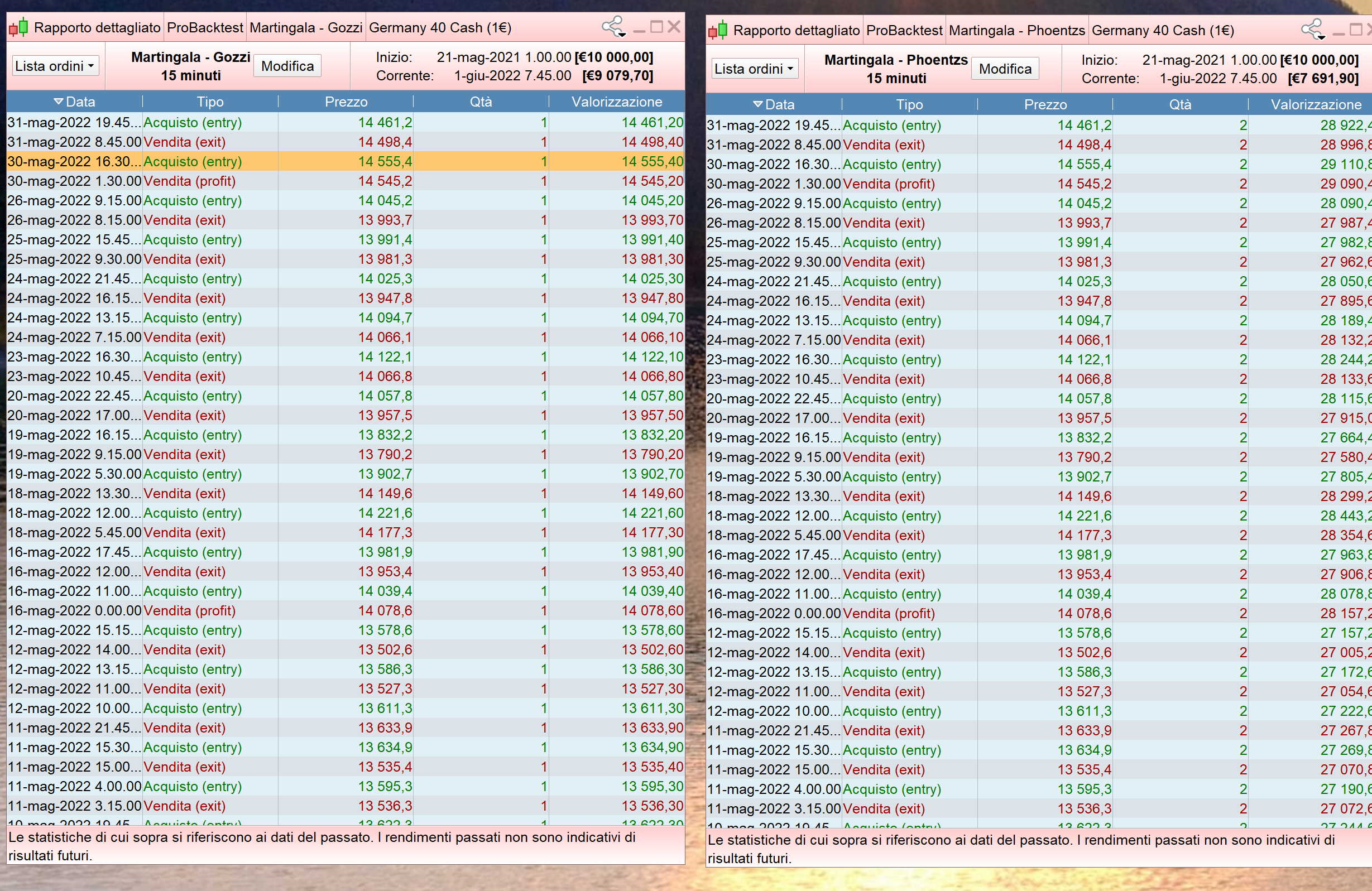

Il codice di Roberto fa SEMPRE 1 operazione.

Il codice di Phoentzs fa SEMPRE 2 operazioni.

//30.03.2022 200000k

//US500 M5 Spread 0.6

//German Time

defparam preloadbars = 10000

defparam CUMULATEORDERS = false

//MM

ONCE LotSize = 5 //starting number of lots/contracts

ONCE MinLots = 5 //minimum lot size required by the broker

ONCE MaxLots = 10 //999 max lots allowed (to be also set in AutoTradung)

ONCE Rise = 5 //numebe of lots to increment

ONCE Fall = 5 //number of lots to decrement

IF StrategyProfit > StrategyProfit[1] THEN

LotSize = LotSize + Rise

ELSIF StrategyProfit < StrategyProfit[1] THEN

LotSize = LotSize - Fall

ENDIF

LotSize = min(MaxLots,max(MinLots,LotSize)) //check both Maximum and Minimum

//LotSize = 5

timeframe(15minute, updateonclose)

RangeMAD5 = average[480,0](close) //Wochentrend Daily MA5

RangelongD5 = close > RangeMAD5

RangeshortD5 = close < RangeMAD5

RangeMAD20 = average[1920,0](close) //"Monatstrend" Daily MA20

RangelongD20 = RangeMAD5 > RangeMAD20

RangeshortD20 = RangeMAD5 < RangeMAD20

MA1 = average[x1,0](close)

MA2 = average[x2,0](close)

//MA3 = average[x3,0](close)

MA4 = average[x5,1](close)

MA5 = average[x6,1](close)

longA = MA1 > MA2 //and MA2 > MA3 //and MA2 > MA2[1]

shortA = MA4 < MA5 //and MA5 < MA5[1]

MAL1 = average[5,0](close)

MAL2 = average[15,0](close) //15

longB = MAL1 crosses over MAL2

shortB = MAL1 crosses under MAL2

timeframe(default)//M5

long = RangelongD5 and longB and longA //and RangelongD20

short = RangeshortD5 and shortB and shortA //and RangeshortD20

Exit1 = RangeshortD5

Exit2 = RangelongD5

// trading window

ONCE BuyTime = 110000

ONCE SellTime = 213000

ONCE BuyTime2 = 150000

ONCE SellTime2 = 213000

// position management

IF Time >= buyTime AND Time <= SellTime THEN

If long then //not onmarket and

BUY LotSize CONTRACT AT market

SET STOP %LOSS hl

SET TARGET %PROFIT gl

EndIf

endif

IF Time >= buyTime2 AND Time <= SellTime2 THEN

If short then

sellshort LotSize CONTRACT AT market

SET STOP %LOSS hs

SET TARGET %PROFIT gs

EndIf

endif

If longonmarket and Exit1 then

sell at market

endif

If shortonmarket and Exit2 then

exitshort at market

endif

if time = 223000 then //223000

//sell at market

exitshort at market

endif

if time = 225500 and dayofweek=5 then //225500

sell at market

exitshort at market

endif

////////////////////////////////////////

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

trailingpercentlong = startl // %

trailingpercentshort = start // %

once acceleratorlong = stepl // typically tst*0.1

once acceleratorshort= step // typically tss*0.1

ts2sensitivity = 2 // [1] close [2] high/low [3] low/high [4] typicalprice

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=(typicalprice)

ts2sensitivityshort=(typicalprice)

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong then

newsl = positionprice+trailingsteplong + 0.2

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong then

newsl = newsl+trailingsteplong

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort then

newsl = positionprice-trailingstepshort

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort then

newsl = newsl-trailingstepshort

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

if (shortonmarket and newsl > 0) or (longonmarket and newsl>0) then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

endif

if shortonmarket then

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

//////////////////////////////////////////////////////////////

Caro @MauroPro

, visto che ho postato questa strategia prima… Ti ricordi? MA Croce? Qui la strategia con MM Qui il codice funziona.

Ciao Phoetzs, grazie per l’esempio. Stavo facendo delle prove con il tuo codice. Ho visto che funziona in questo modo:

A) Raddoppia la posizione dopo un guadagno (come fa il tuo codice “Multi SP500”)

IF StrategyProfit > StrategyProfit[1] THEN

LotSize = LotSize + Rise

ELSIF StrategyProfit < StrategyProfit[1] THEN

LotSize = LotSize – Fall

ENDIF

B) Raddoppia la posizone dopo una perdita (MARTINGALA):

IF StrategyProfit > StrategyProfit[1] THEN

LotSize = LotSize – Rise

ELSIF StrategyProfit < StrategyProfit[1] THEN

LotSize = LotSize + Fall

ENDIF

Vorrei però aggiungere nel codice B (Martingala), come stava provando Roberto, il flag: RADDOPPIO, per fare in modo che il TS usi due contratti solo dopo la PRIMA perdita, mentre il codice che hai postato mantiene due contratti anche se ci sono più operazioni in perdita consecutive (vd foto).

Siccome però funziona, Roberto potrebbe aggiungere il suo flag RADDOPPIO in questo codice.

Ovviamente puoi anche ottimizzare “Rise” e “Fall” (1-5 entrambi nell’ottimizzatore).

Per la codifica di livello superiore, come Flag, Roberto deve intervenire. Non ne ho idea.

Roberto puoi inserire in questo codice il flag per raddoppiare la posizione in perdita soltanto la prima volta? (vedi immagine allegata sopra)

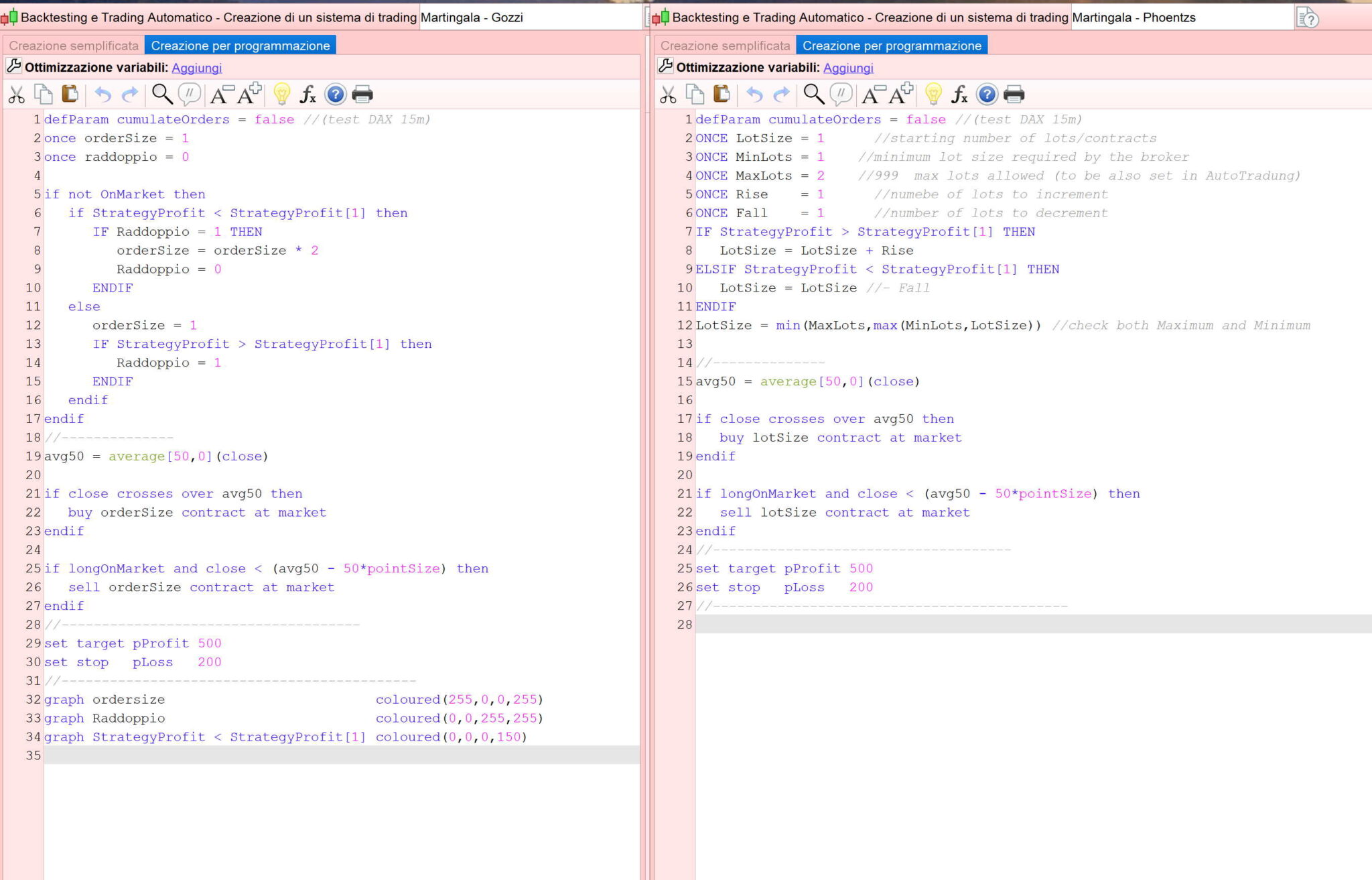

defParam cumulateOrders = false //(test DAX 15m)

ONCE LotSize = 1 //starting number of lots/contracts

ONCE MinLots = 1 //minimum lot size required by the broker

ONCE MaxLots = 2 //999 max lots allowed (to be also set in AutoTradung)

ONCE Rise = 1 //numebe of lots to increment

ONCE Fall = 1 //number of lots to decrement

IF StrategyProfit > StrategyProfit[1] THEN

LotSize = LotSize - Rise

ELSIF StrategyProfit < StrategyProfit[1] THEN

LotSize = LotSize + Fall

ENDIF

LotSize = min(MaxLots,max(MinLots,LotSize)) //check both Maximum and Minimum

//--------------

avg50 = average[50,0](close)

if close crosses over avg50 then

buy lotSize contract at market

endif

if longOnMarket and close < (avg50 - 50*pointSize) then

sell lotSize contract at market

endif

//-------------------------------------

set target pProfit 500

set stop pLoss 200

//--------------------------------------------

Ne ho uno in più. Mi è venuto in mente solo dopo aver letto la tua frase… Basta girare il “>”. Poi fa quasi quello che vuoi. Ho appena provato una strategia diversa… stessa performance ma riduce il drawdown.

IF StrategyProfit < StrategyProfit[1] THEN //erhöht bei Verlust

LotSize = LotSize + Rise

ELSIF StrategyProfit > StrategyProfit[1] THEN

LotSize = LotSize – Fall

ENDIF

Questo che hai postato è il codice martingala che raddoppia la posizione in caso di perdita (come il mio caso B sopra).

Nel tuo “TS Multi” NON usavi il martingala, ma raddoppiavi la posizione in caso di guadagno (che è un altra tecnica).

Giusto. Rilancio a MaxPosition se vinco. Dopo aver parlato con te, ho scoperto che se rilanci in caso di perdita e torni a MinPosition in caso di vittoria, il drawdown del sistema diminuisce. Che a quanto pare è meglio. Questo sarebbe l’ultimo codice che ho postato. Ma penso che funzioni allo stesso modo del tuo codice B. Scritto in modo diverso.

Il vero Martingala raddoppia la posizione OGNI volta che si perde ( e porta ad azzerare i conti in quanto il capitale a disposizione non è infinito!)

Il codice che ho postato per Roberto, che utilizza la tua formula (strategyProfit < StrategyProfit[1] e lotSize +1) è un Martingala che raddoppia una volta la posizione e la mantiene raddoppiata fino che non capita un guadagno…)

Il codice che ho postato sopra e che vorrei che Roberto modificasse con il suo flag dovrebbe raddoppiare solo per la prima perdita la posizione e poi, anche se capitano perdite consecutive, utilizzare sempre un contratto.

Poi c’è il tuo codice Multi che invece raddoppia una posizione vincente e la mantiene raddoppiate per tutte le vincite consecutive fino a che non capita una perdita.

Sono onestamente curioso di sapere come si comporta il codice con il “flag”.

Perdonami se mi sono intromesso qui.

Aspettiamo Roberto che sui flags è un mago!

Ho cambiato una riga ONCE iniziale, più la verifica del raddoppio.

Adesso sembra segua perfettamente la regola del raddoppio solo quando c’è un risultato POSITIVO seguito da uno NEGATIVO (+-), negli altri casi (++ oppure –, oppure -+) non raddoppia.

defParam cumulateOrders = false //(test DAX 15m)

once orderSize = 1

once raddoppio = 1

if StrategyProfit < StrategyProfit[1] then

IF Raddoppio = 1 THEN

orderSize = orderSize * 2

Raddoppio = 0

ELSE

orderSize = 1

ENDIF

elsif StrategyProfit > StrategyProfit[1] THEN

orderSize = 1

Raddoppio = 1

endif

//--------------

avg50 = average[50,0](close)

if close crosses over avg50 then

buy orderSize contract at market

endif

if longOnMarket and close < (avg50 - 50*pointSize) then

sell orderSize contract at market

endif

//-------------------------------------

set target pProfit 500

set stop pLoss 200

//--------------------------------------------

graph ordersize coloured(255,0,0,255)

graph Raddoppio coloured(0,0,255,255)

graph StrategyProfit < StrategyProfit[1] coloured(0,0,0,150)

Quello scritto da phoentzs va bene, il suo scopo è incrementare di uno o diminuire di uno in caso di perdita o di guadagno, rispettando i limiti di 1 e 2 (senza la regola +-)

Per modificarlo devo farlo uguale al mio, non ha molto senso.

Ciao Roberto, ho provato ed ora funziona.

Per raddoppiare la posizione (la prima volta) non di un trade perdente, ma vincente (anti martingala) ho visto (e funziona) che basta invertire < e > nelle rughe 5 e 12.

Volevo apportare un ultima modifica nel seguente TS anti martingala di prova: attendere prima di raddoppiare (la prima volta soltanto) la posizione vincente non un trade vincente, ma due trade vincenti (quindi si raddoppierebbe dopo -++).

Pensavo che bastava scrivere nella riga 5 : if strategyProfit > strategyProfit[1] and strategyProft[1] > strategyProfit[2], ma non funziona (tutte le op. tornano ad essere di un contratto), sai come si corregge?