But this is not related to what’s odd today (in V11).

I meant to say : in V10.3.

Anyway, just use the code I first posted AS IS (you may change it at a later moment), but with the correct spelling, and don’t be afraid of using GRAPH:

// pl: 130 sl: 70 t & ts: 50 x: 1 = 3min 528$, 46,88W, 25% BE, 3.1 G/L ratio, 1,82 time in the market. 64 trades

DEFPARAM CumulateOrders = FALSE

//

ONCE x = 5

ONCE y = 1

ONCE LotSize = y

ONCE WinningTrades = 0

ONCE LosingTrades = 0

IF StrategyProfit > StrategyProfit[1] THEN

WinningTrades = WinningTrades + 1

IF WinningTrades >= x THEN

WinningTrades = 0

LotSize = y

ENDIF

ELSIF StrategyProfit < StrategyProfit[1] THEN

LosingTrades = LosingTrades + 1

IF LosingTrades >= x THEN

LosingTrades = 0

LotSize = LotSize + y

ENDIF

ENDIF

//

ONCE MaxTrades = x //no more than 2 trades a day

ONCE Tally = 0

IF IntraDayBarIndex = 0 THEN

Tally = 0

ENDIF

IF Not OnMarket THEN

MyExit = 0

ELSE

c1 = 0

ENDIF

//

once sl = 30

once pl = sl * 2

once adr = 30

once t = 10

once ts = t

////////////////////////////////////////////////////////////////////////////////////////////////////////////

NewTrade = (OnMarket AND Not OnMarket[1]) OR (LongOnMarket AND ShortOnMarket[1]) OR (LongOnMarket[1] AND ShortOnMarket) OR ((Not OnMarket AND Not OnMarket[1]) AND (StrategyProfit <> StrategyProfit[1]))

IF NewTrade THEN

Tally = Tally + 1

ENDIF

////////////////////////////////////////////////////////////////////////////////////////////////////////////

// ADR Average Daily Range

MyADR = average[20,0](Dhigh(1) - Dlow(1))

//

IF (Time = 000000) OR ((Time > 000000) AND (Time < Time[1])) THEN

MyHI = high

MyLO = low

c1 = 0

ENDIF

IF Time <= 142900 THEN

MyHI = max(MyHI,high)

MyLO = min(MyLO,low)

MyRange = MyHI - MyLO

c1 = ((MyRange / MyADR) * 100) < adr

ENDIF

IF LongOnMarket THEN

SET TARGET pPROFIT PL //you can change this value for LONG trades

SET STOP pLOSS SL //you can change this value for LONG trades

ELSIF ShortOnMarket THEN

SET TARGET pPROFIT PL //you can change this value for SHORT trades

SET STOP pLOSS SL //you can change this value for SHORT trades

ENDIF

IF Time >= 142900 AND Time <= 220000 AND c1 AND Tally < MaxTrades AND Not OnMarket THEN //trade only between 15:30 and 18:00

BUY LotSize Contract AT MyHI + 1 * pipsize STOP

SELLSHORT LotSize Contract AT MyLO - 1 * pipsize STOP

SET TARGET pPROFIT PL //initial values cannot be different with pending orders

SET STOP pLOSS SL

ENDIF

IF MyExit = 0 THEN

IF LongOnMarket AND (close - TradePrice) >= t * pipsize THEN //you can change this value for LONG trades

MyExit = TradePrice

ENDIF

IF ShortOnMarket AND (TradePrice - close) >= ts * pipsize THEN //you can change this value for SHORT trades

MyExit = TradePrice

ENDIF

ENDIF

IF MyExit > 0 THEN

IF LongOnMarket THEN

SELL AT MyExit STOP

ELSIF ShortOnMarket THEN

EXITSHORT AT MyExit STOP

ENDIF

ENDIF

graph LotSize

Here’s my take, based on the original snippet from Roberto.

Ulle, As far as I can see this should do what you want.

It is optimized on the TakeProfit and the StopLoss, and I would not use this in Live. Also, I made it a version for Short only, as this works out for the better (Long loses whatever I try within the mechanism).

ONCE x = 5

ONCE y = 1

ONCE LotSize = y

ONCE WinningTrades = 0

ONCE LosingTrades = 0

ONCE Spread = 1.5 // Nasdaq average of the day. Fill this at Backtest (Editor) start as well.

// These are (over-)optimized, so be careful :

ONCE TPA = 124

ONCE SLA = 66 // Set to 33 for a nice test.

IF StrategyProfit > StrategyProfit[1] THEN

WinningTrades = WinningTrades + 1

LosingTrades = 0 // Reset.

IF WinningTrades >= x THEN

WinningTrades = 0 // Start all over.

LotSize = y

ENDIF

ELSIF StrategyProfit < StrategyProfit[1] THEN

LosingTrades = LosingTrades + 1

WinningTrades = 0 // Reset.

IF LosingTrades >= x THEN

LotSize = LotSize + (y / 5) // = 0.2

LosingTrades = 0 // Start all over.

ENDIF

ENDIF

TP = TPA * LotSize

SL = SLA * LotSize

If Not OnMarket then

//Buy Lotsize Shares at Market // Long version.

SellShort Lotsize Shares at Market // Short version.

else

Gain = (PositionPerf * abs(countofposition) * TradePrice) - (Spread * CountOfPosition)

If Gain > TP then

//Sell at Market // Long version.

ExitShort at market // Short version.

else

If Gain < -SL then // Don't make too small or else no subsequent losses of x will occur.

//Sell at market // Long version.

ExitShort at market // Short version.

endif

endif

endif

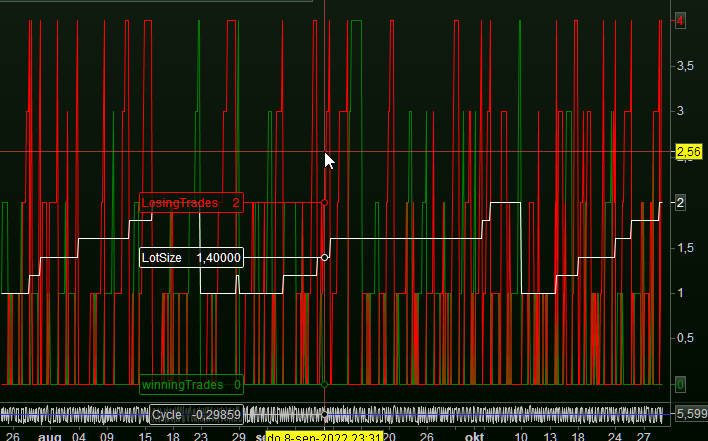

Graph winningTrades Coloured ("Green")

Graph LosingTrades Coloured ("Red")

Graph LotSize Coloured ("White")

Use this on Nasdaq (Tech 100), Contract size of 1 euro.

Timeframe 1 minute.

Load 100K bars.

The problem with this idea – at least how I see it – is that the subsequent losses form the mechanism, while the subsequent losses only form (really emerge) at the lower SL which implies losing because of the Spread. And thus the SL must be higher than the mechanism desires, and next the mechanism doesn’t work well.

Have fun now !