AE

AEParticipant

Senior

Hi guys,

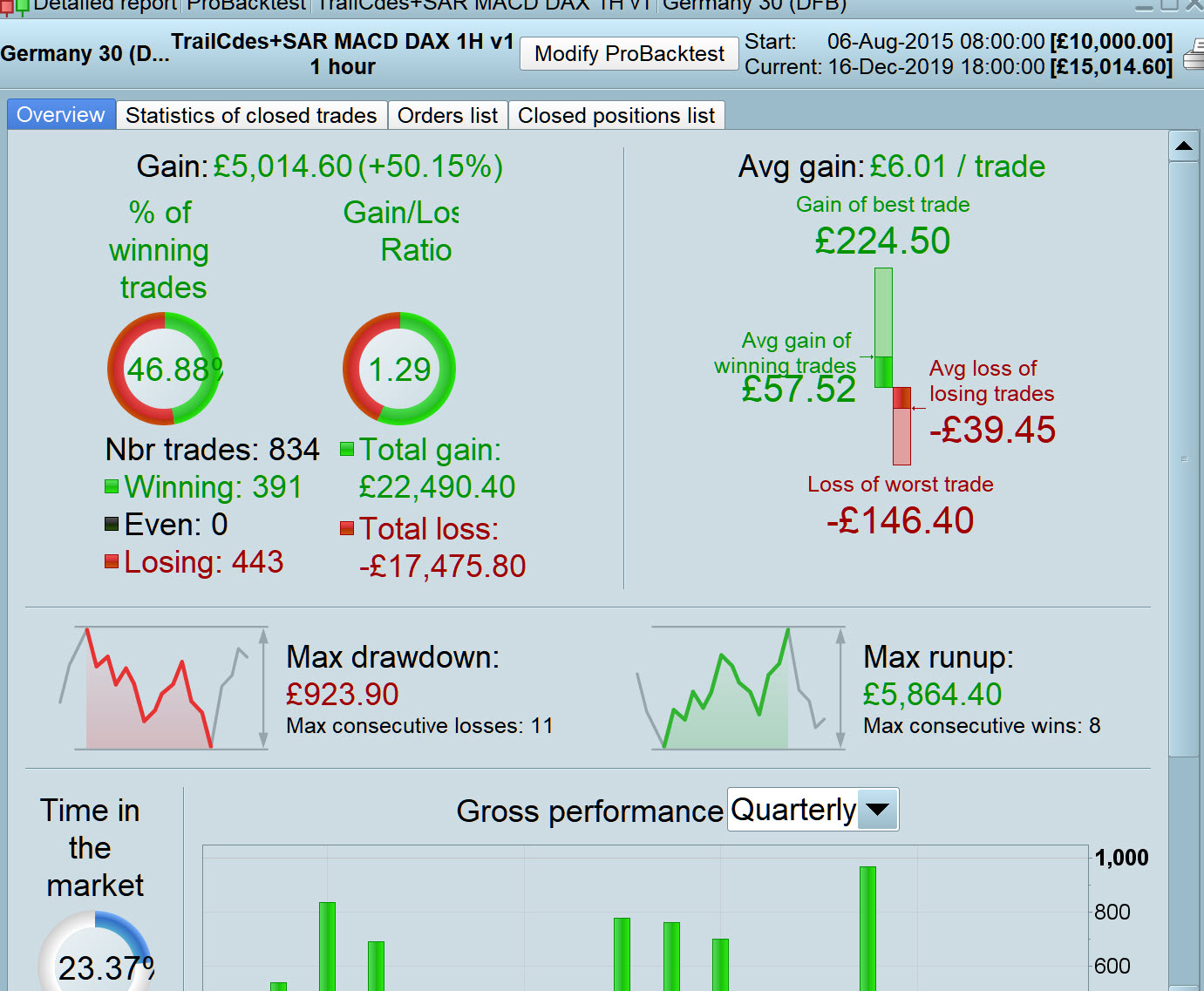

Let me show you this simple strategy using SAR. It use a simple SAR with two filters (stochastic and macd) to select better operations.

I have a lot of fake signals but anyway winners are better than lossers so it make money.

It works for DAX 1h.

Any idea to improve this strategy?

// Definición de los parámetros del código

DEFPARAM CumulateOrders = False // Acumulación de posiciones desactivada

// Condiciones para entrada de posiciones largas

parabolic = SAR[0.02,0.02,0.2]

sto = Stochastic[5,3](close)

signal = average[3](sto)

mac = MACD[12,26,9](close)

c1 = (parabolic < close)

c2 = (signal > 50)

c3 = (parabolic[1] > close[1])

IF c1 AND c2 AND c3 and mac >0 THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Condiciones de salida de posiciones largas

c4 = (close < parabolic)

IF c4 THEN

SELL AT MARKET

ENDIF

c5 = (parabolic > close)

c6 = (parabolic[1] < close[1])

if not c2 and c5 and c6 and mac < 0 then

Sellshort 1 contract at market

endif

c7 = (close > parabolic)

IF c7 THEN

EXITSHORT AT MARKET

ENDIF

SET STOP pTRAILING 55

Thanks for sharing with us online.

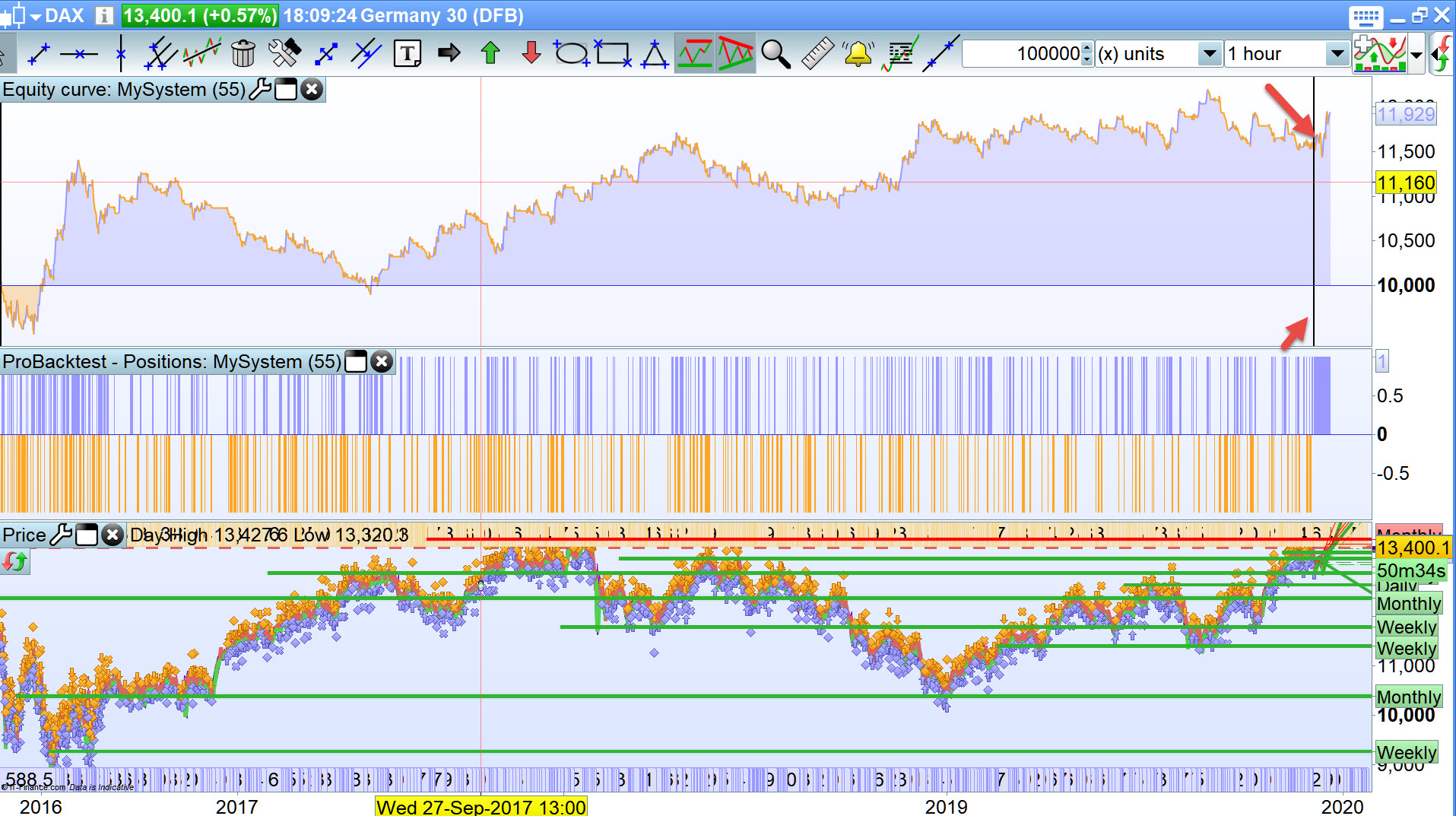

With TS = 55, I get attached error message and the Strategy stopped at the red arrowheads.

Do you get same over 100k bars?

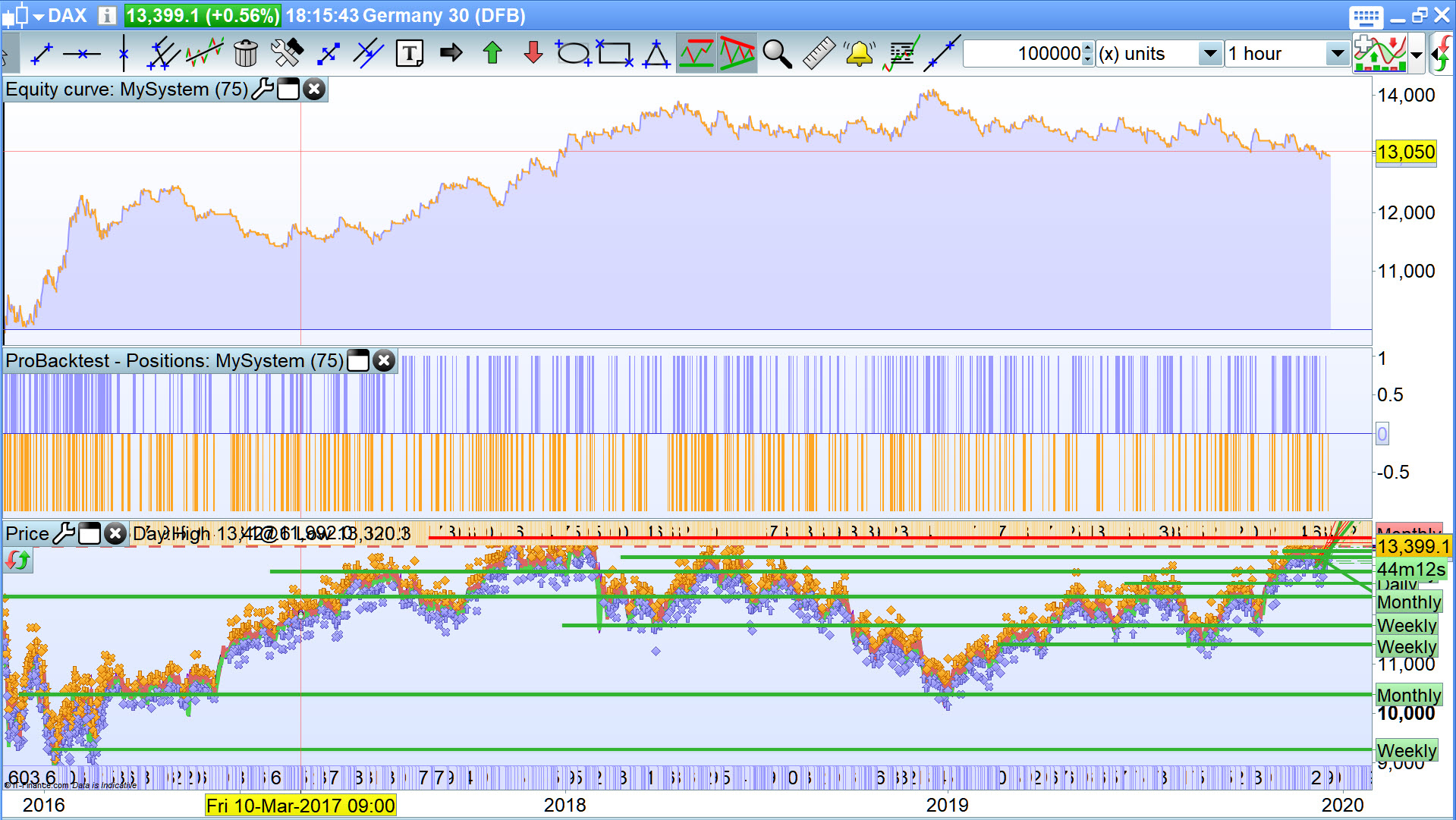

But with TS = 75 I get attached … much better! 🙂

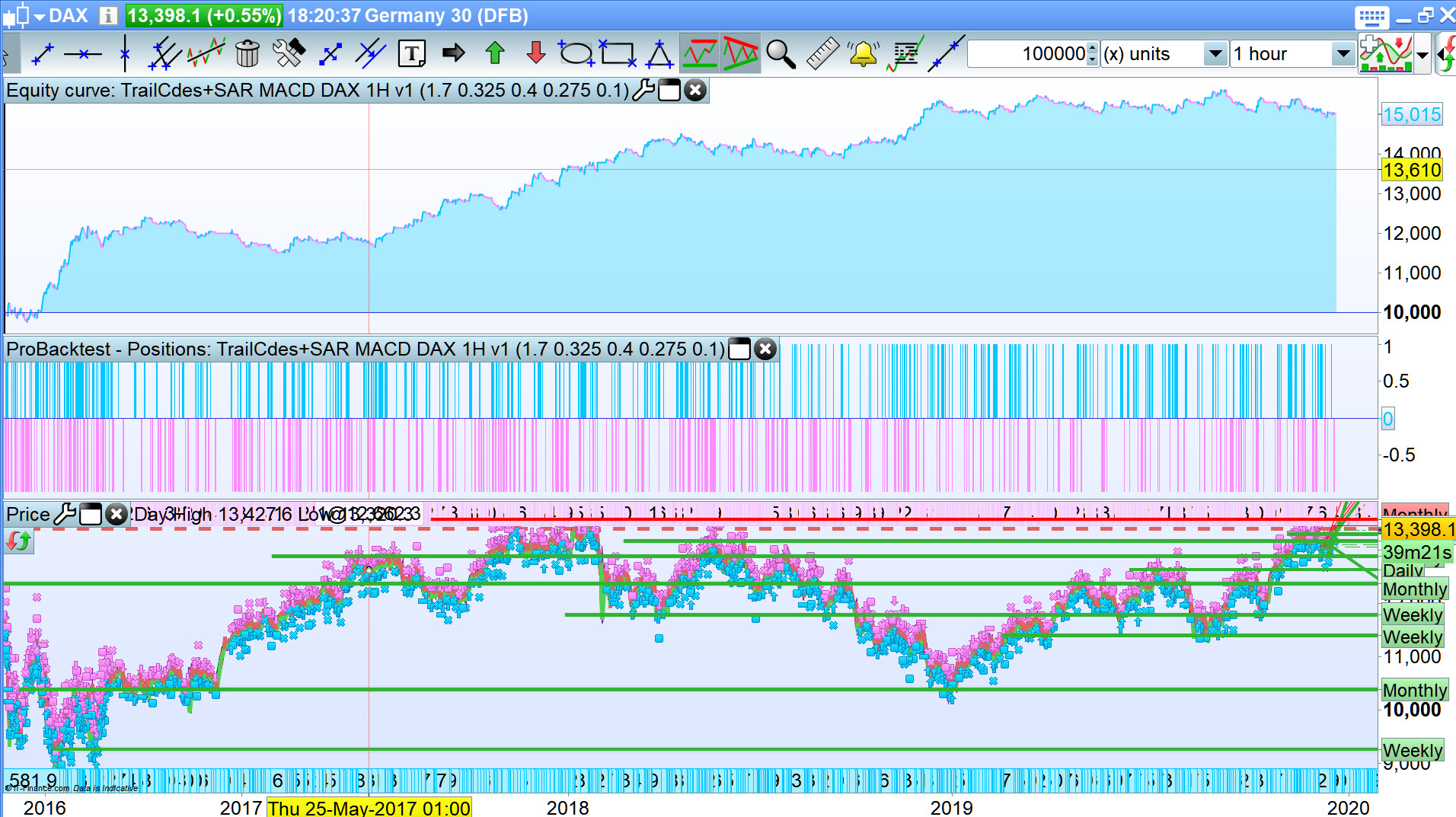

And using the TS code found at Log 65 here …

Snippet Link Library

I get attached … better again! 🙂

AEParticipant

Senior

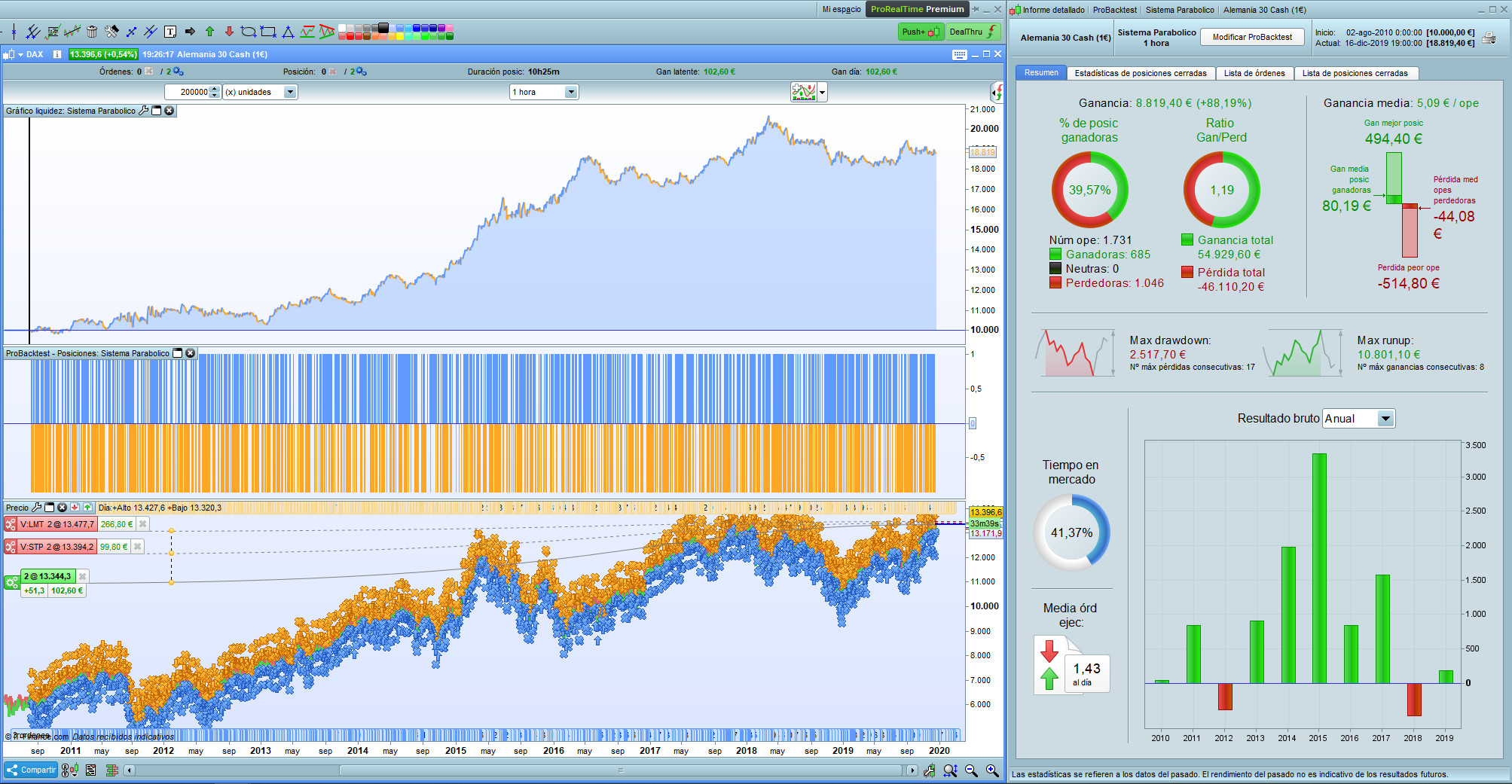

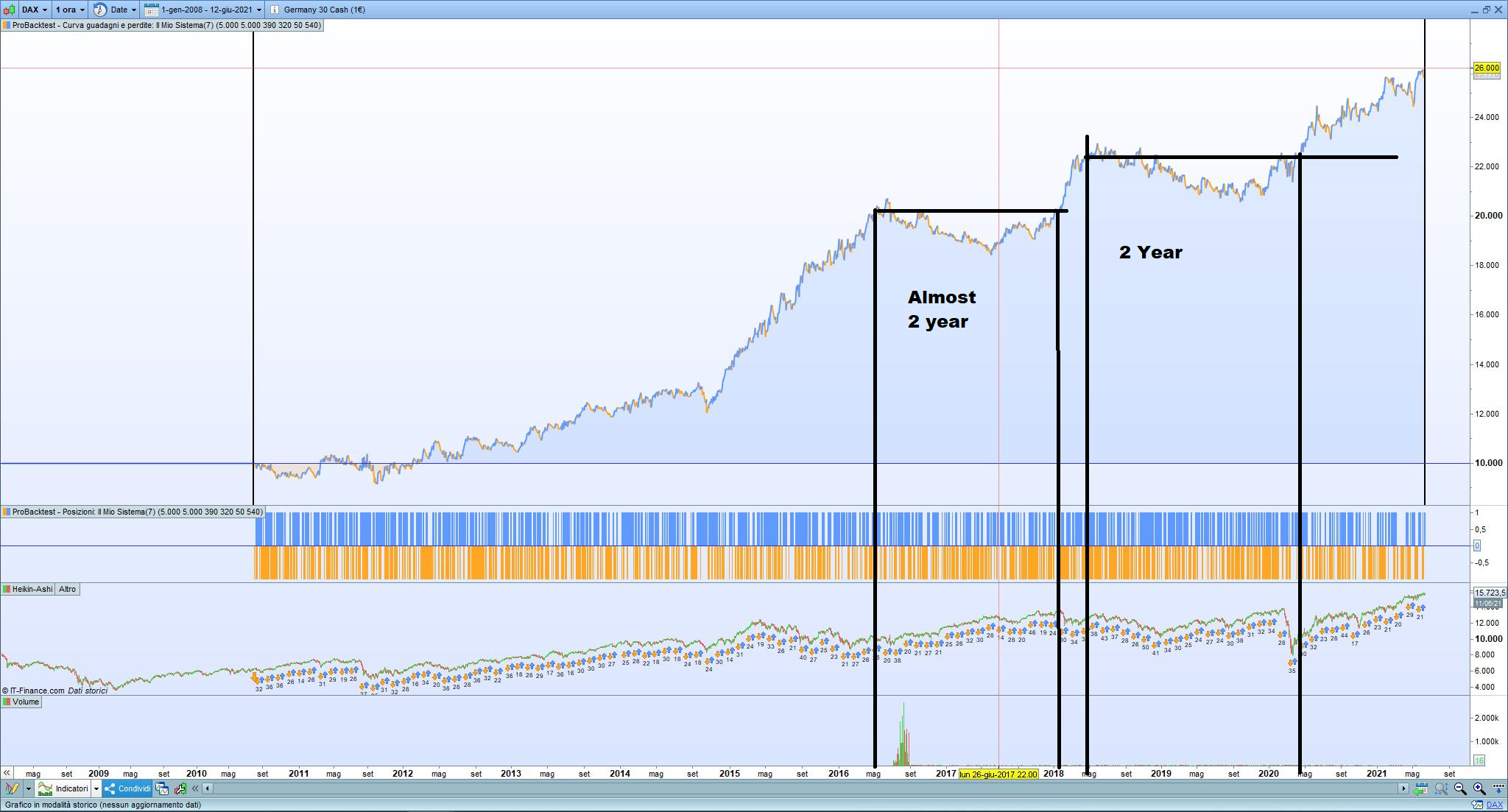

In deed, with no TS you will get the best result, but the DD is more high. Check the picture

Ideas to improve it? 😀

With TS = 55, I get attached error message and the Strategy stopped at the red arrowheads.

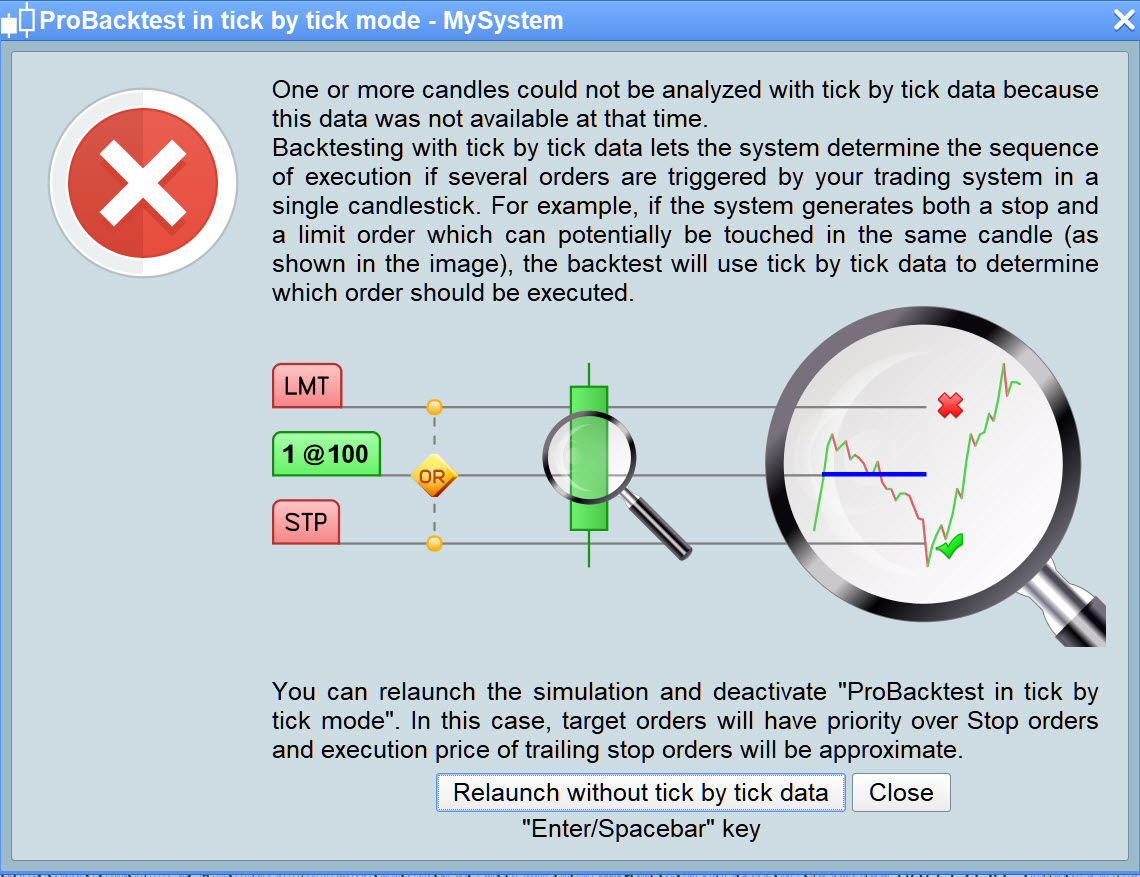

You’ve unfortunately hit on a tick by tick data hole. I see this error quite often on the DJI daily when using tick by tick because there is a day sometime in 2010 that has data problems or no tick by tick and if a trade happens to be open on this day then the strategy crashes and gives me that error message.

Thank you Vonasi … I had no thoughts on what had caused the stoppage … ‘tick by tick data hole’ … I like it (well only the description! 🙂

Hello.

Forgive my ignorance and my English, I am new.

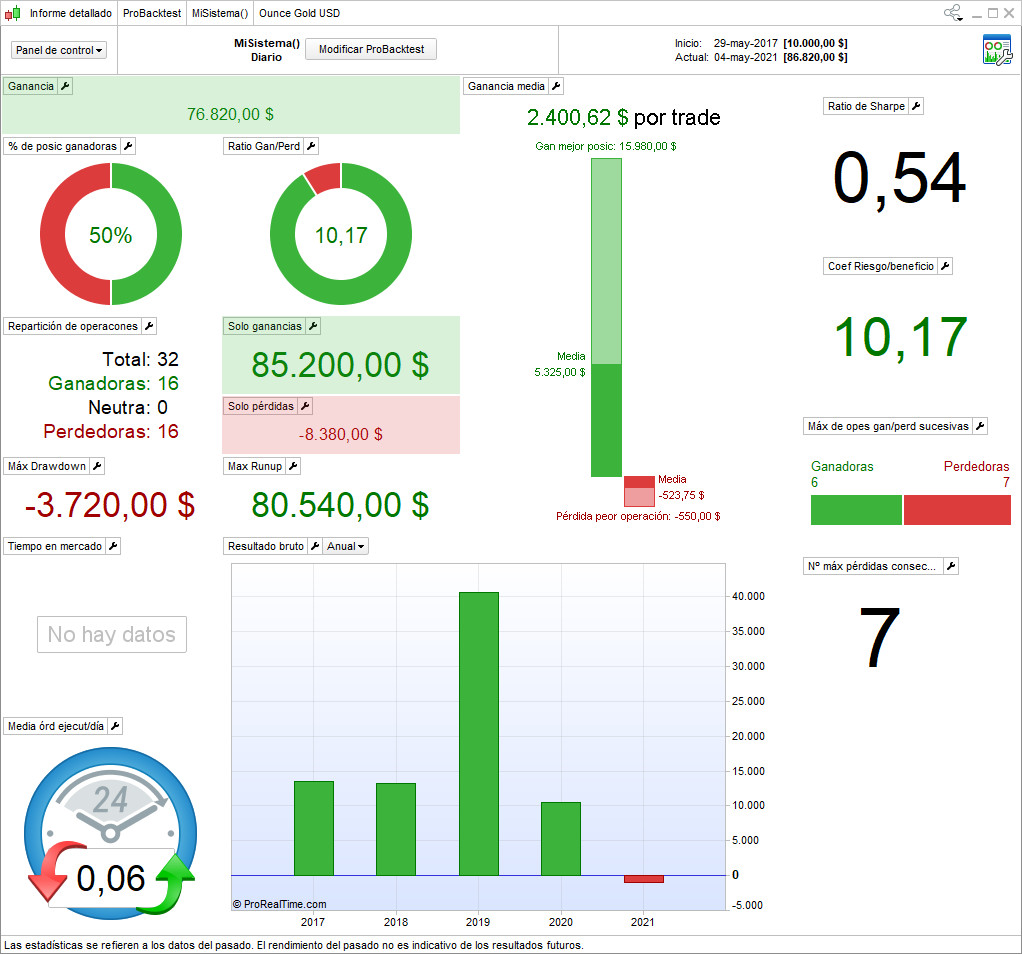

Applying it to Gold I get this (photo attached).

As you see ???. Thanks. Greetings.

@DECO2021

What’s your question exactly, is it too good to be true or is it not as good as expected?

Did you include spread?

Did you use tick-by-tick mode?

How many lots/contracts did you trade each time?

Please post the ITF file you have used.

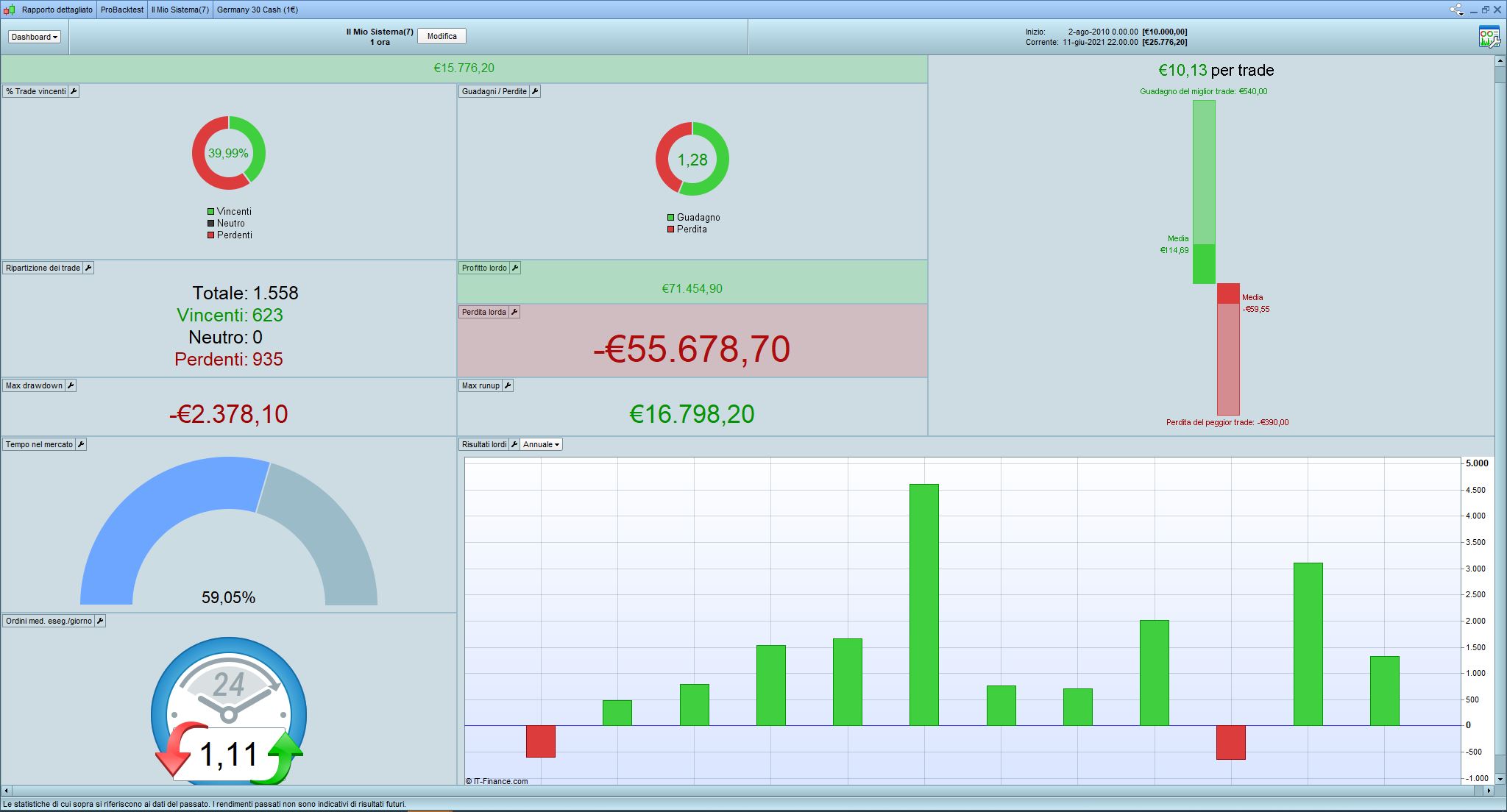

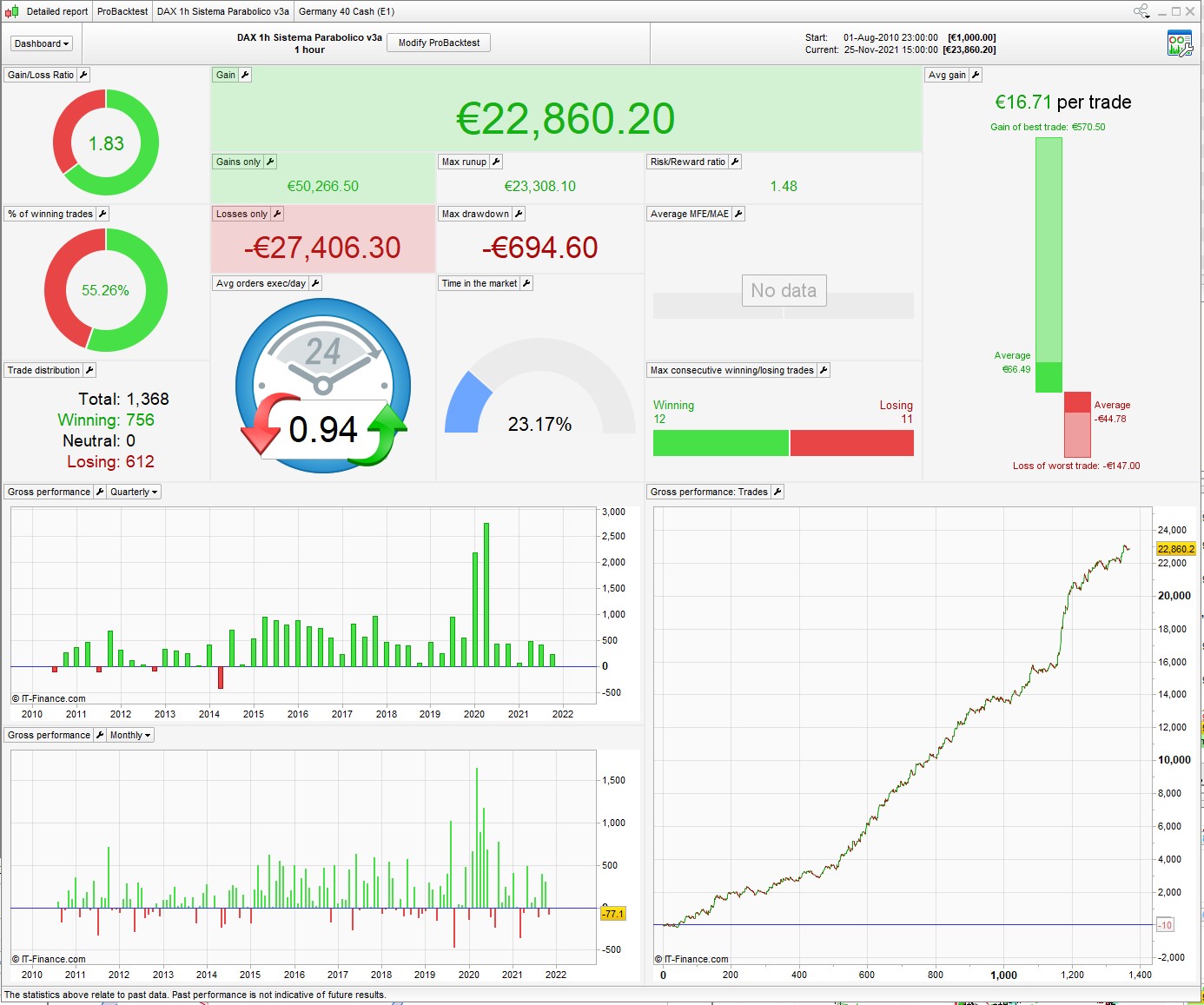

Hi, I’d improved this system with fix stop loss and take profit and Nicolas’s trailing stop. I add a condition that close trade on friday after time that I setted.

I attach file and images of equity and report. In my opinion we have to filter much better, because there are a lot of trade and we have to consider overnight costs (if someone expert coder can do that).

I backtested this system from 2010 to now with tick by tick mode with 2point spread.

I came across this in the library – thanks to AE for sharing.

Made a few changes, tweaked the numbers here and there, I’m sure there’s still room for improvement.

***Optimized on 100% of data so still needs out of sample testing***

No reason this shouldn’t be re-optimized for the NAS, SP etc.

// 25/11/21

DEFPARAM CumulateOrders = False // Acumulación de posiciones desactivada

DEFPARAM preloadbars = 10000

positionsize=1

Timeframe (4 hours)

ma = average[p,t](typicalprice)

cb1 = ma > ma[1]

mb = average[p2,t2](typicalprice)

cs1 = mb < mb[1]

Timeframe (default)

parabolic = SAR[q,w,e]

parabolicS = SAR[qs,ws,es]

sto = Stochastic[s1,s2](close)

signal = average[av,t3](sto)

mac = MACD[m,a,c](close)

cb2 = (close > parabolic)

cb3 = (close[1] < parabolic[1])

cs2 = (close < parabolicS)

cs3 = (close[1] > parabolicS[1])

cb4 = (signal > l)

cs4 = (signal < s)

//Stochastic RSI | indicator

lengthRSI = lr //RSI period

lengthStoch = ls //Stochastic period

smoothK = sk //Smooth signal of stochastic RSI

smoothD = sd //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

cb5 = K>D

cs5 = K<D

//Volatility Filter

Vol = (Std[v1](Close) / Close) * 100

cb6 = Vol < v2

cs6 = Vol < v3

CB = cb1 AND cb2 AND cb3 and cb4 and cb5 and cb6 and mac >0

CS = cs1 AND cs2 AND cs3 and cs4 and cs5 and cs6 and mac <0

IF CB THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

ENDIF

// Condiciones de salida de posiciones largas

IF cs2 THEN

SELL AT MARKET

ENDIF

if CS then

Sellshort positionsize contract at market

SET STOP %LOSS sls

SET TARGET %PROFIT tps

endif

IF cb2 THEN

EXITSHORT AT MARKET

ENDIF

// %trailing stop function incl. cumulative positions

once trailingstoptype1= 1

if trailingstoptype1 then

//====================

trailingpercentlong = tsl // %

trailingpercentshort = tss // %

once acceleratorlong = a1 // [1] default; always > 0 (i.e. 0.5-3)

once acceleratorshort= a2 // 1 = default; always > 0 (i.e. 0.5-3)

ts2sensitivity = 2 // 1 = close 2 = High/Low 3 = Low/High 4 = typicalprice (not use once)

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=typicalprice

ts2sensitivityshort=typicalprice

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong then

newsl = positionprice+trailingsteplong

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong then

newsl = newsl+trailingsteplong

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort then

newsl = positionprice-trailingstepshort

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort then

newsl = newsl-trailingstepshort

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

//*****************************************

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF longonmarket and (barindex-tradeindex(1)>= b1 and positionperf>0) or (barindex-tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF shortonmarket and (barindex-tradeindex(1)>= b3 and positionperf>0) or (barindex-tradeindex(1)>= b4 and positionperf<0) then

exitshort at market

endif

endif

//===================================

RSIexit = 1 // in profit

if RSIexit then

myrsi2=rsi[r](close)

if myrsi2<rl and barindex-tradeindex>1 and longonmarket and positionperf>0 then

sell at market

endif

if myrsi2>rs and barindex-tradeindex>1 and shortonmarket and positionperf>0 then

exitshort at market

endif

endif

Hi – like the look of the results. Was wondering, if you optimise on 100% of the data wouldn’t this effectively curve fit the results shown? So a higher risk that it may fall flat once live? Trying to learn – thanks

that’s why it needs out of sample testing. put it on demo for a few months, see what happens.

Or, you can do your own 70/30 optimization if you prefer.

I find testing in demo to be more reliable as it more closely resembles real trading conditions (changes in the spread, overnight fees etc)

That’s a good point. I have done the same, optimised a strategy on a 70/30 split then run in demo, and finally launched in an incubation phase on small size to test for a period of time. The issue is that the live trades don’t always match up to the back test trades (some trades are completely missing or there is a difference in profit/loss that is greater than the spread).

After all that I look to only keep those strategies which have a 90% or greater match between back test and live results. Optimising becomes dangerous if used excessively, but even still you will always get a difference between live and back test.