@Paul

I will do more tests, but i have to ask you if you can attach the LATEST version of the strategy and on what timeframe you think should work on.

It’s a little bit confusing trying to find the last legit one in 14 pages 😀

Paul

PaulParticipant

Master

Hi, the latest is on page 14 v6p and is designed for the dax 1 minute.

Thing is, I don’t like the 1 minute timeframe one bit, so if can be improved upon would be great (preferably 5/15 min or higher)!

Ok I had it under my eyes and I didn’t noticed sorry 😀

There’s some variables optimizations to do also?

Btw i agree with you, 1min seems too low.

Anyway did you used the system on your live account in these years?

PaulParticipant

Master

Yes on & off and made & lost money. I consider this my worst and boring system 🙂 The last version was to reduce clutter.

Its concept is interesting, that why I still put time in it. Version v6p is running only in demo, still positive with around €100 this year. I make a strategy now on a higher timeframes. Minimum 5 minutes and with lost of trades. My best system has 900+ trades and goes way back on 1 hour timeframe, to put it in perspective!

ps maybe change the 2 and 1.5 variables at the entry section. Better modify the code somehow to get better results.

@paul

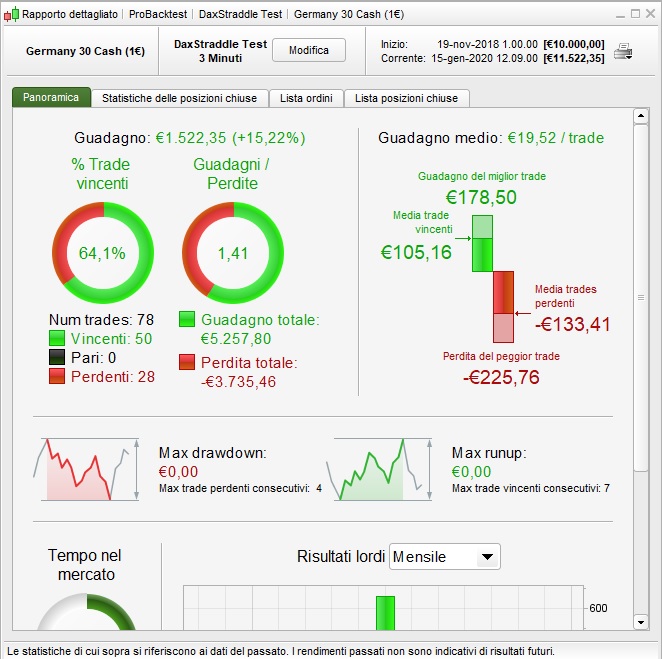

How can you say that a system with this results (around 3 gain loss ratio in the last 200k) is not profitable?

And also, if this is the worst and boring, what is your best? D:

PaulParticipant

Master

@Francesco Petrone I’am not saying the dax dayopen straddle it not profitable, it could be fine for coming months.

I don’t want to put a pic of another strategy here. I will test its robustness later and will post in that topic.

No worries i was just surprised 😀

Btw, this morning the breakeven function did not work, can you check it or is my impression?

No ok that was my impression, doesn’t matter 😀

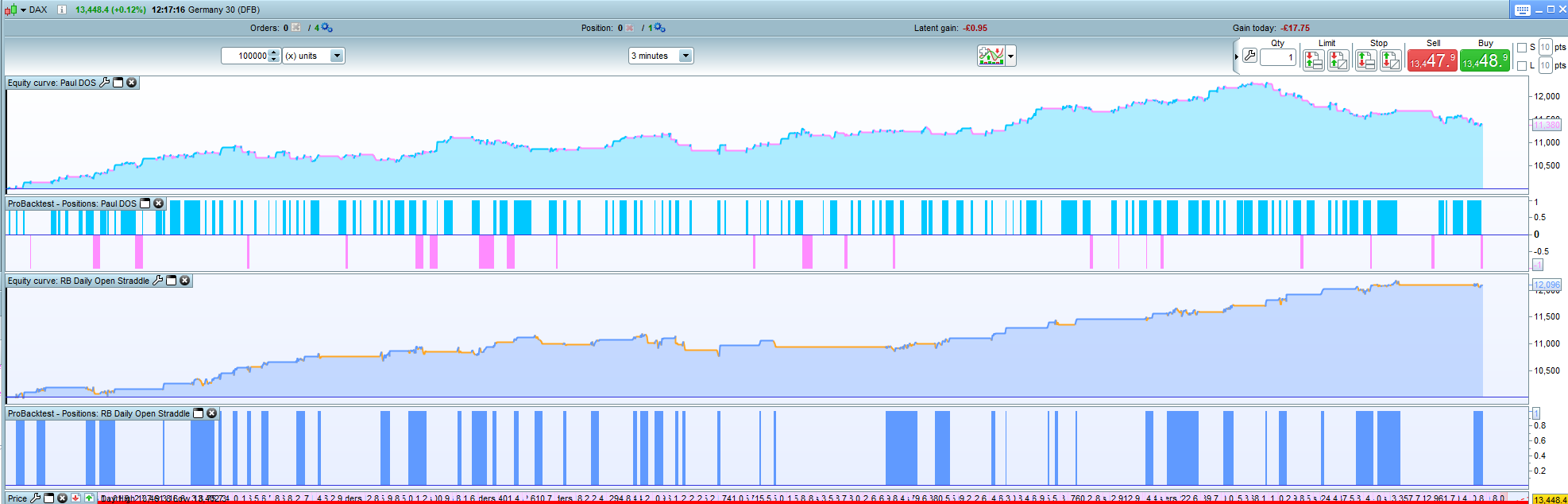

Oddly enough I was looking at this strategy last night, it only works well for long positions

//-------------------------------------------------------------------------

// Main code : DailyOpen Straddle DAX 3minMM

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Main code : Straddle DayOpen

//-------------------------------------------------------------------------

// common rules

DEFPARAM CUMULATEORDERS = false

DEFPARAM PRELOADBARS = 10000

// optional

ExtraTradeCriteria=1

once multiplier=1

once fraction=72

once newlevel=72

once oldlevel=72

once startpositionsize=1

once positionsize=startpositionsize

if strategyprofit>newlevel then

multiplier=multiplier+0.05

oldlevel=newlevel

newlevel=strategyprofit+multiplier*fraction

positionsize=multiplier*startpositionsize

elsif strategyprofit<oldlevel and multiplier>=1 then

newlevel=strategyprofit

oldlevel=strategyprofit-multiplier*fraction

multiplier=multiplier-0.05

positionsize=multiplier*startpositionsize

endif

// positionsize and stops

sl = 1 // % Stoploss 0.6

pt = 0.8 // % Profit Target 0.4

ts = 7 // % MFETrailing

// indicator settigns

NOP=15 //number of points

TimeOpen=080000

// day & time rules

ONCE entertime = TimeOpen

ONCE lasttime = 100000

ONCE closetime = 240000 // greater then 23.59 means it continues position overnight

ONCE closetimeFriday=173000

tt1 = time >= entertime

tt2 = time <= lasttime

tradetime = tt1 and tt2

DayForbidden = 0 // 0=sunday

df = dayofweek <> dayforbidden

// setup number of trades intraday

if IntradayBarIndex = 0 then

longtradecounter = 0

Shorttradecounter = 0

Tradecounter=0

endif

// general criteria

GeneralCriteria = tradetime and df

// trade criteria

tcLong = countoflongshares < 1 and longtradecounter < 1 and tradecounter <1

tcShort = countofshortshares < 1 and shorttradecounter < 1 and tradecounter <1

// indicator criteria

If time = TimeOpen then

DayOpen=open

endif

if IntradayBarIndex = 0 then

lx=0

sx=0

endif

if high > DayOpen+NOP then

lx=1

else

lx=0

endif

if low < DayOpen-NOP then

sx=1

else

sx=0

endif

// trade criteria extra

min1 = MIN(dhigh(0),dhigh(1))

min2 = MIN(dhigh(1),dhigh(2))

max1 = MAX(dlow(0),dlow(1))

max2 = MAX(dlow(1),dlow(2))

If ExtraTradeCriteria then

tcxLong = high < MIN(min1,min2)

tcxShort = low > MAX(max1,max2)

else

tcxLong = high

tcxShort = low

endif

// long entry

If GeneralCriteria then

if lx and tcLong and tcxLong then

buy positionsize contract at market

longtradecounter=longtradecounter + 1

tradecounter=tradecounter+1

endif

endif

// short entry

If GeneralCriteria then

if sx and tcShort and tcxShort then

sellshort 0 contract at market

shorttradecounter=shorttradecounter + 1

tradecounter=tradecounter+1

endif

endif

// MFETrailing

trailingstop = (tradeprice/100)*ts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=trailingstop*pipsize then

priceexit = MAXPRICE-trailingstop*pipsize

endif

endif

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=trailingstop*pipsize then

priceexit = MINPRICE+trailingstop*pipsize

endif

endif

If onmarket and priceexit>0 then

sell at market

exitshort at market

endif

// exit at closetime

If onmarket then

if time >= closetime then

sell at market

exitshort at market

endif

endif

// exit friday at set closetime

if onmarket then

if (CurrentDayOfWeek=5 and time>=closetimefriday) then

sell at market

exitshort at market

endif

endif

// build-in exit

SET TARGET %PROFIT pt

SET STOP %LOSS sl

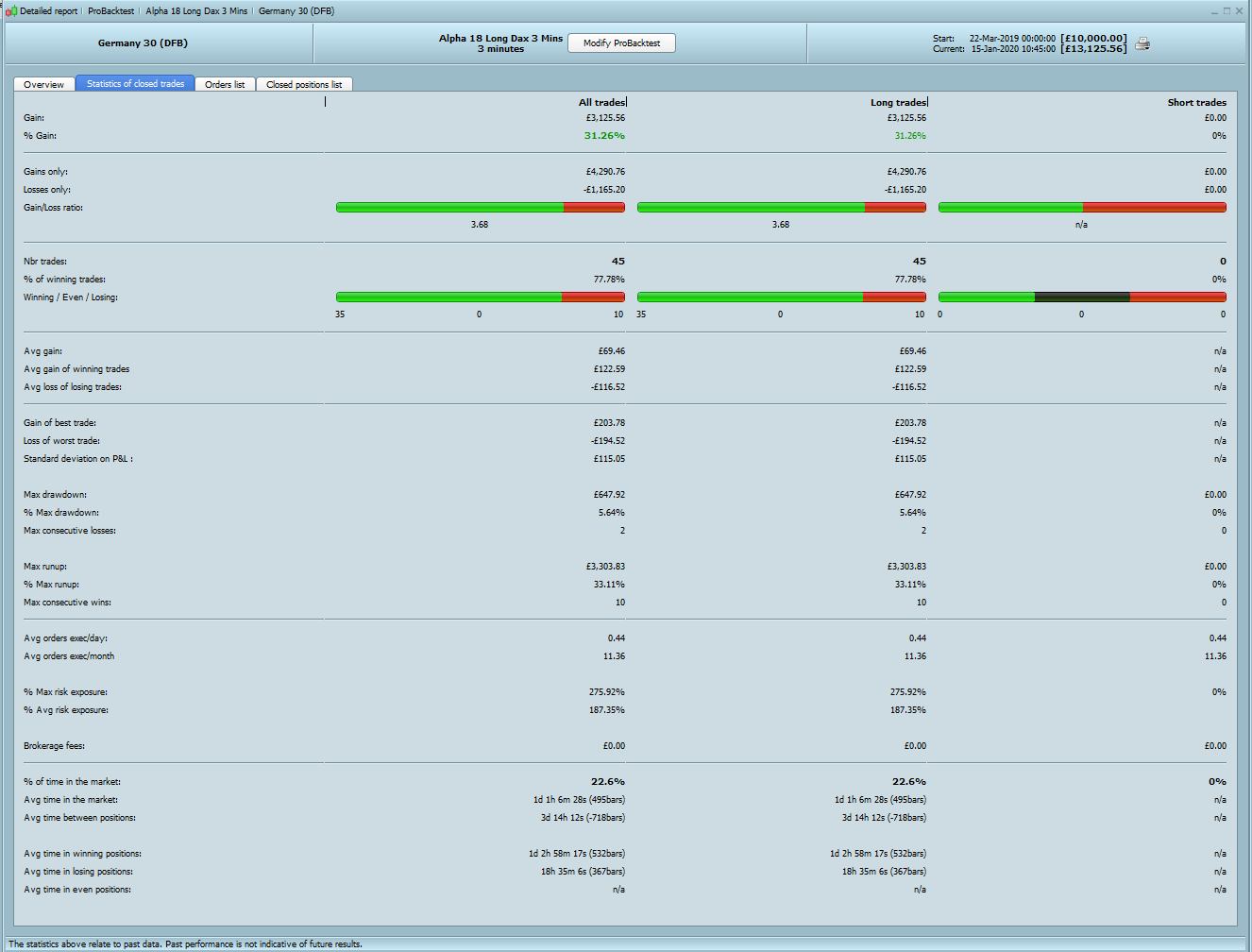

I took the above code live last night, tested over 100k bars with 1 point spread

@RoboFuturesTrader

Tested on 200k on 3min and 1min timeframe, does not look good as the last paul’s version

Please ignore the first 2 screenshots I hadn’t changed the opening time

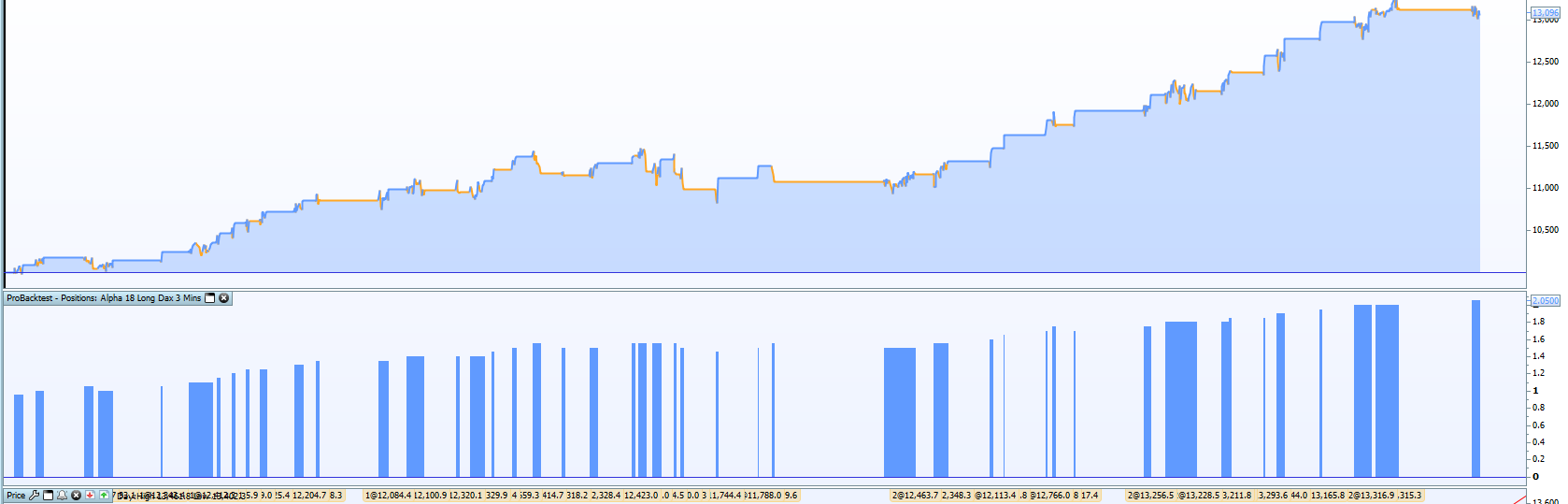

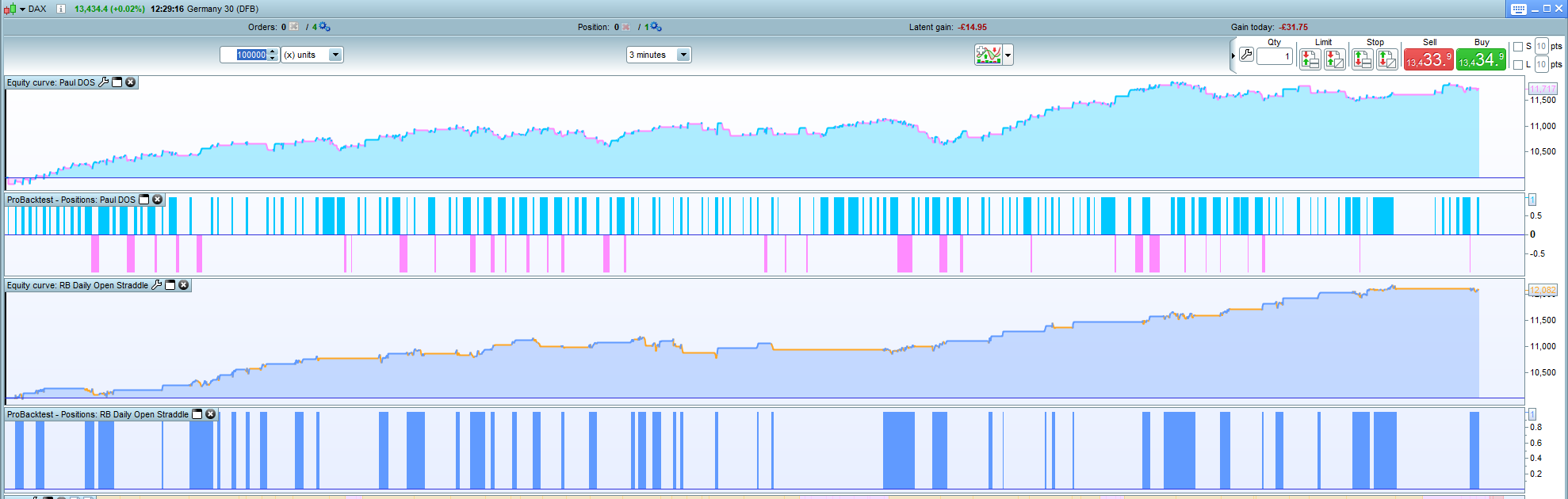

The systems side by side at 3 mins over 100k bars are shown in images 5 & 6 and I have turned off the money management so that we are both using one point per pip

I chose the parameters that allowed for a smoother curve so you can see that my system has taken around 1/3 of the trades of Pauls system

Mine is based from Pauls original posting so I am keen to test the new code and new time frames

They are really two versions of the same system and when I looked down the optimisation report I preferred this version of the system, I have around 20 systems running now so I prefer to have fewer trades with a higher Gain/Loss ratio to help with management of capital

More great work from @Paul for the community

Latest version of Paul works on 1min timeframe not on 3min.

With that scenario, compared to the screen of your version, you have a slightly better ratio on gains, but the number of trades is less than half as you said.

OT: You’re not working anymore on your blog? I would have liked to read you.

Ah okay I will test on 1 Minutes, yes still working on the blog I just need to finish to the robo futures trader process section before developing the main blog

If you sign up for the newsletter here https://robofuturestrader.com/newsletter-sign-up/ then I will be sending out updates

To be honest it may end up as a vlog as I hate writing…….. not sure if you would have a preference of text/video or both

Subscribed to your newsletter immediately, and i started to follow you on insta too.

Well, personally i prefer vlogs, and if your goal is to have a good niche I think they are the most functional thing.

Thanks Francesco

On the Daily Straddle topic is did some work on it last night and it reminded me why I don’t like 1 min systems, with only having 100k bars there just isn’t enough of a trading period to make a decision on the system so I will probably get a version up and running in demo and revisit it in the summer. I had the same problem with the code below (can’t find the original link now) in that it looked great for Dax and Brent for 3 months but then flipped when I began testing

DEFPARAM FLATBEFORE=090100

// Festlegen der Code-Parameter

DEFPARAM CumulateOrders = false // Kumulieren von Positionen deaktiviert

// einmalige werte

once size = 0.5

once profi = 20

once in = 1

once korrek = 1

sl = 35

// Verhindert das Trading an bestimmten Wochentagen

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

noEntryAfterTime = 100000

timeEnterAfter = time < noEntryAfterTime

// einen trade nur

IF (CurrentTime = 010000) then

onetrade = 0

ENDIF

// Bedingungen zum Einstieg in Long-Positionen

IF (CurrentTime = 085900) then

high7 = HIGHEST[120](high)

low7 = LOWEST[120](low)

ENDIF

IF (close > high7) AND (CurrentTime >= 090100) then

onetrade = 1

ENDIF

IF (CurrentTime >= 090100) AND not daysForbiddenEntry AND (onetrade = 0) AND timeEnterAfter THEN

BUY size CONTRACT AT high7 STOP

ENDIF

IF (LONGONMARKET = 1) then

onetrade = 1

in = 1

korrek = 0

//l1 = POSITIONPRICE + 0.0008

l2 = POSITIONPRICE - sl

//sell at l1 LIMIT

sell at l2 stop

ENDIF

// Bedingungen zum Einstieg in Short-Positionen

IF close < low7 AND (CurrentTime >= 090100) then

onetrade = 1

ENDIF

IF (CurrentTime >= 090100) AND not daysForbiddenEntry AND (onetrade = 0) AND timeEnterAfter THEN

SELLSHORT size CONTRACT AT low7 STOP

ENDIF

IF (SHORTONMARKET = 1) then

onetrade = 1

in = 1

korrek = 0

//s1 = POSITIONPRICE - 0.0008

s2 = POSITIONPRICE + sl

//EXITSHORT at s1 LIMIT

EXITSHORT at s2 STOP

ENDIF

// korrektur

IF (LONGONMARKET < 1) AND (SHORTONMARKET < 1) then

in = 0

ENDIF

IF in = 0 and korrek = 0 then

d1 = POSITIONPERF(1) > 0

d2 = POSITIONPERF(1) < 0

IF d1 and size > 1 then

size = size - 1

korrek = 1

ELSIF d2 then

size = size + 1

korrek = 1

ENDIF

ENDIF

// Stops und Targets

SET STOP pLOSS 60

SET TARGET pPROFIT sl

// Performance

IF STRATEGYPROFIT > profi then

size = 1

profi = profi + 20

ENDIF