Hi everyone,

I coded my idea of screening in different timeframes of same slope direction of coppock curve indicator(in 3 timeframes, coppock curve slope be same. upward or downward!). the problem is that some detected markets had not meet all conditions. sometimes in 1 timeframe the slope direction is different. i used 2 methods to code as i mentioned below.

my coppock curve indicator is according to the library of this website.

at the first code, used ROC[1] of coppock curve to find the slope.

at second code, compared the value of coppock curve than previous bar same value to see if downward or upward.

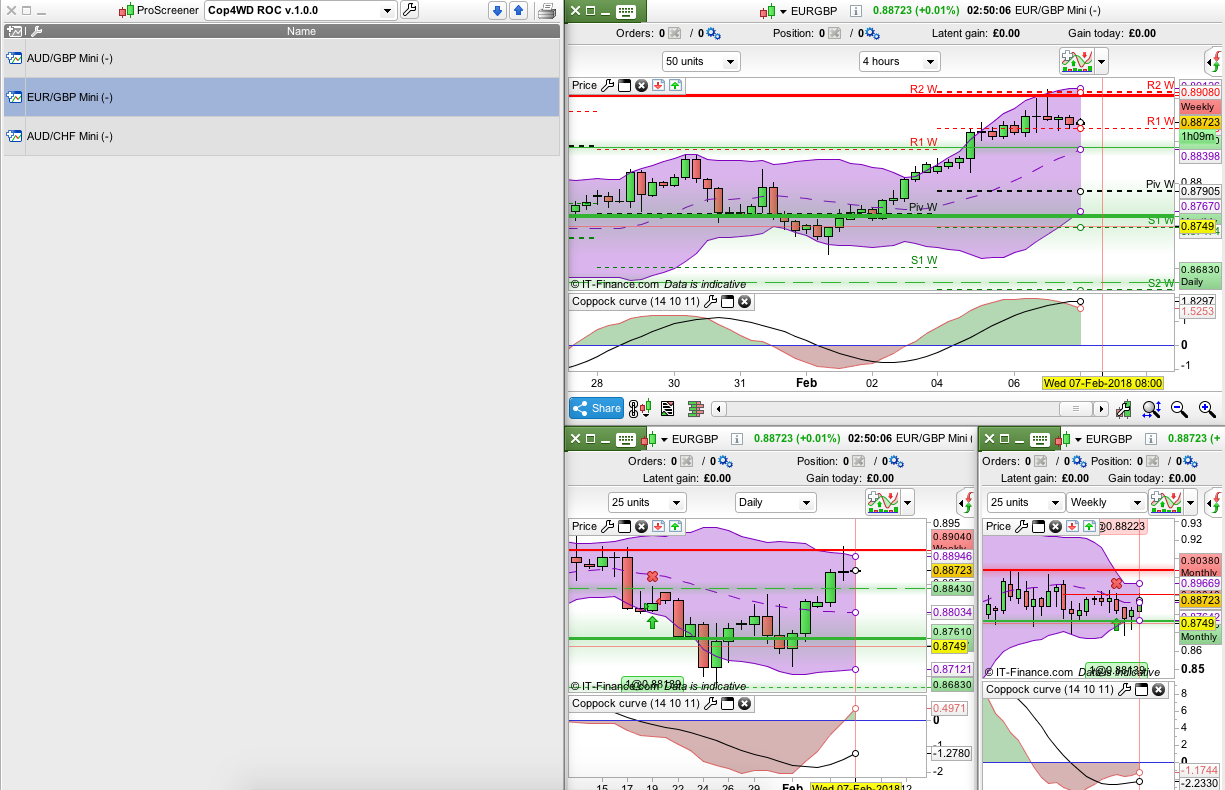

as can be seen in the picture, the eur/gbp detected but in 4 hour timeframe, the slope of coppock curve is in different direction than Daily and weekly time frame.

//Cop4WD ROC v.1.0.0

timeframe(4h)

COP4N= CALL "Coppock curve"

COP4=ROC[1](COP4N)

c1=cop4>0

c2=cop4<0

c7=cop4N<0

c8=cop4N>0

timeframe(daily)

COPDN= CALL "Coppock curve"

COPD=ROC[1](COPDN)

c3= CopD>0

c4=CopD<0

timeframe(weekly)

COPWN= CALL "Coppock curve"

COPW=ROC[1](COPWN)

c5=copw>0

c6=copw<0

C9=c1 and c3 and c5 and c7

C10=c2 and c4 and c6 and c8

screener[C9 OR C10]

//Cop4WD v.1.1.0

timeframe(4h)

cop4= CALL "Coppock curve"

c1=cop4>cop4[1]

c2=cop4<cop4[1]

c7=cop4[1]<0

c8=cop4[1]>0

timeframe(daily)

CopD = CALL "Coppock curve"

c3= CopD>CopD[1]

c4=CopD<CopD[1]

timeframe(weekly)

copW = CALL "Coppock curve"

c5=copw>copw[1]

c6=copw<copw[1]

screener[c1 and c3 and c5 and c7]

screener[c2 and c4 and c6 and c8]

Kindly, advise!

Did you test with:

timeframe(4 hours)

Could you please post the “Coppock curve” code you are using?

a = ROC[14](close)

b = ROC[11](close)

coppock = weightedaverage[10](a+b)

RETURN coppock as "Coppock curve"

my coppock curve

with “timeframe(4 hours)” already tested. there is same fake out result.

Dear Nicolas,

Please look at the results today. those are totally fake outs. actually, this screener was working pretty good in last month but there was few fake outs but recently show all fake result. i can ignore fake results but i am afraid if it doesn’t show genuine results. and also as a programmed screener shouldn’t have such fake outs.

Please help to refurbish this Idea!

with thanks.

You are right, values are not the same between the ones called into ProScreener and the ones shown in ProBuilder. Some indicators are calculated differently between the 2, but here it is only a ROC and a WMA, so I don’t understand where is the trouble … Please send a report with the attached code and a reference to this topic with the console inside the platform (CTRL+M). I’ll do the same.

//Cop4WD v.1.1.0

timeframe(4 hours)

a4 = ROC[14](close)

b4 = ROC[11](close)

cop4 = weightedaverage[10](a4+b4)

//cop4= CALL "Coppock curve"

c1=cop4>cop4[1]

c2=cop4<cop4[1]

c7=cop4[1]<0

c8=cop4[1]>0

timeframe(daily)

CopD = CALL "Coppock curve"

c3= CopD>CopD[1]

c4=CopD<CopD[1]

timeframe(weekly)

copW = CALL "Coppock curve"

c5=copw>copw[1]

c6=copw<copw[1]

screener[(c1 and c3 and c5 and c7) or (c2 and c4 and c6 and c8)] (copd)

I reported just now. so how can i get reply? how they contact me?

They should contact you by email. But it can take some times, depending of how many request they have currently in queue.

Dear Nicloas,

I postponed screening to one bar behind and it worked properly. it shows no fake out. also i tried for only 2 TFs and it shows few markets that all having same direction at the 4hour and daily timeframe. it can only help diagnosis of the issue but not workable for me as it is giving delayed detection. anyway, i posted new code as per below:

//Cop4WD v.1.1.1

timeframe(4 hours)

a4 = ROC[14](close)

b4 = ROC[11](close)

cop4 = weightedaverage[10](a4+b4)

//cop4= CALL "Coppock curve"

c1=cop4[1]>cop4[2]

c2=cop4[1]<cop4[2]

c7=cop4[1]<0

c8=cop4[1]>0

timeframe(daily)

ad = ROC[14](close)

bd = ROC[11](close)

copd = weightedaverage[10](ad+bd)

c3= CopD[1]>CopD[2]

c4=CopD[1]<CopD[2]

timeframe(weekly)

aw = ROC[14](close)

bw = ROC[11](close)

copw = weightedaverage[10](aw+bw)

c5=copw[1]>copw[2]

c6=copw[1]<copw[2]

screener[(c1 and c3 and c5 and c7) or (c2 and c4 and c6 and c8)]

Thank you for the hint. I still don’t understand why it gives correct values for one bar ago and not for the current period though.. Did you try on another list? (not forex mini)

I tested this hint with other same codes but it shows really unstable. i just give this hint if maybe help for diagnosis. i will keep testing if it is workable in long run and hope it would be resolved!

regarding market list, i only tried on my predefined list including mini markets and Currencies list including all forex list. when I chose share markets screener need daily TF or maybe some other requirements to operate for IG clients.

Now I can surely say, the method to delay screening 1 bar behind really NOT work too.

The problem had been identified, it only impact instruments with small ticksize such as forex pairs. It should be fixed in the next update.

so next update for Mac OS would be when roughly?