You have to calculate it yourself but it’s very easy. You simply drag-n-drop the tab “Closed positions list” from the backtest report into an empty Excel sheet. Then summarize the MFE and MAE columns and divide.

Here is a short video tutorial of how to “export” data: https://www.youtube.com/watch?v=W35tjsD4PrM&feature=youtu.be&t=413

Hi, seems many variables in there.

May I know which lines will be more important?

Thanks.

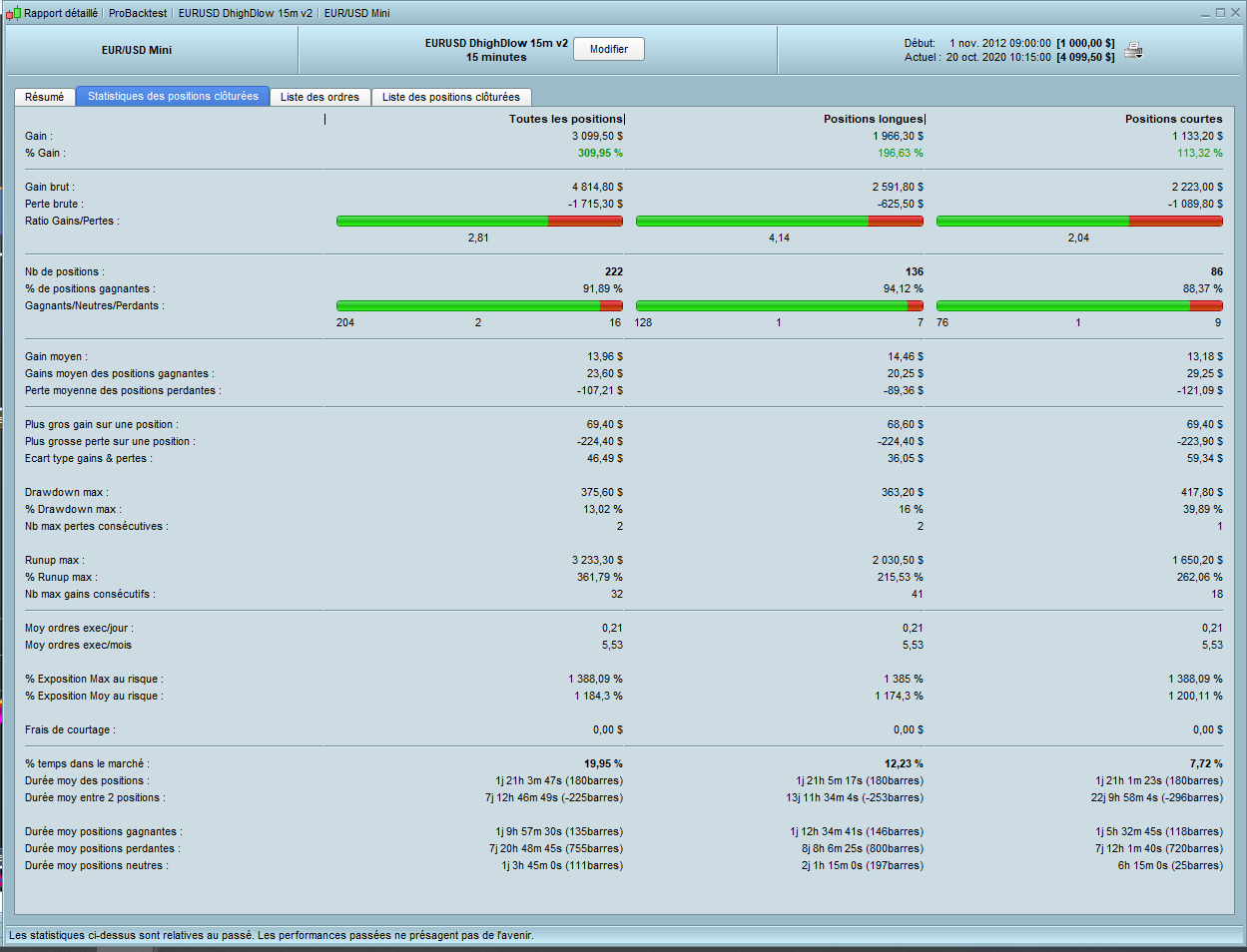

EUR/CAD bot has been going well but idk if I will keep running it cause of no sl.

Bonjour

J’ai des énormes pertes

Quelle est la procédure à suivre la faire fonctionner ?

je suis ssur l’EURUSD 15 min , UTC +02:00 (paris)

Beaucoup de posisitions gagnantes et puis des énormes pertes.

Aussi bien avec le code posté précédent que le code original. et CloturePartielle + 0 ou 1

Hello

I have huge losses

What is the procedure to make it work?

I am on EURUSD 15 min, UTC +02: 00 (paris)

Lots of winning positions and then huge losses.

Both with the previous posted code and the original code. and Partial Closure + 0 or 1

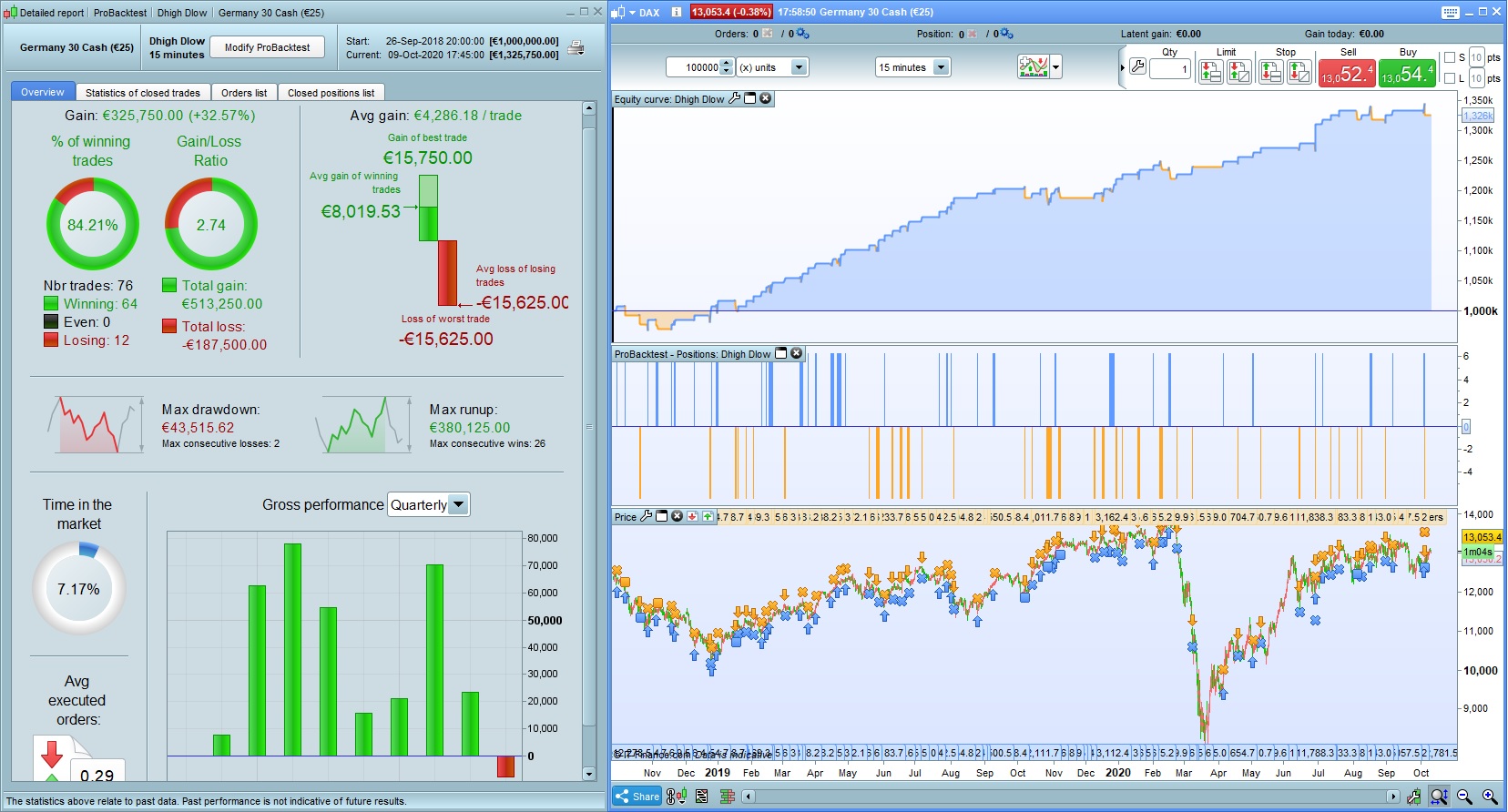

I don’t understand, on more screenshoot of “Detailed report”; the sum of losses are under max drawdawn?????

pat95162 – English language only in the English language forums. Please respect the forum rules with any future posts.

To understand as this stratégy worsk, I have create an indicator on grapf and an indicator for the inside.

Indicator on graph:

once select=1 // optimized for period1,2,3

once tds =1 // added on optimized results

if select=1 then // TF 15 MIN

tr1=45

tr2=25

period1=78

period2=12

period3=4

elsif select=2 then // TF 15 MIN

tr1=45

tr2=20

period1=84

period2=6

period3=8

endif

// trend detection

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=Average[tr1](close)//>Average[tr1](close)[1])

trenddown=Average[tr2](close)//<Average[tr2](close)[1])

else

if tds=2 then

endif

endif

endif

mm = average[period1,3](totalprice)

Newhighest=max(DHigh(0), DHigh(1))

Newlowest=min(DLow(0), DLow(1))

avghl = (Newhighest+Newlowest)/2

c1 = average[period2,period3]((Newhighest+avghl)/2)

c2 = average[period2,period3]((Newlowest+avghl)/2)

return trendup As "Trendup", trenddown AS "Trenddown", mm AS "mm", avghl as "Avgh1", c1 as "C1", c2 AS "C2"

Indicator for inside:

myTrendup, myTrenddown, mymm, myAvgh1, myC1, myC2 = CALL "Dhigh/Dlow"

HA = 0

If mymm > myc1 and close crosses over myAvgh1 and mytrendup > mytrendup[1] then

HA = +1

endif

If mymm < myc2 and close crosses under myAvgh1 and mytrenddown < mytrenddown[1] then

HA = -1

endif

Return HA

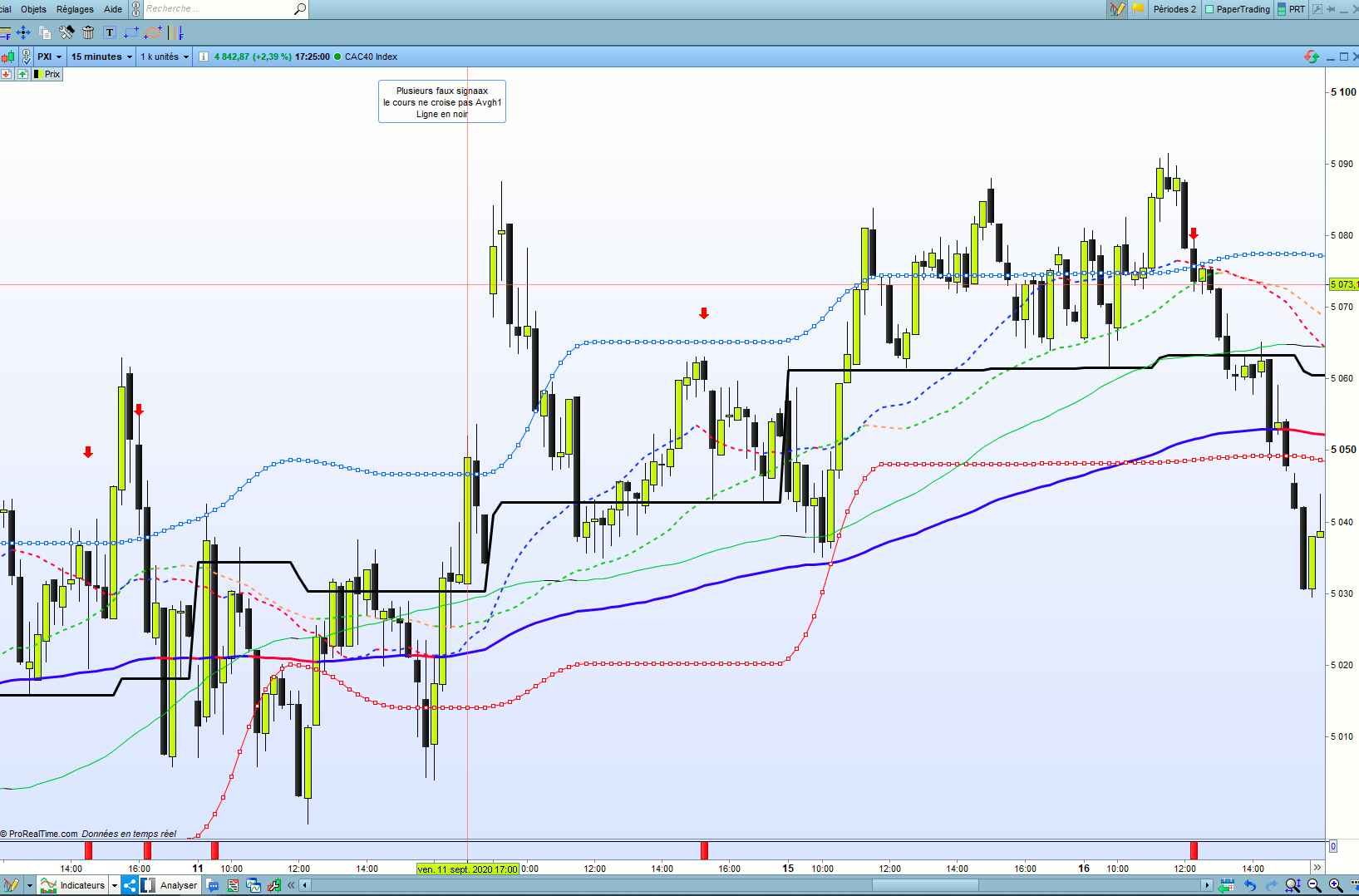

PRT make false signal????? Cf view

@Demon

Always use the ‘Insert PRT Code’ button when putting code in your posts to make it easier for others to read.

Thank you 🙂

Sorry.

I’ll be the next time I write.

Have a nice day

Hi all,

I had some success in DAX under backtest environment.

As below

DEFPARAM CumulateOrders = False

DEFPARAM PRELOADBARS = 10000

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Schedule = time >= 000000 and time <= 220000

Positionsize = 6.25

TREND = Average[8,8](totalprice)

Newhighest=max(DHigh(0), DHigh(1))

Newlowest=min(DLow(0), DLow(1))

Middle = (Newhighest+Newlowest)/2

Overbought = average[45,5]((Newhighest+Middle)/2)

Oversold = average[45,5]((Newlowest+Middle)/2)

CA = (TREND > Overbought) and (close crosses over Middle)

CV = (TREND < Oversold) and (close crosses under Middle)

// Long Entries

IF Schedule AND CA AND not daysForbiddenEntry AND NOT SHORTONMARKET THEN

BUY Positionsize CONTRACTS AT MARKET

ENDIF

IF LONGONMARKET THEN

SELL AT TRADEPRICE +50*pointsize LIMIT

ENDIF

// Short Entries

IF Schedule AND CV AND not daysForbiddenEntry AND NOT LONGONMARKET THEN

SELLSHORT Positionsize CONTRACTS AT MARKET

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT TRADEPRICE - 50*pointsize LIMIT

ENDIF

//SET TARGET pPROFIT 46

SET STOP pLOSS 100

Very bad results on 200k candles, do not go live with it, see picture attached

Great improvement @kj1988

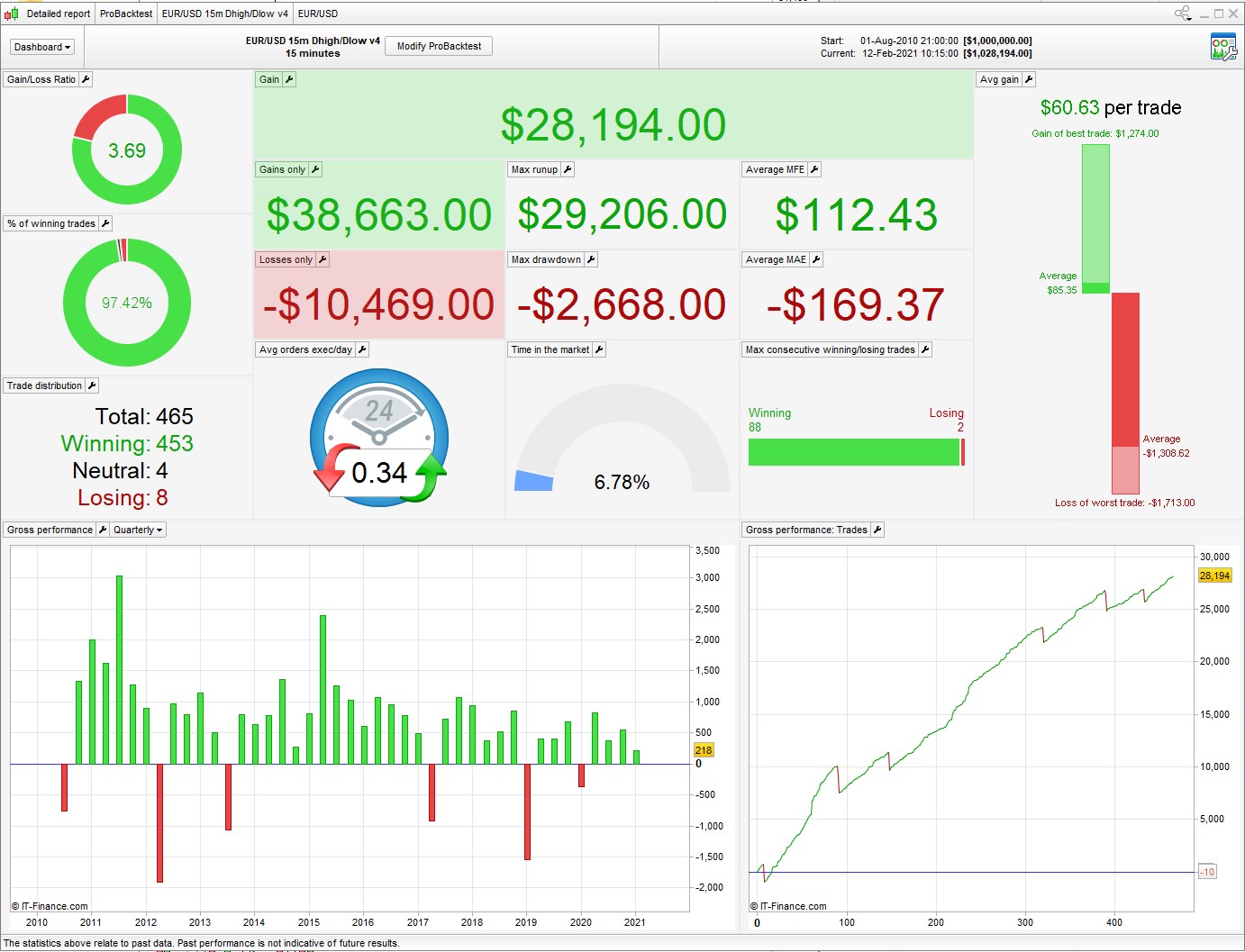

I also did some tweaking with your file to boost the result (100k period), see attached. It was missing a profit target which I find necesary even with a trail. Also added some MoneyM and RiskM. The problem is still the big drawdown on almost every trade. The MFE/MAE ratio is a dreadful 0.99. If we can find better entry signals we might have something.

Hello guy and thank for your share. As you, i observe that you some time have big loss in 1 trade. But i also see in details report that when you win in Long or Short, it’s in less than 150 candles and when you loose, it’s in 700 to 800 candles. Maybe you can add in your code something who close your trade after 150 or 200 candles. It certainly would limit the lost trades

Hi! News about big losses? Trading system is very very good (over 94% winning) but the 6% remaining is a disaster for the equity

Here’s another version of this with a few changes to try to curb the losses. There aren’t very many, but when it loses, it loses big time.

I’ve raised the SL to 2%, which can mean dealing with some big red numbers while waiting for it to turn around, something to be aware of.