Dear Colleagues,

I am trying to put together a simple Daily Martingale Code.

The system start at 090000 every day a takes the price at that time as reference (levelZERO) for the rest of the day.

If the price goes up from levelZERO and pass the 10 pips up (level1up) opens a BUY STOP order with a SL=20 and PF=20

If the price goes down from levelZERO and pass the 10 pips down (level1down) opens a SELLSHORT STOP order with a SL=20 and PF=20

Every time our operation goes wrong and start again, the Martingale doubles the position size.

The idea is to create and area of 30 pips up and 30 pips down in which, if the price trespass those levels up or down, it is a winning operation (20 pips) and then no more trading for the day.

We all know the risk of the Martingale or any other systems based on the accumulation of orders, but since the operations are close daily and the range is 30 pips up and down from the starting price (levelZERO) at 090000, I felt very curious to see the long term results.

I have put together the code below, but it seems that after the first operations, it stops. I know there is a way to keep the STOP orders active in the following bars but I don’t remember how it goes. Everything I tried is not working, so I will leave the code here in case anyone finds the problem.

// GRIDDIARIO20 5' DAX

//----------------------------

// PARAMETERS

DEFPARAM CumulateOrders = false

DEFPARAM Flatbefore = 090000

DEFPARAM Flatafter = 210000

// DAILY operations. It resets the variable each new DAY

IF INTRADAYBARINDEX = 0 THEN

nomoretrading = 0

ENDIF

// NO MORE TRADING per DAY if one operation is POSITIVE (20 pips)

IF positionperf(1)>0 THEN

nomoretrading=1

ENDIF

// Positioning

perdida1 = positionperf(1)<0

perdida2 = positionperf(1)<0 and positionperf(2)<0

perdida3 = positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0

perdida4 = positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0 and positionperf(4)<0

perdida5 = positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0 and positionperf(4)<0 and positionperf(5)<0

perdida6 = positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0 and positionperf(4)<0 and positionperf(5)<0 and positionperf(6)<0

IF INTRADAYBARINDEX = 0 THEN

positionsize=1

ENDIF

IF perdida1 THEN

positionsize=2

ENDIF

IF perdida2 THEN

positionsize=4

ENDIF

IF perdida3 THEN

positionsize=8

ENDIF

IF perdida4 THEN

positionsize=16

ENDIF

IF perdida5 THEN

positionsize=32

ENDIF

IF perdida6 THEN

positionsize=32

ENDIF

// STOP LOSS and PROFITs

SET STOP pLOSS loss1

SET TARGET pPROFIT profit1

profit1 = 20

loss1 = 20

// Distancia GRID

disgrid1 = 10

// Determinición niveles GRID

IF time=090000 AND nomoretrading=0 THEN

levelZERO = close

ENDIF

level1up = levelZERO + disgrid1*pipsize

//level2up = level0 + disgrid2*pipsize

level1down = levelZERO - disgrid1*pipsize

//level2down = level0 - disgrid2*pipsize

// ORDERS //////////////////////////////////////////////////////////////////////////////////////////////////////////

IF nomoretrading=0 THEN

BUY positionsize CONTRACT AT level1up STOP

SELLSHORT positionsize CONTRACT AT level1down STOP

ENDIF

Thanks,

Juan

Before anyone point it out, I know that the Martingale code is a little unconventional and there is another one here in the library shorter and simplified, but I understand this much better and it is easier for me to change it and modify it in case I want to create a reverse or other type of Martingale.

Eric

EricParticipant

Master

I am not sure but could it be that you open the trades with stoporders that causes the problem? (using stoporders and positionperf)

Its an interesting approach, i have tried something similar but never did get it to work, ( but i am not any good at coding)

EricParticipant

Master

Another thing i been thinking about but i doubt it can be done with proorder?

First of all you need a account with hedging allowed

If you start with a box of 30 points or a inside bar or whatever

and quit if profit is 60 points

then you open 1 buy at boxhigh (no stop) and if it reach boxlow before take profit

then you open 2 sell (no stop)

and next 3 buy and so on

you just keep all trades open and hedge so that you have only 1 extra open buy or sell and wait for take profit and close all

most of the time you only need 1 buy or maybe one sell open before TP

of course TP could be 1:1 but then you need to double size each time

the thing is you lower the risk and the margin is lower when hedging

and less slippage because less stoporders

Try the following in replacement of line 14-17 of your system :

// NO MORE TRADING per DAY if one operation is POSITIVE (20 pips)

diffTiBi = barindex - tradeindex

diffTiBi1 = barindex - tradeindex(2)

c1 = positionperf(1) > 0

IF (c1 and date[diffTiBi] = date and (not onmarket)) OR (c1 and date[diffTiBi1] = date and onmarket) THEN

nomoretrading=1

ENDIF

However, the result looks like a conventional Martingale system : long periods with nice gains and a few catastrophic events that destroy everything.

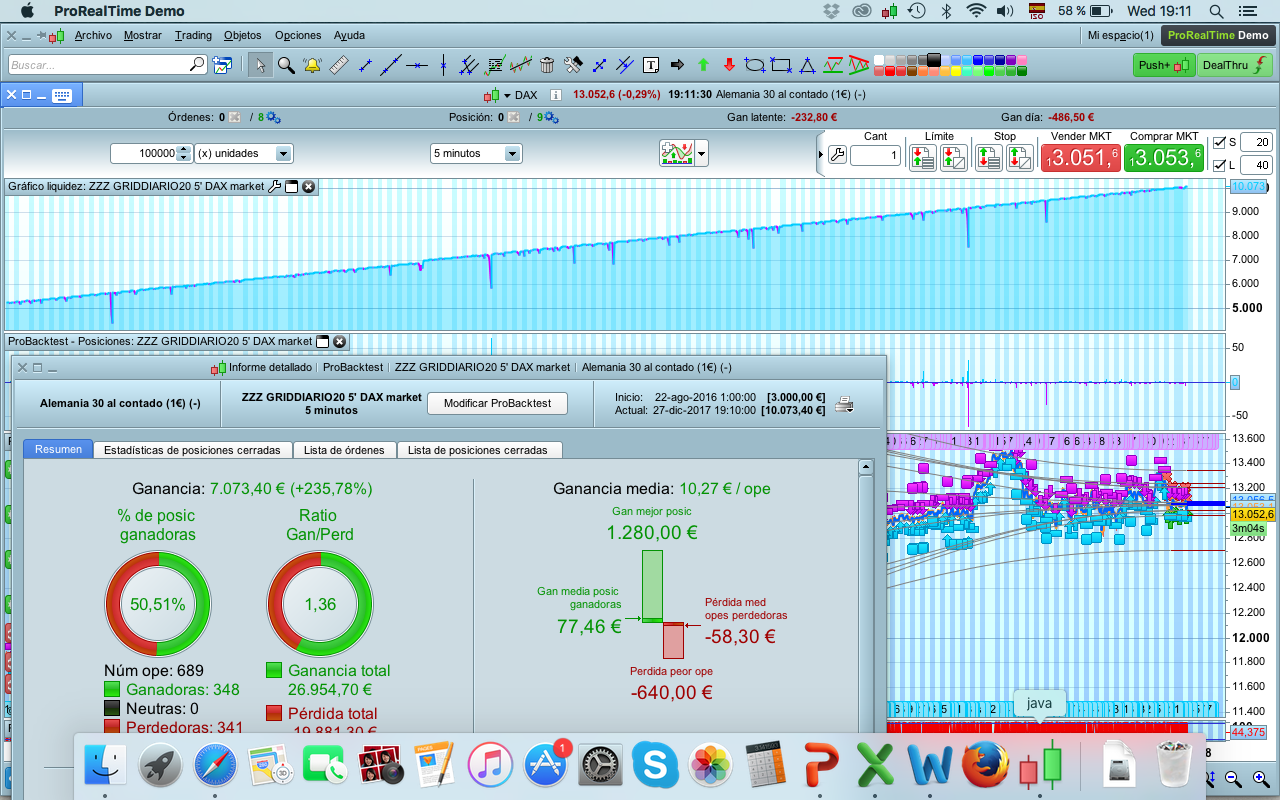

Hi Verdi and Eric,

Thanks so much for your suggestions and for your piece of code. It works fine, and pretty much what I expected of a Martingale: Nice periods of steady gain and sudden drops.

Nevertheless, it is not quite what I want. I had the idea of doing the daily martingale. It means that at the end of the day the accumulation is over and next day start when positionsize=1. I realised that many of the drops are due to the accumulation of contracts through different days, which is very plausible. On the contrary, if we reduced the martingale to just one day, the probability of failing more than 4-5 consecutive operations (critical number) in one day, when a simple grid is rare.

I have tried to reset the number of contracts every day by:

IF time=010000 THEN

positionsize=1

ENDIF

It doesn’t work.

Any suggestions??

Thanks,

Juan

Same problem as before : positionperf(x) keeps counting the performance of every position, whenever it was. So, if positionperf(6)<0 occured, say 6 days ago, it will still reset positionsize to a higher value than 1. You need to find a way that only the performance of positions of the same day (not of the days before) are counted for the calculation of positionsize, just as I did it in my short code.

“IF (positionperf(1) > 0 and date[diffTiBi] = date and (not onmarket)) OR (positionperf(1) > 0 and date[diffTiBi1] = date and onmarket)” only counts the positionperf of positions that were closed on the same day.

Hi Verdi,

Thanks, I will try it this afternoon. If this work, it is going to be very useful for me in the future, because it is a problem/condition that I have been having in my last codes and didn’t know how to solve it.

Let you of the results later,

Thanks,

Juan

Hi JR1976,

I am using 5 min, but the smaller the better, although you will have to get a decent backtest due to the limited past.

I have changed the orders at market, since does not interfere with the reading of the Martingale. The result attached are not bad, but like any Martingale subject to any sudden drawdown. Anyway, I wanted to try and see the results since I am exploring different ways to approach strategies, different than pure Technical Analysis.

Regards,

Juan

P.S.- I am having your code “Riding the trend/SP500” on REAL, and it is going fairly well. Thanks.

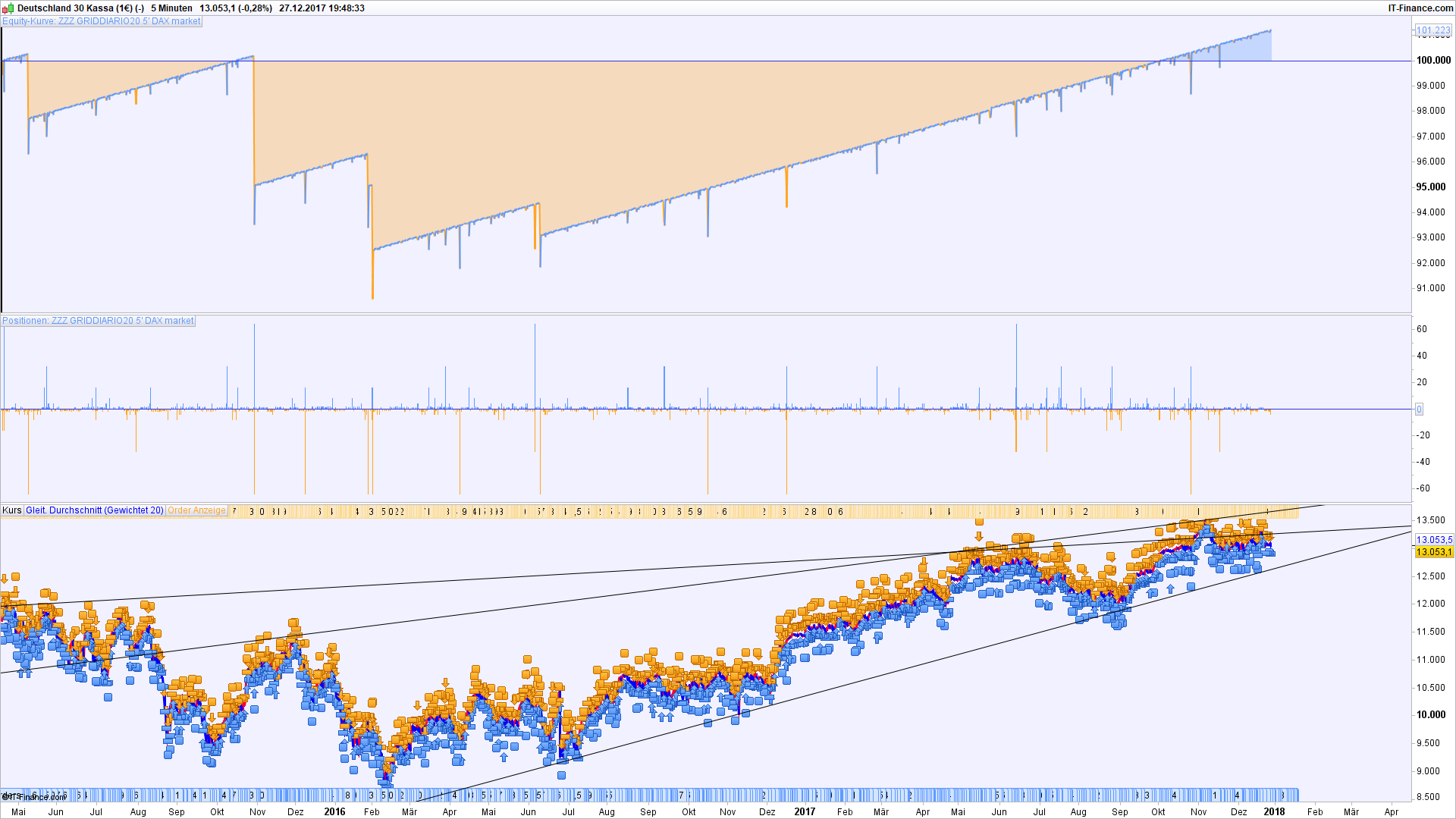

This is my try with 200.000 bars :

Oh, the attachments…[attachment file=56687]

Martingale will fail, whatever conditions or filters you’ll add in your strategy. The backtests’ results (or equity curve looks) depends mainly of when you start the strategy, it is all clear in the picture that verdi55 has attached. Anyway, this is a very good coding exercise 🙂

Hi Verdi,

Thanks for the 200k. No doubt about what Nicolas said. I would have never put this in REAL because any day may be the last one (literally), but I am coding and studying new different types of grid strategies, and part of this code is going to be very useful for the future.

Regards,

Juan

Have you had a look at this one: https://www.gridtrendmultiplier.com/

Have bookmarked it some time ago in order to code something similar when I have some time but never seem to get to it.