You’re absolutely right, if it weren’t for the tight backtest period I would have already implemented it in my portfolio.

Let’s see if it’s possible to increase the time frame and obtain the same excellent results 😀

As said before, the sort timeframe is a problem for an ideal future live implementation of the strategy.

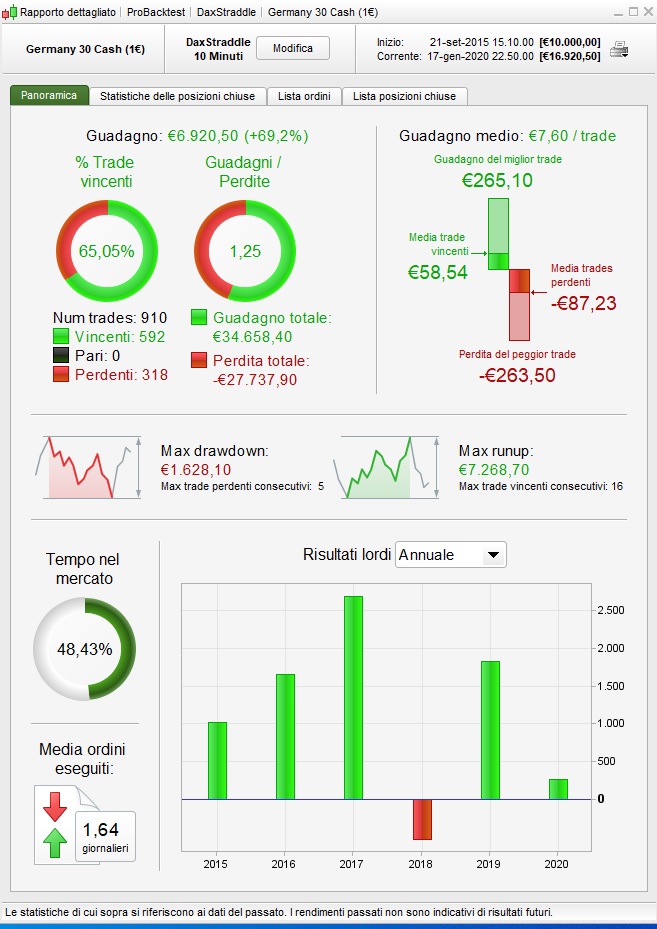

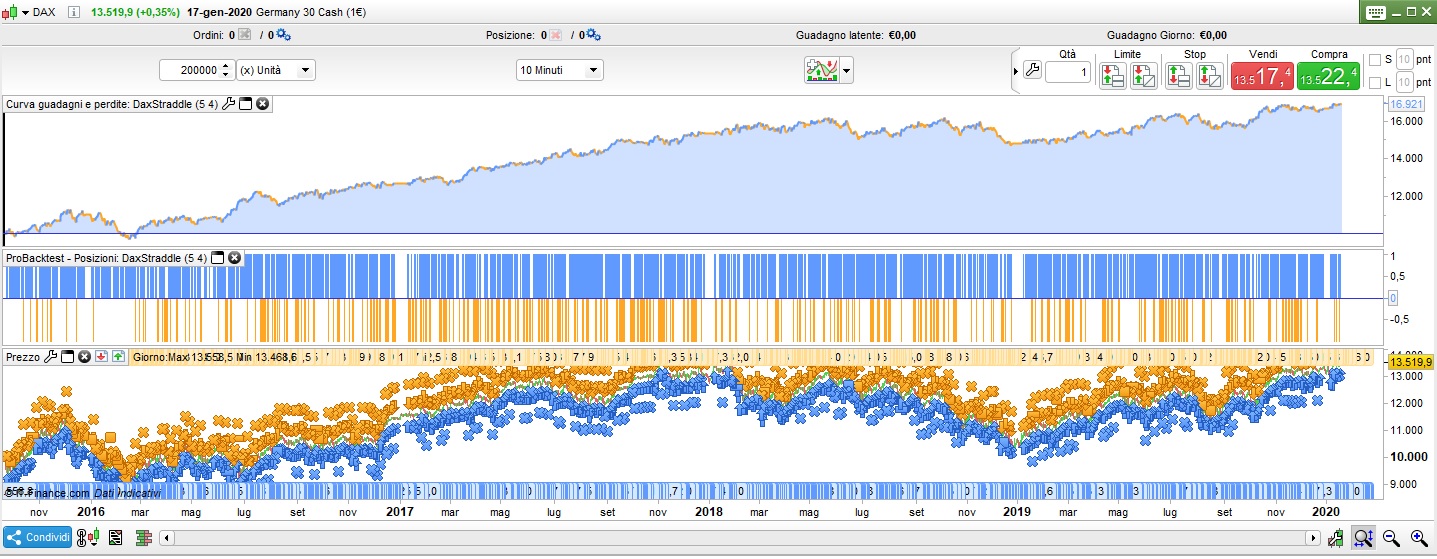

So, i tried to make little fixes to the 1min code in order to fit in a 10min timeframe and have a larger backtest view.

Results are not the best, but could be a starting point.

Paul

PaulParticipant

Master

@Francesco

That timeframe is a lot better I think. What is a bit of issue with this strategy, is the way the entry is coded. The current way it is it checks first the long criteria, that’s why long has preference has the better results especially in a rising market.

If you swap in the code below the long & short the strategy breaks down, because then it checks short criteria first. It’s because “elsif”

if tradetime and tradeday then

if pclong and mclong then

orderpriceL=dayopen+((close/10000)*2)*pipsize

buy positionsize contract at orderpriceL stop

longtradecounter=longtradecounter + 1

tradecounter=tradecounter+1

elsif pcshort and mcshort then

orderpriceS=dayopen-((close/10000)*2)*pipsize

sellshort positionsize contract at orderpriceS stop

shorttradecounter=shorttradecounter + 1

tradecounter=tradecounter+1

endif

endif

or you could code it like this below, which is in essence better; Then long above short, or visa versa give the same results. But then again results go down.

if tradetime and tradeday then

if pclong and mclong then

orderpriceL=dayopen+((close/10000)*2)*pipsize

buy positionsize contract at orderpriceL stop

longtradecounter=longtradecounter + 1

tradecounter=tradecounter+1

endif

if pcshort and mcshort then

orderpriceS=dayopen-((close/10000)*2)*pipsize

sellshort positionsize contract at orderpriceS stop

shorttradecounter=shorttradecounter + 1

tradecounter=tradecounter+1

endif

endif

ps on the strategy you posted. if you remove

if onmarket then

if time >= closetime or (currentdayofweek=5 and time>=closetimefr) then

sell at market

exitshort at market

endif

endif

once closetime = 240000 // greater then 23.59 means it continues position overnight

once closetimefr = 172900

then results go up.

Good results with those fixes, but huge drawdown and not smooth curve 🙁

Anyway, as i said it was a good starting point!

PaulParticipant

Master

the v6p in demo since 2 january

hello paul, well done for all your work. have you ever had canceled orders on the 1 min version because it happens 2 times out of 3. thank you in advance

PaulParticipant

Master

Hi

Wacko. Yes it happens. it could be that the stop for entry is too near the current close to be placed and doesn’t meet the criteria of the minimum stop distance. In that case you can try to increase the 1.5/2 figures to something a bit higher.

Hi folks. I have been running daxv6p on live since 16th may. About 300€ profit.

@Paul have you ran it since you posted in jan to 16th may without any improvements, if so whats the results?

PaulParticipant

Master

no I haven’t ran it and didn’t look at the code for a long time!

Well it has been profiting since may. Why did you stop it

@Paul?

depending what version, i had several front testing, deleted the data, (stupid) but it had hugh drawdown!!!

Well im talking about The v6p

PaulParticipant

Master

it works mostly in uptrends, so it’s not good enough.

Hi, i am currently testing the V5.3 on my demo account. I have tried loading the D6p version and i get a warning message,

Optimization limit. Your back test exceeds the limit for repetitions for walk forward optimization.

backtest.limit.optimisation.occurence,teasing

How do i edit the variables ? No lines are highlighted in red as not working…

This looks like a great system by the way and i would really like to see it working for me.

Lastly , what world time zone does it work best in?

Many thanks

Open the optimization window, activate WF, reduce the number of repetitions, deactivate WF, close optimization window.