stop %Loss 1

Set Target %Profit 2

// End EMA-Strategy, End Main-Code

//-----------------------------------------------------------------------------------------------------------------------

//not integrated any strategyprofit-maximize-strategy like re-invest-strategies, maybe some help to integrate this ?

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

//-----------------------------------------------------------------------------------------------------------------------

// kind regards JohnScher

DEar JHON

I think is necessary to have the NR7 detail code , isnt’it ?

Please enclosed the backtest screenshot if you want

Regards

@JR1976

I think you can add the NR7 code like this (replace the line 168 with this one):

cx = Range<Range[1] and Range<Range[2] and Range<Range[3] and Range<Range[4] and Range<Range[5] and Range<Range[6] and Range<Range[7]

I did not test this strategy myself, but it seems over optimized, John didn’t explained us how he found all these variables values and indicators periods.

can we see a screenshot of the statistics of the backtest?

Thanks

Francesco

my problem is: can i believe the backtest… ?

results are good, but too good

code little bit more fine

see on yourself

so my question, can you controll the result on backtest?

timeframe 4h, start 01.01.2013 until today, Dax 1 Euro mini, spread = 2, no brokerage few

do i right put the screenshots?

can’t print the details as screenshot, find no “safe as” button .. how it works?

//-------------------------------------------------------------------------

// Hauptcode : EA Head V1.2

// created by JohnScher, coded with help from ProRealTime

//-------------------------------------------------------------------------

// Start Pathfinder-System

// with define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

defparam flatafter = 210000

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 0 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 1 //0 risk(1)

ONCE June1 = 1 //1 ok 2

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 0 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = Day

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

Endif

position = 2

// End Pathfinder-System

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Code Indicator NR7

// C1= Range<Range[1] and Range<Range[2] and Range<Range[3] and Range<Range[4] and Range<Range[5] and Range<Range[6] and Range<Range[7]

// RETURN C1

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Start maincode

//-------------------------------------------------------------------------

// maincode : H4 Live

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

cx1 = cci[11]<90

cx2 = cci[21]>-90

cx3 = Momentum[12](close)>0

cx4 = ADX[11] >14

// cx5 = MoneyFlow[11](close)<0

cx6 = TR(close) >14

//cx7 = PVT(close)<1

cx8 = EaseOfMovement[14]<70

cx9 = SmoothedStochastic[21,3](close)<90

cx10 = PriceOscillator[5,25](close)<0.5

cx11 = LinearRegressionSlope[12](close)>-14

cx12 = AccumDistr(close)>-0.1

cx13 = Chandle [21](close)>-21

cx14 = STD[6](close)<99

cx15 = Chandle [6] (close)<49

cx16 = RSI[6](close)<51

cx17 = RSI[6](close)>49

TradingDayShort = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingDayLong = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingTimeShort = time = 090000 or time = 130000 or time = 170000

TradingtimeLong = time = 090000 or Time = 130000 or time = 170000

IF TradingDayShort and TradingTimeShort Then

IF cx1 and cx4 and cx8 and cx9 and cx10 and cx12 and cx14 and cx15 and cx16 Then

IF ExponentialAverage [1] (close) < ExponentialAverage [8] (close) THEN

sellshort position*saisonalPatternMultiplier CONTRACTS AT MARKET

ENDIF

Endif

Endif

IF TradingDayLong and TradingTimeLong Then

IF cx2 and cx3 and cx6 and cx11 and cx13 and cx17 Then

IF ExponentialAverage [1] (close) > ExponentialAverage [6] (close) THEN

buy position*saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

Endif

Endif

Set Stop %Loss 3

Set Target %profit 3

// to be optimize

// kind JohnScher

nr7 isn´t integrated, is remnant from former code

target is : find filters to get out the main losses… want anyone help?

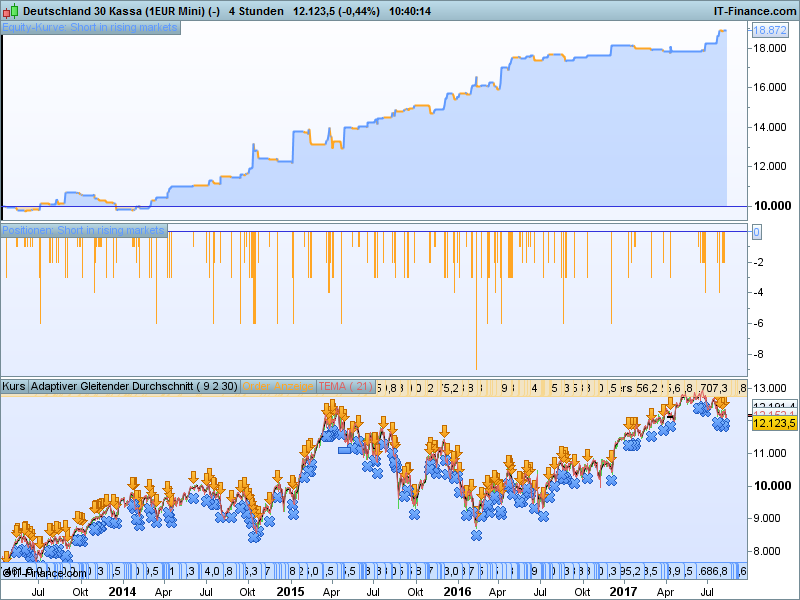

try this too as backtest

Short Trades in a rising market

//-------------------------------------------------------------------------

// Hauptcode : H4 live cxxxx last PF flat2100

//-------------------------------------------------------------------------

// Start Pathfinder-System

// with define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

defparam flatafter = 210000

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 1 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 1 //0 risk(1)

ONCE June1 = 1 //1 ok 2

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 1 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = Day

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

Endif

position = 2

// End Pathfinder-System

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Start Code Indicator NR7

//-------------------------------------------------------------------------

// C1= Range<Range[1] and Range<Range[2] and Range<Range[3] and Range<Range[4] and Range<Range[5] and Range<Range[6] and Range<Range[7]

// RETURN C1

//-------------------------------------------------------------------------

// End Code IndicatorNr7

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Start Hauptcode

//-------------------------------------------------------------------------

// Hauptcode : H4 Live

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

cx1 = cci[11]<90

//cx2 = cci[21]>-90

//cx3 = Momentum[12](close)>0

cx4 = ADX[11] >14

//cx5 = MoneyFlow[14](close)>0

//cx6 = TR(close) >14

//cx7 = PVT(close)<1

cx8 = EaseOfMovement[14]<70

cx9 = SmoothedStochastic[21,3](close)<90

cx10 = PriceOscillator[5,25](close)<0.5

//cx11 = LinearRegressionSlope[12](close)>-14

cx12 = AccumDistr(close)>-0.1

//cx13 = Chandle [21](close)>-21

cx14 = STD[6](close)<99

cx15 = Chandle [14] (close)<49

cx16 = RSI[6](close)<51

//cx17 = RSI[6](close)>49

cx18 = Chandle[12](close)>-21

cx19 = Williams[14](close)<-29

cx20 = Repulse[6](close)<-0.22

cx21 = MassIndex[12]>10

TradingDayShort = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

//TradingDayLong = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingTimeShort = time = 090000 or time = 130000 or time = 170000

//TradingtimeLong = time = 090000 or Time = 130000 or time = 170000

IF TradingDayShort and TradingTimeShort Then

IF cx1 and cx4 and cx8 and cx9 and cx10 and cx12 and cx14 and cx15 and cx16 and cx18 and cx19 and cx20 and cx21 Then

IF ExponentialAverage [1] (close) < ExponentialAverage [4] (close) THEN

sellshort position*saisonalPatternMultiplier CONTRACTS AT MARKET

ENDIF

Endif

Endif

IF ShortonMarket Then

Set Stop %Loss 3

Set Target %Profit 3

Endif

//IF TradingDayLong and TradingTimeLong Then

//IF cx2 and cx3 and cx5 and cx6 and cx11 and cx13 and cx15 and cx17 Then

//IF ExponentialAverage [1] (close) > ExponentialAverage [8] (close) THEN

//buy position*saisonalPatternMultiplier CONTRACT AT MARKET

//ENDIF

//Endif

//Endif

//IF Longonmarket then

//Set Stop %Loss 1

//Set Target %profit 1

//Endif

Thank you John, I received also your post in the library pending review list. I may be wrong, but I think you have optimized many variables (indicators’periods and levels), am I right? In this case, did you test also the best values in OOS (Out Of Sample) periods? Now that is available, you can use Walk Forward optimiser which help you find the good edge between over optimized strategy and robust one.

The fact is that the result of your backtest is, as you stated, “unbelievable”, because it is like you use the best suitable values for things you know already how they will happen.

Hello Nicolas.

So the Backtest give not a right result?

What ist OOS?

How does works walk forward? Do you have any Link or can you test the EA HEad only Short with walk forward?

The strategy seems quite overfitted on past price behaviour. I encourage you reading these articles:

In this first one, you’ll learn about In Sample and Out Of Sample testing methodology:

https://www.prorealcode.com/blog/avoid-equity-curve-fitting-with-probacktest-trading-strategy-optimisation/

This one is the extract of the proorder documentation about the new tool (walk forward analysis):

https://www.prorealcode.com/blog/learning/strategy-optimisation-walk-analysis/

Another post I made, as a FAQ for the Walk Forward tool (made of pieces from different discussions here and there on forums):

https://www.prorealcode.com/blog/learning/prorealtime-walk-analysis-tool/

Hello Nikolas.

Thanks so lot.

I have integrate EA Head and “Short on rising markets” in Demo-Account on PRT.

I ll give response, after 10 Trades run out. I ll give response about the match of the backtest results with the demo results too.

Dito EA Head.

So far so good.

best regards

First Trade: “Short on rising market”

at Demo-Account

Open 17:00:06 today at 12.202,08 6 CFD closed 21:00:04 at 12.158,1

Result +268.20

the code i use

copy paste

//-------------------------------------------------------------------------

// Hauptcode : Short in a rising market

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Hauptcode : H4 live cxxxx last PF flat2100

//-------------------------------------------------------------------------

// Start Pathfinder-System

// with define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

defparam flatafter = 210000

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 1 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 1 //0 risk(1)

ONCE June1 = 1 //1 ok 2

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 1 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = Day

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

Endif

position = 2

// End Pathfinder-System

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Start Code Indicator NR7

//-------------------------------------------------------------------------

// C1= Range<Range[1] and Range<Range[2] and Range<Range[3] and Range<Range[4] and Range<Range[5] and Range<Range[6] and Range<Range[7]

// RETURN C1

//-------------------------------------------------------------------------

// End Code IndicatorNr7

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Start Hauptcode

//-------------------------------------------------------------------------

// Hauptcode : H4 Live

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

cx1 = cci[11]<90

//cx2 = cci[21]>-90

//cx3 = Momentum[12](close)>0

cx4 = ADX[11] >14

//cx5 = MoneyFlow[14](close)>0

//cx6 = TR(close) >14

//cx7 = PVT(close)<1

cx8 = EaseOfMovement[14]<70

cx9 = SmoothedStochastic[21,3](close)<90

cx10 = PriceOscillator[5,25](close)<0.5

//cx11 = LinearRegressionSlope[12](close)>-14

cx12 = AccumDistr(close)>-0.1

//cx13 = Chandle [21](close)>-21

cx14 = STD[6](close)<99

cx15 = Chandle [14] (close)<49

cx16 = RSI[6](close)<51

//cx17 = RSI[6](close)>49

cx18 = Chandle[12](close)>-21

cx19 = Williams[14](close)<-29

cx20 = Repulse[6](close)<-0.22

cx21 = MassIndex[12]>10

TradingDayShort = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

//TradingDayLong = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingTimeShort = time = 090000 or time = 130000 or time = 170000

//TradingtimeLong = time = 090000 or Time = 130000 or time = 170000

IF TradingDayShort and TradingTimeShort Then

IF cx1 and cx4 and cx8 and cx9 and cx10 and cx12 and cx14 and cx15 and cx16 and cx18 and cx19 and cx20 and cx21 Then

IF ExponentialAverage [1] (close) < ExponentialAverage [4] (close) THEN

sellshort position*saisonalPatternMultiplier CONTRACTS AT MARKET

ENDIF

Endif

Endif

IF ShortonMarket Then

Set Stop %Loss 3

Set Target %Profit 3

Endif

//IF TradingDayLong and TradingTimeLong Then

//IF cx2 and cx3 and cx5 and cx6 and cx11 and cx13 and cx15 and cx17 Then

//IF ExponentialAverage [1] (close) > ExponentialAverage [8] (close) THEN

//buy position*saisonalPatternMultiplier CONTRACT AT MARKET

//ENDIF

//Endif

//Endif

//IF Longonmarket then

//Set Stop %Loss 1

//Set Target %profit 1

//Endif