defparam cumulateorders = false

n=2

soglia = 0.02

timestart = 90000

timeend = 180000

profitti = 275

perdite = 350

timeok = time>=timestart and time<=timeend

c = (sin(atan((close-open[n])/open[n]*100/n)))

if c crosses over soglia and timeok then

buy 1 contract at market

endif

if c crosses under -soglia and timeok then

sellshort 1 contract at market

endif

set target pprofit profitti

set stop ploss perdite

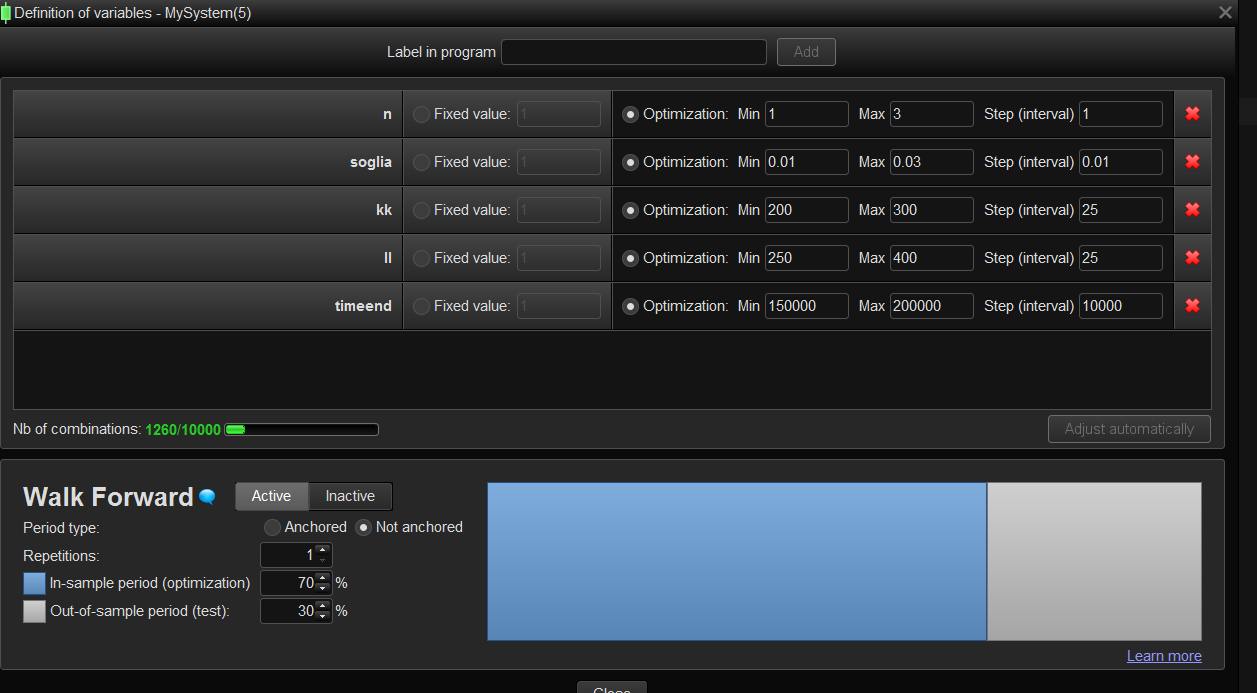

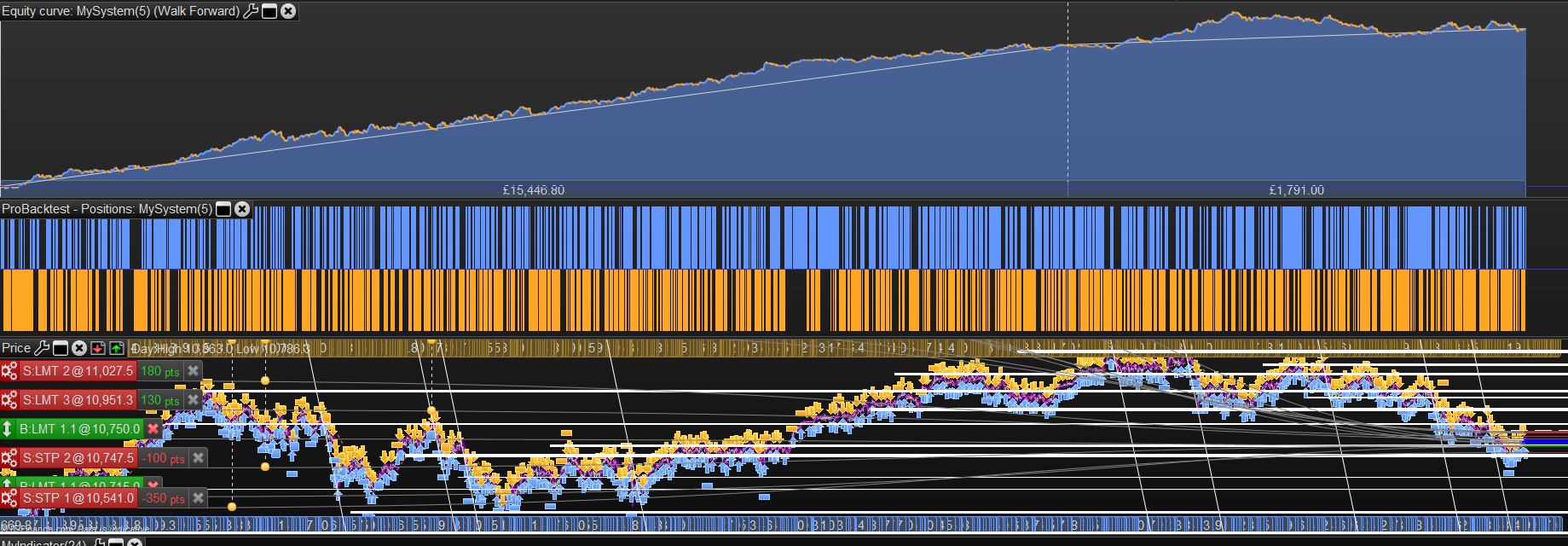

Thanks again Francesco, any WFA to share for this one?

Ok but the optimized variables in your first post are the ones found for a 100% IS optimization? Better to know and explain in the post because people will ask a lot of questions 🙂

Hello Francesco,

Thank you again for another contribution. It is really appreciated.

I have a question, do you optimise all of the data or do you use in-sample and out-of-sample?

Best regards

The first

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

|

defparam cumulateorders = false

n=2

soglia = 0.02

timestart = 90000

timeend = 180000

profitti = 275

perdite = 350

timeok = time>=timestart and time<=timeend

c = (sin(atan((close–open[n])/open[n]*100/n)))

if c crosses over soglia and timeok then

buy 1 contract at market

endif

if c crosses under –soglia and timeok then

sellshort 1 contract at market

endif

set target pprofit profitti

set stop ploss perdite

|

is optimized over the whole set of data.

the second post shows walk forward 75/25

Hope this answer your question

Regards

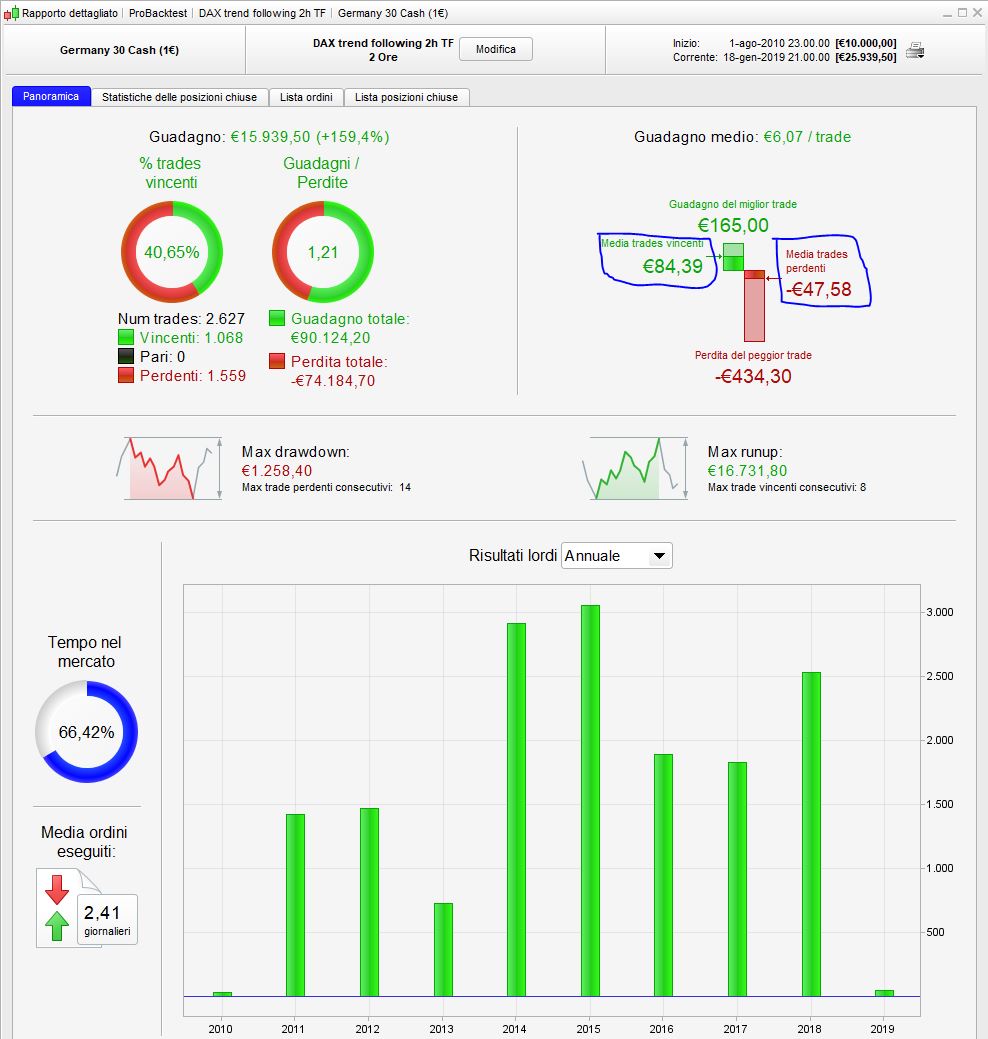

Ciao, i had very different result with 200k bars, but anyway i changed something in the code.

i have 2 questions

in this function

c = (sin(atan((close–open[n])/open[n]*100/n)))

i never seen the command SIN AND ATAN what are they? and how you found them? i the function search of PRT they aren’t presents. Thank you.

This is my version of your code, hoping could help.

defparam cumulateorders = false

//1/TRAILING STOP//////////////////////////////////////////////////////

once trailinstop= 1 //1 on - 0 off

trailingstart = 100 //trailing will start @trailinstart points profit

trailingstep = 60 //trailing step to move the "stoploss"

///2 BREAKEAVEN///////////

once breakeaven = 1 //1 on - 0 off

startBreakeven = 50 //how much pips/points in gain to activate the breakeven function?

PointsToKeep = 30 //how much pips/points to keep in profit above of below our entry price when the breakeven is activated (beware of spread)

n=2

soglia = 0.01

sogliashort=-0.06

timestart = 90000

timeend = 180000

profitti = 165

entratalong=0

entratashort=0

timeok = time>=timestart and time<=timeend

c = ((sin(atan((close-open[n])/open[n]*100/n)))*100)+close

c2 = (sin(atan((close-open[n])/open[n]*100/n)))

graphonprice c

if c>close and c2 > soglia and timeok then

entratalong=high+1*pipsize

sl = (entratalong - low) / pipsize

buy 1 contract at entratalong stop//market

entratalong=0

set target pprofit profitti

set stop ploss sl+10

endif

if c<close and c2<sogliashort and timeok then

entratashort=low-1*pipsize

sl = (high - entratashort) * pipsize

sellshort 1 contract at entratashort stop

entratashort=0

set target pprofit profitti

set stop ploss sl+10

endif

///1///////////////////////////////////////////////

//reset the breakevenLevel when no trade are on market

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

//2////////////////////////////

//test if the price have moved favourably of "startBreakeven" points already

if breakeaven>0 then

IF onmarket AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

endif

//************************************************************************

//trailing stop function

if trailinstop>0 then

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

endif

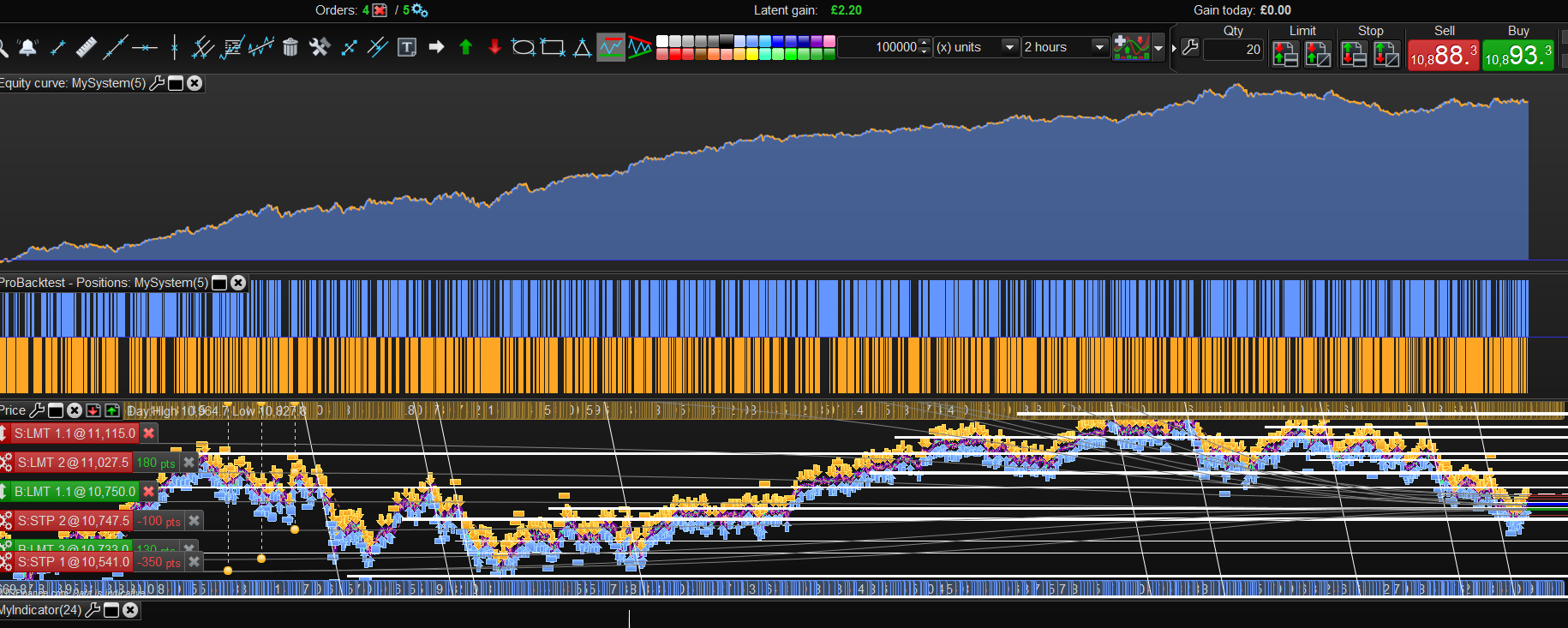

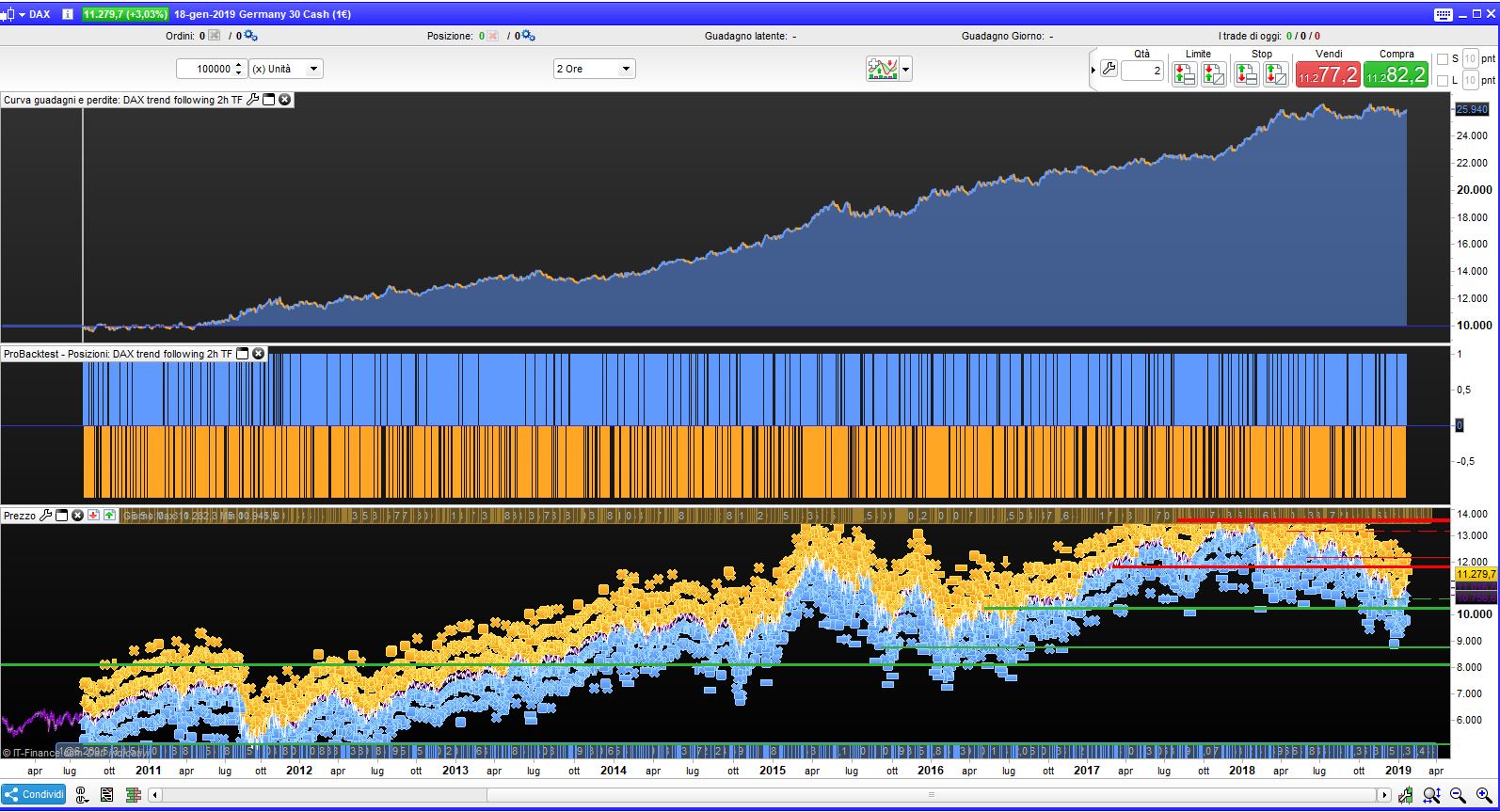

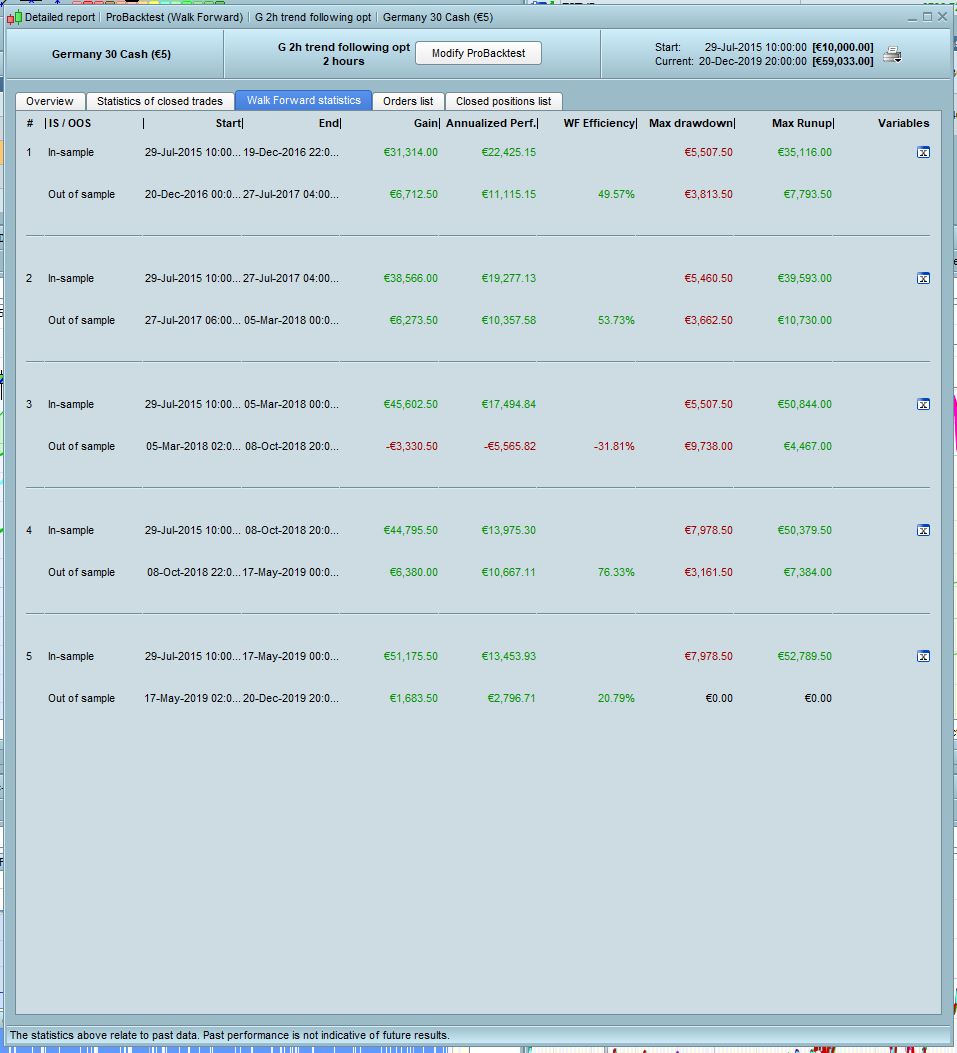

[attachment file=”89168″]

[attachment file=”89169″]

Ciao Francesco, I have added a trailing stop to your code which seems to help but I’m unclear about the WFE. See the screen shots below, does this look over-optimized?

This is my version:

defparam cumulateorders = false

n=2

soglia = 0.02

timestart = 90000

timeend = 180000

profitti = 280

perdite = 340

timeok = time>=timestart and time<=timeend

c = (sin(atan((close-open[n])/open[n]*100/n)))

if c crosses over soglia and timeok then

buy 1 contract at market

endif

if c crosses under -soglia and timeok then

sellshort 1 contract at market

endif

set target pprofit profitti

set stop ploss perdite

//trailing stop function

trailingstart = 57 //trailing will start @trailinstart points profit

trailingstep = 1 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF