What broker do u use? is optimized just for IG and market is dax contado..ticker is DAX…diferent broker maybe does not work because difrent market ticker.

2 pics…same in dax and ibex

I’m also with IG through prorealtime.

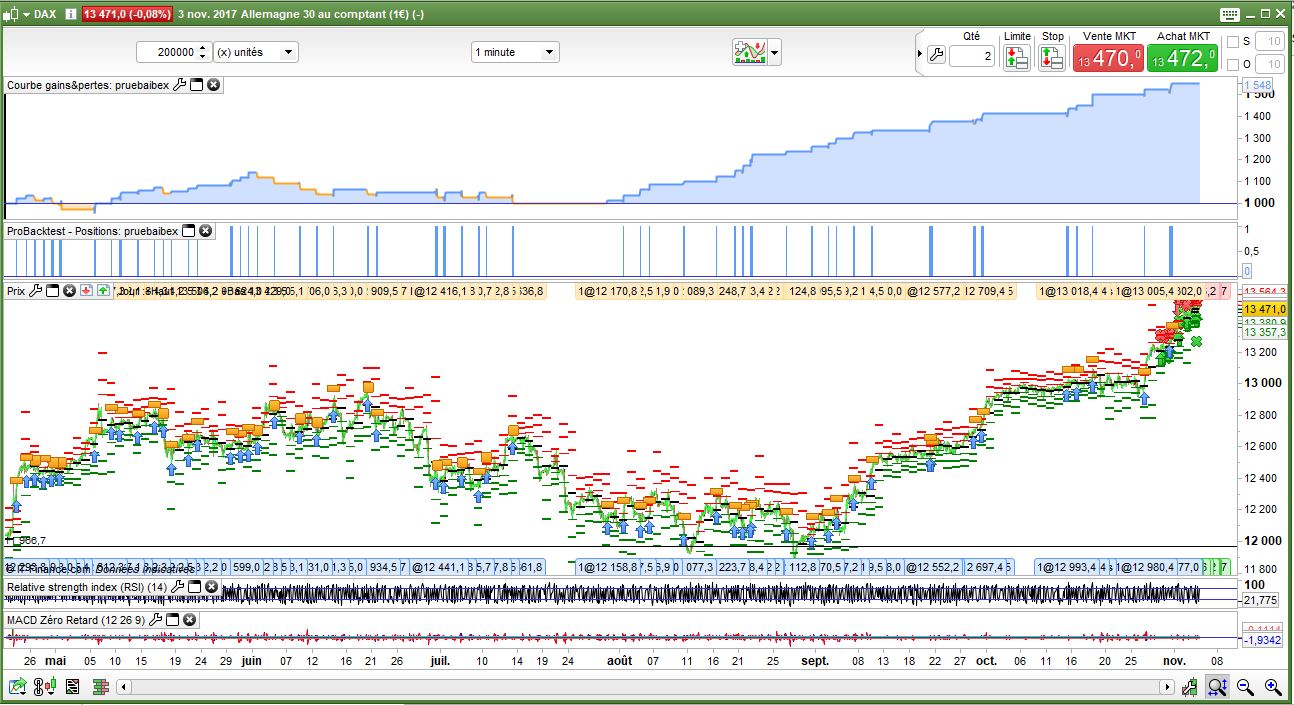

Edit: Now I got some trades. I expected the strategy to generate more trades. I had not enough data loaded. I attached a test with 200K bars. Did you optimize on 100k bars? Basically it works since august and there are not a lot of trades and A LOT of variables. But well if it works….question is in that case for how long.

I’ve the tested the code with 200000 bars and it shows that, as you’ve done the code to adapt to very specific data, the non-tested period give very different result. Anyway it doesn’t loose, but it doesn’t win on the non-tested period, so it is not as promising for the future.

//-------------------------------------------------------------------------

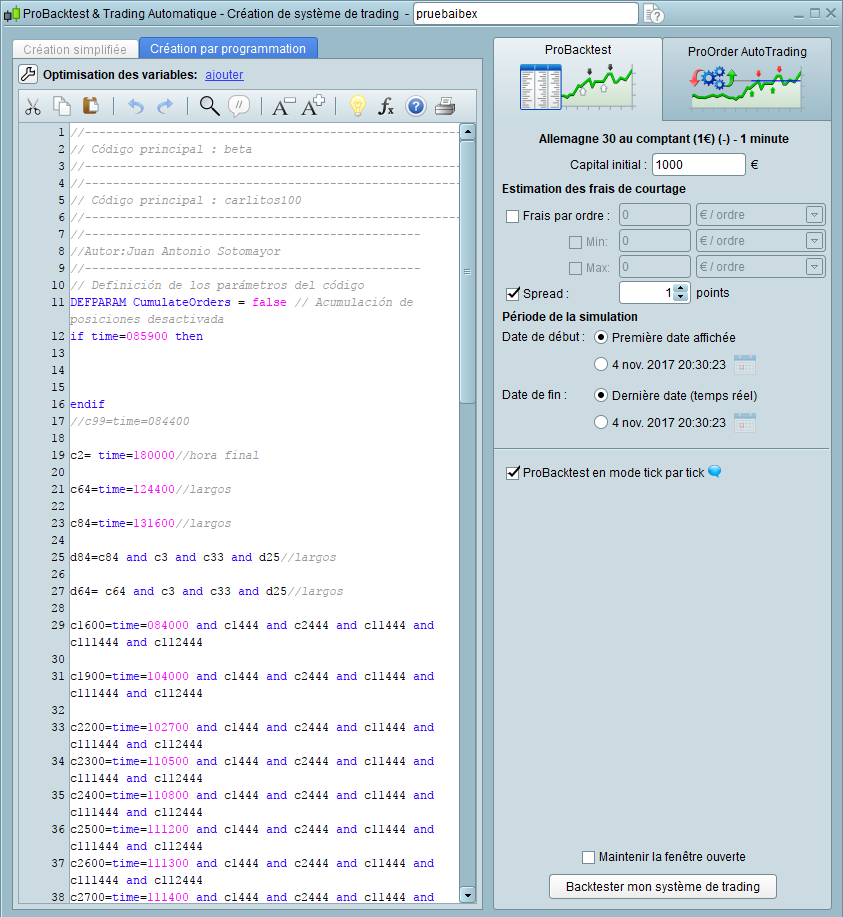

// Código principal : beta

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Código principal : carlitos100

//-------------------------------------------------------------------------

//------------------------------------------------

//Autor:Juan Antonio Sotomayor

//------------------------------------------------

// Definición de los parámetros del código

DEFPARAM CumulateOrders = false // Acumulación de posiciones desactivada

if time=085900 then

endif

//c99=time=084400

c2= time=180000//hora final

c64=time=124400//largos

c84=time=131600//largos

d84=c84 and c3 and c33 and d25//largos

d64= c64 and c3 and c33 and d25//largos

c1600=time=084000 and c1444 and c2444 and c11444 and c111444 and c112444

c1900=time=104000 and c1444 and c2444 and c11444 and c111444 and c112444

c2200=time=102700 and c1444 and c2444 and c11444 and c111444 and c112444

c2300=time=110500 and c1444 and c2444 and c11444 and c111444 and c112444

c2400=time=110800 and c1444 and c2444 and c11444 and c111444 and c112444

c2500=time=111200 and c1444 and c2444 and c11444 and c111444 and c112444

c2600=time=111300 and c1444 and c2444 and c11444 and c111444 and c112444

c2700=time=111400 and c1444 and c2444 and c11444 and c111444 and c112444

c2800=time=111500 and c1444 and c2444 and c11444 and c111444 and c112444

c2900=time=111600 and c1444 and c2444 and c11444 and c111444 and c112444

c3000=time=111700 and c1444 and c2444 and c11444 and c111444 and c112444

c3100=time=111800 and c1444 and c2444 and c11444 and c111444 and c112444

c3200=time=111900 and c1444 and c2444 and c11444 and c111444 and c112444

c3300=time=112200 and c1444 and c2444 and c11444 and c111444 and c112444

c3900=time=121900 and c1444 and c2444 and c11444 and c111444 and c112444

indicator1444 = SmoothedStochastic[14,3](close)

indicator2444 = Average[5](indicator1444)

c1444 = (indicator1444 >= indicator2444)

indicator3444 = ADX[14]

indicator4444 = ADXR[14]

indicator111444 = ROC[12](close)

c111444 = (indicator111444 >= 0)

indicator112444 = Average[50](close)-Average[127](close)

c112444 = (indicator112444 >= 0)

c2444 = (indicator3444 >= indicator4444)

indicator11444 = Average[50](close)-Average[127](close)

c11444 = (indicator11444 > indicator11444[2])

indicator55=Average[50](close)-Average[127](close)

indicator22 = SmoothedStochastic[14,3](close)

indicator24 = Average[5] (indicator22)

c33=(indicator22>=indicator24)

d25=indicator55>indicator55[2]//c24= indicator111>-2//largos

indicator1 = ADX[14]

indicator2 = ADXR[14]

c3 = (indicator1 >= indicator2)//laros

//c999=(indicator1-indicator2)>2

IF c2200 or c1900 or c2300 or c2400 or c2500 or c2600 or c2700 or c2800 THEN

BUY 1 CONTRACT AT MARKET

hora=7

ENDIF

if c1600 or c2900 or c3000 or c3100 or c3200 or c3300 or c3900 then

buy 1 contract at market

hora=7

endif

if hora=7 then //

//Stops y objetivos

SET STOP pLOSS 25

SET TARGET pPROFIT 25

endif

if d64 or d84 then

buy 1 shares at market

hora=4

if hora=4 then

set target pprofit 12

endif

endif

if c2 then

sell at market

endif

if c2 then

exitshort at market

set stop ploss 28

endif

Hi Despair, works for me…

@juanan71

This code is the code that you have test this week or it’s a other?

Thanks

No this code i was making just for ibex and surprimse me when checked in dax…working too…just a few steps and no filtered

File i’m working..still working.. is this one

I know is a caos lol…still working and no assembled and depured…is my first automatism

Aloysius my theory is somerhing happens every x months by this automatis are not forever…from pril to july fails and from 17th july works perfect same conditions…now maybe will lose again because third 3 months..october to december…maybe working in conditions april to july applied to ictuber-december works….just a theory

is a radical change but….theres some if all of them works from april to now…why? Maybe indicators are supported…add to the file sent before condition of bollsup-bollinf>15 or 20 and check

maybe you could help me with this project

Hi Juanan ,

DO you have just tested 200k for the code in the post #51520 ??

Thanks

REgards.

Yes is tested but still working on it

Didn’t test it, but I think it’s probably over fit on last 100k bars. About your “theory”, did you think of summer time change that may modify how the strategy behaved?

Via Prorealtime Premium, importation of the code didn’t trigger any error, but did on IG.

Had to modify the line regarding the call of the “xoindicator”, which is already define at the beginning of the code under the name indicator xo, if I’m not mistaken. By the way, Dax has a bid-offer of 4bp if my memory is correct, making the winning rate drop from 100% to 90% on 200k bar (still very impressive). Unfortunately, nothing understood from your code, so hard to get more confortable with it, but great performance Juanan!