Thank you for code.

I found a little bit better result with:

- max size for stop loss

- different values for adxval and atrmin between morning and afternoon (US open time 2:30PM or 3:30pm).

Regards

Thanks a lot Noisette, what do you mean by max size for stop loss?

Sorry, I mean max value fo stop loss.

Try to add:

If pl > xxx then

Pl = xxx

Endif

Best value for xxx seems to be around 80~85 points.

Regards.

My WF analysis has been stucked by the 12 hours limitations .. I should consider reduce the variables values ranges..

Anyway, @Noisette, could you kindly post here your settings to discuss about? Thanks.

Hi Nicolas,

yes unfortunatley there are a few variables.

I can suggest this variable ranges:

ADXVAL [18:28, 2]

M,N,M1,N1 = [1:4,1]

k,y [3:10,1]

atrmin :[15:40,5]

timestart and timeend I think can be optimized later, they dont have a big impact.

Hope this help

@Francesco78 sorry for taking so long to respond, been very busy with work!

Yes I’ve been running the 30 min and 1hr on my live account and had good results, although I have to admit that I tend to close positions manually when they show a good profit… Although I also run the same systems on my demo account too.

As for the optimisation are those variables you posted recently the ones to optimise for? I am just trying to understand the logic of the system so I can play around with it, once the volatility has been determined does it simply enter at a multiple of the ATR? What made you think to try a system such as this?

Once again thanks a lot and great work! 🙂

Here the modified code:

- Different values morning vs afternoon

- Maximum value for stop loss

- Positions can be stopped later (20h instead of 17h30)

I think that we can add trailing stop (Nicolas code) to improve this code.

Regards.

// dax - IG MARKETS

// TIME FRAME 30min

// SPREAD 1.0 PIPS

DEFPARAM CumulateOrders = False

DEFPARAM FLATBEFORE = 070000

DEFPARAM FLATAFTER = 200000

ONCE POSITION =1

timestart = 080000

timeend = 173000

timeenterbefore = time <= timeend

timeenterafter = time >= timestart

//highvolume = average[30](volume)<=volume//

//lowvolume = average[30](volume)>=volume

adxperiod =15//15

atrperiod = 17//17

indicator1 = adx[adxperiod]

atr = AverageTrueRange[atrperiod]

//exitafternbars = 1

//// OPTIMIZED VARIABLES/////

K = 8 //8

Y = 3 //5

MAXPL = 80

AFTERNOON = 143000

IF TIME < AFTERNOON THEN

adxval = AA//20//20

atrmin = BB//27//19

m = 3 // high vol coefficient for mean reversion

n = 2 //high vol coefficient for breakout

Z = 1 //1.4

ELSE

adxval = CC//26//20

atrmin = DD//22//19

m = 3 // high vol coefficient for mean reversion

n = 2 //high vol coefficient for breakout

Z = 1 //0.8

ENDIF

m1 = m- Z //1 // low vol coefficient for mean reversion

n1 = n// low vol coefficient for breakout

pr = K*atr

pl = Y*atr

IF PL > MAXPL THEN

PLL = MAXPL

ELSE

PLL = PL

ENDIF

///////////////////////////////////////

lowvolenvironment = atr<atrmin //define lowvol environment use m1 and n1 as coefficient of movement

highvolenvironment = atr> atrmin //define highvol environment use m and n as coefficient of movement

meanrevertingenv = indicator1< adxval //define meanreverting environment

trendenv = indicator1 > adxval// define trendy environment

//////description of the possible combinations

sellhighvolmeanreverting = abs(open-close) > (atr*m) and close > open and meanrevertingenv and highvolenvironment

buyhighvolmeanreverting = abs(open-close) > (atr*m) and close < open and meanrevertingenv and highvolenvironment

buyhighvoltrendy = abs(open-close) > (atr*n) and close > open and close> DOPEN(1) and trendenv and highvolenvironment

sellhighvoltrendy = abs(open-close) > (atr*n) and close < open and close< DOPEN(1) and trendenv and highvolenvironment

selllowvolmeanreverting = abs(open-close) > (atr*m1) and close > open and meanrevertingenv and lowvolenvironment

buylowvolmeanreverting = abs(open-close) > (atr*m1) and close < open and meanrevertingenv and lowvolenvironment

buylowvoltrendy = abs(open-close) > (atr*n1) and close > open and trendenv and lowvolenvironment

selllowvoltrendy = abs(open-close) > (atr*n1) and close < open and trendenv and lowvolenvironment

////////////////////////////////////////////////////////

//long

IF (buyhighvolmeanreverting or buyhighvoltrendy or buylowvolmeanreverting or buylowvoltrendy ) and timeenterbefore and timeenterafter THEN

buy POSITION CONTRACTS AT MARKET

ENDIF

// short

IF (sellhighvolmeanreverting or sellhighvoltrendy or selllowvolmeanreverting or selllowvoltrendy) and timeenterbefore and timeenterafter THEN

sellshort POSITION CONTRACTS AT MARKET

ENDIF

IF TIME > TIMEEND AND LONGONMARKET AND (sellhighvolmeanreverting or sellhighvoltrendy or selllowvolmeanreverting or selllowvoltrendy) THEN

SELL AT MARKET

ENDIF

IF TIME > TIMEEND AND SHORTONMARKET AND (buyhighvolmeanreverting or buyhighvoltrendy or buylowvolmeanreverting or buylowvoltrendy ) THEN

EXITSHORT AT MARKET

ENDIF

@Francesco78

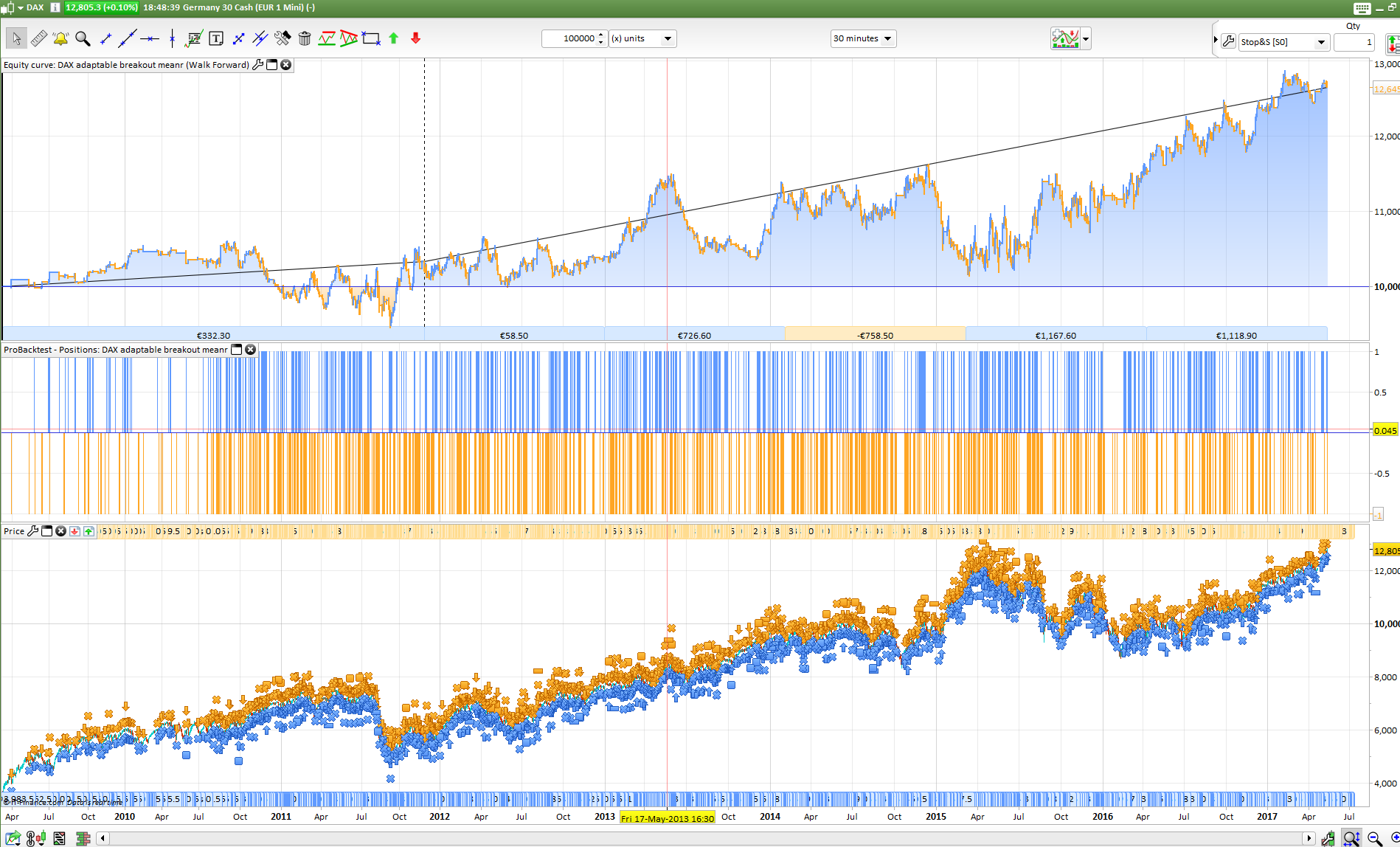

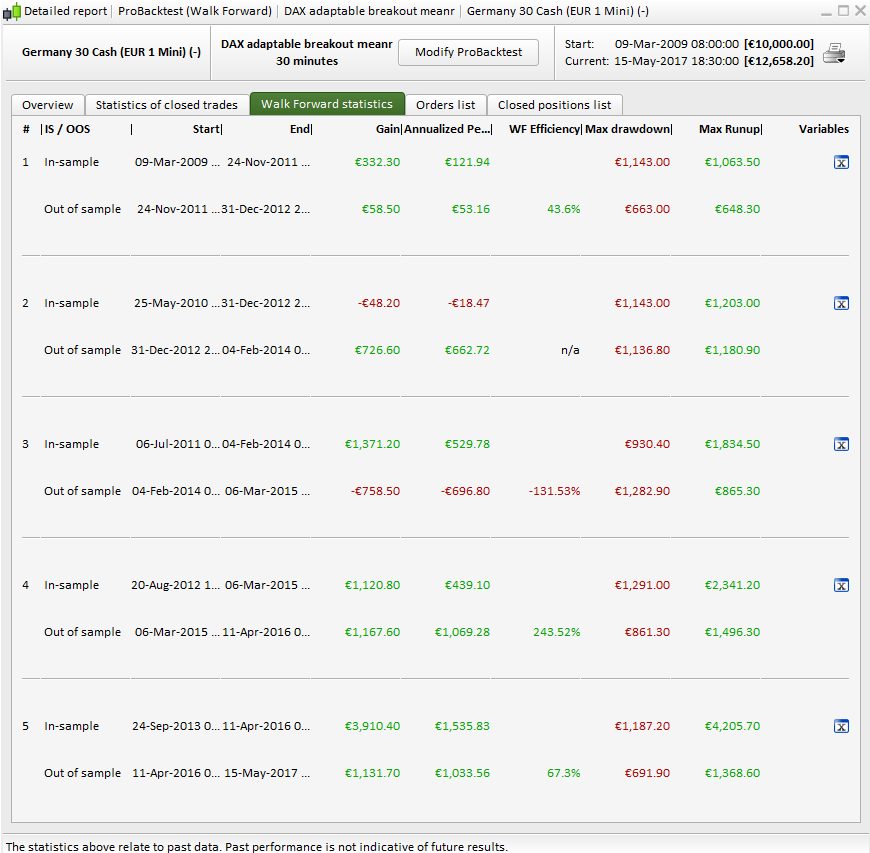

I ran a 5 iterations Walk Forward analysis yesterday (on 100k bars only) with the variables ranges you gave me (for the 30 minutes version), PFA the results. Even if the equity curve is not steady, the WF study is not so “critical”. Remember that in its current state, the WF tool only give the result of the most profitable OOS settings at the end, it doesn’t mean that other settings wouldn’t have made a more “steady” curve..

Thank you very much Noisette will have a look this afternoon.

Thanks Nicolas for your time spent on the code. Just for my info can you tell me which version of the code you used for the wf? Thanks again

I used this one:

// dax - IG MARKETS

// TIME FRAME 30min

// SPREAD 1.0 PIPS

DEFPARAM CumulateOrders = False

timestart = 080000

timeend = 200000

timeenterbefore = time <= timeend

timeenterafter = time >= timestart

adxperiod = 14

atrperiod = 14

myADX = adx[adxperiod]

atr = AverageTrueRange[atrperiod]

//// OPTIMIZED VARIABLES/////

profitCoeff = 8

lossCoeff = 5

myprofit = profitCoeff*atr

myloss = lossCoeff*atr

//adxval = 20

//atrmin = 19

m = 3 // high vol coefficient for mean reversion

n = 2 //high vol coefficient for breakout

m1 = m-1 // low vol coefficient for mean reversion

n1 = n // low vol coefficient for breakout

///////////////////////////////////////

positionlong = 1 // define sixe of long trades

positionshort = 1 // define size of short trade

lowvolenvironment = atr < atrmin //define lowvol environment use m1 and n1 as coefficient of movement

highvolenvironment = atr > atrmin //define highvol environment use m and n as coefficient of movement

meanrevertingenv = myADX < adxval //define meanreverting environment

trendenv = myADX > adxval // define trendy environment

//////description of the possible combinations

//mean reverting

sellhighvolmeanreverting = abs(open-close) > (atr*m) and close > open and meanrevertingenv and highvolenvironment

buyhighvolmeanreverting = abs(open-close) > (atr*m) and close < open and meanrevertingenv and highvolenvironment

selllowvolmeanreverting = abs(open-close) > (atr*m1) and close > open and meanrevertingenv and lowvolenvironment

buylowvolmeanreverting = abs(open-close) > (atr*m1) and close < open and meanrevertingenv and lowvolenvironment

//trend following

buyhighvoltrendy = abs(open-close) > (atr*n) and close > open and close> DOPEN(1) and trendenv and highvolenvironment

sellhighvoltrendy = abs(open-close) > (atr*n) and close < open and close< DOPEN(1) and trendenv and highvolenvironment

buylowvoltrendy = abs(open-close) > (atr*n1) and close > open and trendenv and lowvolenvironment

selllowvoltrendy = abs(open-close) > (atr*n1) and close < open and trendenv and lowvolenvironment

////////////////////////////////////////////////////////

//long

IF (buyhighvolmeanreverting or buyhighvoltrendy or buylowvolmeanreverting or buylowvoltrendy ) and timeenterbefore and timeenterafter THEN

buy positionlong CONTRACTS AT MARKET

ENDIF

if longonmarket and time = timeend then

sell at market

endif

// short

IF (sellhighvolmeanreverting or sellhighvoltrendy or selllowvolmeanreverting or selllowvoltrendy) and timeenterbefore and timeenterafter THEN

sellshort positionshort CONTRACTS AT MARKET

endif

if shortonmarket and time = timeend then

exitshort at market

endif

set target pprofit myprofit

set stop ploss myloss

Noisette, I cant run it, can you make a version with only the relevant variables?

THanks a lot

Ok, I’ll post itf file tonight.

Please also note that conditions from line 79 to the end don’t modify results if you suppress them.

Regards.

Herewith the code without the last line of the code that don’t improve strategy.

kg6450

Sorry for the late reply.

As for the optimisation are those variables you posted recently the ones to optimise for?

yes that’s correct

I am just trying to understand the logic of the system so I can play around with it, once the volatility has been determined does it simply enter at a multiple of the ATR?

yes that’s correct, ATR is the measure of volatility that I like to use in my codes

What made you think to try a system such as this?

Honestly in this case is just logic, I wanted to create a system that could work on both mean reverting and trendy market so I just split my scenario in 2 parts depending on the ADX indicator that measure the trendiness of the market. As far as the ATR, I think in general it is very useful to smoothen the curve when you define your position size as inverse function of the ATR, so the system will automatically reduce the position in case of high volatility and viceversa.