Hi there,

Lately I am having serious doubts about the confidence of the backtest results in PRT. Mainly because I found significant differences in backtests that shouldn´t exist. For instance between real and demo results, in backtest and also in proorder trading. I understand that it´s normal to have some differences but I am talking about serious differences in different systems. Also when I share some systems with a friend that lives in a different timezone, even changing the hours accordingly the difference in results are too high.

Do you experience same kind of things? Because if I can´t belive the backtest results then my systems are worthless

For instance between real and demo results, in backtest

Do you mean differences between Backtest on your Live Platform and Backtest on your Demo Platform? Are both Platforms same settings, time zone and spread etc?

Why not post screen shots of the differences and (better still) post the code so one of us could also backtest on our Live and Demo Platforms and compare with yours?

Just ideas to move your issue forward a bit?

Hi Grahal,

Yes, differences between Live and Demo Platforms. I haven´t checked all my systems, but some of them have small differences and others biggers, with everything the same of course (system, period, spread…)

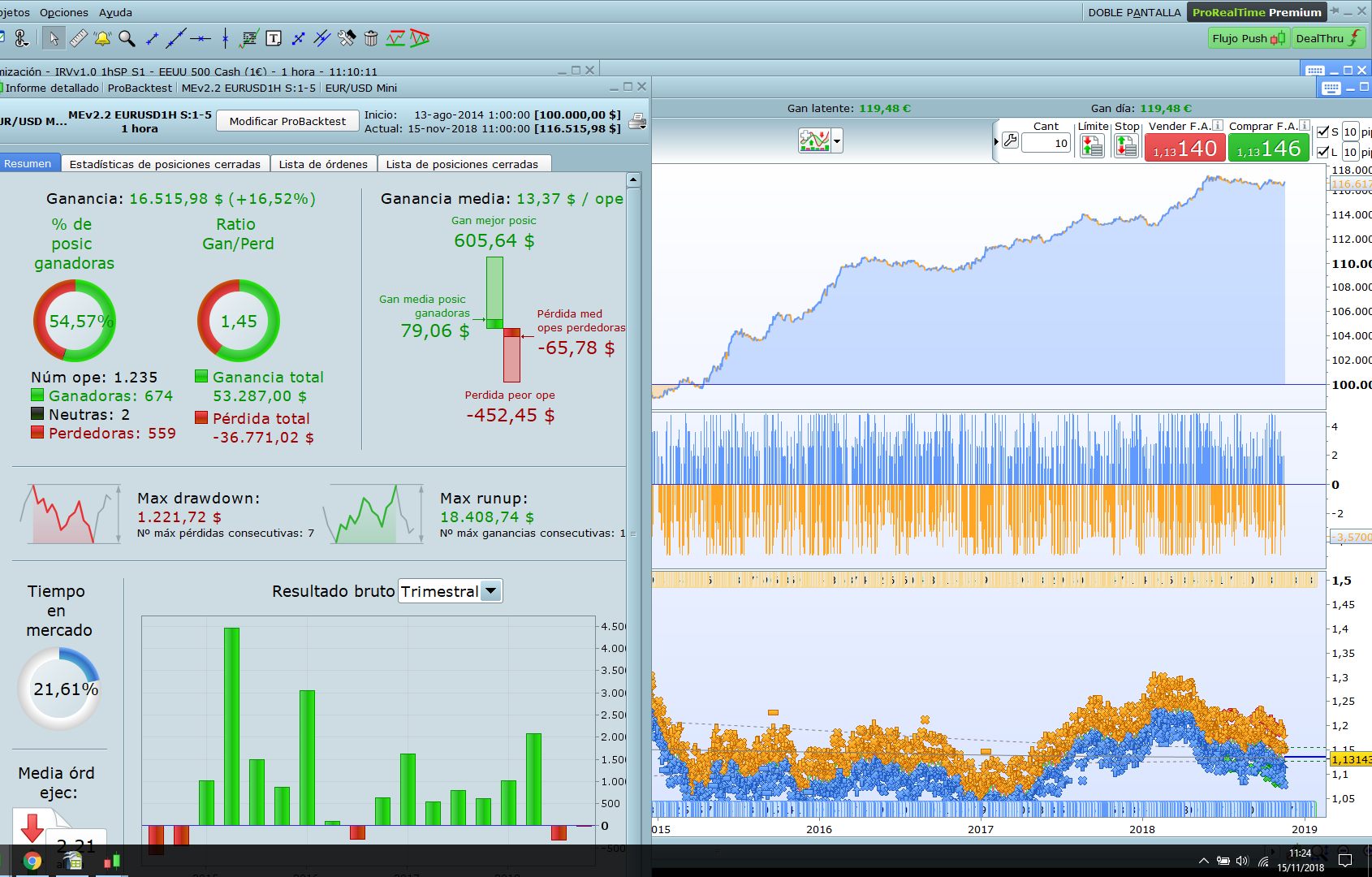

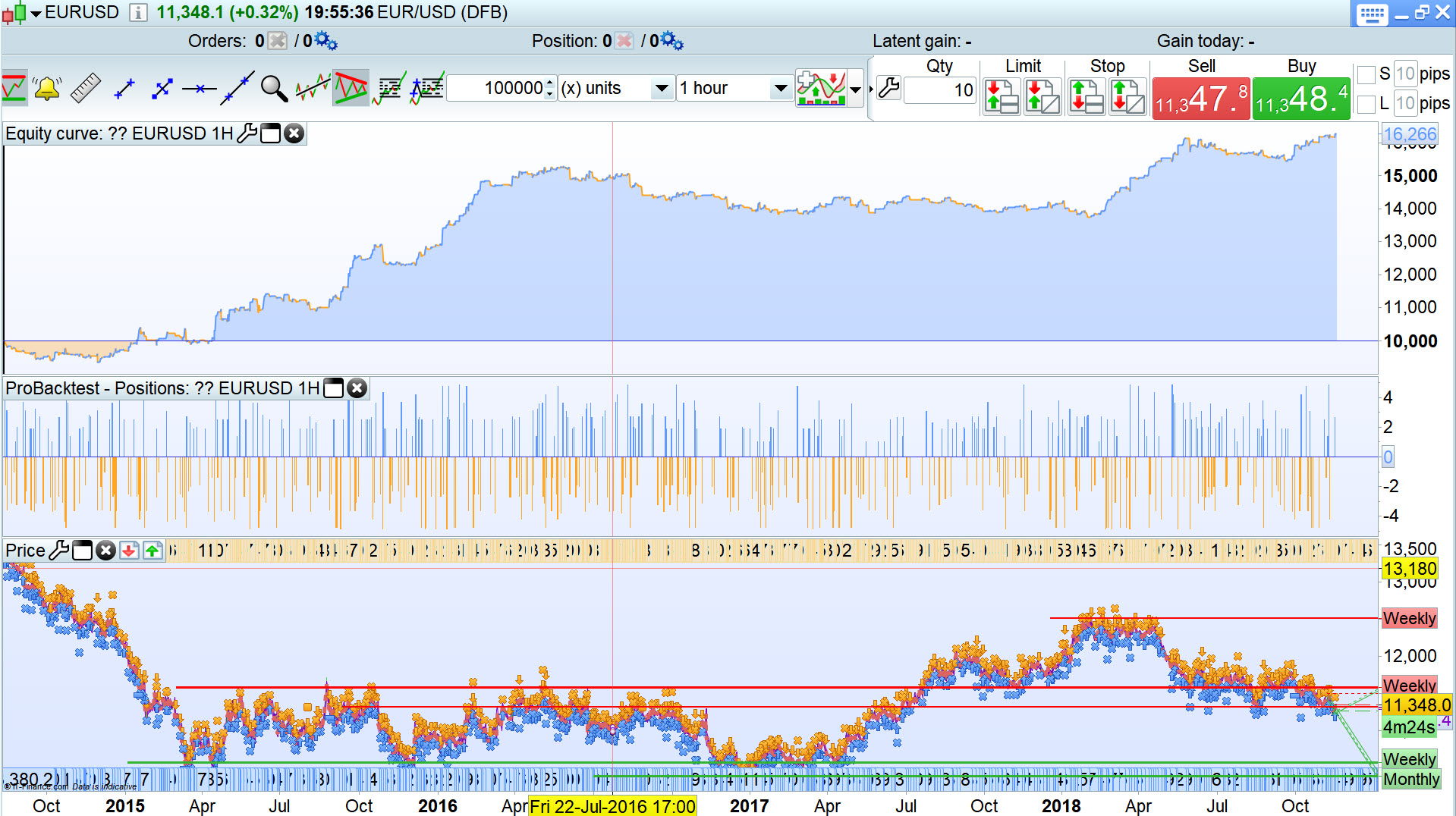

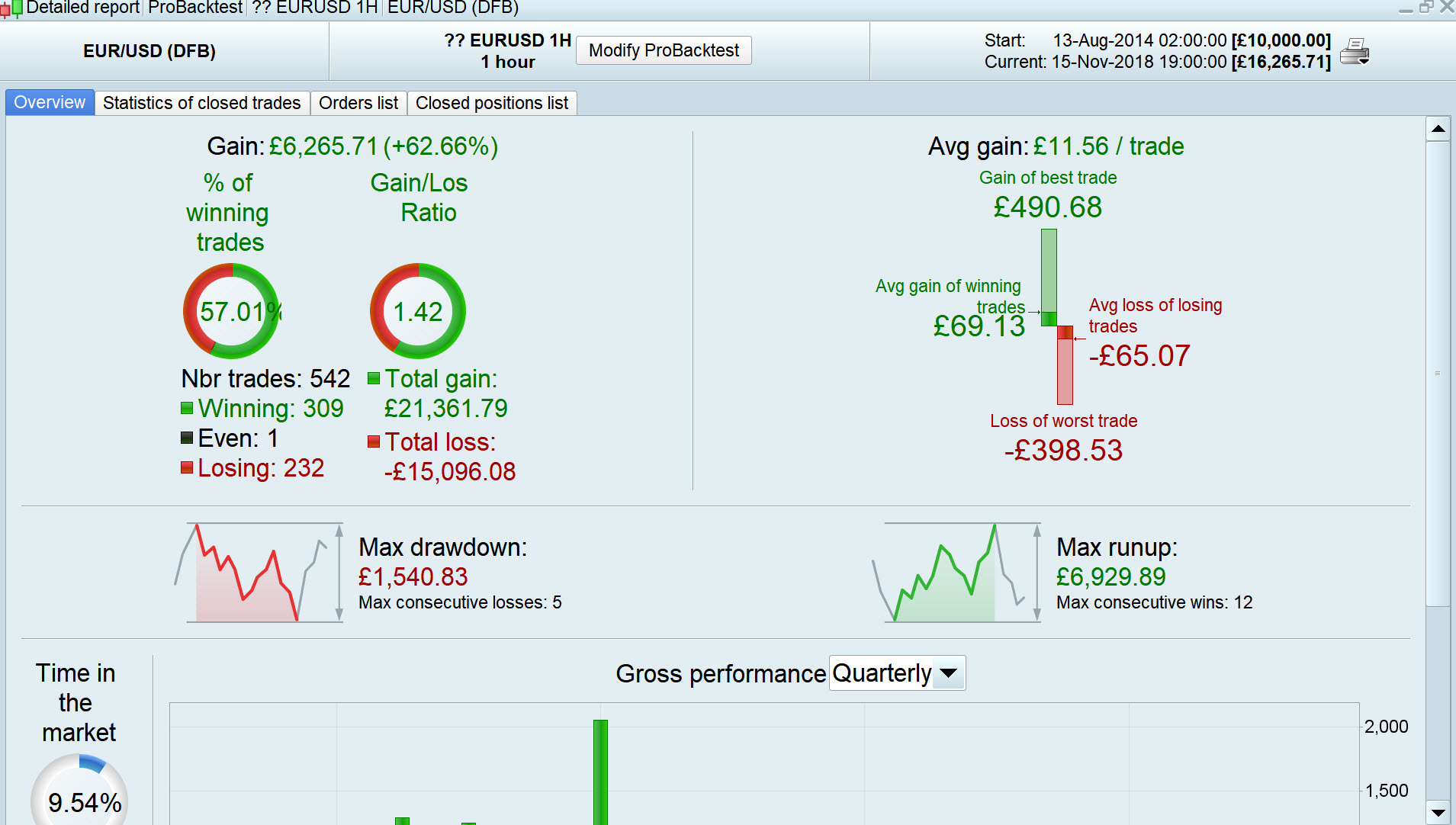

For instance these are the results in Live and Demo for the same system,timezoneperiod/spread…

This is the code and my timezone is UTC+00:00 Europe/London

///Sistema ME (Market Edge)

//EURUSD 1H v2.2

//Por TempusFugit

//Ultima revisión: 14-11-2018

////////////////////////////////////////////////

// System parameters

DEFPARAM CumulateOrders = False

DEFPARAM PRELOADBARS = 2000

//VARIABLES

HL = 16 //Hora Entrada Largos

HLS = 20 //Hora Salida Largos

HS = 7 //Hora Entrada Cortos

HSS= 13//Hora Salida Cortos

LongStopPercentage = 0.65

LongProfitPercentage = 1.1

ShortStopPercentage = 1.9

ShortProfitPercentage = 0.65

RSL = 85//LIMITE PARA FILTRO RSI-MOMENTUM LARGOS

RSS = 70//LIMITE PARA FILTRO RSI-MOMENTUM CORTOS

m = 7 //PRIMERA CIFRA DEL MACD PARA FIJAR TENDENCIA

XMACD = -0.25 //LIMITE VALOR MACD PARA FILTRAR TENDENCIA

// GESTION POSICION

POSITIONSIZEINCREASE = 1.4//MULTIPLICADOR PARA TODAS LAS POSICIONES.

RSIMAXSIZE = 1.6//Max incremento posicion por RSI-Momentum

SHORTINCREASE = 1//Multiplicador para posiciones cortas

LIMITEPERDIDAS = 99999 //SI LLEGA A ESTA CANTIDAD DE PERDIDAS EL SISTEMA SE PARA

REDUCIRPOSICION = 0.75 //MULTIPLICADOR DE LA POSICION SI EL BENEFICIO ESTA POR DEBAJO DE SU MEDIA

NMAPS = 500 //PERIODOS DE LA MEDIA PARA CALCULAR SI SE REDUCE POSICION. MAYOR O MENOR SEGUN LO ACTIVO QUE SEA EL SISTEMA Y DEL TIMEFRAME

PERCENTCROSSMA = 0 //PORCENTAJE QUE TIENE QUE SUPERAR EL SPROFIT A SU MEDIA PARA REDUCIR LA POSICION

IF STRATEGYPROFIT<-LIMITEPERDIDAS THEN

QUIT

ENDIF

//CALCULO SOBRECORMPRA/SOBREVENTA

OVERBOUGHT = RSI[2](close)>RSL

OVERSOLD = RSI[2](close)<100-RSS

//CALCULO TENDENCIA ALCISTA/BAJISTA

b = round(m*26/12)

c = round(m*9/12)

NOBEAR = MACDline[m,b,c](close)>XMACD/100

NOBULL = MACDline[m,b,c](close)<-XMACD/100

//////////////////POSITION SIZE\\\\\\\\\\\\\\\\\\\\\\

//Position Size by WeekDay.Media de 1.5 por día

IF CurrentDayOfWeek=1 THEN

LPDAY=0

SPDAY=1

ELSIF CurrentDayOfWeek=2 THEN

LPDAY=1

SPDAY=0

ELSIF CurrentDayOfWeek=3 THEN

LPDAY=1.9

SPDAY=1.9

ELSIF CurrentDayOfWeek=4 THEN

LPDAY=1.8

SPDAY=1.8

ELSIF CurrentDayOfWeek=5 THEN

LPDAY=1.8

SPDAY=1.8

ENDIF

//Position Size by RSI2

XRSI = RSI[2](close)

IF 100-XRSI>=80 THEN

LPSRSI = RSIMAXSIZE

ELSIF 100-XRSI>=70 THEN

LPSRSI = RSIMAXSIZE*0.75

ELSIF 100-XRSI>=60 THEN

LPSRSI = RSIMAXSIZE*0.50

ELSE

LPSRSI=0

ENDIF

IF XRSI>=80 THEN

SPSRSI = RSIMAXSIZE

ELSIF XRSI>=70 THEN

SPSRSI = RSIMAXSIZE*0.75

ELSIF XRSI>=60 THEN

SPSRSI = RSIMAXSIZE*0.50

ELSE

SPSRSI=0

ENDIF

//Cálculo de tamaño de posición

sp = strategyprofit

IF strategyprofit*(1+(PERCENTCROSSMA/100))<Average[NMAPS](sp) THEN

LPOSITIONSIZE = REDUCIRPOSICION*POSITIONSIZEINCREASE*(LPDAY+LPSRSI)

SPOSITIONSIZE = SHORTINCREASE*REDUCIRPOSICION*POSITIONSIZEINCREASE*(SPDAY+SPSRSI)

ELSE

LPOSITIONSIZE = POSITIONSIZEINCREASE*(LPDAY+LPSRSI)

SPOSITIONSIZE = SHORTINCREASE*POSITIONSIZEINCREASE*(SPDAY+SPSRSI)

ENDIF

//////////////CONDICIONES ENTRADA/SALIDA/////////////

LongEntry = Hour=HL

LongEntry = LongEntry AND NOT OVERBOUGHT

LongEntry = LongEntry AND NOBEAR

LongEntry = LongEntry AND DAYOFWEEK<>1

//LongEntry = LongEntry AND close>99999999999

ShortEntry = Hour=HS OR (BARINDEX-TRADEINDEX>4 AND Hour=HS+2)

ShortEntry = ShortEntry AND NOT OVERSOLD

ShortEntry = ShortEntry AND NOBULL

ShortEntry = ShortEntry AND DAYOFWEEK<>2

ShortEntry = ShortEntry AND DAY<>1 AND DAY<>2 AND DAY<>24 AND DAY<>29 AND DAY<>31

//ShortEntry = ShortEntry AND close>99999999999

IF LongEntry THEN

BUY LPOSITIONSIZE CONTRACTS AT close LIMIT

SET STOP LOSS LongStopPercentage*CLOSE/100

SET TARGET PROFIT LongProfitPercentage*CLOSE/100

ENDIF

If LongOnMarket AND Hour>=HLS THEN

SELL AT close LIMIT

ENDIF

IF ShortEntry THEN

SELLSHORT SPOSITIONSIZE CONTRACTS AT close LIMIT

SET STOP LOSS ShortStopPercentage*CLOSE/100

SET TARGET PROFIT ShortProfitPercentage*CLOSE/100

ENDIF

IF ShortOnMarket AND Hour>=HSS THEN

EXITSHORT AT close LIMIT

ENDIF

I forgot… for EUR/USD 1h, spread 0,9

On my Demo Platform on EURUSD 1H with spread = 0.9 100k bars I get results attached … number of trades < half what you get!

The plot thickens, I am thinking what might be the reason.

I cannot test on Live sorry as I have my Live Platform disabled.

Because of these inconsistencies now I am running some systems both in Demo and Live at the same time and as expected there are some differences in the results of the trades (no exactly the same prices of entry/exit –> normal/expected) but also a few trades that doesn´t match between Live/Demo (WHY???). Very few days running both systems so I can tell yet how often or if it occurs only in some systems but I can tell that it happens.

Am I the only one with these inconsistencies?

Am I the only one with these inconsistencies?

I doubt it very much, but others are not checking the same inconsistency that you are?

We are all trying to deal with other inconsistencies … roll on Version 11.3 and this will be all behind us (I bet NOT!? 🙁 )

I see clearly at same period GraHal differences between demo and live in orders.

meaning it’s opening a buy while the criteria not match. Demo works fine…