Oops, I’ve been running it with select=2 on 15m …. and it still made $100 today. Very nice!

But should the tds value correspond to the select value? or is it just an optional on/off ?

I’ve been running it with select=2 on 15m

Well double check on my logic as I may be wrong? Try it with select = 2 on 30 mins … is it bigger profit?

TDS is the Trend Detection System and so needs to be same as Trend value in the optimiser.

Select=2 is def better at 15m. I’m running the juju333 version at 30m … also outstanding.

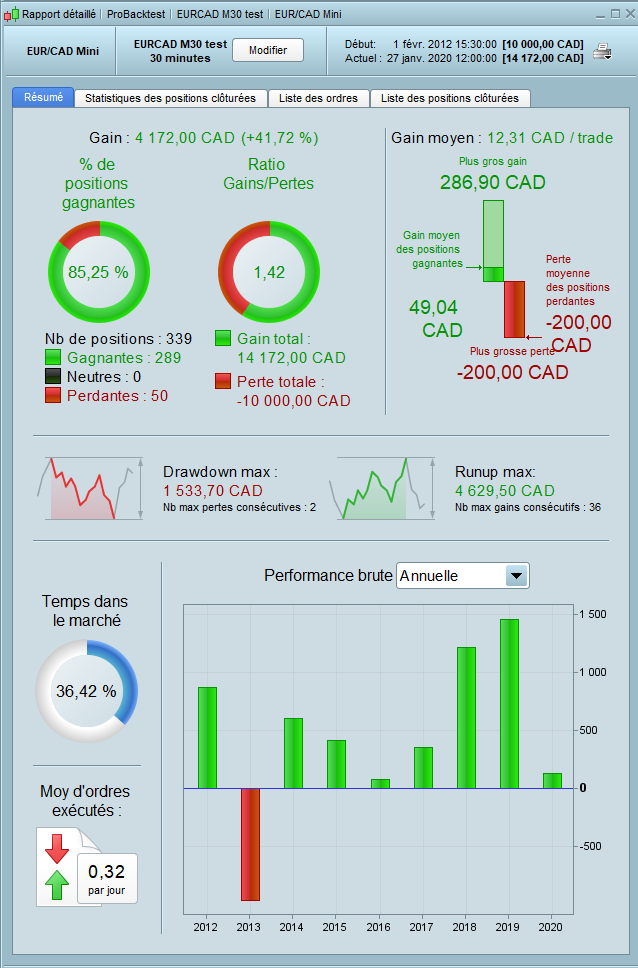

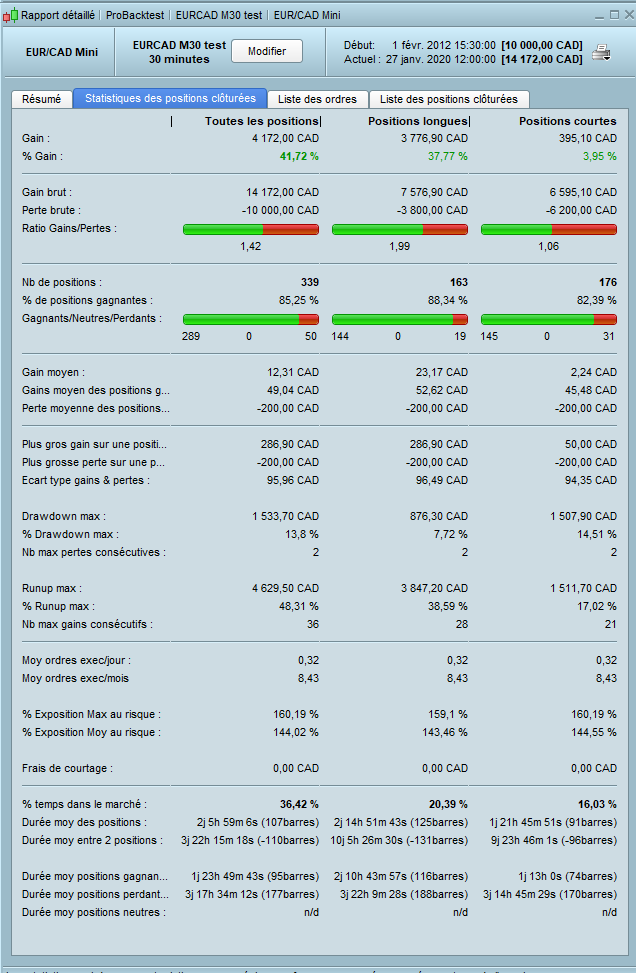

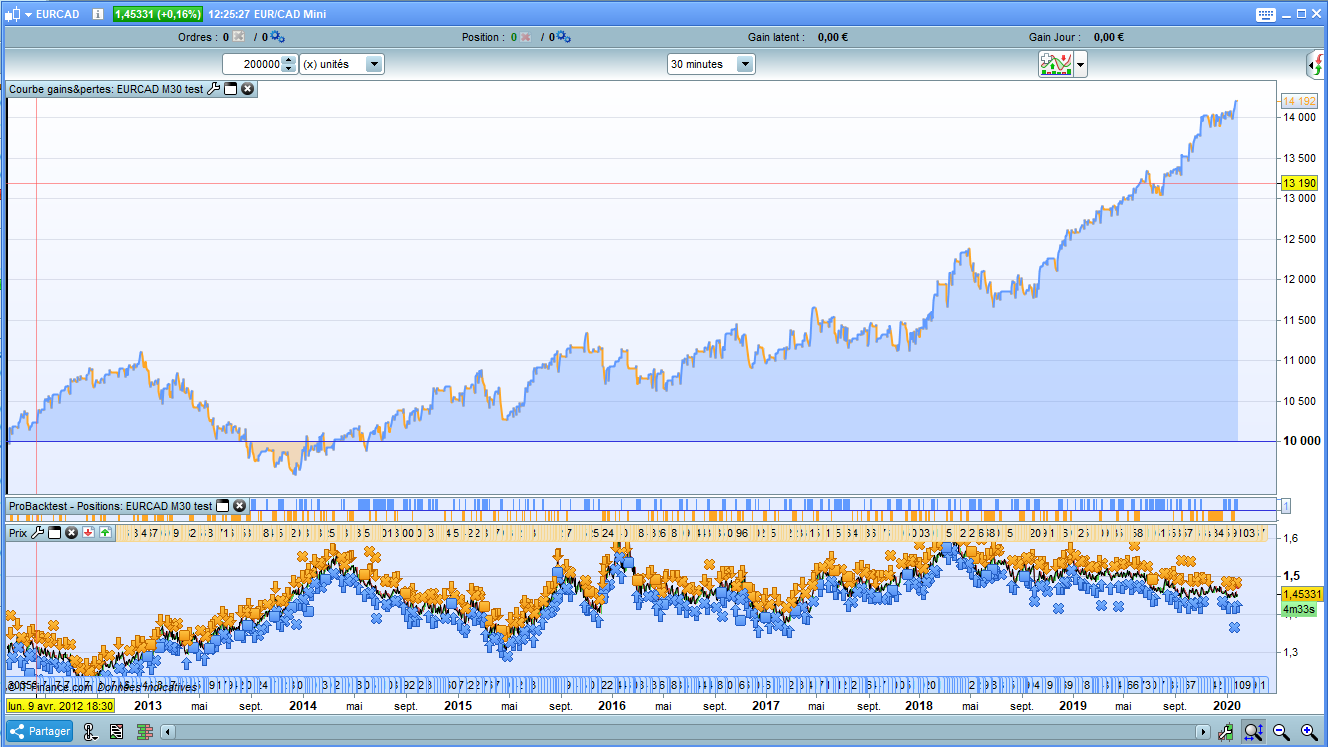

Hi, i’ve turned partial closure off and slightly optimized for EURCAD and M30. Too good to be true, but i share it (running in demo mode from this morning). Indeed take care of drawdown… :

DEFPARAM CumulateOrders = False

DEFPARAM PRELOADBARS = 10000

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Horaire = time >= 000000 and time <= 220000

PositionsizeA = 1

PositionsizeV = 1

MM = Average[56,3](totalprice)

Newhighest=max(DHigh(0), DHigh(1))

Newlowest=min(DLow(0), DLow(1))

Milieu = (Newhighest+Newlowest)/2

Surachat = average[10,4]((Newhighest+Milieu)/2)

Survente = average[10,4]((Newlowest+Milieu)/2)

CA = (MM > Surachat) and (close crosses over Milieu)

CV = (MM < Survente) and (close crosses under Milieu)

// Long Entries

IF Horaire AND CA AND not daysForbiddenEntry AND NOT SHORTONMARKET THEN

BUY PositionsizeA CONTRACTS AT MARKET

ENDIF

IF LONGONMARKET THEN

SELL AT TRADEPRICE +540*pointsize LIMIT

ENDIF

// Short Entries

IF Horaire AND CV AND not daysForbiddenEntry AND NOT LONGONMARKET THEN

SELLSHORT PositionsizeV CONTRACTS AT MARKET

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT TRADEPRICE – 50*pointsize LIMIT

ENDIF

//MFE

//trailing stop

trailingstop = 40

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)–MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE–tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE–trailingstop*pointsize //set the exit price at the MFE – trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//SET TARGET pPROFIT 46

SET STOP pLOSS 200

Hi Juju333

I have been running this version live on 1min TF since 16 december and so far 6 winning trades, 0 losing trades. Can someone run it on 200 K

>> For clarity of messages on ProRealCode’s forums, please use the “insert code PRT” button to separate the text of the code part! Thank you! << 🙂

Hello @jmf125,

It’s no possible backtest 200 k with TF 1 min… i don’t understand…

Hello @jmf125,

It’s no possible backtest 200 k with TF 1 min… i don’t understand…

Apologies this is on a 30 mins EUR/CAD

Hello @jmf125,

It’s no possible backtest 200 k with TF 1 min… i don’t understand…

Yes it is, but obviously the tested period will be shorter than 5 min, 15 min or 1h

@jmf125 : EUR/CAD M30, 200k, spread 2.5

Thanks EricN78

Not as good, 2013 seems to be the year giving the negative results. DD is also much bigger.

Hey guys,

I’ve started working on the code, but i still can’t figure out this part:

Newhighest=max(DHigh(0), DHigh(1))

Newlowest=min(DLow(0), DLow(1))

avghl = (Newhighest+Newlowest)/2

c1 = average[period2,period3]((Newhighest+avghl)/2)

c2 = average[period2,period3]((Newlowest+avghl)/2)

NewHighest is a single value, but later used to draw a moving average. Usually we use a “close” or at least an array, im confused about the type of this variable. Can someone help me clarify this ? 🙂

Hi Bobflynn

You can average any single value. As you correctly say the usual moving average will be on close; but you can also average any other value e.g open , low, high … or average a calculated value like newhighest

Check this out – by splitting into 2 strategies for long and short then re-optimizing each individually gives an extra 60% gain with combined win rate of 97% (4 losses out of 122).

More trades, more wins, lower drawdown, better best trade, better average gain, better gain/loss.

Left hand image is the combined strategy, based on Paul’s EURCAD-DhighDlow-v1p position size =1

Check this out – by splitting into 2 strategies for long and short then re-optimizing each individually gives an extra 60% gain with combined win rate of 97% (4 losses out of 122).

More trades, more wins, lower drawdown, better best trade, better average gain, better gain/loss.

Left hand image is the combined strategy, based on Paul’s EURCAD-DhighDlow-v1p position size =1

This looks awesome !! Thank you