Hi Folks

I’m moving on from my basic breakout indicator to try and code a simple trend following system with some ATR inputs for risk sizing and profit taking.

The system should trade the Daily TF of xxx FX pair. The rules are quite simple.

Long

21ema >63ema AND Carver 1 indicator >0 AND price is greater than previous day’s close

Short

21ema <63ema AND Carver 1 Indicator <0 AND price is lower than previous day’s close

I’m getting a infinite loop error so any help would be appreciated! Also any other glaring code errors you see would be insightful!

I have placed the indicator code for Carver 1 below the Pro Real Code.

defparam cumulateorders=false

// --- settings

balance = 10000 //balance of the strategy when activated the first time

minlot = 1 //minimum lot size for the current instrument (example: 1 for DAX)

riskpercent = 2 //risk percent per trade

//activationtime = 220000//Close time of the candle to activate the strategy

//LimitHour = 130000 //Time to close off strategy

if dayofweek=1 then //Monday

daytrading=1

endif

if dayofweek=2 then // Tuesday

daytrading=1

endif

if dayofweek=3 then // Wednesday

daytrading=1

endif

if dayofweek=4 then //Thursday

daytrading=1

endif

if dayofweek=5 then // Friday

daytrading=0

endif

if dayofweek=6 or dayofweek=7 then //Sat and Sun

daytrading=0

endif

//-- indicators

ema = exponentialaverage[63](close)

ema2 = exponentialaverage[21](close)

EMAabove = ema2>ema

EMAbelow = ema2<ema

atr = averagetruerange[24]

hh = highest[1](high)+1

ll = lowest[1](low)-1

//set Breakout

LongBO = CALL"Carver 1"[close >0.01]

ShortBO= CALL"Carver 1"[close <0.00]

Long = emaabove and LongBO

Short = emabelow and ShortBO

if intradaybarindex=0 then

alreadytraded = 0

case = 0

levelhi = 0

levello = 0

endif

if onmarket or (onmarket[1] and not onmarket) or (currentprofit<>strategyprofit) then

alreadytraded = 1

endif

//if time=activationtime then

// case 1 : If price candle touches MA (even wicks) then look at high or low of signal candle

if high>ema and low<ema then

case = 1

levelhi = CALL"#floor and ceil"[high,10.0,1]

levello = CALL"#floor and ceil"[low,10.0,-1]

endif

//case 2 : If price is above the MA then only trade long BUT only above the highest high of the past 24 hrs

if close >ema and long and case = 0 then

case = 2

levelhi = hh[1]

endif

//case 3 : If price is below the MA then only trade short BUT only below the lowest low of the past 24 hrs

if close <ema and short and case = 0 then

case = 3

levello = ll[1]

endif

//endif

if alreadytraded = 0 then

//money management

if case=1 then

daytrading=0

else

StopLoss = 1*ATR

endif

Risk = riskpercent/100

//calculate contracts

equity = balance + StrategyProfit

maxrisk = round(equity*Risk)

size = max(minlot,abs(round((maxrisk/StopLoss)/PointValue)*pipsize))

//in all cases put pending orders on market

while case <> 0 and daytrading=1 do //(time >= activationtime and time <=LimitHour) do

if levelhi>0 then

buy size contract at levelhi stop

endif

if levello>0 then

sellshort size contract at levello stop

endif

wend

endif

// Friday 22:00 Close ALL operations.

IF onmarket and (DayOfWeek = 5 AND time >= 220000) THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

//set target and profit

if case = 1 then

daytrading=0

endif

if case = 2 or case = 3 then

set target profit 1.4*ATR

set stop loss StopLoss

endif

currentprofit = strategyprofit

//debugging

//graph case as "case"

//graph time=activationtime coloured(100,120,133) as "activation time!"

//graph time

//graph ema

//graph levelhi coloured(0,200,0) as "level high"

//graph levello coloured(200,0,0) as "level low"

//graph size as "mm"

n=21

a = highest[n](high[0])

b = lowest[n](low[0])

c = (a+b)/2

scaledprice = (close-c)/(a-b)

zero =0

return scaledprice as "scaled price"

Because there is indeed an infinite loop! You are creating it at line 89, once the loop is started you are waiting in it that the “case” variable change, while it can’t since there is no instruction to change it in the loop! 🙂

Anyway, there is no need to use loop there, just replace the WHILE/WEND instructions with a IF/ENDIF block.

Try replacing line 89 with:

while Xcase <> 0 and daytrading=1 and not OnMarket do

add this line before line 89:

xCase = case

and add this line just before line 95 (wend):

xCase = 0

this could trick ProOrder into thinking the loop is not infinite (not tested)

Super thanks Guys – that’s got rid of the Infinite Loop. I have tidied up the code too but alas it’s not taking any trades in the backtest? I have adapted this from a code that is working. Is there something the code is missing or not doing? It should only trade on the daily TF?

Thanks

defparam cumulateorders=false

// --- settings

balance = 10000 //balance of the strategy when activated the first time

minlot = 1 //minimum lot size for the current instrument (example: 1 for DAX)

riskpercent = 2 //risk percent per trade

//settings for days to trade

if dayofweek=1 then //Monday

daytrading=1

endif

if dayofweek=2 then // Tuesday

daytrading=1

endif

if dayofweek=3 then // Wednesday

daytrading=1

endif

if dayofweek=4 then //Thursday

daytrading=1

endif

if dayofweek=5 then // Friday

daytrading=1

endif

if dayofweek=6 or dayofweek=7 then //Sat and Sun

daytrading=0

endif

//-- indicators

//emas

ema = exponentialaverage[21](close)

ema2 = exponentialaverage[63](close)

EMAabove = ema2>ema

EMAbelow = ema2<ema

//ATR

atr = averagetruerange[24]

//Highest/lowest candle

hh = highest[1](high)+1

ll = lowest[1](low)-1

//set Breakout

LongBO = CALL"Carver 1"[close >0.01]

ShortBO= CALL"Carver 1"[close <0.00]

//Trade entry rules

Long = emaabove and LongBO

Short = emabelow and ShortBO

if intradaybarindex=0 then

alreadytraded = 0

case = 0

levelhi = 0

levello = 0

endif

if onmarket or (onmarket[1] and not onmarket) or (currentprofit<>strategyprofit) then

alreadytraded = 1

endif

//case 2 : If price is above the MA then only trade long BUT only above the highest high of the past 24 hrs

if close >ema and long and case = 0 then

case = 2

levelhi = hh[1]

endif

//case 3 : If price is below the MA then only trade short BUT only below the lowest low of the past 24 hrs

if close <ema and short and case = 0 then

case = 3

levello = ll[1]

endif

//endif

XCase=case

if alreadytraded = 0 then

//money management

//if case=1 then

//daytrading=0

//else

StopLoss = 1*ATR

endif

//Risk Setting

Risk = riskpercent/100

//calculate contracts

equity = balance + StrategyProfit

maxrisk = round(equity*Risk)

size = max(minlot,abs(round((maxrisk/StopLoss)/PointValue)*pipsize))

//in all cases put pending orders on market

while Xcase <> 0 and daytrading=1 and not OnMarket do //(time >= activationtime and time <=LimitHour) do

if levelhi>0 then

buy size contract at levelhi stop

endif

if levello>0 then

sellshort size contract at levello stop

endif

xCase=0

wend

// Friday 22:00 Close ALL operations.

IF onmarket and (DayOfWeek = 5 AND time >= 220000) THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

//set target and profit

if case = 2 or case = 3 then

set target profit 1.4*ATR

set stop loss StopLoss

endif

currentprofit = strategyprofit

//debugging

//graph case as "case"

//graph time=activationtime coloured(100,120,133) as "activation time!"

//graph time

//graph ema

//graph levelhi coloured(0,200,0) as "level high"

//graph levello coloured(200,0,0) as "level low"

//graph size as "mm"

I cannot test it because I don’t have the indicator you are using, but I want to remark that lines 35-36 could be logically incorrect. I don’t know what you want to achieve with those two lines, but, despite what they look like, they could be easily written as:

hh = high+1

ll = low-1

or (as I encourage you to do, to make your code portable to all instruments):

hh = high + 1*pipsize

ll = low - 1*pipsize

Rightly or wrongly 🙂 … I got it going and I left Line 35 and 36 as original (for now anyway).

.itf attached

I’m interested so please post any improvements. I will post same also.

Thanks GraHal – I actually got it working. I changed the code to that of what Robert suggested at lines 35 and 36.

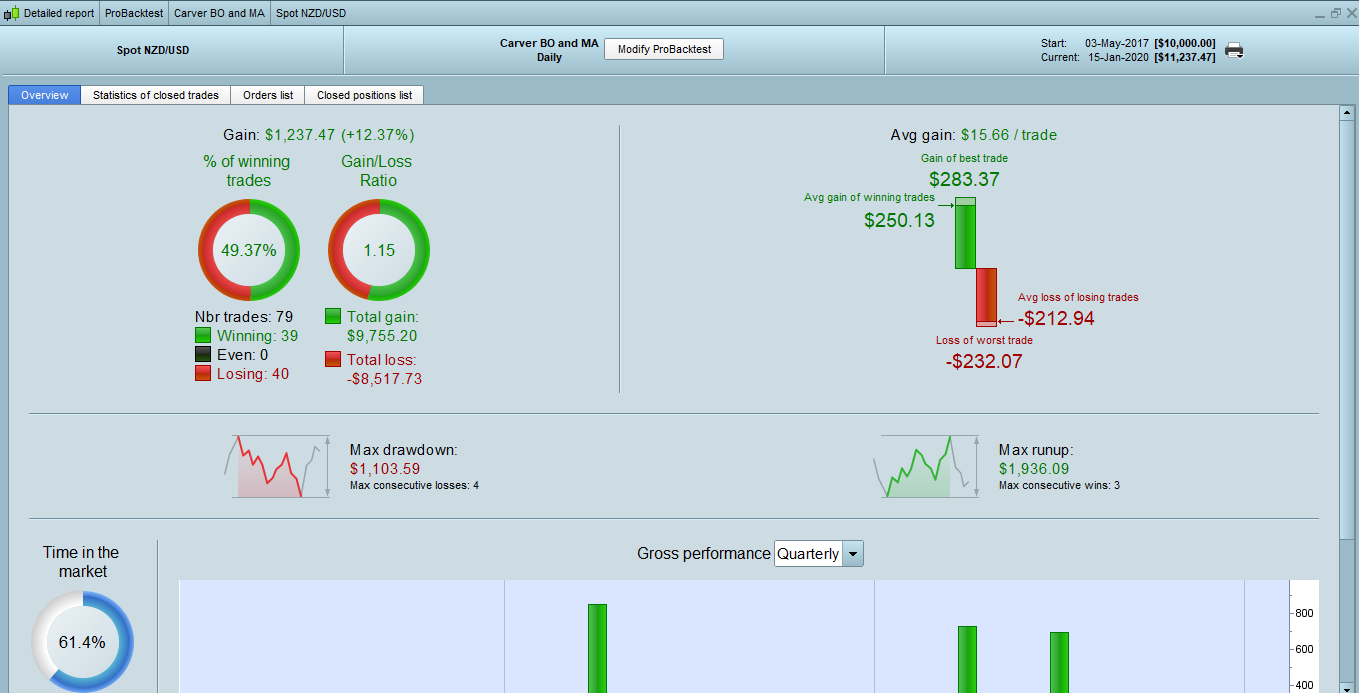

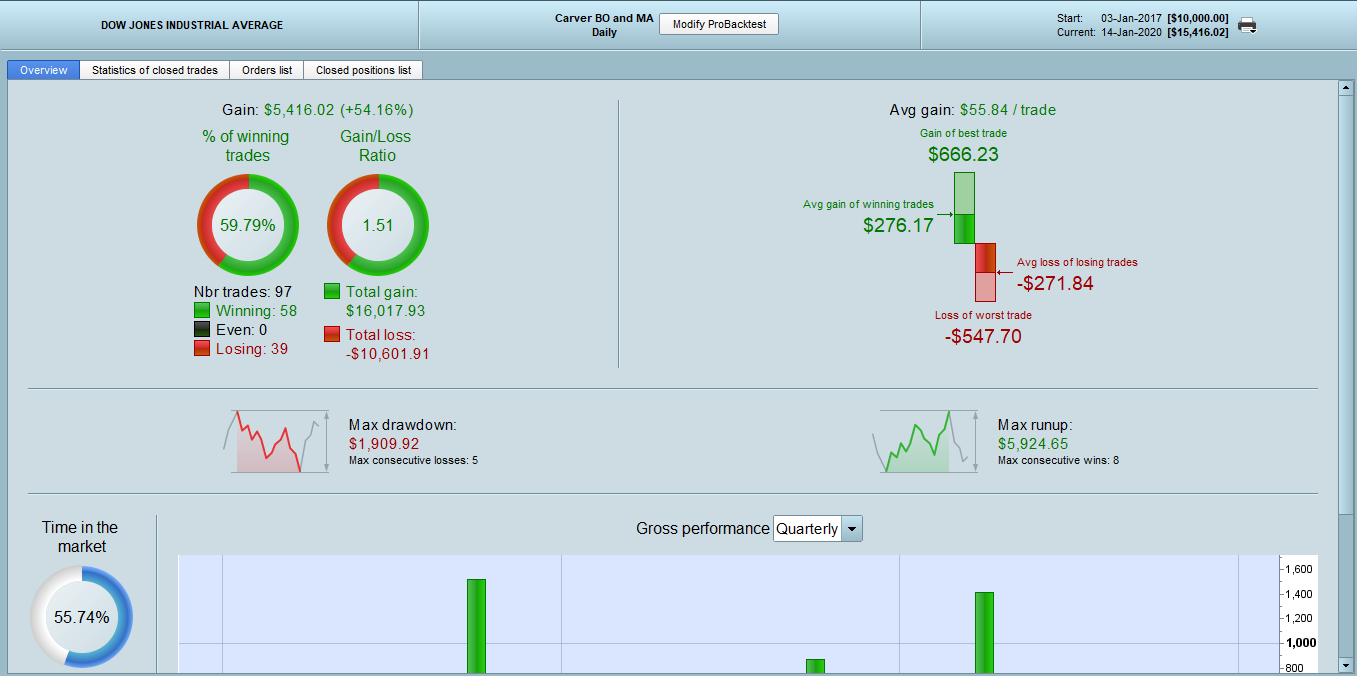

There are a couple of tweaks that I think are worthy of testing. Limiting the profits with a trend system based on ATR could be counter-productive as one needs to collect maximum rent from the trends that keep going. Would it be better to implement a trailing stop as Carver suggests?

Also, when calling an indicator how can we ‘test’ for differing lengths in Carver 1? Carver conducted extensive back testing in his book and the best lengths for Carver 1 are 10,20,40,80,160 and 320. When calling an indicator does it use the value on the chart being tested? Can it be changed in the code (ie tested under an ‘n’ variable)?

Also, this system doesn’t add on. Carver recommends taking a ‘nibble’ at the first entry signal and then scaling in, protecting profits with a trailing stop. Could this be added to the code as it’s a little beyond my capabilities.

I have also added a 10ema to the Carver 1- the reason being I only want to initiate a trade (long) if Carver 1 is >0 but ALSO >10ema to prove value is not falling.

I don’t want to complicate the system as that goes against the simplicity of a trend breakout system. Many of the big hedge funds will tell you that overly complex systems that backtest well will nearly always fail in real markets. The fewer rules, the better the expected Sharpe Ratio of the system. To increase the Sharpe you are better adding more markets than more trading rules – you achieve a much better payoff!

defparam cumulateorders=false

// --- settings

balance = 10000 //balance of the strategy when activated the first time

minlot = 1 //minimum lot size for the current instrument (example: 1 for DAX)

riskpercent = 2 //risk percent per trade

//settings for days to trade

if dayofweek=1 then //Monday

daytrading=1

endif

if dayofweek=2 then // Tuesday

daytrading=1

endif

if dayofweek=3 then // Wednesday

daytrading=1

endif

if dayofweek=4 then //Thursday

daytrading=1

endif

if dayofweek=5 then // Friday

daytrading=1

endif

if dayofweek=6 or dayofweek=7 then //Sat and Sun

daytrading=0

endif

//-- indicators

//emas

ema = exponentialaverage[63](close)

ema2 = exponentialaverage[21](close)

EMAabove = ema2>ema

EMAbelow = ema2<ema

//ATR

atr = averagetruerange[24]

//Highest/lowest candle

hh = high + 1*pipsize

ll = low - 1*pipsize

//set Breakout

MA= CALL"Carver 1"[exponentialaverage[10](close)]

LongBO = CALL"Carver 1"[close >0.01 and close > MA]

ShortBO= CALL"Carver 1"[close <-0.01 and close < MA]

//Trade entry rules

Long = emaabove and LongBO

Short = emabelow and ShortBO

if intradaybarindex=0 then

alreadytraded = 0

case = 0

levelhi = 0

levello = 0

endif

if onmarket or (onmarket[1] and not onmarket) or (currentprofit<>strategyprofit) then

alreadytraded = 1

endif

//case 2 : If price is above the MA then only trade long BUT only above the highest high of the past 24 hrs

if close >ema and long and case = 0 then

case = 2

levelhi = hh[1]

endif

//case 3 : If price is below the MA then only trade short BUT only below the lowest low of the past 24 hrs

if close <ema and short and case = 0 then

case = 3

levello = ll[1]

endif

//endif

XCase=case

if alreadytraded = 0 then

//money management

//if case=1 then

//daytrading=0

//else

StopLoss = 1.4*ATR

endif

//Risk Setting

Risk = riskpercent/100

//calculate contracts

equity = balance + StrategyProfit

maxrisk = round(equity*Risk)

size = max(minlot,abs(round((maxrisk/StopLoss)/PointValue)*pipsize))

//in all cases put pending orders on market

while Xcase <> 0 and daytrading=1 and not OnMarket do //(time >= activationtime and time <=LimitHour) do

if levelhi>0 then

buy size contract at levelhi stop

endif

if levello>0 then

sellshort size contract at levello stop

endif

xCase=0

wend

// Friday 22:00 Close ALL operations.

IF onmarket and (DayOfWeek = 5 AND time >= 220000) THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

//set target and profit

if case = 2 or case = 3 then

set target profit 1.7*ATR

set stop loss stoploss

endif

currentprofit = strategyprofit

//debugging

//graph case as "case"

//graph time=activationtime coloured(100,120,133) as "activation time!"

//graph time

//graph ema

//graph levelhi coloured(0,200,0) as "level high"

//graph levello coloured(200,0,0) as "level low"

//graph size as "mm"

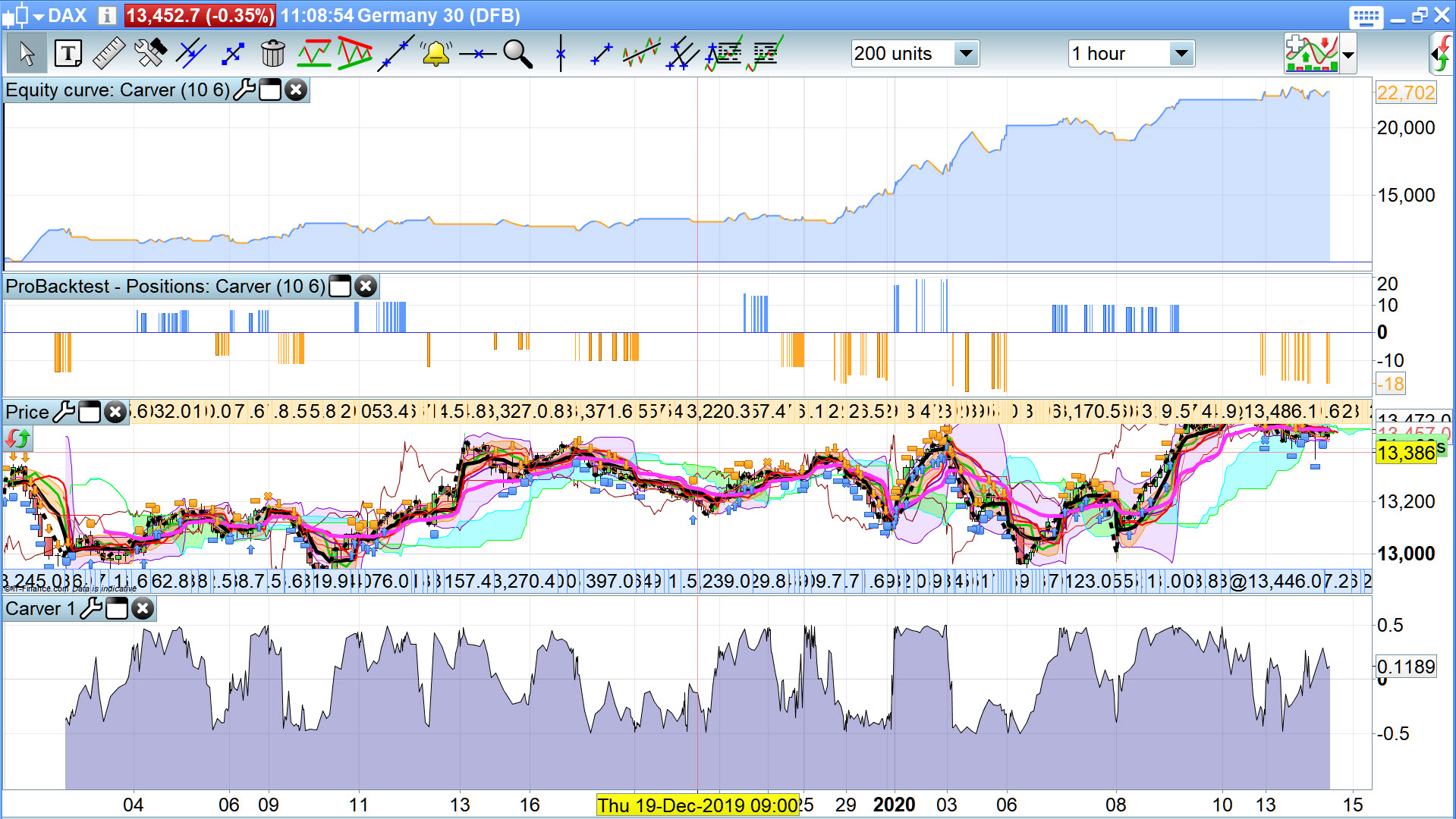

Ok, so I have added a Trailing stop to the code and the changes to the system (DAX anyway) seem impressive. I backtested in 50% of the data available and then did WF analysis on the other half of the data, and came out with around the same results of 60% winning trades and Gain/Loss of 6.4 times

Since this seems too good to be true I wonder what I’m missing? I also added spread of 1.5

I’ve used ATR of 21 and also the 21ema and 63ema (3x this as one business quarter) as I know from my time in the City, that the ‘machine’ (algos) at many CTA/Hedge funds are mainly interested in 1 month momentum.

defparam cumulateorders=false

// --- settings

balance = 10000 //balance of the strategy when activated the first time

minlot = 1 //minimum lot size for the current instrument (example: 1 for DAX)

riskpercent = 2 //risk percent per trade

//settings for days to trade

if dayofweek=1 then //Monday

daytrading=1

endif

if dayofweek=2 then // Tuesday

daytrading=1

endif

if dayofweek=3 then // Wednesday

daytrading=1

endif

if dayofweek=4 then //Thursday

daytrading=1

endif

if dayofweek=5 then // Friday

daytrading=1

endif

if dayofweek=6 or dayofweek=7 then //Sat and Sun

daytrading=0

endif

//-- indicators

//emas

ema = exponentialaverage[63](close)

ema2 = exponentialaverage[21](close)

EMAabove = ema2>ema

EMAbelow = ema2<ema

//ATR

atr = averagetruerange[21]

//Highest/lowest candle

hh = high+1*pipsize

ll = low-1*pipsize

//set Breakout

MA= CALL"Carver 1"[exponentialaverage[10](close)]

LongBO = CALL"Carver 1"[close >0.01 and close > MA]

ShortBO= CALL"Carver 1"[close <-0.01 and close < MA]

//Trade entry rules

Long = emaabove and LongBO

Short = emabelow and ShortBO

if intradaybarindex=0 then

alreadytraded = 0

case = 0

levelhi = 0

levello = 0

endif

if onmarket or (onmarket[1] and not onmarket) or (currentprofit<>strategyprofit) then

alreadytraded = 1

endif

//case 2 : If price is above the MA then only trade long BUT only above the highest high of the past 24 hrs

if long and close >ema and case = 0 then

case = 2

levelhi = hh[1]

endif

//case 3 : If price is below the MA then only trade short BUT only below the lowest low of the past 24 hrs

if short and close < ema and case = 0 then

case = 3

levello = ll[1]

endif

//endif

XCase=case

if alreadytraded = 0 then

//money management

//if case=1 then

//daytrading=0

//else

StopLoss = 1.4*ATR

endif

//Risk Setting

Risk = riskpercent/100

//calculate contracts

equity = balance + StrategyProfit

maxrisk = round(equity*Risk)

size = max(minlot,abs(round((maxrisk/StopLoss)/PointValue)*pipsize))

//in all cases put pending orders on market

while Xcase <> 0 and daytrading=1 and not OnMarket do //(time >= activationtime and time <=LimitHour) do

if levelhi>0 then

buy size contract at levelhi stop

endif

if levello>0 then

sellshort size contract at levello stop

endif

xCase=0

wend

// Friday 22:00 Close ALL operations.

IF onmarket and (DayOfWeek = 5 AND time >= 220000) THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

//set target and profit

if case = 2 or case = 3 then

set target profit 10*ATR

set stop loss stoploss trailing ATR*0.2

endif

currentprofit = strategyprofit

//debugging

//graph case as "case"

//graph time=activationtime coloured(100,120,133) as "activation time!"

//graph time

//graph ema

//graph levelhi coloured(0,200,0) as "level high"

//graph levello coloured(200,0,0) as "level low"

//graph size as "mm"

Wow! Looks great … you are flying man!! 🙂

What did you do in the City? Good to have an ex Gordon Gekko on board!! 🙂

Haha that’s why I think the backtest is throwing up bad results!

Just worked at NYSE Euronext for a year (which is why I think most lower TF trading is pointless as the Algos have all those timeframes sewn-up – they will always be quicker, have co-location with the matching engines etc). Then worked in Private Wealth mostly since…

which is why I think most lower TF trading is pointless

Finally someone who thinks like I do!

Hi Grimweasel,

Thanks for sharing your strategy but I cannot test it as the Indicator “Carver 1” doesn’t work.

n=21

a = highest[n](high[0])

b = lowest[n](low[0])

c = (a+b)/2

scaledprice = (close-c)/(a-b)

zero =0

return scaledprice as "scaled price"

it seems there is a problem with zero ?

Can you check ? Thanks in advance

Hi Lifen

Sorry I’m not sure why? Did you create the indicator and place into your local library and charts, otherwise the call function won’t work? The code is exactly as I have added to my chart.

@Lifen comment out (with //) zero=0 as it is not used anyway??

When i try to run the strategy the system says: The “Carver 1″ function retrieved from the strategy is named with 1 parameter instead of 0 expected”