No, I was talking about your previous post, to exit 75% of the whole position in three steps, without using different flags and sevarel IF…ENDIF’s:

// partial close

ONCE partialclose = 1

ONCE PerCent = 0.25 //25% = positions to close

ONCE PerCentGain = 0.005 //0.5% increase

ONCE MinLotSize = 0.5 //0.5 lots minimum

//

if partialclose and OnMarket then

ExitQuantity = max(ExitQuantity[1],abs(CountOfPosition) * PerCent)

LeftQty = max(MinLotSize,abs(CountOfPosition) - ExitQuantity)

CloseQuantity = abs(CountOfPosition) - LeftQty

else

CloseQuantity = 0

endif

//

IF close >= (PositionPrice * (1 + PerCentGain)) AND LongOnMarket AND CloseQuantity > 0 THEN

SELL CloseQuantity Contracts AT Market

ENDIF

Example on Dax, daily TF:

// partial close

ONCE partialclose = 1

ONCE PerCent = 0.25 //25% = positions to close

ONCE PerCentGain = 0.005 //0.5% increase

ONCE MinLotSize = 0.5 //0.5 lots minimum

//

if partialclose and OnMarket then

ExitQuantity = max(ExitQuantity[1],abs(CountOfPosition) * PerCent)

LeftQty = max(MinLotSize,abs(CountOfPosition) - ExitQuantity)

CloseQuantity = abs(CountOfPosition) - LeftQty

else

CloseQuantity = 0

endif

//

IF close crosses over average[200] and Not OnMarket then

buy 10 contracts at market

set target pProfit 1000

set stop pLoss 500

endif

//

IF close >= (PositionPrice * (1 + PerCentGain)) AND LongOnMarket AND CloseQuantity > 0 THEN

SELL CloseQuantity Contracts AT Market

ENDIF

graph abs(countofposition)

The use of [1] in line 8 is to make sure it never falls below the previous value, so that the percentage of 25%, whatever the number it is calculated on, remains unchanged.

So that will make a 25% partial close at each .5% increase? Doesn’t it need the flag to keep it from repeating each step?

You are right ,

I added Increments to my example above, so that the percentage is increased each new closure by PerCentGain steps:

// partial close

ONCE partialclose = 1

ONCE PerCent = 0.25 //25% = positions to close

ONCE PerCentGain = 0.005 //0.5% increase

ONCE MinLotSize = 0.5 //0.5 lots minimum

ONCE Increments = 1

//

if partialclose and OnMarket then

ExitQuantity = max(ExitQuantity[1],abs(CountOfPosition) * PerCent)

LeftQty = max(MinLotSize,abs(CountOfPosition) - ExitQuantity)

CloseQuantity = abs(CountOfPosition) - LeftQty

else

CloseQuantity = 0

Increments = 1

endif

//

IF close crosses over average[200] and Not OnMarket then

buy 10 contracts at market

set target pProfit 1000

set stop pLoss 500

endif

//

IF close >= (PositionPrice * (1 + (PerCentGain * Increments))) AND LongOnMarket AND CloseQuantity > 0 THEN

SELL CloseQuantity Contracts AT Market

Increments = Increments + 1

ENDIF

graph abs(countofposition)

graph PerCentGain * Increments

graph ExitQuantity

you can also remove and Not OnMarket to accumulate positions.

that looks great, and far more elegant.

but now I’m thinking it would be better to be able to alter the percent and percentgain independently. so, for example, it might close 0.3 of the position after a 0.6% gain, then 0.5 at 1.6% gain (all percentages to be optimized).

This seems to work, but it looks very clunky compared to yours:

ONCE partialclose = 1

ONCE PerCent = pc //10% positions to close

ONCE PerCent2 = pc2 //25% positions to close

ONCE PerCentGain = pcg //0.5% increase

ONCE PerCentGain2 = pcg2 //1% increase

ONCE MinLotSize = 0.5 //0.5 lots minimum

ExitQuantity = abs(CountOfPosition) * PerCent

LeftQty = max(MinLotSize,abs(CountOfPosition) - ExitQuantity)

CloseQuantity = abs(CountOfPosition) - LeftQty

ExitQuantity2 = abs(CountOfPosition) * PerCent2

LeftQty2 = max(MinLotSize,abs(CountOfPosition) - ExitQuantity2)

CloseQuantity2 = abs(CountOfPosition) - LeftQty2

IF Not OnMarket THEN

Flag = 1

ENDIF

IF partialclose AND LongOnMarket and close >= (PositionPrice * (1 + PerCentGain)) AND Flag THEN

SELL CloseQuantity Contracts AT Market

Flag = 0

endif

IF Not OnMarket THEN

Flag2 = 1

ENDIF

IF partialclose AND LongOnMarket and close >= (PositionPrice * (1 + PerCentGain2)) AND Flag2 THEN

SELL CloseQuantity2 Contracts AT Market

Flag2 = 0

endif

endif

Yes, but if percentages need to be different you have no choice but do as you’ve done.

Well… you could use arrays… but that’s more complicated!

Ok, I’ll stay with what I’ve got then – thanks for confirming.

I was wondering if this code is valid, bit confused with use of ONCE function

What I am trying is – once the price trades above 10% of Positionprice, LTU condition is valid forever – even if price comes under 10% of position price. I am trying to replace ONCE PIP in above code with percentage.

Once PercentLTU=1.1

LTU=Close>PERCENTLTU*Positionprice

IF longonmarket and ExitClose and LTU then

Sell at MARKET

ENDIF

Line 3 changes every bar, so LTU isn’t valid forever!

ONCE is used only in line 1 because PercentLTU never changes.

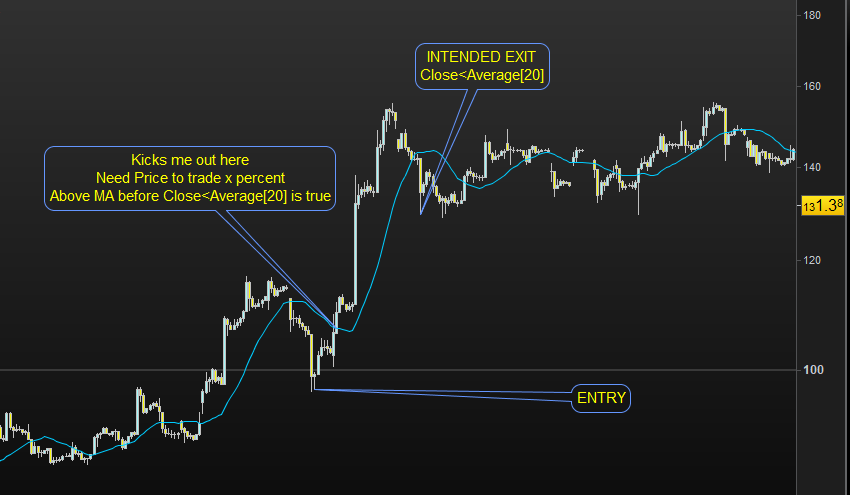

thanks. Then how would it be possible to allow price to trade above the MA and then exit it when it closes below MA. For example, how to have the strategy do nothing before price trades above a Moving average after entry (eg. price is now above Daily 20 MA, but entry was well below that MA.

Please see the attached image.

Exit:

If OnMarket AND close CROSSES OVER average[20] THEN

SELL AT MARKET //Long

EXITSHORT AT MARKET //Short

ENDIF

I am not sure I really understood your question, though.

Can you make an example with the percentage you talked about?

Timeframe (daily)

MA=Average[20]

Dailyclose=close

//Entry price is well below daily MA or Daily MA is still bearish at Entry

Timeframe (1 Hour)

If price crosses over Average [10] then

Buy 1 contract at Market

Endif

//Below condition is triggered when Daily MA tries to turn bullish and exit trade prematurely

If longonmarket and Dailyclose<MA then

Sell at market

Endif

Entry is no issue. Problem is that the entry is below the daily MA, as the price hovers around the daily MA in the process of turning bullish for first time after trade entry, the exit condition is triggered. To solve this i wanted price to trade 20% above positionprice. Once the 20% mark is reached, the exit condition always remains true. For example, If entry price is $10, price goes to $15 and then returns to $11 – I want to exit if Dailyclose<MA in below code.

Once PercentLTU=1.1

LTU=Close>PERCENTLTU*Positionprice

If longonmarket and Dailyclose<MA and LTU then

Sell at market

Endif

I was assuming the below code does what I am saying above. I wanted to replace pips with percentage. For below code when price trades above 20 pips from position price, the condition is still true if the price comes back to say 10 pips from position price.

ONCE PerCent = 0.5 //50% = positions to close

ONCE Pips = 20 * PipSize

ONCE MinLotSize = 0.5 //0.5 lots minimum

ExitQuantity = abs(CountOfPosition) * PerCent

RemainQty = max(MinLotSize,abs(CountOfPosition) - ExitQuantity)

CloseQuantity = abs(CountOfPosition) - RemainQty

IF close >= (PositionPrice + Pips) AND LongOnMarket THEN

SELL CloseQuantity Contracts AT Market

ELSIF close <= (PositionPrice - Pips) AND ShortOnMarket THEN

EXITSHORT CloseQuantity Contracts AT Market

ENDIF

This is the code you need (not tested):

Timeframe (daily)

MA=Average[20]

Dailyclose=close

//Entry price is well below daily MA or Daily MA is still bearish at Entry

Timeframe (1 Hour)

IF Not OnMarket THEN

ExitFlag = 0

ENDIF

If price crosses over Average [10] then

Buy 1 contract at Market

Endif

IF close >= (PositionPrice * 1.2) THEN

ExitFlag = 1 //Signal when current price reaches +20%

ENDIF

//Below condition is triggered when Daily MA tries to turn bullish and exit trade prematurely

If longonmarket and Dailyclose<MA AND ExitFlag then

Sell at market

Endif

I just added a flag to signal when exit is allowed (after reaching +20%) once it retraces below MA.